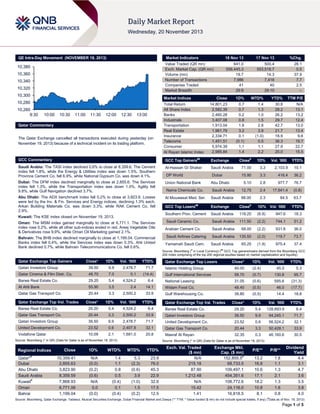

1. QE Intra-Day Movement (NOVEMBER 18, 2013)

Market Indicators

10,380

10,360

10,340

10,320

10,300

17 Nov 13

%Chg.

641.0

556,445.3

19.7

7,986

41

29:9

500.4

553,518.7

14.3

7,418

40

29:10

28.1

0.5

37.9

7.7

2.5

–

Market Indices

10,280

10,260

9:30

18 Nov 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The Qatar Exchange cancelled all transactions executed during yesterday (on

November 19, 2013) because of a technical incident on its trading platform.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,801.23

2,582.39

2,460.28

3,407.08

1,913.04

1,961.79

2,334.71

1,451.51

5,974.39

2,985.84

0.7

0.7

0.2

0.8

1.8

3.2

0.1

(0.1)

1.1

1.4

1.4

1.3

1.0

1.5

2.8

3.9

(1.0)

0.5

1.1

2.2

30.8

28.2

26.2

29.7

42.7

21.7

18.9

36.3

27.9

20.0

N/A

13.1

13.2

12.4

13.0

13.4

9.6

19.7

22.7

15.5

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index declined 0.6% to close at 8,359.6. The Cement

index fell 1.8%, while the Energy & Utilities index was down 1.5%. Southern

Province Cement Co. fell 6.9%, while National Gypsum Co. was down 4.1%.

Al-Hassan GI Shaker

Dubai: The DFM index declined marginally to close at 2,855.6. The Services

index fell 1.3%, while the Transportation index was down 1.0%. Agility fell

9.8%, while Gulf Navigation declined 3.7%.

Abu Dhabi: The ADX benchmark index fell 0.2% to close at 3,823.9. Losses

were led by the Inv. & Fin. Services and Energy indices, declining 1.3% each.

Arkan Building Materials Co. was down 3.3%, while RAK Cement Co. fell

2.9%.

Kuwait: The KSE index closed on November 19, 2013.

Oman: The MSM index gained marginally to close at 6,771.1. The Services

index rose 0.2%, while all other sub-indices ended in red. Areej Vegetable Oils

& Derivatives rose 9.9%, while Oman Oil Marketing gained 2.1%.

Bahrain: The BHB index declined marginally to close at 1,199.04. Commercial

Banks index fell 0.4%, while the Services index was down 0.3%. Ahli United

Bank declined 0.7%, while Bahrain Telecommunications Co. fell 0.6%.

Close#

1D%

Saudi Arabia

71.00

3.3

2,103.9

10.1

DP World

Dubai

15.90

3.3

416.4

36.2

Union National Bank

Abu Dhabi

5.10

2.8

977.7

76.7

Nama Chemicals Co.

Saudi Arabia

12.75

2.4

17,641.4

(0.8)

Al Mouwasat Med. Ser.

Saudi Arabia

88.00

2.3

84.5

63.7

##

#

Vol. ‘000

YTD%

GCC Top Losers

Exchange

Close

1D% Vol. ‘000

Southern Prov. Cement

Saudi Arabia

118.25

(6.9)

947.6

18.3

Saudi Ceramic Co.

Saudi Arabia

111.50

(2.2)

744.1

51.2

Arabian Cement Co.

Saudi Arabia

68.00

(2.2)

931.8

36.0

Saudi Airlines Catering

Saudi Arabia

135.50

(2.0)

119.7

73.7

Yamamah Saudi Cem.

Saudi Arabia

65.25

(1.9)

975.4

37.4

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Qatari Investors Group

39.50

9.9

2,478.7

71.7

Qatar Cinema & Film Distr. Co.

48.70

7.0

0.1

(14.4)

Barwa Real Estate Co.

29.20

5.4

4,524.2

Al Ahli Bank

55.90

3.5

2.4

Qatar Gas Transport Co.

20.44

3.3

2,500.2

33.9

Qatar Exchange Top Gainers

Close*

1D%

Vol. ‘000

Islamic Holding Group

40.00

(2.4)

45.5

5.3

Gulf International Services

58.70

(0.7)

130.8

95.7

6.4

National Leasing

31.05

(0.6)

595.6

(31.3)

14.1

Widam Food Co.

48.40

(0.5)

46.0

(17.7)

Gulf Warehousing Co.

39.80

(0.5)

14.4

18.8

YTD%

Qatar Exchange Top Losers

YTD%

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

Barwa Real Estate Co.

29.20

5.4

4,524.2

6.4

Barwa Real Estate Co.

29.20

5.4

128,893.9

6.4

Qatar Gas Transport Co.

20.44

3.3

2,500.2

33.9

Qatari Investors Group

39.50

9.9

94,245.1

71.7

Qatari Investors Group

39.50

9.9

2,478.7

71.7

United Development Co.

23.52

0.6

56,524.2

32.1

United Development Co.

23.52

0.6

2,407.8

32.1

Qatar Gas Transport Co.

20.44

3.3

50,428.1

33.9

Vodafone Qatar

10.09

2.1

1,681.0

20.8

Masraf Al Rayan

32.35

0.3

46,160.6

30.5

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR) (Data for Qatar is as of November 18, 2013)

Regional Indices

Qatar*#

Dubai

Abu Dhabi

Saudi Arabia

Kuwait#

Oman

Bahrai

Qatar Exchange Top Val. Trades

Source: Bloomberg (* in QR) (Data for Qatar is as of November 18, 2013)

Close

1D%

WTD%

MTD%

YTD%

10,359.41

2,855.63

3,823.90

8,359.59

7,868.93

6,771.06

1,199.04

N/A

(0.0)

(0.2)

(0.6)

N/A

0.0

(0.0)

1.4

1.1

0.8

0.5

(0.4)

0.1

(0.4)

5.3

(2.3)

(0.6)

3.9

(1.0)

1.5

(0.2)

23.9

76.0

45.3

22.9

32.6

17.5

12.5

Exch. Val. Traded

($ mn)

N/A

215.18

87.90

1,212.48

N/A

15.42

1.41

Exchange Mkt.

Cap. ($ mn)

152,855.5#

68,733.5

109,497.1

454,351.6

108,772.6

24,116.0

16,818.5

P/E**

P/B**

13.2

16.8

10.6

17.1

18.2

10.8

8.1

1.8

1.1

1.3

2.1

1.3

1.6

0.8

Dividend

Yield

4.4

3.1

4.7

3.6

3.5

3.8

4.0

#

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as of Nov. 18, 2013)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.7% to close at 10,359.4. The Real Estate

and Transportation indices led the gains. The index rose on the

back of buying support from non-Qatari shareholders despite

selling pressure from Qatari shareholders.

Qatari Investors Group and Qatar Cinema & Film Distr. Co. were

the top gainers, rising 9.9% and 7.0% respectively. Among the

top losers, Islamic Holding Group fell 2.4%, while Gulf

International Services declined 0.7%.

Overall Activity#

Buy %*

Sell %*

Net (QR)

Qatari

73.89%

78.87%

(31,926,727.26)

Non-Qatari

26.11%

21.12%

31,926,727.26

#

Source: Qatar Exchange (* as a % of traded value) ( Data as of November 18, 2013)

Volume of shares traded on Monday rose by 37.9% to 19.7mn

from 14.3mn on Sunday. Further, as compared to the 30-day

moving average of 8.0mn, volume for the day was 147.1%

higher. Barwa Real Estate Co. and Qatar Gas Transport Co.

were the most active stocks, contributing 23.0% and 12.7% to

the total volume respectively.

Ratings, Earnings and Global Economic Data

Ratings Updates

Company

Agency

National Bank of

Bahrain (NBB)

CI

Market

Bahrain

Type*

Old Rating

LT FCR/ ST FCR

New Rating

Outlook

Outlook Change

BBB/ A2

BBB+/ A2

Rating Change

Stable

–

#

Source: News reports (* LT – Long Term, ST – Short Term, FCR – Foreign Credit Rating) (#Rating downgrade for LT FCR)

Earnings Releases

Company

Revenue

(mn) 3Q2013

% Change

YoY

Operating Profit

(mn) 3Q2013

% Change

YoY

Net Profit (mn)

3Q2013

% Change

YoY

KD

3.7

-41.4%

–

–

0.9

N/A

USD

98.8

22.0%

–

–

–

–

Market

International Financial

Advisors (IFA)

Topaz Energy and Marine

Currency

Kuwait

Oman

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

11/19

Germany

ZEW

ZEW Survey Expectations

November

11/19

Germany

ZEW

Consensus

Previous

60.2

–

59.1

November

ZEW Survey Expectations

Actual

54.6

54.0

52.8

–

2.2%

–

1.0%

11/19

Italy

Istat

Industrial Orders MoM

September

1.6%

11/19

Italy

Istat

Industrial Sales MoM

September

0.1%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QE cancels day's trade due to technical incident – The Qatar

Exchange cancelled all executed transactions yesterday

(November 19, 2013) because of a technical incident on its

trading platform. The exchange said after consultation with the

Qatar Financial Markets Authority, it has agreed to cancel all

transactions that took place on November 19 and any other

orders that had not been executed. (QE, Reuters)

DHBK to raise capital via private placement or bonds;

opens office in Sharjah – Doha Bank’s (DHBK) CEO

Raghavan Seetharaman said the bank is planning to raise its

capital via private placement or bonds. He added that depending

on market conditions, DHBK will either opt for a private

placement or bond issuance. He also said that DHBK is

planning to expand its capital by QR2bn within this year

(deadline is end-1Q2014, EOGM to be held on Nov. 24, 2013)

and seeks approval for a $549mn perpetual bond issue.

Meanwhile, the bank has opened its first representative office in

Sharjah, following regulatory approval from the UAE Central

Bank. (Bloomberg, Gulf-Times.com)

GISS updates investors on Al Koot – Gulf International

Services Company (GISS) has confirmed that discussions

regarding change of ownership of Al Koot (wholly-owned

insurance and reinsurance firm) have been put indefinitely on

hold. Hence, no major change is expected in the company

structure or in its operation. (QE)

Doha Metro works begin at several sites – Construction work

has begun at a number of project sites of the Doha Metro and

Rail network. The initial work of clearing, fencing and drilling

studies is being set in motion at several station locations

including Al Sadd, next to Toyota Tower, and in front of

Sheraton Hotel in Dafna. Work has also started at a few other

sites including the Sports City in Al Waab, Souq Waqif and the

Diwan. Drilling work has commenced at 20 station locations.

(Qatar Tribune)

Qatar has the lowest break-even oil price in region –

According to Moody’s, Qatar has the lowest break-even oil price

in the Gulf region. Furthermore, Qatar’s vast oil and gas

resources, robust non-hydrocarbon growth, a high per capita

income, and persistent surpluses in fiscal and external accounts

support its highest sovereign ratings. (Gulf-Times.com)

Qatari government to audit all state entities and projects –

The Qatari government has placed all institutions and projects

that receive its financing, as well as overseas investments made

by the sovereign wealth fund under its audit agency, the State

Audit Bureau (SAB). (Peninsula Qatar)

Page 2 of 5

3. Ministry to issue new specifications for building materials –

The Laboratory and Standardization Department at the Ministry

of Environment said that it will issue a new set of specifications

for construction materials in Qatar by early 2014. The new

specifications will be mandatory for all companies. (Peninsula

Qatar)

PetroChina’s new LNG terminal gets first cargo from

Qatargas – Qatargas has delivered the first LNG cargo to China

National Petroleum Corporation’s (PetroChina) Tangshan

Caofeidian LNG Terminal in the Hebei province of China. The

cargo was delivered onboard a Q-Flex class LNG vessel, AlGharrafa and will be used to commission the third LNG terminal

owned by PetroChina in the country. (Gulf-Times.com)

QPI, Total sign deal for joint participation in Congo – Qatar

Petroleum International (QPI) and Total have signed a detailed

agreement for QPI’s participation in Total E&P Congo. This

participation will be through a share capital increase of Total

E&P Congo, resulting in QPI holding 15% share after the

subscription. Earlier in May, the two companies had signed a

framework agreement to this effect. QPI will be an active nonoperating partner and will support the ambitious development

programs undertaken in the Republic of Congo. (GulfTimes.com)

ORDS CEO urges operators to reduce mobile broadband

costs – Ooredoo’s (ORDS) Chairman Sheikh Abdullah bin

Mohammed bin Saud al Thani has called on the global

communications industry to take on the challenge of providing

more people with broadband internet access. Abdullah urged

operators to work together to lower mobile broadband costs and

improve networks. (Qatar Tribune)

Upgraded weather forecasting facilities to be installed at

HIA – The multi-billion dollar Hamad International Airport (HIA)

will have upgraded weather forecasting capabilities. The stateof-the-art facility will be installed under a new project to be

executed by the Qatar Civil Aviation Authority, in association

with the Qatar Meteorology Department and Qatar Datamation

Systems. (Peninsula Qatar)

International

Bernanke: US Fed committed to easy policy for as long as

needed – The US Federal Reserve Chairman Ben Bernanke

said the Fed will maintain its ultra-easy monetary policy for as

long as needed and will only begin to taper bond-buying once it

is assured that labor market improvements would continue.

Bernanke said that while the US economy had made significant

progress, it was still far from where officials wanted it to be. He

said the Federal Open Market Committee remains committed to

maintaining highly accommodative policies. Since 2008, the Fed

has maintained its interest rates at near zero and quadrupled its

balance sheet to $3.9 trillion through three massive rounds of

bond buying. In October 2013, the Fed decided to maintain

asset purchases at an $85 billion monthly pace. (Reuters)

Chinese central bank vows faster foreign exchange reform;

IPO hopes tempered – China's central bank chief Zhou

Xiaochuan vowed to quicken the process of full convertibility for

the Chinese yuan, which would allow the free movement of

capital across China's borders. This has been a demand of

many of the country's major trading partners. Meanwhile, the

China Securities Regulatory Commission has reiterated its

commitment to ease the government's control over the initial

public offering process, but said the government will also

intensify its auditing of companies that hope to list on the

market. (Reuters)

OECD calls on ECB to buy Eurozone assets; ECB says all

options on the table – The Organization for Economic

Cooperation & Development (OECD) said the European Central

Bank (ECB) must consider buying government and corporate

bonds to help the Eurozone to avoid a Japanese-style

deflationary spiral. In October, inflation in the 17-nation

Eurozone fell to its lowest in nearly four years, along with the

economy struggling to recover after emerging from its longest

ever recession. Despite a surprise ECB rate cut this month, the

OECD said that the bank needs to take bolder measures at a

time of massive unemployment and difficult credit. Meanwhile,

ECB’s Vice President Vitor Constancio said all policy options are

open for the ECB and it has discussed the broad possibility of

asset buying. (Reuters)

OECD sees China’s growth accelerating in 2014, urges

more reforms – The OECD said China's annual economic

growth is likely to accelerate to 8.2% in 2014 from an expected

7.7% this year, on the back of stronger domestic demand. The

OECD said growth is picking up, inflation remains low, and

domestic demand has led the turnaround. The organization

highlighted the need for China to quicken structural reforms in

favor of stronger domestic consumption, since economic

expansion still relies heavily on investment. The OECD said with

the economy recovering, there is now a favorable window to

push forward with various structural reforms, particularly

financial liberalization, encouraging labor mobility and tax

reform. (Reuters)

OECD: Emerging markets hold back global recovery – The

OECD said slowing emerging markets are dragging down the

global economic recovery, while advanced countries are

struggling to pick up the slack after years of debt crises. The

OECD has trimmed its global growth forecasts, expecting the

world economy to grow 3.6% next year. The OECD’s Chief

Economist Pier Carlo Padoan said forecasts have been lowered

for many reasons, but the most important ones are the growth

downgrade in emerging countries, slower trade and subdued

investment. Padoan said advanced economies would not be

able to make up for the momentum lost by major emerging

economies, which are hit by capital outflows triggered by the US

Federal Reserve’s plans to rein in its exceptional monetary

stimulus. The OECD said the Fed should scale down its bond

purchases as activity strengthens next year, forecasting that

growth in the US economy would reach 2.9% in 2014, its

strongest performance since 2005, after an estimated 1.7% this

year. (Gulf-Times.com)

Regional

S&P: minimal impact of US shale boom on Gulf energy –

According to Standard & Poor’s (S&P), the shale boom in the

US has only a minimal impact on Gulf-based oil & gas

producers, which can endure a 15-20% drop in global oil prices

for now. S&P’s Credit Analyst Karim Nassif said notwithstanding

the potential consequences of shale oil production in North

America on the level of oil imports, there will be a limited effect

on the GCC producers at present. He said this reflects Gulfbased oil producers’ ability to redirect oil exports, as well as the

fact that many of them export heavier crude that are not

displaced by shale volumes. (Gulf-Times.com)

BCG: Digital technologies to raise quality in GCC

healthcare sector – According to a recent study by the Boston

Consulting Group (BCG), GCC governments need to implement

digital technologies in the healthcare sector to increase its

quality and productivity. The study noted that the move will also

support the transition to a prevention-focused healthcare

Page 3 of 5

4. system, which is the need of the hour for the local markets.

(GulfBase.com)

Italy woos UAE funds on Alitalia – According to Fabrizio

Pagani, a senior economic adviser to the Italian Prime Minister,

Italy’s government has spoken to sovereign wealth funds from

the UAE for the possibility of investing in its struggling airline,

Alitalia. He said Alitalia is looking for a partner outside Europe,

following Air France-KLM's decision not to take part in a capital

increase and allow its 25% stake to be diluted to just 7%.

(Reuters)

Cluttons: Dubai property growth cools after new measures

– According to a report by Cluttons, the measures introduced

recently to regulate the Dubai property market have already

begun to have an impact with its growth rate cooling down. The

Cluttons report found that the steps initiated by the UAE Central

Bank to limit the size of mortgage loans, along with the Dubai

Land Department’s recent doubling of property registration fees

from 2% to 4%, are affecting the volume of deals being

registered in the residential market. (GulfBase.com)

DGCX to list plastics futures contract – The Dubai Gold and

Commodities Exchange (DGCX) will launch its new plastics

futures contract on February 28, 2014. The contract is designed

to provide enhanced liquidity in the global plastics trade and will

be the first ever plastics contract to be listed in the MENA

region. (GulfBase.com)

Dubai Airports to bring more cargo carriers to new hub –

Dubai Airports said it is in talks with many cargo carriers to

persuade them to operate from the new Al Maktoum airport hub,

while it is continuing to work on adding more passenger airlines

after the facility opened last month. (Bloomberg)

Etihad, CFM sign $2.8bn aircraft engine deal – Abu Dhabibased Etihad Airways has selected CFM International’s

advanced Leap-1A engine worth $2.8bn to power its 26 Airbus

A321neo, which is scheduled to be delivered in 2018. To

support its new fleet, the airline has signed a 15-year rate-perflight-hour agreement, under which CFM will guarantee the

maintenance costs on a dollar per engine flight hour basis.

(GulfBase.com)

Mubadala to service Rolls Royce Trent XWB engines –

Rolls-Royce has entered into a strategic agreement with Abu

Dhabi's Mubadala Aerospace that will allow the governmentowned company to service the engine manufacturer's Trent

XWB engines. According to Rolls-Royce, Mubadala will become

an approved provider of Trent engine maintenance, repair &

overhaul, Rolls-Royce's first such designation in the Middle

East. As part of the deal, the engine manufacturer will also

source $500mn worth of spare parts from Mubadala over a 10year period. (Reuters)

Abu Dhabi’s CPI up 1.1% in first 10 months – According to

the Statistics Centre–Abu Dhabi (SCAD), the inflation rate of

consumer prices for the first 10 months of 2013 in Abu Dhabi

was 1.1% YoY. The CPI increased from 123.7 points in October

2012 to 125.7 points in October 2013, indicating a 1.6% rise.

However, the CPI decreased by 0.2% in October 2013

compared with September 2013. (GulfBase.com)

ADNOC eyes Saudi market next year – The Abu Dhabi

National Oil Company (ADNOC) has revealed plans to expand

into the Saudi market in 2014 by providing service stations as

well as aviation services in the Kingdom. ADNOC’s CEO

Abdullah Al Dhaheri said the company is in final stages of

discussion with the operator who will be operating as a

franchisee to ADNOC’s distribution. Al Dhaheri said there are

currently around 110 stations under discussion, of which 21 are

under construction and around 80 are under design. These

service stations are expected to be operational over the next two

years. (GulfBase.com)

Aldar Properties picks banks for sukuk sale – Aldar

Properties has hired five banks to arrange the sale of a

benchmark-sized Islamic bond to refinance its debt. The firm

has hired the National Bank of Abu Dhabi, First Gulf Bank,

Dubai Islamic Bank, Standard Chartered and Goldman Sachs.

The company is reportedly planning to issue the sukuk by the

year-end. (GulfBase.com)

Ashmore seeks buyer for Alphaland stake – London-based

private equity fund Ashmore Group reportedly is in talks with

several parties, including a member of Abu Dhabi's ruling family,

for the acquisition of its stake in Ongpin-led upscale property

developer Alphaland Corp. (Reuters)

Abu Dhabi’s Cepsa pays $2.2bn for Coastal Energy – Abu

Dhabi-owned oil refiner Cia. Espanola de Petroleos (Cepsa) and

partner Strategic Resources (Global) Ltd. agreed to buy Coastal

Energy for $2.2bn. Citigroup and Credit Suisse Group are the

financial advisers for Coastal Energy, while Goldman Sachs is

the financial adviser for Cepsa. PriceWaterhouseCoopers is

advising both Cepsa and Strategic Resources. (Reuters)

The National Investor’s CEO resigns – Abu Dhabi-based

investment firm, The National Investor’s Chief Executive Orhan

Osmansoy has resigned and his replacement is yet to be

named. Osmansoy, who joined the firm in 2004, was

instrumental in expanding the company into a regional

investment firm, operating in private equity, investment advisory

and asset management businesses. However the company was

hard hit during the global financial crisis. (Peninsula Qatar)

LS2 Consulting wins 5 energy contracts – LS2 Consulting, a

leading business solution provider, has secured five different

new contracts in the oil & gas contracting industry. These new

deals have raised the group's portfolio value to over AED10mn

($2.7mn) in the UAE. (GulfBase.com)

Kuwait offers $2bn in loans to African states – Kuwait's Emir

Sheikh Sabah al Ahmad al Sabah has pledged $1bn in lowinterest loans and a similar amount in investments to African

states over the next five years. (Qatar Tribune)

CBO warns against higher credit ceiling for salaried

employees – The Central Bank of Oman (CBO) has issued a

warning for all licensed banks in the country to abide strictly by

the royal orders regarding the standardization of grades and

salaries of all the staff in the civil sector. The CBO has warned

all banks against any abuse or exploitation of the resulting

increase in the salaries of the intended recipients. The CBO

stressed that banks should not raise the personal loan ceiling

limits or loan interest rates of the beneficiaries or take any other

measure of similar effect. (GulfBase.com)

Oman Oil Marketing signs agreement with Duqm Port – The

Oman Oil Marketing Company has signed a bunkering license &

land lease agreement with Port of Duqm Company to develop a

bunkering terminal and ancillary facilities at the Duqm Port. This

terminal will offer heavy fuel oil, marine diesel oil and marine

lubricants to ships calling at the port. (Bloomberg)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

0.4%

148.9

130.9

0.0%

0.0%

0.0%

0.0%

(0.0%)

(0.0%)

118.9

(0.2%)

(0.4%)

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Dubai

Oman

Bahrain

Jul-13

Abu Dhabi

QE Index

May-12 Dec-12

Kuwait*

Oct-11

Qatar *

Jan-10 Aug-10 Mar-11

(0.6%)

Saudi Arabia

(0.8%)

Source: Bloomberg (*As of November 19, 2013)

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,275.19

(0.0)

(1.1)

(23.9)

DJ Industrial

15,967.00

(0.1)

0.0

21.8

20.38

(0.2)

(2.1)

(32.8)

S&P 500

1,787.87

(0.2)

(0.6)

25.3

107.36

(1.0)

(1.0)

(3.4)

NASDAQ 100

3,931.55

(0.4)

(1.3)

30.2

3.63

(2.2)

2.1

6.0

322.56

(0.7)

(0.2)

15.3

118.50

(0.2)

(0.1)

32.4

DAX

9,193.29

(0.3)

0.2

20.8

142.75

(0.3)

(0.5)

(17.5)

FTSE 100

6,698.01

(0.4)

0.0

13.6

STOXX 600

Euro

1.36

0.4

0.5

2.8

Yen

99.96

(0.0)

(0.2)

15.3

Nikkei

4,272.29

(1.1)

(0.4)

17.4

15,132.22

(0.2)

(0.2)

45.6

GBP

1.61

0.1

(0.0)

(0.8)

CHF

1.10

(0.1)

0.1

0.2

MSCI EM

1,024.53

(0.1)

1.9

(2.9)

SHANGHAI SE Composite

2,193.13

(0.2)

2.7

(3.4)

AUD

0.94

0.1

0.2

(9.7)

HANG SENG

23,657.80

(0.0)

2.7

4.4

USD Index

80.70

(0.2)

(0.2)

RUB

32.71

0.5

0.4

1.1

BSE SENSEX

20,890.80

0.2

2.4

7.5

7.1

Bovespa

53,032.90

(2.3)

(0.8)

(13.0)

BRL

0.44

0.1

2.5

(9.3)

1,455.04

(0.5)

0.8

(4.7)

Source: Bloomberg

CAC 40

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5