Network operators innovate-or-die

•

0 gefällt mir•260 views

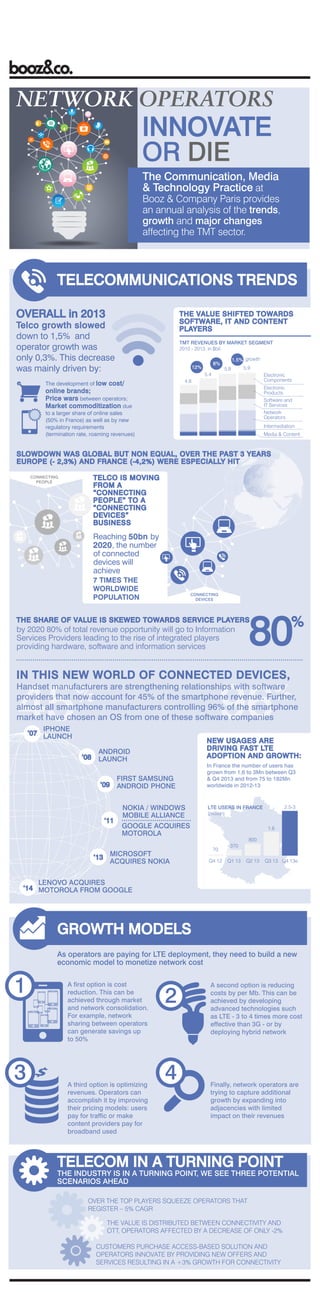

The Communication, Media & Technology Practice at Booz & Company Paris provides an annual analysis of the trends affecting the TMT sector. In the context of the growth in the Telco industry slowing down over the past 3 years, operators are facing a challenge: the value is shifting towards software providers and IT which oblige them to build a new economic model based on market consolidation, optimization of their pricing models, deployment of advanced technologies, diversification into adjacent markets. The entire industry is really in a turning point.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (18)

Ähnlich wie Network operators innovate-or-die

Ähnlich wie Network operators innovate-or-die (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Network operators innovate-or-die

- 1. NETWORK OPERATORS The Communication, Media & Technology Practice at Booz & Company Paris provides an annual analysis of the trends, growth and major changes affecting the TMT sector. OVERALL in 2013 THE VALUE SHIFTED TOWARDS SOFTWARE, IT AND CONTENT PLAYERS Telco growth slowed down to 1,5% and operator growth was only 0,3%. This decrease was mainly driven by: TMT REVENUES BY MARKET SEGMENT 2010 - 2013, in $bil. 8% 12% 5.4 1.5% growth 5.8 5.9 Electronic Components 4.8 The development of low cost/ Electronic Products Software and IT Services Network Operators online brands; Price wars between operators; Market commoditization due to a larger share of online sales (50% in France) as well as by new regulatory requirements (termination rate, roaming revenues) Intermediation Media & Content SLOWDOWN WAS GLOBAL BUT NON EQUAL, OVER THE PAST 3 YEARS EUROPE (- 2,3%) AND FRANCE (-4,2%) WERE ESPECIALLY HIT TELCO IS MOVING FROM A “CONNECTING PEOPLE” TO A “CONNECTING DEVICES” BUSINESS CONNECTING PEOPLE Reaching 50bn by 2020, the number of connected devices will achieve 7 TIMES THE WORLDWIDE POPULATION CONNECTING DEVICES THE SHARE OF VALUE IS SKEWED TOWARDS SERVICE PLAYERS by 2020 80% of total revenue opportunity will go to Information Services Providers leading to the rise of integrated players providing hardware, software and information services IN THIS NEW WORLD OF CONNECTED DEVICES, Handset manufacturers are strengthening relationships with software providers that now account for 45% of the smartphone revenue. Further, almost all smartphone manufacturers controlling 96% of the smartphone market have chosen an OS from one of these software companies IPHONE ‘07 LAUNCH ‘08 NEW USAGES ARE DRIVING FAST LTE ADOPTION AND GROWTH: ANDROID LAUNCH ‘09 ‘11 FIRST SAMSUNG ANDROID PHONE NOKIA / WINDOWS MOBILE ALLIANCE In France the number of users has grown from 1,6 to 3Mn between Q3 & Q4 2013 and from 75 to 182Mn worldwide in 2012-13 GOOGLE ACQUIRES MOTOROLA ‘13 MICROSOFT ACQUIRES NOKIA 2.5-3 LTE USERS IN FRANCE (million) 1.6 800 70 Q4 12 370 Q1 13 Q2 13 Q3 13 Q4 13e LENOVO ACQUIRES ‘14 MOTOROLA FROM GOOGLE GROWTH MODELS As operators are paying for LTE deployment, they need to build a new economic model to monetize network cost 1 3 A first option is cost reduction. This can be achieved through market and network consolidation. For example, network sharing between operators can generate savings up to 50% A third option is optimizing revenues. Operators can accomplish it by improving their pricing models: users pay for traffic or make content providers pay for broadband used 2 4 A second option is reducing costs by per Mb. This can be achieved by developing advanced technologies such as LTE - 3 to 4 times more cost effective than 3G - or by deploying hybrid network Finally, network operators are trying to capture additional growth by expanding into adjacencies with limited impact on their revenues TELECOM IN A TURNING POINT THE INDUSTRY IS IN A TURNING POINT, WE SEE THREE POTENTIAL SCENARIOS AHEAD OVER THE TOP PLAYERS SQUEEZE OPERATORS THAT REGISTER – 5% CAGR THE VALUE IS DISTRIBUTED BETWEEN CONNECTIVITY AND OTT, OPERATORS AFFECTED BY A DECREASE OF ONLY -2% CUSTOMERS PURCHASE ACCESS-BASED SOLUTION AND OPERATORS INNOVATE BY PROVIDING NEW OFFERS AND SERVICES RESULTING IN A +3% GROWTH FOR CONNECTIVITY