1. Page 1 of 6

QE Intra-Day Movement

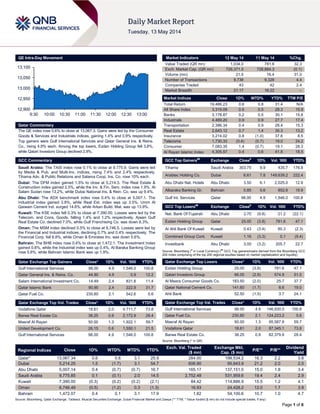

Qatar Commentary

The QE index rose 0.6% to close at 13,067.3. Gains were led by the Consumer

Goods & Services and Industrials indices, gaining 1.4% and 0.9% respectively.

Top gainers were Gulf International Services and Qatar General Ins. & Reins.

Co., rising 4.9% each. Among the top losers, Ezdan Holding Group fell 3.8%,

while Qatari Investors Group declined 2.9%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.1% to close at 9,775.9. Gains were led

by Media & Pub. and Multi-Inv. indices, rising 7.4% and 2.4% respectively.

Tihama Adv. & Public Relations and Salama Coop. Ins. Co. rose 10% each.

Dubai: The DFM index gained 1.5% to close at 5,214.3. The Real Estate &

Construction index gained 2.5%, while the Inv. & Fin. Serv. index rose 1.9%. Al

Salam Sudan rose 13.2%, while Dubai National Ins. & Rein. Co. was up 9.4%.

Abu Dhabi: The ADX benchmark index rose 0.4% to close at 5,007.1. The

Industrial index gained 3.8%, while Real Est. index was up 3.5%. Umm Al

Qaiwain Cement Ind. surged 14.6%, while Arkan Build. Mat. was up 13.9%.

Kuwait: The KSE index fell 0.3% to close at 7,390.00. Losses were led by the

Telecom. and Cons. Goods, falling 1.4% and 1.2% respectively. Ajwan Gulf

Real Estate Co. declined 7.0%, while Gulf Franchising Co. was down 6.3%.

Oman: The MSM index declined 0.5% to close at 6,746.5. Losses were led by

the Financial and Industrial indices, declining 0.7% and 0.4% respectively. The

Financial Corp. fell 6.8%, while Oman & Emirates Inv. was down 5.6%.

Bahrain: The BHB index rose 0.4% to close at 1,472.1. The Investment Index

gained 0.8%, while the Industrial index was up 0.4%. Al Baraka Banking Group

rose 5.6%, while Bahrain Islamic Bank was up 1.9%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Gulf International Services 98.00 4.9 1,546.0 100.8

Qatar General Ins. & Reins. Co. 44.80 4.9 0.9 12.2

Salam International Investment Co. 14.49 2.4 831.8 11.4

Qatar Islamic Bank 90.90 2.4 222.9 31.7

Qatar Fuel Co. 230.80 2.1 542.6 5.6

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Vodafone Qatar 18.61 2.0 4,711.7 73.8

Barwa Real Estate Co. 38.25 0.9 2,172.9 28.4

Masraf Al Rayan 50.00 1.3 1,922.1 59.7

United Development Co. 26.15 0.6 1,550.1 21.5

Gulf International Services 98.00 4.9 1,546.0 100.8

Market Indicators 12 May 14 11 May 14 %Chg.

Value Traded (QR mn) 1,034.0 781.6 32.3

Exch. Market Cap. (QR mn) 726,371.5 726,884.3 (0.1)

Volume (mn) 21.5 16.4 31.0

Number of Transactions 9,738 9,328 4.4

Companies Traded 43 42 2.4

Market Breadth 21:17 16:22 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,486.23 0.6 0.8 31.4 N/A

All Share Index 3,319.09 0.5 0.5 28.3 15.9

Banks 3,178.87 0.2 0.5 30.1 15.8

Industrials 4,469.20 0.9 0.9 27.7 17.4

Transportation 2,386.34 0.4 0.9 28.4 15.3

Real Estate 2,643.12 0.7 1.4 35.3 13.2

Insurance 3,214.02 0.8 (1.0) 37.6 8.5

Telecoms 1,730.33 (0.4) (0.7) 19.0 24.2

Consumer 7,083.35 1.4 (0.7) 19.1 28.3

Al Rayan Islamic Index 4,305.57 0.4 0.6 41.8 18.5

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Tihama Saudi Arabia 303.75 9.9 435.7 176.8

Arabtec Holding Co. Dubai 6.61 7.8 149,639.2 222.4

Abu Dhabi Nat. Hotels Abu Dhabi 3.50 6.1 2,025.0 12.9

Albaraka Banking Gr. Bahrain 0.85 5.6 852.6 19.9

Gulf Int. Services Qatar 98.00 4.9 1,546.0 100.8

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Nat. Bank Of Fujairah Abu Dhabi 3.70 (9.8) 21.2 (22.1)

Ezdan Holding Group Qatar 25.00 (3.8) 781.6 47.1

Al Ahli Bank Of Kuwait Kuwait 0.43 (3.4) 80.3 (2.3)

Combined Group Cont. Kuwait 1.16 (3.3) 0.1 (9.4)

Investbank Abu Dhabi 3.00 (3.2) 205.7 22.7

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 25.00 (3.8) 781.6 47.1

Qatari Investors Group 66.00 (2.9) 574.9 51.0

Al Meera Consumer Goods Co. 183.50 (2.0) 25.7 37.7

Qatar National Cement Co. 141.60 (1.7) 8.6 19.0

Ahli Bank 52.50 (1.5) 3.7 24.1

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Gulf International Services 98.00 4.9 146,930.5 100.8

Qatar Fuel Co. 230.80 2.1 124,223.2 5.6

Masraf Al Rayan 50.00 1.3 95,587.9 59.7

Vodafone Qatar 18.61 2.0 87,345.1 73.8

Barwa Real Estate Co. 38.25 0.9 82,379.9 28.4

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,067.34 0.6 0.8 3.1 25.9 284.00 199,534.2 16.3 2.2 3.8

Dubai 5,214.25 1.5 (1.7) 3.1 54.7 606.90 95,643.9 21.2 2.0 2.0

Abu Dhabi 5,007.14 0.4 (0.7) (0.7) 16.7 165.17 137,151.0 15.0 1.8 3.4

Saudi Arabia 9,775.85 0.1 (0.1) 2.0 14.5 2,752.48 531,959.6 19.4 2.4 2.9

Kuwait 7,390.00 (0.3) (0.2) (0.2) (2.1) 84.42 114,886.9 15.5 1.2 4.1

Oman 6,746.49 (0.5) (1.2) 0.3 (1.3) 16.93 24,428.2 12.0 1.7 3.9

Bahrain 1,472.07 0.4 0.1 3.1 17.9 1.82 54,100.6 10.7 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,900

12,950

13,000

13,050

13,100

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.6% to close at 13,067.3. The Consumer

Goods & Services and Industrials indices led the gains. The

index rose on the back of buying support from non-Qatari

shareholders despite selling pressure from Qatari shareholders.

Gulf International Services and Qatar General Ins. & Reins. Co.

were the top gainers, rising 4.9% each. Among the top losers,

Ezdan Holding Group fell 3.8%, while Qatari Investors Group

declined 2.9%.

Volume of shares traded on Monday rose by 31.0% to 21.5mn

from 16.4mn on Sunday. However, as compared to the 30-day

moving average of 30.5mn, volume for the day was 29.6% lower.

Vodafone Qatar and Barwa Real Estate Co. were the most

active stocks, contributing 21.9% and 10.1% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

MB Holding Co.

(MBH)

S&P Oman

LT CCR/ Senior

Unsecured $320 mn

Bond

B/B- B/B- – Negative –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency, CCR – Corporate Credit Rating )

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

Drake & Scull International

(DSI)

Dubai AED 1251.9 2.1% 54.3 -17.7% 40.3 -28.0%

Air Arabia Dubai AED 826.6 14.5% – – 71.7 29.4%

Alliance Insurance Dubai AED – – 5.7 1.6% 13.6 0.4%

Aldar Properties Abu Dhabi AED 1720.0 NA – – 453.4 193.8%

Umm Al Qaiwain Cement

Industries Co. (QCEM)

Abu Dhabi AED 3.0 -18.5% – – 22.7 30.3%

Ras Al Khaimah Poultry and

Feeding Co. (Rak Poultry)

Abu Dhabi AED 12.7 81.8% – – 13.6 2145.6%

Future Kid Entertainment &

Real Estate Co.

Kuwait KD – – – – -0.02 NA

Boubyan Petrochemical Co.

(BPC)*

Kuwait KD – – – – 27.3 4.2%

Amar Finance & Leasing Co. Kuwait KD – – – – -0.03 NA

International Resorts Co.

(IRC)

Kuwait KD – – – – -0.1 NA

Raysut Cement Co. (RCC) Oman OMR 24.8 -1.6% – – 8.2 0.7%

Gulf International Chemicals

(GIC)

Oman OMR 1.0 5.3% – – 0.1 17.8%

The Bahrain Ship Repairing

and Engineering Co.

(BASREC)

Bahrain BHD 1.1 -2.9% – – 0.4 28.4%

Bahrain Flour Mills Co.

(BFM)

Bahrain BHD 1.2 7.0% 0.1 NA 0.4 70.8%

Source: Company data, DFM, ADX, MSM (* FY2013 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/12 US US Treasury Monthly Budget Statement April $106.9B $114.0B $112.9B

05/12 France Banque De France Bank of France Bus. Sentiment April 98.0 99.0 99.0

05/12 UK Lloyds Bank Lloyds Employment Confidence April 1.0 – -2.0

05/12 China PBOC Money Supply M2 YoY April 13.20% 12.20% 12.10%

05/12 China PBOC Money Supply M0 YoY April 5.40% 5.50% 5.20%

05/12 China PBOC Money Supply M1 YoY April 5.50% 5.80% 5.40%

05/12 China NBS Aggregate Financing RMB April 1550.0B 1475.0B 2070.9B

05/12 China NBS New Yuan Loans April 774.7B 800.0B 1050.0B

05/12 Japan Bank of Japan Bank Lending Incl Trusts YoY April 2.10% – 2.10%

05/12 Japan Bank of Japan Bank Lending Ex-Trusts YoY April 2.20% – 2.30%

05/12 Japan Tokyo Shoko Research Bankruptcies YoY April 1.66% – -12.37%

Overall Activity Buy %* Sell %* Net (QR)

Qatari 64.64% 68.66% (41,478,179.36)

Non-Qatari 35.35% 31.35% 41,478,179.36

3. Page 3 of 6

05/12 Japan ESRI Eco Watchers Survey Current April 41.6 45.0 57.9

05/12 Japan ESRI Eco Watchers Survey Outlook April 50.3 40.0 34.7

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

ERES buys 20% stake in QIGD – Ezdan Holding Group

(ERES) has acquired more than 20% stake in Qatari Investors

Group (QIGD), its second acquisition in a month. ERES’ Deputy

Chairman Sheikh Abdullah bin Thani bin Abdullah al-Thani said

that the QIGD stake purchase is a significant move towards

diversifying ERES’ investments. QIGD, operates through 12

companies and 23 subsidiaries in different sectors such as

industry, trade and services. However, details of total acquisition

cost or the funding for this acquisition was not disclosed by the

group. (Gulf-Times.com)

QATI chosen sole insurance bond carrier for HIA – The

Qatar Civil Aviation Authority announced that the Qatar

Insurance Company (QATI) has been appointed as the

insurance bond carrier for the Hamad International Airport (HIA).

The state-of-the-art, world-class airport facility is fully insured for

a value of QR45.97bn. The Civil Aviation Authority said QATI

will be the sole insurance provider of the HIA. (Gulf-Times.com)

CBQK hires banks for $500mn bond sale – According to

sources, the Commercial Bank of Qatar (CBQK), has hired

banks to help arrange a potential dollar-denominated bond sale.

CBQK – Qatar’s second-largest lender by assets – has picked

Bank of America Corp, Morgan Stanley and HSBC Holdings for

a possible sale within the next month. The lender is seeking to

raise at least $500mn. Qatari banks are selling bonds as the

country raises funds to develop infrastructure projects in

preparation for the 2022 Soccer World Cup. Earlier in October

2013, QNB – the country’s biggest lender – had raised $1.5bn

from a two-part bond sale. (Gulf-Times.com)

ORDS launches new wholesale entity – Ooredoo (ORDS) has

established Ooredoo Global Services (OGS) as the group’s

wholesale arm. OGS will be the single point of contact for

wholesale carriers to access the company’s 18 operating

companies, representing one of the largest internet peering

networks in the Middle East that is interconnected with more

than 100 operators. The company has appointed Yousuf Abdulla

Al Kubaisi as the CEO for OGS. He previously served as

Ooredoo Qatar’s Chief Wholesale & International Officer since

2012. (GulfBase.com)

QFMA gets 4 IPO requests in 2013, nod only for MPHC –

The Qatar Financial Market Authority (QFMA) stated that it

received four requests for IPOs in 2013, but approval was given

only to Mesaieed Petrochemical Holding Company (MPHC). The

country’s equity market witnessed the advent of 247.2mn new

shares, leading to a total of 10.5bn listed shares, following

QFMA’s approval for capital increase of 13 listed companies. In

2013, the QFMA also received 11 requests for listing of

government treasury bills and three government bonds.

Besides, it also received three new requests related to

acquisition of Alternatifbank by Commercial Bank; Finansal

Kiralama by Al Salam Company and Mannai Corporation’s

acquisition of Gulf Laboratories. (Gulf-Times.com)

RLPC: Drinking water demand to rise by 138% in next 6

years – Ras Laffan Power Company-Qatar’s (RLPC) Managing

Director Mubarak al-Nasr said that the demand for drinking

water in Qatar is expected to increase by 138% in the next six

years, mainly due to economic growth and a rapidly rising

population. Al-Nasr recalled there has been a similar increase

(138%) in the drinking water requirements in Qatar over the last

six years. In 1997, water demand was only at 61mn gallons per

day (mlgd), which increased to 138 mlgd after 10 years. Since

then the demand has further grown to 328 mlgd in 2013. (Gulf-

Times.com)

International

US posts smaller budget surplus in April than forecast –

The US posted a smaller budget surplus in April 2014 than

economists expected, as spending increased at more than twice

the pace of tax receipts. The Treasury Department said

revenues exceeded spending by $106.9bn last month as

compared to $112.9bn surplus in April 2013. So far this fiscal

year, which began October 1, 2013, the country is running a

budget shortfall, which is about 37% smaller than it was a year

earlier and was the narrowest at the seven-month mark since

2008. Still, the economy nearly stalled in the January-March

quarter, while outlays rose last month on defense and

entitlement programs. (Bloomberg)

EU banks urged to boost capital prior to ECB stress tests –

European banks have been urged to boost their ability to

withstand losses before the conclusion of a stress test that has

been drawing criticism for its design. Axel Weber, the chairman

of Zurich-based UBS AG said that conducting stress-test on

banks that have depleted capital is similar to expecting a patient

recovering from a heart attack to pass a rigorous physical exam.

Moody’s Analytics Inc. said last week that the tests are not

internally consistent. The European Central Bank (ECB) is

leading the charge to prove that the region’s banks are robust

before it takes over their financial supervision in November. ECB

has forced an unprecedented Asset Quality Review and a

stress-test into its year of preparation, whose pressure has led

to some disquiet about the compromises needed to get the job

done on time. (Bloomberg)

PBoC: China’s new credit declines – China’s broadest

measure of new credit fell last month as authorities extended

their campaign to tame financial risks even as construction and

manufacturing data point to risks that the economy’s slowdown

will worsen. The People’s Bank of China (PBoC) said that

aggregate financing stood at CNY1.55tn ($249 billion) in April,

compared with CNY2.07tn in March. New local-currency bank

loans were at CNY774.7bn, down from CNY1.05tn the previous

month. These figures add to signs that officials are reluctant to

heed calls for monetary stimulus, with President Xi Jinping

stating that the nation needs to stay cool-minded amid what

analysts forecast will be the weakest annual growth since 1990.

The PBoC’s Deputy Governor Liu Shiyu said that shadow

banking threatens to undermine the financial system, even as

policy makers try to rein in credit. (Bloomberg)

Regional

MEED: GCC project awards could go up by 20% in 2014 –

According to MEED Insight, the value of new contract awards in

the GCC region is expected to rise by 20% to $178bn, a new

record for the region’s construction sector. MEED Insight Head,

Ed James said that the value of contracts awarded in 2013

stood at $147bn, while in 2012, it was under $120bn. James

said the near and long-term trend for the Middle East projects

market is now highly positive following a great 2013 and an even

better start to 2014. Driving this growth are high oil prices, as

well as strong economic and population growth. Although many

political, security and bureaucratic issues remain, the project

4. Page 4 of 6

gap across key sectors outweighs the obstacles. Kuwait, Oman

and Qatar could become significant growth markets. New

contract awards in the GCC so far this year has already reached

$60bn, with Kuwait being the largest market for new contracts

awarded in 1Q2014. (Peninsula Qatar)

GPCA: Petchem exports top $55bn in 2013 – According to

Gulf Petrochemicals & Chemicals Association (GPCA), GCC

countries exported approximately 79% of their total product

portfolio to 177 countries in 2013, amounting to 63.4mn tons of

chemicals, while petrochemical exports were valued at $55.5bn.

Mohammad Husain, Chairman of the GPCA Supply Chain

Committee said that the expansion and introduction of new land

and sea transport infrastructure would make the Gulf’s

petrochemicals industry more flexible. (GulfBase.com)

Mobily joins Etisalat's SmartHub to enhance internet

service – Etihad Etisalat Company (Mobily) has joined Emirates

Telecommunications Corporation’s (Etisalat) SmartHub, the

region's largest capacity and content hub in the Middle East.

Mobily will be part of the Etisalat's SmartHub IX community,

providing direct access to the largest content delivery networks

and streaming video services. This alliance will enhance internet

speed by providing direct access to some of the world's largest

content providers hosted in the UAE's Smarthub. Further, Mobily

recently connected its subscribers via Etisalat SmartHub IPX,

which enables 4G/LTE roaming services and mobile data

services. (GulfBase.com)

Emirates NBD: GCC emerges as strong investment

destination – According to Emirates NBD Wealth Management

CEO, Arjuna Mahendran, due to the changing global economic

outlook, most emerging markets are becoming less attractive as

compared to developed markets, while the Gulf region’s asset

classes retain their competitiveness. The GCC region remains

extremely robust, despite the ever-present threat of a decline in

oil prices in 2014. This is because all GCC countries continue to

build large external surpluses and have sufficient foreign

exchange and fiscal reserves to withstand a 10-20% correction

in oil prices. (GulfBase.com)

Saudi KFH invites subscription for initial issuance fund –

Saudi Kuwait Finance House (Saudi KFH) has launched

subscription for its first investment fund, “KFH Fund for Initial

Issuances” denominated in Saudi Riyal for one month till June

10, 2014. The fund seeks to achieve high returns by allowing

investors to primarily invest in the shares of public companies

during the IPO phase of their shares, or in the shares of new

listed companies that have been enlisted less than three years

ago. The fund is offered for SR10 per unit and is considered to

be a group investment program setup for investors who seek

real returns that compete against returns yielded by other

products that invest in enlisted shares. (GulfBase.com)

SABIC awards health insurance contract to BACI – Saudi

Basic Industries Corporation (SABIC) has awarded Bupa Arabia

for Cooperative Insurance (BACI) a contract to provide health

insurance for its employees and their families for one year

starting May 7, 2014. The contract revenues are expected to be

greater than 5% of the 2013 annual gross written premiums of

BACI and are expected to have a major impact on its 2014

financial results. (Tadawul)

SASCO opens investment portfolio – Saudi Automotive

Services Company (SASCO) has completed the transactions of

opening an investment portfolio managed by Saudi Fransi

Capital Company as per the Capital Market Authority’s (CMA)

approved portfolio management agreement. This investment

portfolio is aimed at diversifying resources of investments and

revenues. (Tadawul)

RSH to deposit proceeds from fractions shares – Red Sea

Housing Services Company (RSH) announced the completion of

selling fractions shares arising out of the company's capital

increase. The total number of shares fractions is 13,612 shares,

while fractions shares were sold on May 7, 2014 with a value of

SR836,177.63mn at an average price of SR61.50. The National

Commercial Bank will be depositing the fractions shares amount

into RSH’s shareholders account on May 19, 2014. (Tadwaul)

JEC to raise SR14bn for Kingdom City project – Jeddah

Economic Company (JEC) is in talks with Saudi-based banks to

raise funds for the first phase of its Kingdom City project worth

SR14bn and the world’s tallest tower. The owners have already

invested SR8.7bn in the project, while the remaining will be

financed by sale of land plots to other investors, as well as from

banks. BNP Paribas is acting as the financial advisor to JEC on

this transaction. The first phase of the project is spread over an

area of 1.4mn square meters, centered around the Kingdom

Tower, which is expected to be completed by 2018 and will cost

the company SR6bn. (GulfBase.com)

Al Tayyar signs deal with Jaadcar – Al Tayyar Travel Group

has signed an agreement with Jaadcar, a European luxury car

rental company. Al Tayyar’s customers can now avail

discounted packages from Jaadcar when they book car services

and also benefit from Al Tayyar’s end-to-end travel plans during

their travel. (GulfBase.com)

Flydubai plans more flights in Kingdom – Flydubai is

planning to further increase its flight frequency to Saudi Arabia.

Flydubai’s CEO Ghaith Al Ghaith said that the airline would aim

for 100 routes and 100 aircraft by 2020. Its operations to the

Kingdom began in 2010 and it serves 11 Saudi destinations

currently. (Gulfbase.com)

DIA’s passenger traffic to reach 70mn mark soon – Dubai

International Airport (DIA) is expecting passenger traffic to reach

the 70mn mark in 2014 despite the 80-day runway closure.

Sheikh Ahmed bin Saeed Al-Maktoum, President of the Dubai

Civil Aviation Authority, said that Dubai, which aims to increase

the aviation sector’s contribution to the GDP to 32% by 2020,

will continue to invest in aviation infrastructure to cater to the

anticipated growth in air passengers and cargo movements.

(GulfBase.com)

DI International to expand into Africa, Asia – Dubai

Investments International (DI International), the wholly-owned

subsidiary of Dubai Investments, is targeting investments, joint

ventures and strategic partnerships across Africa and Asia, and

also eyeing commercial projects in some Middle Eastern

countries. The company is in advanced stages of negotiations

with prospective business partners in Libya and Erbil in

Kurdistan, Iraq to build an industrial, commercial and residential

business park similar to Dubai Investments Park and replicating

the business model in the respective countries. (DFM)

Emirates to launch fifth daily flight to Singapore – Emirates

Airline announced that it will introduce its fifth daily flight

between Dubai and Singapore from August 1, 2014. This new

service will bring Emirates’ total number of flights between the

two cities to 35 per week, with 28 non-stop services and seven

flights via Colombo, along with to its daily services from

Singapore to Brisbane and Melbourne. In addition, Emirates

SkyCargo will operate belly hold cargo space to help transport

goods such as ship spare parts, mobile phones and various

other electronic goods to and from Singapore. (Bloomberg)

NBAD wins three awards – The National Bank of Abu Dhabi

(NBAD) has won three awards at the Banker Middle East

Product Awards 2014. The bank received awards for Best Cash

5. Page 5 of 6

Management, Best Corporate Advisory and Best GCC Equity

Fund. (GulfBase.com)

UNB posts AED512mn profit for 1Q2014 – The Union

National Bank (UNB) has reported a net profit of AED512mn for

1Q2014 as compared to AED495mn for 1Q2013, reflecting an

increase of 3%. Net interest income stood at AED563mn as

compared to AED508mn in 1Q2013. EPS remained at the same

level of AED0.16 at the end of March 31, 2014 as compared to

March 31, 2013. Bank’s total assets grew by 2% to AED89.6bn

at the end of 1Q2014 from AED87.5bn at the end of December

31, 2013. Loans and advances stood at AED61.7bn as at March

31, 2014, up by 6% YoY and by 3% over prior year end.

Customer deposits stood at AED66.7bn as at March 31, 2014,

lower by 2% YoY and up by 2% compared to prior year end.

(ADX)

Abu Dhabi helps RAK Islamic bonds despite S&P threat –

Abu Dhabi is helping Ras Al Khaimah's Islamic bonds to beat

peers even as Standard & Poor's (S&P) says there is a one-in-

three chance it will lower the credit rating of the UAE's fourth-

biggest member. According to data compiled by Bloomberg, the

Emirate's $500mn sukuk due October 2018 returned 2.9% in

2014, compared with an average 2.8% return for all dollar-

denominated sukuk. On May 9, S&P placed the borrower on a

negative outlook, citing slow progress in the development of

government institutions and a dearth of demographic and

economic data. The sovereign is rated A, which is three levels

lower than Abu Dhabi. (Gulf-Times.com)

Yiaco declares 5% bonus shares – Yiaco Medical Company’s

AGM and EGM have approved the distribution of 5% bonus

shares to the company’s shareholders. (Bloomberg)

Vale receives world’s largest iron ore carrier at Sohar –

Vale's operations in Oman has received its 50th Valemax

vessel, the world's largest iron ore carrier, at its deep water jetty

in the Port of Sohar, recording a total shipment of 25mn metric

tons of iron ore since commencing its operations in Oman in

2011. Valemax is a new concept category ore carrier with a

capacity to transport 400,000 metric tons and has alone been

responsible for the delivery of 80% of the iron ore shipments to

Oman from Brazil. Approximately $3.3mn is invested in

unloading the shipment and preparing the vessel for departure.

(GulfBase.com)

DCF appoints GM for support services – Dhofar Cattle Feed

Company (DCF) has promoted Ahmed Ali Qatan as the General

Manager for support services. (MSM)

Sun Metals awards $400mn Sur Steel Mill Project contract –

Sun Metals has selected Posco Engineering & Construction

Company as its technology partner to execute its 2.5mn tons per

annum (mtpa) capacity project at Sur Industrial Estate in Oman.

Additionally, Japan-based Sojitz Corporation will help Sun

Metals in the supply of raw material and the offtake of finished

products. Total investment in the venture is estimated at

$400mn. (Bloomberg)

Ithraa signs MoU with International Trade Centre – Ithraa,

Oman's inward investment and export promotion agency, has

signed a MoU with the International Trade Centre (ITC) along

with five other countries to facilitate the free access of low

income countries to an international database of import and

export markets. This initiation will help low-income countries as

well as exporters by providing them with access to detailed

analysis of current trade patterns, indicators, growth markets

and forecasts for future commerce. (Bloomberg)

BISB’s 1Q2014 profit surges 128% – Bahrain Islamic Bank

(BISB) has recorded a net profit of BHD2.5mn in 1Q2014 as

compared to BHD1.1mn in 1Q2013, reflecting an increase of

128%. This is after deduction of the required net provisions

amounting to BHD2.7mn. Net operating profit before provisions

stood at BHD5.2mn as compared to BHD5.1mn. The bank’s

total income stood at BHD10.6mn as compared to BHD9.9mn

for 1Q2013. EPS amounted to 2.68 fils as at March 31, 2014 as

compared to 1.18 fils a year earlier. Total assets stood at

AED885mn as at March 31, 2014 as compared to AED910mn

as at December 31, 2013. (Bahrain Bourse)

Invita to expand across GCC – Bahrain-based multi-lingual

contact center, Invita is planning to launch its operations in

Kuwait by 3Q2014. The company is further planning to expand

in Saudi Arabia, Qatar as well as Kurdistan in Iraq.

(GulfBase.com)

Diyar Homes awards contract to Al Hedaya – Diyar Homes

has awarded the construction contract for the second phase of

its affordable housing project located in Diyar Al Muharraq to Al

Hedaya Construction. The contract is for the construction of 196

affordable housing units targeted at Bahraini families.

(GulfBase.com)

Bahrain Bourse appoints CEO – Bahrain Bourse’s (BHB)

board of directors has appointed Shaikh Khalifa bin Ebrahim Al-

Khalifa as its CEO on May 11, 2014. Earlier, Shaikh Khalifa was

the Deputy CEO and COO of the bourse. Shaikh Khalifa joined

BHB in 2010 as the Deputy Director of the Settlement & Central

Depositary and IT. (Bahrain Bourse)

6. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (* Market closed on May 12, 2014) Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.1%

0.6%

(0.3%)

0.4%

(0.5%)

0.4%

1.5%

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

1.2%

1.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,295.83 0.5 0.5 7.5 DJ Industrial 16,695.47 0.7 0.7 0.7

Silver/Ounce 19.54 2.0 2.0 0.4 S&P 500 1,896.65 1.0 1.0 2.6

Crude Oil (Brent)/Barrel (FM

Future)

108.41 0.5 0.5 (2.2) NASDAQ 100 4,143.86 1.8 1.8 (0.8)

Natural Gas (Henry

Hub)/MMBtu

4.50 (1.7) (1.7) 3.5 STOXX 600 340.96 0.7 0.7 3.9

LPG Propane (Arab Gulf)/Ton 104.25 0.4 0.4 (17.6) DAX 9,702.46 1.3 1.3 1.6

LPG Butane (Arab Gulf)/Ton 119.25 (0.3) (0.3) (12.2) FTSE 100 6,851.75 0.5 0.5 1.5

Euro 1.38 (0.0) (0.0) 0.1 CAC 40 4,493.65 0.4 0.4 4.6

Yen 102.13 0.3 0.3 (3.0) Nikkei 14,149.52 (0.4) (0.4) (13.1)

GBP 1.69 0.1 0.1 1.9 MSCI EM 1,015.81 0.9 0.9 1.3

CHF 1.13 (0.2) (0.2) 0.6 SHANGHAI SE Composite 2,052.87 2.1 2.1 (3.0)

AUD* 0.94 0.0 0.0 5.0 HANG SENG 22,261.61 1.8 1.8 (4.5)

USD Index 79.90 (0.0) (0.0) (0.2) BSE SENSEX 23,551.00 2.4 2.4 11.2

RUB 35.09 (0.4) (0.4) 6.8 Bovespa 54,052.90 1.8 1.8 4.9

BRL 0.45 (0.1) (0.1) 6.7 RTS 1,234.31 0.1 0.1 (14.4)

187.8

154.3

140.4