Empfohlen

Weitere ähnliche Inhalte

Ähnlich wie RATIO 2015

Ähnlich wie RATIO 2015 (9)

RATIO 2015

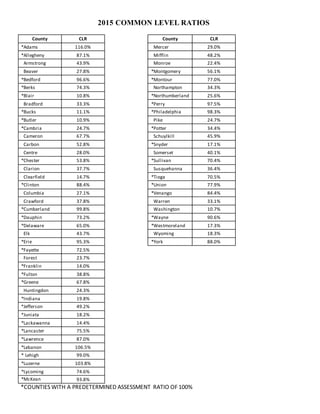

- 1. *COUNTIES WITH A PREDETERMINED ASSESSMENT RATIO OF 100% 2015 COMMON LEVEL RATIOS County CLR County CLR *Adams 116.0% Mercer 29.0% *Allegheny 87.1% Mifflin 48.2% Armstrong 43.9% Monroe 22.4% Beaver 27.8% *Montgomery 56.1% *Bedford 96.6% *Montour 77.0% *Berks 74.3% Northampton 34.3% *Blair 10.8% *Northumberland 25.6% Bradford 33.3% *Perry 97.5% *Bucks 11.1% *Philadelphia 98.3% *Butler 10.9% Pike 24.7% *Cambria 24.7% *Potter 34.4% Cameron 67.7% Schuylkill 45.9% Carbon 52.8% *Snyder 17.1% Centre 28.0% Somerset 40.1% *Chester 53.8% *Sullivan 70.4% Clarion 37.7% Susquehanna 36.4% Clearfield 14.7% *Tioga 70.5% *Clinton 88.4% *Union 77.9% Columbia 27.1% *Venango 84.4% Crawford 37.8% Warren 33.1% *Cumberland 99.8% Washington 10.7% *Dauphin 73.2% *Wayne 90.6% *Delaware 65.0% *Westmoreland 17.3% Elk 43.7% Wyoming 18.3% *Erie 95.3% *York 88.0% *Fayette 72.5% Forest 23.7% *Franklin 14.0% *Fulton 38.8% *Greene 67.8% Huntingdon 24.3% *Indiana 19.8% *Jefferson 49.2% *Juniata 18.2% *Lackawanna 14.4% *Lancaster 75.5% *Lawrence 87.0% *Lebanon 106.5% * Lehigh 99.0% *Luzerne 103.8% *Lycoming 74.6% *McKean 93.8%

- 2. June 29, 2016 The State Tax Equalization Board has established a Common Level Ratio for each county in the Commonwealth for the calendar year 2015. The ratios were mandated by Act 267-1982. The law requires the State Tax Equalization Board to use statistically acceptable techniques, to make the methodology for computing ratios public and to certify, prior to July 1, the ratio to the Chief Assessor of each county each year. The statistically acceptable technique which the Board used for the 2015 Common Level Ratio is to determine the arithmetic mean of the individual sales ratios for every valid sale received from the county for the calendar year 2015. The methodology used is to include every valid sale from 1% to 500% to compute an average mean. Using this average mean as a base, the State Tax Equalization Board has defined high and low limits by multiplying and dividing this computed average mean by 4. After the high and low limits are defined, the extreme upper sales ratio limit is 200%. Using these computed limits, the State Tax Equalization Board has utilized the valid sales, rejecting those sales which exceed the limits. The resulting arithmetic mean ratio is the ratio which the State Tax Equalization Board is certifying as the Common Level Ratio for each county for 2015. The Common Level Ratios for 2015 are listed on the back of this page. STATE TAX EQUALIZATION BOARD Peter Barsz, Board Chairman Daniel G. Guydish, Board Member Anthony Pinizzotto, Board Member Local Government Services – State Tax Equalization Board/Tax Equalization Division 400 North St., 4th Floor | Commonwealth Keystone Bldg. | Harrisburg, PA 17120-0225 | 717.787.5950 | F 717.214.5318 | newPA.com