Bhubaneswar🌹Kalpana Mesuem ❤CALL GIRLS 9777949614 💟 CALL GIRLS IN bhubaneswa...

India’s Economy Is On The Mend

1. Page 1 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

May 11, 2014

India’s Economy Is On The Mend

Although not yet out of the woods, the Indian

economy is on the mend. The IMF expects the

Indian real GDP growth to recover to 5.4% this

year (4.4% in 2013, the lowest in 5 years),

bolstered by a rebound in agriculture and

stronger exports and government reforms.

However, lingering imbalances and structural

impediments are still holding back a full

recovery. The ongoing parliamentary elections

mark a cross-roads to the current program of

reforms needed to sustain stronger growth. Of

critical importance will be how the new

leadership will tackle the lack of infrastructure

investment and structural reforms whilst

attempting at the same time to keep the

current account and fiscal deficits in check.

Following robust annual average growth of

over 9.0% during 2004-07 spurred by a rapid

expansion of services and commerce, the

Indian economy suffered a slowdown with the

onset of the global financial crisis of 2008-09,

with real GDP growth falling to an average

6.2%. Growth did rebound initially between

2010-11 in response to large fiscal and

monetary stimulus but subsequently slowed

down markedly, reflecting weak global

demand and slow progress on key structural

reforms. Led by weaker corporate investment

growth with deteriorating asset quality

impacting the financial positions of banks and

corporates, the slowdown had ripple effects

throughout the economy between 2012-13.

The balance of payment pressures intensified

severely last summer. The announcement that

the US Federal Reserve would begin tapering

its quantitative easing program in May 2013

resulted in large capital outflows with

downward pressures on the currency and asset

prices. India was one of the main emerging

market countries affected due to its heavy

reliance on capital inflows to finance its large

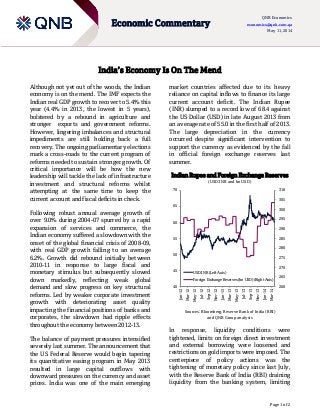

current account deficit. The Indian Rupee

(INR) slumped to a record low of 68.4 against

the US Dollar (USD) in late August 2013 from

an average rate of 55.0 in the first half of 2013.

The large depreciation in the currency

occurred despite significant intervention to

support the currency as evidenced by the fall

in official foreign exchange reserves last

summer.

Indian Rupee and Foreign Exchange Reserves

(USD:INR and bn USD)

Sources: Bloomberg, Reserve Bank of India (RBI)

and QNB Group analysis

In response, liquidity conditions were

tightened, limits on foreign direct investment

and external borrowing were loosened and

restrictions on gold imports were imposed. The

centerpiece of policy actions was the

tightening of monetary policy since last July,

with the Reserve Bank of India (RBI) draining

liquidity from the banking system, limiting

260

265

270

275

280

285

290

295

300

305

310

40

45

50

55

60

65

70

Jan-12

Mar-12

May-12

Jul-12

Sep-12

Nov-12

Jan-13

Mar-13

May-13

Jul-13

Sep-13

Nov-13

Jan-14

Mar-14USD:INR (Left Axis)

Foreign Exchange Reserves (bn USD) (Right Axis)

2. Page 2 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

May 11, 2014

access to borrowing from its discount windows

and hiking short-term interest rates. In

addition, limits on foreign investments and

external commercial borrowing in foreign

currency were eased in order to allow more

capital inflows. Moreover, higher import duties

and quantitative restrictions on gold were

implemented to reduce the overall import bill.

As a result, the current account deficit has

narrowed, helped also by robust remittance

flows, and the INR has appreciated.

This strong domestic policy response has also

helped calm markets and bolster investor

sentiment. The parliament has passed the

Land Acquisition, Pension and Companies

Acts, which is expected to unleash previously

stalled public projects worth around 5% of

GDP. On the fiscal front, measures have been

implemented to raise diesel prices, shrink the

financial losses of the state electricity board

and to contain central government spending.

Going forward, against the background of

parliamentary elections due to be completed

by mid-May and prospective global liquidity

tightening, the new administration coming to

power will face a number of key economic

reform challenges. At the top of the agenda is

addressing infrastructure investment gaps and

supply-side constraints. In particular,

electricity shortages and an inadequate

transportation system need to be tackled in

the short term. Over the medium term, further

fiscal consolidation is needed, particularly tax

and subsidy reforms to lower fiscal

imbalances. In addition, more effective

education and health spending will be critical

to ensure that the demographic dividend pays

off over the long run. Finally, addressing

structural challenges in agriculture as well as

in the pricing and allocation of natural

resources will be essential to achieve faster

growth and higher job creation.

Overall, stronger global growth, improving

export competitiveness, measures already

underway to advance stalled infrastructure

projects and a confidence boost from recent

policy actions are likely to result in a moderate

growth recovery over the medium term.

However, further structural reforms in the

areas of electricity and transportation, fiscal

consolidation, education and health spending,

and the pricing of natural resources are needed

in order for India to achieve its full growth

potential.

Contacts

Joannes Mongardini

Head of Economics

Tel. (+974) 4453-4412

Rory Fyfe

Senior Economist

Tel. (+974) 4453-4643

Ehsan Khoman

Economist

Tel. (+974) 4453-4423

Hamda Al-Thani

Economist

Tel. (+974) 4453-4646

Ziad Daoud

Economist

Tel. (+974) 4453-4642

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.