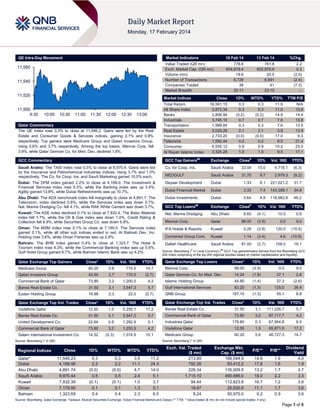

1. QE Intra-Day Movement

Market Indicators

11,560

11,540

11,520

11,500

9:30

16 Feb 14

13 Feb 14

%Chg.

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

778.6

604,679.4

19.6

6,729

38

25:11

761.8

602,979.9

20.0

6,891

41

23:15

2.2

0.3

(2.0)

(2.4)

(7.3)

–

Market Indices

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.3% to close at 11,546.2. Gains were led by the Real

Estate and Consumer Goods & Services indices, gaining 2.1% and 0.9%

respectively. Top gainers were Medicare Group and Qatari Investors Group,

rising 5.6% and 3.7% respectively. Among the top losers, Mannai Corp. fell

3.9%, while Qatar German Co. for Med. Dev. declined 1.8%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

16,591.15

2,872.34

2,808.56

3,745.10

1,999.84

2,029.29

2,733.20

1,592.44

6,555.12

3,324.28

0.3

0.3

(0.2)

0.7

0.3

2.1

(0.0)

0.2

0.9

1.0

0.3

0.3

(0.2)

0.7

0.3

2.1

(0.0)

0.2

0.9

1.0

11.9

11.0

14.9

7.0

7.6

3.9

17.0

9.5

10.2

9.5

N/A

13.8

14.4

13.8

13.5

13.9

6.3

21.4

25.0

17.1

GCC Commentary

GCC Top Gainers##

Exchange

Close#

Saudi Arabia: The TASI index rose 0.5% to close at 8,970.4. Gains were led

by the Insurance and Petrochemical Industries indices, rising 3.7% and 1.0%

respectively. The Co. for Coop. Ins. and Saudi Marketing gained 10.0% each.

Co. for Coop. Ins.

1D%

Saudi Arabia

33.00

10.0

4,718.1

(6.3)

MEDGULF

Saudi Arabia

31.70

9.7

2,979.3

(9.2)

Dubai: The DFM index gained 2.2% to close at 4,189.0. The Investment &

Financial Services index rose 5.5%, while the Banking index was up 3.4%.

Agility gained 13.8%, while Dubai Refreshments was up 10.7%.

Deyaar Development

Dubai

1.33

8.1

221,021.2

31.7

Dubai Financial Market

Dubai

3.33

7.4

143,388.1

34.8

Abu Dhabi: The ADX benchmark index fell marginally to close at 4,891.7. The

Telecomm. index declined 0.8%, while the Services index was down 0.7%.

Nat. Marine Dredging Co. fell 4.1%, while RAK White Cement was down 3.7%.

Dubai Investments

Dubai

3.64

4.9

118,982.6

46.2

GCC Top Losers

Exchange

Kuwait: The KSE index declined 0.1% to close at 7,832.4. The Basic Material

index fell 1.7%, while the Oil & Gas index was down 1.0%. Credit Rating &

Collection fell 8.9%, while Securities Group Co. was down 6.8%.

Nat. Marine Dredging

Abu Dhabi

Mannai Corp.

Oman: The MSM index rose 0.1% to close at 7,180.0. The Services index

gained 0.1%, while all other sub indices ended in red. Al Batinah Dev. Inv.

Holding rose 3.6%, while Oman Fisheries was up 2.8%.

Bahrain: The BHB index gained 0.4% to close at 1,323.7. The Hotel &

Tourism index rose 4.3%, while the Commercial Banking index was up 0.6%.

Gulf Hotel Group gained 6.7%, while Bahrain Islamic Bank was up 4.2%.

##

#

Close

Vol. ‘000

1D% Vol. ‘000

YTD%

YTD%

8.65

(4.1)

10.5

0.6

Qatar

98.00

(3.9)

0.0

9.0

IFA Hotels & Resorts

Kuwait

0.26

(3.8)

120.0

(10.5)

Combined Group Cont.

Kuwait

1.14

(3.4)

4.6

(10.9)

Dallah Healthcare

Saudi Arabia

81.00

(2.7)

158.0

16.1

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Medicare Group

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

60.20

Qatar Exchange Top Gainers

5.6

774.5

14.7

Mannai Corp.

98.00

(3.9)

0.0

9.0

Qatar German Co. for Med. Dev.

14.24

(1.8)

37.1

2.8

Qatar Exchange Top Losers

Qatari Investors Group

42.50

3.7

170.5

(2.7)

Commercial Bank of Qatar

73.80

3.2

1,200.5

4.2

Islamic Holding Group

44.80

(1.4)

37.3

(2.6)

Barwa Real Estate Co.

31.50

3.1

3,547.3

5.7

Gulf International Services

83.20

(1.3)

125.0

36.4

Ezdan Holding Group

16.88

2.3

22.0

(0.7)

QNB Group

187.10

(1.3)

55.1

8.8

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Barwa Real Estate Co.

31.50

3.1

111,226.7

5.7

5.7

Commercial Bank of Qatar

73.80

3.2

87,117.7

4.2

1,292.9

0.1

Industries Qatar

179.80

0.3

67,954.8

6.5

3.2

1,200.5

4.2

Vodafone Qatar

12.55

1.5

65,871.0

17.2

(0.3)

1,074.9

10.1

Medicare Group

60.20

5.6

46,727.3

14.7

Close*

1D%

Vol. ‘000

YTD%

Vodafone Qatar

12.55

1.5

5,250.1

17.2

Barwa Real Estate Co.

31.50

3.1

3,547.3

United Development Co.

22.64

0.9

Commercial Bank of Qatar

73.80

Salam International Investment Co.

14.32

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Close

1D%

WTD%

MTD%

YTD%

11,546.23

4,188.98

4,891.74

8,970.44

7,832.39

7,179.95

1,323.68

0.3

2.2

(0.0)

0.5

(0.1)

0.1

0.4

0.3

2.2

(0.0)

0.5

(0.1)

0.1

0.4

3.5

11.1

4.7

2.4

1.0

1.3

2.3

11.2

24.3

14.0

5.1

3.7

5.1

6.0

Exch. Val. Traded

($ mn)

213.80

792.26

229.34

1,715.10

94.44

19.47

8.24

Exchange Mkt.

Cap. ($ mn)

166,044.9

83,412.2

135,009.5

490,686.0

112,823.8

25,630.9

50,975.0

P/E**

P/B**

14.6

17.8

13.2

18.0

16.7

11.1

9.2

1.9

1.6

1.7

2.2

1.2

1.7

0.9

Dividend

Yield

4.0

1.9

3.7

3.3

3.6

3.6

3.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.3% to close at 11,546.2. The Real Estate

and Consumer Goods & Services indices led the gains. The

index rose on the back of buying support from non-Qatari

shareholders despite selling pressure from Qatari shareholders.

Medicare Group and Qatari Investors Group were the top

gainers, rising 5.6% and 3.7% respectively. Among the top

losers, Mannai Corp. fell 3.9%, while Qatar German Co. for Med.

Dev. declined 1.8%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

65.11%

71.38%

(48,742,002.89)

Non-Qatari

34.89%

28.62%

48,742,002.89

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday fell by 2.0% to 19.6mn from

20.0mn on Thursday. However, as compared to the 30-day

moving average of 11.7mn, volume for the day was 67.2%

higher. Vodafone Qatar and Barwa Real Estate Co. were the

most active stocks, contributing 26.8% and 18.1% to the total

volume respectively.

Ratings and Earnings

Ratings Updates

Company

Agency

Finance House (FH)

CI

Market

Abu

Dhabi

Type*

Old Rating

New Rating

Rating Change

Outlook

Outlook Change

–

LT corporate credit

rating/ ST corporate

credit

ratings

BBB-/A3

–

Stable

–

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency)

Earnings Releases

Company

Dubai Insurance Company

(DIC) *

Al Kamil Power Company

(AKPC)*

Nat. Aluminium products *

BMMI *

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

AED

321.4

-2.4%

–

–

20.3

-3.5%

Oman

OMR

–

–

–

–

3.1

–

Oman

OMR

–

–

–

–

1.2

–

Bahrain

BHD

98.3

7.1%

8.6

31.3%

10.1

17.3%

Market

Currency

Dubai

Source: Company data, DFM, ADX, MSM

News

Qatar

Qatar infrastructure spending to touch $24bn in 2014 –

According to the organizers of the 11th Annual Qatar Projects

Conference, scheduled next month, Qatar will see a significant

rise in project activity in 2014 with contract awards expected to

peak at $24bn. After successfully completing a 20-year

investment program to develop its natural gas resources in

2011, Qatar has embarked on an infrastructure investment

program in its non-oil and gas sectors driven by the Qatar

National Vision 2030. The Qatari projects market accelerated in

2013, overtaking the UAE in terms of contract awards midway

through the year with $12.2bn in new awards, the bulk of which

came from the multi-billion-dollar tunneling contracts awarded as

part of the Doha metro project. Qatar, which plans to grow its

downstream sector with investment over $13bn, currently has

$16.5bn worth of upstream oil schemes at various pre-execution

phases. (Gulf-Times.com)

IQCD Announces Significant Dividend Boost Despite a

Weak 4Q2013 – IQCD reported Weaker-than-expected 4Q2013

results that missed our estimates/consensus. IQCD reported

QR1.67bn in net income (-5% QoQ, -6% YoY) vs. our estimate

of QR1.98bn and Reuters consensus of QR1.99bn. A drop in

steel revenue and margins versus our estimates along with a

slightly weaker-than-expected fertilizer performance more than

offset better-than-forecast petrochemical revenue and profits.

Overall group EBITDA declined by around 5% sequentially to

QR1.7bn. Petrochemicals benefited from improved pricing and

increase in LDPE sales volumes. Revenue of QR1.5bn

increased by ~9% QoQ with net profit dropping by ~2% to

around QR1bn. Improvement in LDPE prices along with LDPE

sales volume growth due to the timing of specific shipments

(despite down production due to 29 days of shutdowns vs. 18

days in 3Q2013) led to the improved performance relative to our

model. Fertilizers were affected by flattish urea prices offsetting

improved sales volume. Revenue of QAR1.3bn increased

around 4% QoQ with urea sales volume sequentially gaining by

100k tons. Net profit of QR323mn (-3% QoQ), was slightly below

our model. Sales volumes improved despite a number of

planned and unplanned shut-downs (ammonia: 29 days, urea:

44 days) and made up for static urea selling prices that

remained mostly flat during the quarter. According to IQCD, its

urea prices declined by +$100/MT since beginning -2013 to

close at a 3-year low of $293/MT. Steel segment benefits from

sequential growth in re-bar sales volume. Revenue of QAR1.4bn

increased~3% QoQ with moderate sequential volume growth.

Net income, however, dropped 23% QoQ driven by increased

raw material costs. Significant positive surprise on dividends.

IQCD’s BoD proposed a DPS of QR11.00 vs. our estimate of

QR9.00 and Bloomberg consensus of QR8.71. We have long

held the view that upside to dividend expectations is possible

given lack of significant capex needs and a bullet-proof balance

sheet (QR5.7bn in net cash as of 2013). We will await more

color if such a high level of payout (83% for 2013) is sustainable

going forward. We continue to favor IQCD as a long-term play.

With major expansions now complete, significant costPage 2 of 5

3. advantaged volume growth in fertilizers/petrochemicals should

continue to aid in FCF generation. We continue to believe that

upside to our dividend expectations and/or new expansions is

possible over the medium term. (IQCD Press Release, QNBFS

Research

QCFS reports QR11.4mn net profit, recommends 20% cash

dividend – Qatar Cinema and Film Distribution Company

(QCFS) has reported a net profit of QR11.4mn in 2013 as

compared to QR11.8mn in 2012. EPS amounted to QR2.00 in

2013 vs. QR2.07 in 2012. Meanwhile, QCFS’ board has

recommended 20% cash dividend, i.e. QR 2.0 per share. (QE)

QIC gets shareholders’ nod for capital hike to QR1.6bn – An

extraordinary general meeting of Qatar Insurance Company

(QIC) has approved an increase in its capital to QR1.6bn from

QR1.28bn by distributing bonus shares at the rate of one share

for every four shares held by shareholders. The EGM authorized

QIC’s board of directors to amend article six of the company’s

article of association to reflect the capital increase. Meanwhile,

the board’s recommendation for distributing a cash dividend of

QR2.5 a share and a special 50th anniversary bonus share of

25% has also been approved. (Gulf-Times.com)

Tasweeq, ADNOC sign first condensate term contract –

Qatar International Petroleum Marketing Company (Tasweeq)

has signed its first condensate term contract with Abu Dhabi

National Oil Company (ADNOC). Qatar condensate is produced

by Dolphin Energy and Qatar Shell’s Pearl GTL Plant from the

North Field Gas Reservoir in Qatar. The condensate is primarily

used in the condensates splitter units and topping refineries, and

is also used as a lightning agent for blending heavier crude oil.

ADNOC will use Qatar condensate as splitter refinery feedstock.

(Gulf-Times.com)

Trading suspension in DOHI’s shares on February 17 due to

its AGM & EGM – The Qatar Exchange (QE) has announced

trading suspension on Doha insurance Company’s (DOHI)

shares on February 17, 2014due to its AGM and EGM being

held on that day. (QE)

International

China’s ICBC weighs Mid-east acquisitions to boost profit –

The Industrial & Commercial Bank of China (ICBC) stated that it

will consider acquisitions in the Middle East as part of its plans

to boost earnings from the region by 50% this year. ICBC’s CEO

for the Middle East, Zhou Xiaodong said ICBC is seeking new

acquisition opportunities since acquisitions are the reason why

ICBC grew so fast in Hong Kong. Zhou said ICBC is seeking to

triple its overseas earnings until 2016 by targeting more

business from Middle Eastern companies after previously

focusing on Chinese firms in the region. The bank plans to open

retail branches in Kuwait, Saudi Arabia and the UAE. ICBC lent

$600mn to regional clients including Emirates Airline, Qatar

Airways and DEWA in 2013. In 2014, the bank is seeking to

boost lending to Dubai real estate projects, energy companies in

Abu Dhabi and infrastructure work in Qatar. In January, it

advanced $201mn to Dubai-based real estate investment

company SKAI Holdings for the development of a hotel on the

Palm Jumeirah. (Bloomberg)

BoJ mulls refraining from 2015 monetary-base forecast –

According to sources, the Bank of Japan (BoJ) is considering to

refrain from issuing a monetary-base forecast for 2015 to avoid

signaling a commitment to monetary easing for a specific time

period. Sources added that when the BoJ unveiled

unprecedented easing in April 2013, it said the monetary base

will rise to 270tn yen ($2.65tn) by the end of 2014, however,

now the central bank may avoid issuing any update for coming

years. The BoJ is forecasted to leave its policy unchanged at its

upcoming meeting even after a report indicated weaker-thanforecast growth in the fourth quarter. (Bloomberg)

BoE: jobs, incomes, wages to be factored into any rate rise

– The Bank of England’s (BoE) Governor Mark Carney said the

central bank will only start to increase interest rates when a

range of measures suggest the UK economy is operating at

closer to full capacity. Earlier, the BoE stated that it would look

at a broader range of measures of slack in the economy than

just the unemployment rate when considering rate rise, and that

it was in no rush to raise rates. Carney said both the path of

monetary policy and the path of interest rates are going to be

calibrated carefully to ensure that adjustments are made only

when a sustainable growth in jobs, incomes and spending is

visible. (Reuters)

Regional

QNB Group: Saudi non-oil private sector key growth driver

in 2014 – According to a report by QNB Group, the non-oil

private sector in Saudi Arabia is expected to be the key growth

driver in 2014, boosted by large public sector infrastructure

investment and the rapidly growing population. Saudi Arabia has

been one of the best performing G20 economies in recent years

with its real GDP growth averaging 5.9% per year during 200813. Saudi authorities recently announced the 2014 state budget

plan, projecting another expansionary budget to continue the

process of diversifying the economy. Based on a conservative

oil price assumption of $80 per barrel, government revenues

and expenditures are expected to be $228bn in 2014. The

budget includes substantial outlays for education, health and

infrastructure, despite the expected declines in oil revenues. The

preliminary macroeconomic data suggests that the overall

economic growth slowed to 3.8% YoY in 2013 owing to a

decline in oil output. Meanwhile, non-oil growth grew by a robust

5.0% YoY in 2013 as consecutive years of government

spending lifted business and consumer confidence and banks'

comfort in lending. QNB said that the budget announcement

indicated that the fastest growing sectors in 2013 were:

construction (8.1%), followed by transport & communication

(7.2%), and retail (6.1%). (Gulf-Times.com)

FARM Superstores begins trading on Tadawul – The Saudi

Capital Market Authority (CMA) announced that equity shares of

FARM Superstores would begin trading on the Saudi stock

exchange (Tadawul) from February 16, 2014, under the code

4006 in the retail sector. The CMA also stated that the daily

price fluctuation on the company’s shares would be limited to

10% from the first trading day. (GulfBase.com)

UAE to double budget on homeland security to $10bn in 10

years – According to a US study on security & safety resources,

the UAE is set to double its spending on homeland security from

$5.5bn to more than $10bn in the next 10 years. Meanwhile, the

UAE spending on airport security is likely to reach $57.7mn by

2015. The study, published in the 2013-2014 annual report of

the US Department of Commerce’s International Trade

Administration, showed that the increased investment on

homeland security is aimed at protecting economic

development, to curtail regional unrest and the increased

complexity of potential threats. (GulfBase.com)

du Telecom agrees terms on $720mn loan financing –

According to sources, UAE-based du Telecom has agreed on

the terms for a $720mn loan that will be used to replace two

existing debt facilities and lower the company's funding costs.

The five-year loan will be provided by Abu Dhabi Commercial

Bank, the National Bank of Abu Dhabi and Samba Financial

Page 3 of 5

4. Group. The interest rate paid by du Telecom for the new loan

will be 140 basis points above the Libor. (Gulf-Times.com)

DEWA starts work on substation to power MBR City – The

Dubai Electricity & Water Authority (DEWA) has commenced

construction work and the commissioning of a 400kv main

substation at Seih Al Dahl. This substation will connect the

projects of the Mohammed Bin Rashid Al Maktoum Solar Park to

DEWA’s grid, as well as provide power to Mohammed Bin

Rashid City. (Bloomberg)

SVCP declares SR18.75mn dividend for 1Q2014 – Saudi

Vitrified Clay Pipe Company’s (SVCP) board of directors has

recommended the distribution of dividends worth SR18.75mn to

its shareholders for 1Q2014. The dividend per share will be

SR1.25, representing 12.5% of the face value. Those

shareholders who are registered with the Securities Depository

Center on March 31, 2014 will be eligible for this dividend.

(Tadawul)

ADNH appoints Acting CEO – Abu Dhabi National Hotels

Company (ADNH) has appointed Ahmed Siddiq Mohamed

Khoori as its Acting Chief Executive Officer, effective from

February 13, 2014 and until further notice. (GulfBase.com)

Kuwaiti oil refineries still at shutdown risk – Oil refineries in

Kuwait risk further shutdowns due to the poor power supply

system in the country. The reason behind the power failure that

caused three of the country's oil refineries with a total capacity

of around 930,000 bpd to go offline last month is still unclear.

The incident however points out that the fault lies in the state

electricity supplier, and not electrical faults in the refineries

themselves. Kuwait refines around a third of its crude oil

production of 3mn bpd and exports around 660,000 bpd of those

petroleum products. (Bloomberg)

AKPC declares OMR9.625mn dividend for 2013 – Al Kamil

Power Company’s (AKPC) board of directors has proposed a

distribution of a cash dividend of 10% on the paid-up capital of

OMR9.625mn for 2013 to its shareholders. Those shareholders

who are registered in with Muscat Depository & Securities

Registration Company on July 29, 2014, will be eligible for this

dividend. The company’s AGM is scheduled to be held on March

16, 2014. (MSM)

NAPCO recommends 12% cash dividend – National

Aluminium Products Company’s (NAPCO) board has

recommended a total cash dividend of 12%, i.e. 12 baizas per

share (par value of 100 baizas) for the year ended December

31, 2013. This dividend is subject to the approval of its

shareholders. Meanwhile, NAPCO’s board has agreed for the

AGM to be held on March 13, 2014. (MSM)

Bahrain's Al Baraka Islamic Bank sees new scope to

expand – Bahrain based Islamic lender Al Baraka expects at

least 15% growth in net profit this year as its business recovers

across a region hit by the Arab Spring unrest. The growth will

also be fuelled by the company's entry into the Moroccan and

Libyan markets and expansion in Tunisia as monetary

authorities become more welcoming to Islamic banking. Chief

Executive Officer Adnan Ahmed Yousif said that, the bank,

which has operations across the Middle East, Asia and Africa, is

due to announce a double digit increase in 2013 profits, driven

by overall growth in core business and a 15% rise in lending.

(Bloomberg)

NBK appoints Isam Al Sager as Group CEO – The National

Bank of Kuwait (NBK) has appointed Isam Al Sager as the

Group CEO. Al-Sager, has been NBK’s Deputy Group CEO

since 2010 and has served in several other banks in Kuwait.

(Bloomberg)

MOTC Oman plans to revamp ONTC – The Ministry of

Transport & Communications (MOTC Oman) is planning to

revamp the state-owned Oman National Transport Company

(ONTC) for providing an integrated public transport system for

the country, which will include taxi services. The plan is to

convert ONTC into a complete transport solution provider along

with underground metro and ferry services, if needed. MOTC

Oman’s Minister Dr. Ahmed bin Mohammed bin Salim al Futaisi

signed an agreement with Inco, a Spanish transport consultancy

agency last December for advising the government on

developing a multi-modal public transport system, which will

reduce the growing traffic congestion in Muscat. (GulfBase.com)

DICS signs deal with Munich Health for new company –

Dhofar Insurance Company (DICS) has signed a MoU with Abu

Dhabi-based Munich Health Daman Holding Ltd to establish a

new partnership company specializing in health insurance in

Oman. Munich Health is a JV between the Government of Abu

Dhabi and Munich Reinsurance Company for the purpose of a

joint regional expansion. (Zawya)

SHCS declares 15% cash dividend for 2013 – Salalah Beach

Resort’s (SHCS) board of directors has recommended a cash

dividend of 15% on paid-up share capital of the company,

amounting to 150 baizas per share for the financial year ended

December 31, 2013. The dividend is subject to approval by the

company’ shareholders at the AGM scheduled to be held on

March 17, 2014. (GulfBase.com)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

180.0

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

143.6

130.5

1.8%

1.2%

0.6%

0.5%

0.4%

0.3%

0.1%

0.0%

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

1,318.69

0.0

0.0

9.4

21.48

0.0

0.0

10.3

109.08

0.0

0.0

5.54

0.0

155.00

Global Indices Performance

Close

1D%

WTD%

YTD%

16,154.39

0.0

0.0

(2.5)

S&P 500

1,838.63

0.0

0.0

(0.5)

(1.6)

NASDAQ 100

4,244.03

0.0

0.0

1.6

0.0

27.4

STOXX 600

333.32

0.0

0.0

1.5

0.0

0.0

22.8

DAX

9,662.40

0.0

0.0

1.2

138.50

0.0

0.0

1.5

FTSE 100

6,663.62

0.0

0.0

(1.3)

DJ Industrial

1.37

0.0

0.0

(0.4)

CAC 40

101.80

0.0

0.0

(3.3)

Nikkei

GBP

1.67

0.0

0.0

1.1

MSCI EM

CHF

1.12

0.0

0.0

0.0

SHANGHAI SE Composite

AUD

0.90

0.0

0.0

1.3

USD Index

80.14

0.0

0.0

RUB

35.17

0.0

0.0

BRL

0.42

0.0

0.0

(1.0)

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

Kuwait

Jan-11

(0.0%)

(0.1%)

Qatar

(0.6%)

Saudi Arabia

Jun-10

2.2%

2.4%

165.9

4,340.14

0.0

0.0

1.0

14,313.03

0.0

0.0

(12.1)

957.31

0.0

0.0

(4.5)

2,115.85

0.0

0.0

(0.0)

HANG SENG

22,298.41

0.0

0.0

(4.3)

0.1

BSE SENSEX

20,366.82

0.0

0.0

(3.8)

7.0

Bovespa

48,201.11

0.0

0.0

(6.4)

1,343.20

0.0

0.0

(6.9)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5