Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (16)

Ähnlich wie Mad Mad Money Mar 2017

Ähnlich wie Mad Mad Money Mar 2017 (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Mad Mad Money Mar 2017

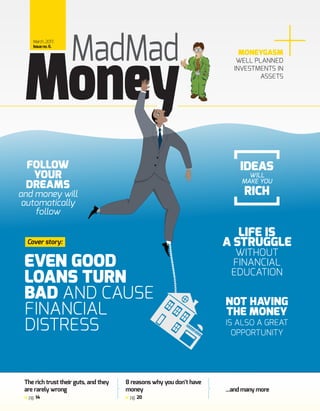

- 1. MONEYGASM WELL PLANNED INVESTMENTS IN ASSETS ...and many more 8 reasons why you don’t have money pg. 20 The rich trust their guts, and they are rarely wrong pg. 14 EVEN GOOD LOANS TURN BAD AND CAUSE FINANCIAL DISTRESS MadMadMarch,2017, Issueno.6. Cover story: Money LIFE IS A STRUGGLE WITHOUT FINANCIAL EDUCATION NOT HAVING THE MONEY IS ALSO A GREAT OPPORTUNITY IDEAS WILL MAKE YOU RICH FOLLOW YOUR DREAMS and money will automatically follow

- 2. Content 14_ Ideas will make you rich 16_Follow your dreams and money will automatically follow 18_5 unbelievable money habits that millionaires have! 20_ Life is a struggle without financial education 22_ Moneygasm 24_ If you want to be considered successful, invest in experiences 26_The rich trust their guts, and they are rarely wrong 28_ 8 reasons why you don’t have money Money Mad Mad Issue no.6 Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form of by any means electronic, mechanical, photocopying, recording or otherwise, without the permission of MadAboutMoney magazine. All information in MadAboutMoney magazine is checked and verified to the best of the publisher’s ability, however the publisher cannot be held responsible for any mistake or omission enclosed in the publication. 0812 10 Even good loans turn bad and cause financial distress Your cars and gadgets are not assets They are eating your money Paying debts through debts can make a deep hole Cover story: 06Not having the money is also a great opportunity 2

- 3. Money Mad Mad Editor’s Note 3 Welcome to this edition of Mad Mad Money! Last edition we talked about how an individual’s mentality and attitude matter when it comes to being successful and getting rich and what kind of money mindsets we need to inculcate in order to make it really big in life! This issue we will be looking more at the unique personality traits and habits that rich people have and the various tools that will helps you towards achieving those! So, while the previous issue was more about concepts, this issue fundamentally looks at how to get those concepts into practice in real life. What are the avenues via which the conceptual mindset gets channelized into real life habits and personality traits that ultimately work towards getting you to where you deserve to be!Starting from the habits that rich people have, to the dreams that they see, the way they generate their ideas to the faith they have on their instincts, the role financial education plays to their traits of dealing with debts, from how they buy their houses and cards to anything and everything about the rich that you always wanted to know, this issue is bound to be an extremely interesting read with a range of topics that has vast opportunities to learn from! My question to you all would be that we are all mad about money, but to what extent is your madness? How mad are you to make money? This defines how one’s destinies are finally crafted. Are we ready to unlearn our pre-existing thoughts and habits and inculcate the new to become something and someone in life? Do we have what it takes to learn about the rich and inculcate the same passions? Mad Mad Money is here to talk about everything to do with money that draws your attention and passion, but in a different way, with a slightly different touch… that unique magic wand of mindset change that just makes all this attainable in practical terms. Simply put, if taken in seriously and internalized with sincerity, it holds the power to change lives and destinies. Are you up for it? Keep reading and keep getting rich! Sachin Mittal

- 4. The Mad Gang who makes it possible every month Vijendra Singh, Manager Money Craft Giving a tight twist to money Swadesh Mishra, Officer Out-standing The world in his pocket Shravan Giri, Creative Technologist Tech at his fingertips Anubha Rathore, Arts & Crafts Designer Designer craft creator Rajiv Ranjan, Joint Creative Technologist Joining forces in troubleshooting Dheeraj Kumar, Chief Money Scientist Sees the glass half full Money Mad Mad 4

- 5. Akanksha Mishra, Associate Money Scientist Hopefully optimistic Abhijit Banerjee, Idea Ambassador An idea for a song… Johny Chopra, Buzz Ambassador Spreading the good word Ahmed Ansari, Lord of the Ledgers Tight fisted…always Soma Ghosh, Chief Buzz Creator Creating the big buzz Dillip Rout, Account-ability Officer Wire | Digital Creative AgencyMagazine designed by: Money Mad Mad 5

- 6. Money Mad Mad 6 Sounds strange, doesn’t it? How’s this statement even be true you must be thinking? All of your lives you must have heard that money is the most important tool you must have if you want to get rich and successful. But let me tell you today, even if you have less or no money, it is still a great opportunity for you to be even more successful in life. Not having the money is also a great opportunity

- 7. 7 Money Mad Mad N ow let’s look at how is this possible. Most of you know that money attracts money, and to have a good return, you always must make good investments. Well, it’s true for the people who already has inherited or made money. What about those who doesn’t have either? Does that mean the later can never make money because they don’t have lots of it now? It’s quite the opposite actually. LESS MONEY MAKES YOU MORE CREATIVE Combine your lack of money with large amount of motivation and inspira- tion, and you will generate an endless stream of creativity. And that is your first step towards succe- ss. When you have fewer funds, you have to think of lots of scenarios to make a single situation work. It will force you to re-think your strategies and brainstorm about different approac- hes. You will start talking to your peers and friends about these ideas and start getting a lot of perspecti- ves from them, which will further help you to stren- gthen your idea. Folks with money generally think they have the upper hand and they lack trusted people around them. So, most of the time they put their mo- ney without brain-storming much and that leads them to invest into wrong areas most of the time. So you see, you have the upper hand without money, rather than someone who does. LESS MONEY MAKES EVERY PENNYVITAL Having less or no money, means every little bit of your money is important to you. You know the “worth” of the money you have with you and you will think hundred times before you spend or invest it somewhere. I have heard from a lot of people who has made/inherited money easily that they have spent a lot of money on things they didn’t need or want in the first place. They got pulled in diffe- rent direction, listened to so-called experts, and lost a lot of their money. I’m not talking only about blowing money on mate- rialistic things or partying, I’m also talking about all those business expenses that weren’t necessary in the first place. People are always looking for deep pockets and finding a way to rob them. This gives you an edge above others. Ha- ving lesser funds means you will think and re-think hundred times before making a purchase or an investment, and that is a good thing. Not only you will be making a right cho- ice, you will also be saving a lot of money because you have really thought about your strategies. And that saved money will ensure more investments in the future. YOU WILL MAKE GREAT FINANCIAL PLANS Remember, “Failing to plan is planning to fail.” Before you start looking for an opportunity to start a business or a career, planning must be your major goal. Money is not the only thing required to start something, there is so much more that goes into it. Let’s say, for example, you want to start a new business. What you require most is a business model, a business plan, an objective, the marke- ting plan, the strategic partners, the customers, the providers, the list goes on. All these things require proper planning even if you “do” have the money. So why wait till the time you have the money, start planning anyways. Start planning now! All the above pointers must stop you from thin- king that money is such a huge limitation to go ahe- ad. Build a solid strategy today, so that when the money comes in, you will be more successful. Remember, “Failing to plan is planning to fail.”

- 8. Money Mad Mad 8 Even good loans turn bad and cause financial distress F irst of all, a loan is a loan. A liability. Yes, you can argue that there are good loans and bad loans, the ones which you take to invest in some asset including your own development that would pay returns in the future vis-a-vis the ones you take for entertainment and travel which are nothing but just blowing up money without any returns. I take your point, but still…loans are loans and even good loans can turn bad and cause financial distress.

- 9. Money Mad Mad 9 3. DURATION OF LOANTERM: If the amortization of a loan goes on for more than what it was permitted then it becomes a bad loan by default and the entire loan amount is a deemed distribution. For example, if a plan issues a loan for more than 5 years, and that is anyway the regulatory limit, then this defect cannot be solved by plan amendment for longer amortization. However, if a plan chooses to limit all loans to 5 years and then issues a particular loan, let’s say a residential loan for more than that duration,than there is scope for plan amendment. 4. NON-STARTED PAYMENTS: Sometimes a loan is taken that would be repaid later on by regular deductions form payroll. Common example would be an educational loan. However, lets say, the payrollsystem was not set up or it somehow does not deduct the same. So the loan goes to default. This does not make the entire loan amount defective though, the payer has till the end of the period to make it up to date to avoid deemed distribution. 5. PAYMENTS DISCONTINUED: Lastly, in some circumstances, when a person can no longer afford to make loan payments he/she asks the company to stop with holding, either on a temporary or a permanent format. The company might or might not abide by the request. Even if they do in order to help out its employee, the loan is very much default and might become a deemed distribution. Even though loan takers borrow from his/her own account balance, but for the loan plan, it is still an asset. So by voluntarily discontinuing, the plan is basically failing to ensure the pre-determined legal agreement between the plan and the borrower, reducing the plan asset to decrease in value. So for all the above cases we see how a good loan may turn into abide one. Hence financial education and thereafter financial planning is crucial to avoid loans in the first place and even if going for a loan, to take into consideration all that which might suddenly turn it into a bad one! YOU MIGHT BE APPLYING FOR A LOAN WHICH IS CATEGORIZED AS GOOD AND MAYBE PLANS ARE NOT REQUIRED TO START WITH. BUT ONE MUST BE SURE THAT THE NECESSARY PROVISIONS FOR LOAN APPROVAL ARE INCLUDED IN THE PLAN. How can good loans go bad? Here are a few examples: 1. WHEN LOANSARE NOT PERMITTED: You might be applying for a loan which is categori- zed as good and maybe plans are not required to start with. But one must be sure that the necessary provisions for loan appro- val are included in the plan. Plan sponsors might be just approving your plan without taking the effort to see to the amendments required in it. However, issuing a loan where in reality the plan does not allow it can turn into a bad loan since the loan amount is immediately deemed as distributed. 2. WHEN REFINANCING OF ALOAN IS NOT PERMITTED: Many a times home owners wish to change or modify their loan or get it refinanced. Not all plans permit refinancing and also most of the times the inability to refinance is also not very clear. Long story short, when refinancing does not get permission, your good loan might just turn into a bad one.

- 10. Money Mad Mad M eet Anita, middle- aged, confident, well-to-do urban wife, mother and hard worker. At this point in her life she is in a happy and well placed position in her society. Her colleagues and friends admire her most fondly and many wishes to live her life just for one day. But the truth is all of this is a façade, if she rips her mask of stability and good life, what her friends and admirers would see is a deep dark secret. A secret that unveils the fact that Anita and her husband is living dangerously close to the edge, completely drowned in debt. Does this sound familiar? Has this happened to you or someone you know? Because people like Anita are everywhere, drowning in debt and can’t get out of it. And do you know what’s the reason behind getting so deep in debt that you can’t even breathe? More debt. Yes, it’s as simple as that, if you incur more debt to cover previous debt, you are making the worst mistake of your life. THE SHAME: A lot of you are living in debts of varying amount. Some of you might have a debt of a year paying through your credit card for a smartphone, some of you might have a sizable home or business loan that will take years to cover. But a lot of you are in a condition of being in a debt that has snowballed to such an extent that it is impossible to repay it in your current circumstances. What you then feel is “shame”. The shame comes from the fact that you are now in a certain position in the society where people admire and respect you. For that you have taken a loan, and now the loan is unpayable and you take more loan to maintain that position which in turn makes your debt more overwhelming. So, the “shame” basically makes you more vulnerable to take more debt so that your status-quo in society is maintained. THE PAIN: What happens after getting stuck with a sizable debt is banks and other financial organiza- tions providing you “easy way out”. And that is just PAYING DEBTS THROUGH DEBTS CAN MAKE more loans. Now, you are already feeling the “shame”, you are weak and edgy, what you do is accept the loan and make your situation even worse. The “pain” part of your life begins as you go deeper and deeper into debt without a proper plan to get out. THE SOLUTION: The solution is actually quite simple. All you need is to have a timely wa- ke-up call. What you need to do is firstly don’t take debt you can’t handle. No matter how much you get seduced by “upper-class” living and have an urge to buy things you can’t afford, stop yourself there. Take a loan when it’s absolutely necessary, don’t take a loan just for the heck of it, no matter how easily it’s available to you. And even if you do, don’t take another loan to cover the first one, pay one loan fully and then go for another. A DEEP HOLE 10 Do you know what’s the reason behind getting so deep in debt that you can’t even breathe? More debt. Yes, it’s as simple as that, if you incur more debt to cover previous debt, you are making the worst mistake of your life.

- 11. 11 I’M NOT SAYING DON’T GO AHEAD IN LIFE AND CHOOSE TO LIVE FRUGALLY. I’M JUST SAYING TAKE A LOAN WHEN IT IS RIGHT FOR YOU, DON’T STRETCH YOUR LIMITS. COVER YOUR BASICS FIRST, EARN SOME EXTRA, HAVE A MORE OR LESS STEADY FINANCIAL FUTURE, THEN GO FOR A LOAN. AND MORE IMPORTANTLY, PAY THE FIRST LOAN AND BE OUT OF DEBT BEFORE YOU JUMP INTO ANOTHER DEBT, BECAUSE THAT IS WHAT IS GOING TO CREATE A DEEP HOLE YOU CANNOT COME OUT OF. WHAT YOU NEED TO DO IS FIRSTLY DON’T TAKE DEBT YOU CAN’T HANDLE. NO MATTER HOW MUCH YOU GET SEDUCED BY “UPPER-CLASS” LIVING AND HAVE AN URGE TO BUY THINGS YOU CAN’T AFFORD, STOP YOURSELF THERE. Money Mad Mad

- 12. Money Mad Mad 12 ASSETSVS ‘PERSONAL BELONGINGS’ – KNOWINGTHE DIFFERENCE Confused? Don’t be. The reason these are not considered as an asset is actually quite simple. Your car is not an asset is be- cause it does not yield you any income or appreciate in value. The same goes with all your expensive gadgetries. So, unless you are running a well-perfor- ming taxi service or a cyber café, these things are definitely not keeping your money safe, it is actually eating through it. Finan- cially speaking, your car or your gadgets will not be termed as an asset, they will be termed as “personal belongings”. Now let’s get YOUR CARS AND GADGETS ARE NOT ASSETS THEY ARE EATING down to the real reason why your car or your gad- gets are not assets for you. The obvious and basic re- ason why your car or your i-phone is not an asset is it depreciates in value every second of every day and driving and maintaining it is eating away your wallet. For example, your car is constantly devouring your cash due to its constant maintenance, fuel, insu- rance and other things. You can actually buy a property with the money you are spending in keeping a car and that makes more sen- se because a real estate is actually going to apprecia- te in value. INVESTING IN ASSETS OR INVESTING IN CONVENIENCE? You might argue that how can a car or a gadget not be an asset when you can always sell it and get cash in return? You have to understand that your cash in the bank is actually your asset, the intention of selling the car or the gadget, which may or may not happen, cannot be an asset. You might also argue that you might use the car or say an expen- sive laptop and borrow it against some investment purposes. In this case as well, the investment you do becomes asset, not your car or your laptop. Some of you also may ar- gue that in your nature of work your car saves a lot of time and you can visit many clients in the same day, or say your expensive laptop helps you multita- sk faster, so you deem it as an asset. You have to understand that I am not against the convenience of your car or your laptop. Your car might take you to a lot of places, or your lap- top might help you work faster, and both of these activities might help you earn more money, and you can invest that money into meaningful places. Again, the investment you are doing is actually your asset, not your car or your laptop. The convenience only helps you to invest more, which is the asset you are building. THE SENSE OF SE- CURITY– REALOR FALSE? Do understand that I am not against having a car or nice gadgets, I under- stand the convenience it provides you. I am just trying to remove the false sense of security you are brooding in your mind, thinking your cars and your gadgets are actually assets, which they are not. It is also deluding you in thinking you are “doing well” because of the kind of car you are driving or the kind of smartphone you are using. To maintain the image, you might be spending more on a car or a gadget you don’t need and might use it to invest somewhere else. You are also spending a lump sum annually to maintain your car and your gadget, whi- ch again you can save to invest wisely. Be wise, stop and think. Put your money in the right place! This might come to you as a bitter shock, but the fact of the matter is the statement is 100% accurate. Your car, your super-cool smartphone, your smart watch, your expensive laptop, is not in any way can or will be considered as an asset. These things will never be an asset to you, what it will actually do is burn a hole in your pocket. YOUR MONEY

- 13. 13 Money Mad Mad

- 14. Money Mad Mad 14 T oday, instead to telling you to “find the right idea”, I will tell you how you can identify, validate, and test your own idea, that will eventually make you rich. Instead of telling you to figure out a popular money making idea in the market, I’ll tell you to find your own idea and make FROM WHAT I SEE EVERYDAY, I FIND THAT THE NUMBER ONE PROBLEM OF MAKING MORE MONEY TO GET RICH IS FINDING THE RIGHT IDEA. YOU EITHER HAVE ZERO IDEAS OR JUST TOO MANY OF THEM, OR MAYBE YOU DON’T KNOW WHERE AND HOW TO START. TODAY I’LL TALK TO YOU ABOUT HOW TO IMPLEMENT A HABIT OF GENERATING THE RIGHT IDEA THAT WILL GET YOU TO CLIMB THE SUCCESS TRAIN. it a profitable one. The one idea that is already there in the market, or someone you know is “their” ides which might or might not work for you. Why not use your own, to create your own success? As I said ear- lier, there are two main barriers for you to make a “money making” idea: IDEASWILL MAKE YOU RICH You can’t identify an idea at all You have too many ideas and don’t know where to get started Remember, to break down these barriers and acquire the right money-making idea requires you to meet 4 criteria:

- 15. 15 Money Mad Mad Criteria 1: SHOWCASE YOUR SKILLS: This one’s most important. Your money- making idea should match with what skills you currently have. No matter who you are, you have skills. Skills you are born with, skills you have learned in school, office, college wherever, just remember that all these skills are important. You can be either good at math, or a particular language, or in good shape or have a persuasive way to speak to people. All these are skills. And you need to be face-to-face with them. How? Simple. Take a paper and pen and time with yourself and jot down your skills. That’s the first step. Criteria 2: SHOWCASE YOUR STRENGTHS: Your money-making idea must highlight your strengths. Strengths are the qualities which make you stand out of the crowd of people who may have the similar skill sets. How to find your strength? Again, sit with the list of your skills you have jotted down and figure out, among all the skills which skills you have the most strength. Once you have done that, you are ready to proceed to criteria 3. Criteria 3: MATCH YOUR INTEREST: Your money-making idea must match your interest otherwise you won’t stick to that idea for long. You have make sure that your strength which you have derived from your skills must match your interest quotient. You are gene- rally passionate about your interest, so you will work hard to generate your idea because that passion will keep you going. Remember, it’s not just the job, it’s somet- hing you love to do. Criteria 4: HAS AN ACTUAL MARKET: After you figure out to break through the third criteria, you must make sure that your interest area from where you want to make money, must have a tangible market as well. In other words, people should be ready to shell out money to attain your services. The idea will only make sense if there is a real market for it, people who are willing to pay for your product or service. Once all these criteria are met, and all these tick boxes are checked you can validate that your idea is a money-making one and with the right amo- unt of passion and work ethics you can reach the pinnacle of success.

- 16. Money Mad Mad 16 FOLLOW YOUR DREAMS AND MONEY WILL AUTOMATICALLY FOLLOW PEOPLE DO NOT CARE ABOUT HOW MUCH MONEY YOU HAVE. WHAT THEY CARE ABOUT IS HOW YOU MADE IT,

- 17. 17 Money Mad Mad M oney is perhaps the most fantastic resource to have, being rich and making it big in life being the epitome of success. But having experienced both poverty and wealth, from experience I can tell you that if one is focused on making money he/she usually doesn’t make it ever. You need to follow your dreams and channe- lize your passion. Money will automatically follow. Yes, that’s my secret of being rich and in this ar- ticle I’m going to tell you 4 concrete reasons for it! 01 REACHINGYOUR DREAM CAN GENERATE MONEY AUTOMATICALLY This point is rarely un- derstood. See, when you have a dream and you go for it forgetting everything else, chances are that you will eventually succeed. Now, when you have a dream and succeed in that, essentially you would be creating value, value for others, and that gives you the scope to generate money. So you need to dream big in order to generate money. Don’t be bogged down by self-doubt. The skills to attain the dream can always be acquired but the point is to change your mindset, dream big and go for it! 02 MONEYCOMES AND GOESATTHE BLINK OFAN EYE Sad but true. The hard truth is that money can go as quickly as it comes. So it is always better to be focused on your dream rather than the money per se. What I mean is, your mindset should be tuned towards creating value and not making money. If it’s not that way, then even if you were to win a lottery, yet do not possess the mindset to create value, then the money would drain out pretty soon! 03 MONEYSTATUS DOES NOTREALLY MEANANYTHING Yes, your money status is actually useless, to put it bluntly. People do not care about how much money you have. What they care about is how you made it, the impossible fe- ats you have achieved, the kind of person you beca- me, what you did with the money, how much value you created, etc. Simply put – they care about how successful you are. And the definition of real success is not just making money but a whole lot of other factors along with the money part. Hence, just focusing on making money would never make you successful. Achieving your dream can. When Richard Branson comes in, people recognize him and look at him not because of his money but because they are impressed by the number of dreams he has achieved. Long story short, millions of dollars doesn’t necessarily create social status. Social status increases from your obse- ssion with value creation. MOST OF US USUALLY SPEND OUR ENTIRE LIVES IN THE RAT RACE OF MAKING MONEYAND UNKNOWINGLY FALL INTO THE MONEYTRAP. DON’T GET ME WRONG, I DO NOTASCRIBE TO THE ‘MONEY IS EVIL’ LOGIC ATALL! IN FACT I THINK LACK OF MONEY IS THE ROOT OF ALL EVIL. 04 MONEYDOES NOT CREATE HAPPINE- SS OR MEMORIES This might sound phi- losophical but it is definitely one of the most crucial reasons for chasing a dream instead of money. When you see rich people driving fancy cars, living in luxury apar- tments, does it necessa- rily tell you that they are happy in life when they go to bed each night? Facebook and Intagram image perceptions often hide many a rich but lonely and unhappy souls. Making money has never and cannot make memo- ries or create happiness. But if you are chasing a dream and focusing on it forgetting everything else, cross all hurdles to achieve it and make lots of money in that process, the feel of achievement, the inner happiness and self-worth of having crea- ted value is unimaginable. So Dream Big. Achieve. Earn. Make Memories. Be Happy – My Mantra. Stop chasing money dude, cha- se your dream instead!

- 18. 5 unbelievable money habits that millionaires have! 18 S ounds unbelievable right? But it’s true! In fact, that’s exactly how they became millionaires in the first place! Some normal people like you and me who maintained a frugal lifestyle, planned their budgets, invested wisely and most importantly, developed a positive mindset about money and wealth. That’s exactly their secret to success! Given below are the top 5 surprising money habits that millionaires possess that anybody can follow to become rich and successful in life! 1. GOALSETTING: From surveys by experts it has been found that more than two-thirds of millionaires set goals for themselves on a regular basis. These are daily goals, weekly goals, monthly goals, annual goals as well as long term goals for their life. This is one of the most common habits that most millionaires possess. A sure shot way to effective and efficient time management that lets you achieve the most in a short time! According to motivati- onal speaker Zig Ziglar, one should fix goals for all the areas of one’s life and then work towards making them happen! 2. WISE SPENDING: Surprisingly, for most millionaires, financial independence is actu- ally more important than status. So most of them spend wisely rather than buying expensive stuff all the time. What I mean is, that what they buy mi- ght seem very expensive to you but to them, from their level, its modest Money Mad Mad UNLIKE THE USUAL IMAGE THAT WE HAVE ABOUT MILLIONAIRES IN OUR MINDS, WHICH INCLUDE EXTREMELY WELL GROOMED MEN AND WOMEN IN LUXURIOUS CLOTHES DRIVING LAMBORGHINIS AND HAVING CAVIAR, MILLIONAIRES IN REALITY ARE OFTEN FOUND DRIVING JUST RELIABLE CARS AND EATING MASHED POTATOES AND SAUSAGES!

- 19. From surveys by experts it has been found that more than two-thirds of millionaires set goals for themselves on a regular basis. 19 and they could have bought something more expensive. But most of them don’t. This is one of their secrets of success which usually people do not understand. From my own experience, I would like to make the point that one should never buy things to show off or impress other people. But things which you really want, need and have saved up for which you would actually use in reality. 3. BUDGETING &TRACKING EXPENSES: Everyone should budget and that includes milli- onaires. There’s hardly a millionaire who does not possess the habit of budgeting and then tracking their spending on a monthly basis. If you ask any one of them, they know exactly what portion of their money is going where at any given point in time. My tip on this would be, create a budget at the beginning of the month and track your spending through it as days go by, making adjustments whenever needed. 4. SAVING AND INVESTING: Again from the surveys it has been found that milli- onaires invest 20% of their income. Also, while most of them have various inve- stment accounts, they are never on auto mode or on the hands of investment advisors. Millionaires keep control on their own inves- tments and take their own decisions. 5. MODESTCARS: As unbelievable as this may sound millionaires do buy modest cars. Again, the ‘modest’ is not in your terms but in their and you need to understand that. They could have bought cars which are too expensive for them but usually they don’t. My advice would be to save up and buy a car that you can afford and drive for a long time! To conclude it can be said that millionaires are never millionaires for their luck…they are rich because of certain habits and precisely the ones mentioned above! Money

- 20. Money Mad Mad 20 Y ou might acquire 4 degrees from 4 different colleges yet you might not know about personal savin- gs and how to manage loans. You might be a doctor or a lawyer with an open practice yet you might not have a clue about how to read a financial document. Point is, what you must acquire today is a solid financial education otherwise you will be struggling to make and keep money thro- ughout your life. This is hardly a suggestion, this is a must-take advice I’m gi- ving all of you. Be financia- lly educated, and if you are not, start today.The best investment you can make is on yourself and your financial education. It’s the starting point to building wealth and be successful. So, what makes financial education so important? How will financial educa- tion benefit you? Here is a list of reasons: Financial education will help you make the right choice: If you are unaware of finance and how it works, you will always be struggling with money. You will be exposed to a lot of financial advices from others and it will be very difficult for you to choose the right one. All those financial “experts” would easily dupe you to make a wrong choice about investing somewhere that’ll profit them rather than you. So, if you’re financially educated, you have less chance of being duped and make your own investments in the right places. Financial education will help you build a custom wealth plan: Every financial advice in the market is not one-size-fits-all. Every person is different, so is their skills and strengths and so is their TOUNDERSTANDTHIS,YOUMUSTFIRST REALIZE THAT FINANCIAL EDUCATION IS VERY DIFFERENT FROM YOUR COLLEGE OR BUSINESS SCHOOL EDUCATION IN MANY WAYS LIFE IS A STRUGGLE WITHOUT FINANCIAL EDUCATION

- 21. Money Mad Mad 21 wealth plan. You must have a wealth plan that is custom-fit to your induvial need and aspirations. It certainly is a struggle for someone to build a wealth plan that’ll help them reach their goals if they are financially educated. Don’t be that someone, get the right financial education and build your custom wealth plan. Financial education helps you achieve financial security Remember you are responsible for your financial decisions, no one else. You might hire loads of financial experts and market gurus but fact of the matter is you are the one who’s shelling out the money at the end of the day, making you responsible for your financial security. You have to be financially educated to take important investment decisions that would ensure your financial security. Your financial education acts like a ceiling that limits your growth of wealth. As and when you keep on educating yourself more and more, your ceiling starts to raise higher and higher and so does your wealth. Your financial education sets the context for your financial success. You cannot make a million rupees with thousand rupees worth of financial education. So, as you raise the bar of knowledge, you raise the bar of your wealth as well. Financial education is not just something you learn once and use that knowledge forever. You keep on learning more and more as the market and opportunities grow around you. If you haven’t started to financially educate yourself yet, start now, it’s the best thing you can invest on yourself. Financial education tells you how you can use the taxation policies in your favor and how to avoid the bad debt and use good debt to your financial advantage. Financial education helps you reach greater financial goals:

- 22. Money Mad Mad 22 Some common investment options in assets include: Real Estate – Rent from property Inventions – Royalty from Patent Brand Creation – Fees from Trademark Licensing Original Works – Royalties from original works such as books, songs, other publications. Business – Profit from business which does not need your day-to-day efforts Online – Advertisement income from website/blog you might own Market - Dividends from Stocks, mutual funds and other securities WELL PLANNED INVESTMENTS IN ASSETS SITUATION Think about the situation where passive income gets generated on a regular basis without your effort going in, so you can spend all your time in doing what you actually want to do in life! Wouldn’t be truly moneygasmic! Now this kind of passive income is only possible by well planned investments in Assets. Hence for people who are engaged in providing direct labour in service now, without hereditary income or property, is to invest a substantial portion of your current income into assets and do it in a well planned and regular way so that after a certain duration of time it generates considerable amount of passive income for you. A TRUE MONEYGASMIC SITUATION IS COMPLETE FINANCIAL INDEPENDENCE WHERE A SUBSTANTIAL PORTION OF YOUR INCOME FLOWS IN NOT AGAINST YOUR DIRECT LABOUR BUT PASSIVELY, AGAINST YOUR INVESTMENTS IN THE ASSET CLASS.

- 23. Money Mad Mad 23 HAVING MULTIPLE INCOME STREAMS IS AS GOOD AS HAVING MULTIPLE ORGASMS! NO WAIT, ITS EVEN BETTER! HAVING MORE THAN ONE INCOME FLOW IS TRULY MONEYGASMIC TO SAY THE LEAST! MULTIPLE INCOME STREAM SITUATION Most people work their guts out, get exploited by doing overtimes with massive workloads and remains constantly under pressure simply because they have just that one job, one business or basically just one means to earn their livelihood and feed their families. Not keeping all your eggs in one basket and instead, having different types of strong and sturdy baskets which you generously redistribute your eggs in, is the moneygasmic situation at its best! Making Multiple Income Stream Situations truly Moneygasmic, include: 1. Having more than one stream of income. The best combination is to have a steady income from an occupation/job along with a business that follows your passion as well as income from assets/investments 2. Having different income streams reflect different kinds of portfolio so that if the market goes down one averages out the loss of the other. For example, if you have investment in stocks and mutual funds, distribute your money over different sectors, industries as well as over different types of funds. What You get: 1. More income and more savings 2. Less stress and tension since you know if one stream stops you have others to bank on 3. Takes away the mid-life crisis situations and the boredom from life from having income generated from the same old avenue year after year

- 24. 24 IF YOU WANT TO BE CONSIDERED SUCCESSFUL, INVEST IN EXPERIENCES H owever, one thing is common, all of us want to be considered successful… by our friends, family and by the world. It gives a sense of achievement, a sense of a high, when the world looks up at you as a successful individual and points to you as an example. So how does the world define success? Why and what would make it consider you successful? The single word answer to that is – experience. Yes, if you want to be considered successful, invest in experience. When Richard Branson or Warren Buffet enters a room, everybody looks up. Everyone knows who he is. That particular room is full of rich and successful people so what makes them different? Simply because of the experience they have WEALLHAVEDIFFERENTDEFINITIONSOFSUCCESS.WHATSUCCESS MEANS TO YOU MIGHT NOT MEAN SUCCESS TO ME. FOR SOME, CLIMBING UP THE CORPORATE LADDER TO SENIOR MANAGEMENT POSITIONS HAVING LUXURIOUS APARTMENTS AND FANCY CARS MIGHT WELL DEFINE SUCCESS, FOR OTHERS HAVING THEIR OWN BUSINESS, CREATING JOBS FOR OTHERS MIGHT BE PERCEIVED BY THEM TO BE MORE SUCCESSFUL THAN THE FORMER. Money Mad Mad

- 25. 25 created as a part of their growth and success story. INVESTIN EXPERIENCE FOR YOURSELF There is a distinct difference in ‘buying’ and ‘experiencing’. When you are rich you can always buy things or services that you need or want, but for real happiness or self-contentment, invest in ‘experiences’. Experiences have an emotional element that makes you ‘feel’. INVESTIN EXPERIENCE FOR YOUR CUSTOMERS If the above is true for you, then it is true for everyone else right? People are happier when they invest in experiences. In today’s world of global digital ecommerce economy, most of us can buy what we want. There is a complete clutter of everyone selling everything that one needs or wants. So maybe it is time we look into the niche areas that just doesn’t give customers products or services that they need but give an experience that has an emotional quotient to it. WHATTHE ELEMENTOF ‘EXPERIENCE’ MEANS INTHE BUSINESSWORLD This is precisely why from the era of ecom- merce and creation of the global market place we are gradually shifting to the Internet of Thin- gs (IoT) space. IoT is all about experience and the merging of technology to create and provide novel and more innovative experiences to people. Think about if you could arrange your curtains at home via a swipe on your smartphone. Little and random example as this can be numerous. But what I mean to say is that people don’t necessarily want to buy a product that arranges curtains let’s say. However, what you are offering is an ‘experience’, an expe- So how does the world define success? Why and what would make it consider you successful? The single word answer to that is – experience. rience of being able to control one’s home and its element from a touch on your smart phone. This mi- ght just be a very simple example, but you get my point right? The world in future will bow down to people who can offer novel experien- ces to its people. And if you want to be consi- dered really successful, investing in experiences is the way to go. Money Mad Mad

- 26. Money Mad Mad RARELY WRONG The rich trust their guts, and they are 26

- 27. 27 Money Mad Mad S teve Jobs for example had that amazing quality of going by his gut feeling and it was rarely wrong. While numerous experts advised him against Apple going into the phone business, he was the only person who had a gut feeling, an intuition that it would work! Brain Vs Gut – Where’s the contradiction? So what exactly is the difference? What exactly is a gut feeling and how is it a ‘different feel’ than when your brain is telling you that something would work or wouldn’t? Well, there lies the differen- ce really. Your brain will always tell you that so- mething ‘should’ be right or wrong, it has a dataset and analytically assesses it to reach the logical conclusion of what ‘sho- uld’ or ‘shouldn’t’ work. However, the world or destiny isn’t always logi- cal. Your gut feeling is not based on any data, not about what you should do given the circumstan- ces. Its simply the ‘inner feeling’, an intuition you have about something. The feeling you ‘feel’ and not arrive at, the inner whisper to your heart that something will work or something is odd or some imminent danger in something. Rich people are rich because they managed some kind of a breakthrough that others could not, and usually most of this breakthrou- ghs are based on gut fee- lings. If they were thought out from the brain then many other people would have also done it since the data set existing is the same for everyone. It needs someone’s gut fee- ling and more importantly the courage to not listen to anything or anyone and go just by that gut feel to make it big in life. The Gut Feeling – Scientifically Explained Now that we have under- stood that the rich trust their gut, lets scientifically see how it actually works. Experts say that humans have two parts to their memory – the explicit and the implicit. The former is the kind where you remember stuff that you actually make an effort to learn and remember. The latter on the other hand is mostly the indirect things that we remember unconsciously, and our brain hasn’t really made a direct effort to remem- ber them. For example, the explicit memory is when you study before your exams and try to remember things with an effort, or when you make an effort to learn cycling lets say. Implicit memory would include remembe- ring a quote or a movie song that you have never really made an effort to remember but somehow got absorbed by your brain. Or let’s say how you remember that the stove is hot and you shouldn’t touch it. These implicit memories are the ones which act behind your gut instincts, help you make decisions based on some past triggers that otherwi- se your conscious brain doesn’t remember. Personality Traits that go along with your gut’ It’s never enough to simply have a gut feeling if you do not do anything about it. Gut feeling and risk goes hand in hand and for all rich people this combination has basica- lly called the third friend called success along. So next time you have an inner feeling that somet- hing would work, have the courage to take the leap of faith. Best luck! To trust your head or your gut? Undoubtedly one of the most confusing yet pertinent questions in business! The rich trust their guts and they are rarely wrong. If you survey rich people all over the globe, you will find that they are rich for this sole reason in the first place! Steve Jobs for example had that amazing quality of going by his gut feeling and it was rarely wrong. While numerous experts advised him against Apple going into the phone business, he was the only person who had a gut feeling, an intuition that it would work!.

- 28. Money Mad Mad 8REASONS WHY YOU DON’T HAVE MONEY 28

- 29. 29 Money Mad Mad 1. Sticking to the comfort zone We all feel safe at our mummy’s lap. This is good as long as your love for your mummy does not stop you from grabbing the opportuni- ties available in far away destinations. As long as we remain a couch po- tato under the protective wings of our parents, we never explore the golden opportunities outside our doors. 2. Lack of real knowledge about economY Economy in the local man’s language remains the balancing of household income and expenses. This illiteracy makes people comfortably revolve around household expenses and savings year over year. Right from a young age, people must be exposed to the real economy in the world outside the four walls. This will make people more pragmatic in terms of money and accumulating the same 3. Blocked by budgeting mindset Budgeting is good as long as it acts as the beginning for planned activities. When we just keep budgeting, we do budgeting alone and nothing else to earn money. It is true that ‘A penny saved in a penny earned’. But then it is just a penny and will remain one unless it is invested in a prudent manner. 4. Depending on economic miracles Never think too high about politics or socie- tal scenario. Societal economics is in no way going to lift you up as an individual. You have to try to pull yourself up wit- hout depending on any external force outside your control. 5. Stop feeling apathetic about yourself Irrespective of where we stand financially, it is prudent to ascertain our situation in a periodical manner. Even if you don’t have a penny in your wallet, don’t give up. Just assess where you stand financially and what you can do about the same every now and then. If you don’t care for your financial situation, money will not care about ente- ring in to your wallet. 6. ACCEPTINGTHE RESPONSIBILITY Never feel bad about doi- ng any legitimate job that can fetch you the money you want. No job is bad unless it means killing someone physically or Life appears to be a never ending running race most of the times. We get the feeling that despite running the race in a tireless manner, we never seem to have a penny in our wallet whenever we open it. We either live on credit or tend to give away our desires in a dejected manner. We seem to be doing everything right when it comes to money and yet our wallet does not act as a proof for the same. Here are some crucial reasons why we don’t have money. cheating others. Try your hands even on jobs that others are unwilling to take up. For all you know, that is where the money is lying in huge lumps. 7. Don’t com- mit financial suicide Get out of the mindset of comparing your financial situations with that of others whose situations are worse than yours. This means you are comforta- bly justifying your financial situation doing nothing really meaningful to get out of the same. Draw in- spiration from people who are financially better off than you. Think honestly what took them there. Work towards the same. 8. Never feel happywith yourworking schedule We are not asking to kill yourself but never get satisfied when you work between nine and five for five days a week. Having cash in hand all the time requires you to work all the time. It may be mental or physical. But work. It may be true that money is not everything and there is more to life than money. However, remember that in reality, money plays a significant role deciding the quality of the life we live.

- 30. Mad Mad Money