80 ĐỀ THI THỬ TUYỂN SINH TIẾNG ANH VÀO 10 SỞ GD – ĐT THÀNH PHỐ HỒ CHÍ MINH NĂ...

Pbl2 p & l statement - excel

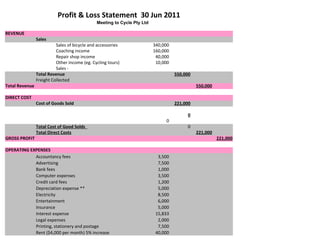

1. Profit & Loss Statement 30 Jun 2011

Meeting to Cycle Pty Ltd

REVENUE

Sales

Sales of bicycle and accessories 340,000

Coaching income 160,000

Repair shop income 40,000

Other income (eg. Cycling tours) 10,000

Sales -

Total Revenue 550,000

Freight Collected

Total Revenue 550,000

DIRECT COST

Cost of Goods Sold 221,000

0

0

Total Cost of Good Solds 0

Total Direct Costs 221,000

GROSS PROFIT 221,000

OPERATING EXPENSES

Accountancy fees 3,500

Advertising 7,500

Bank fees 1,000

Computer expenses 3,500

Credit card fees 1,200

Depreciation expense ** 5,000

Electricity 8,500

Entertainment 6,000

Insurance 5,000

Interest expense 15,833

Legal expenses 2,000

Printing, stationery and postage 7,500

Rent ($4,000 per month) 5% increase 40,000

p.a.

2. Repairs and Maintenance 6,000

Salaries and wages – Directors 50,000

Salaries and wages – Other staff 116,000

Staff amenities (tea, coffee, biscuits) 1,000

Superannuation (@ 9% of total salaries) 15,000

Telephone and facsimile charges 3,000

Other costs 20,000

Bank Charges 0

Freight Paid 0

Set-Up Cost

Opening party 5,500

Fit-out 83,600

Workshop 7,040

Displaying stock 28,160

Indoor windtraining sessions 21,120

Office 14,080

Install tiles 13,200

Cash registers 9,680

Computers 27,060

Photocopying machine 4,180

Facsimile machine 880

Timber bookcases 6,820

Television sets 9,680

Fluorescent lighting system 20,240

Carpets 28,820

MYOB Accounting Plus Version 18 and other 8,360

retail-based computer software

Total Set-Up Cost 204,820

Total Motor Vehicle Expenses 0

Office Supplies 0

Rent 0

Telephone and internet 0

Total Expenses 522,353

NET PROFIT -301,353

3.

4. Under ITAA 1997 S20-30- "upgrading assets to meet GST obligations " are deductible BUT we should consider what is "GST obligation". The

above A NEW TAX SYSTEM (INDIRECT TAX AND CONSEQUENTIAL AMENDMENTS) ACT (NO. 2) 1999 - SCHEDULE 5 - Income tax deductions

for GST-related expenditure : S25-80(d) &(e), we should consider pre-GST annual turnover for income year.

Our fit-out has been installed tiles ($13,200) in 2010 ( Commencement date of the business will be 1 September 2010.), under S25-80 (d),

this upgraded plant is post 1 July 2000 so this item is undeductible.