What an L3C is: A Summary of this Hybrid Legal Structure

•

6 gefällt mir•2,584 views

Self-authored comparison between L3C and not for profit/non-profit

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie What an L3C is: A Summary of this Hybrid Legal Structure

Ähnlich wie What an L3C is: A Summary of this Hybrid Legal Structure (20)

Mehr von Justin Fenwick

Mehr von Justin Fenwick (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

What an L3C is: A Summary of this Hybrid Legal Structure

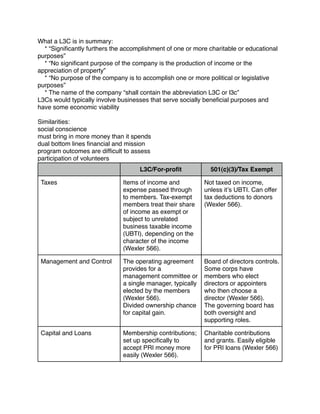

- 1. What a L3C is in summary: * “Significantly furthers the accomplishment of one or more charitable or educational purposes” * “No significant purpose of the company is the production of income or the appreciation of property” * “No purpose of the company is to accomplish one or more political or legislative purposes” * The name of the company “shall contain the abbreviation L3C or l3c” L3Cs would typically involve businesses that serve socially beneficial purposes and have some economic viability Similarities: social conscience must bring in more money than it spends dual bottom lines financial and mission program outcomes are difficult to assess participation of volunteers L3C/For-profit 501(c)(3)/Tax Exempt Taxes Items of income and expense passed through to members. Tax-exempt members treat their share of income as exempt or subject to unrelated business taxable income (UBTI), depending on the character of the income (Wexler 566). Not taxed on income, unless itʼs UBTI. Can offer tax deductions to donors (Wexler 566). Management and Control The operating agreement provides for a management committee or a single manager, typically elected by the members (Wexler 566). Divided ownership chance for capital gain. Board of directors controls. Some corps have members who elect directors or appointers who then choose a director (Wexler 566). The governing board has both oversight and supporting roles. Capital and Loans Membership contributions; set up specifically to accept PRI money more easily (Wexler 566). Charitable contributions and grants. Easily eligible for PRI loans (Wexler 566)

- 2. L3C/For-profit 501(c)(3)/Tax Exempt Distribution of Funds Not Used for Programs Distributions to members and grants for charitable purposes (Wexler 566). Grants for charitable purposes (Wexler 566) Liquidation (Sale of entity/ assets) Net assets to members and to 501(c)(3) charities. (Wexler 566). Net assets to another 501(c)(3) with like exempt purposes (Wexler 566). Social Mission Requires accomplishment of one or more charitable or educational purposes. Must be formed only because of those reasons. Required. Activities that provide services or good not otherwise available. Investment SRI + NPO + market rate investors all under one roof for profit. Attracts investment because of social mission and ability to provide a return. Risk and award can be divided unevenly. Attracts investment because of tax deductibility and social mission. PRIʼs (private foundation) Can accept more easily Cumbersome process, requiring private letter rulings for a program funded by a nonprofit and foundation.

- 3. L3C/For-profit 501(c)(3)/Tax Exempt Fully allowed as long as social mission is not compromised. Secondary goal (Americans for Community Development FAQs). Do not have to maximize profit. "In a not-for-profit organization, the profits go back into the organization -- either in the form of added program funding or by adding to the reserves or capital funds...Many NPOs fail because they didn't plan to earn more than they spent and because they didn't put their profits in reserve accounts for the proverbial rainy day." http:// www.poynteronline.org/q/? id=A159737 Price of services Can be provided at whatever the market will allow. Price mark-ups allowed. Provided below market rates or no detectible markups that seek to maximize profit. Main Advantages Attracting program related investments. Branding and marketing benefit that might open up access to funding, contracts, and investment (Wexler 568). Provides an “in” to the culture of financial decision making. Great if services require grants and contributions to operate. More aligned with the thinking and purposes of education, government, and other nonprofit institutions. The 501c3 is required by most donors, government granting agencies, and foundations for gifts and grants. No pressure to make return for investors. Focus on exempt only activities that are only reaching towards social mission Profit Activities

- 4. L3C/For-profit Main Disadvantages 501(c)(3)/Tax Exempt Loss of collaboration and funding that requires exempt activities. Pressure of return/more focus on finances. “Isnʼt an existing accountability system of IRS 990s, state regulations, etc.” Kate Barr “I fear most institutional funders will remain too risk adverse to jump in.” Adam Huttler Limited access to capital for growth when lots of services are shifting to the government and the large national organizations. Regulatory structure can be very restrictive on movement and growth of organization. It can be hard to manage, govern, and sustain, itʼs awkward for enterprises that plan a profit (even a small one), and it tends to be permanent even when permanence isn't required.

- 5. L3C/For-profit Reasons for a combination 501(c)(3)/Tax Exempt Most clients who talk about a hybrid structure, however, are considering pairing a charitable organization that can receive grants and contributions and a for-profit that can use investment capital to develop a product or service and then provide that product or service to the charity at a fair market value rate. As illustrated below, the two most complicated issues that typically arise in the hybrid model are (1) taking substantive and procedural steps to avoid any excess benefits, and (2) ensuring that the activities of the for-profit and the charity can be sufficiently separated so that the activities of the business are not attributed to the charity, thereby compromising its tax-exempt status. A for-profit combined with an exempt entity to carry out a social enterprise makes sense as follows: • when only a portion of the activity can qualify for exemption; • when capital is required both in the form of private investment and from grants and contributions; and • when the founders want to build a business to sell, but also are willing to dedicate some portion of the enterprise to charity in perpetuity. Whenever an enterprise considers a hybrid structure, it must, at a minimum: • be prepared to delineate clearly the activity that will rest in the exempt versus for-profit structure; there must be a logical and practical way to divide the activities; • be cognizant of, and be prepared to comply with the procedures to avoid, intermediate sanctions under section 4958; the enterprise must develop and follow clear conflict of interest policies and disclose financial interests to the disinterested members of the nonprofit board of directors; • give up legal control of the exempt entity to those who will not benefit financially from the for-profit business; the disinterested members of the tax-exempt board need to be individuals who will understand their independent fiduciary duty and not simply rubber-stamp the decisions of the for-profit founders; and • ensure that the private investors, particularly any venture capitalists, understand that they do not control, and cannot control or benefit from, the exempt side of the enterprise. Segregation of exempt vs. non-exempt activities is a very important step to take. If CRF's non-exempt activities reach too significant of a level, CRF's exempt status is in jeopardy. With that said, the exempt vs. non-exempt activities analysis does not mean that there is a blanket prohibition against CRF from engaging in activities such as the sale of merchandise or other goods and services. The point of inquiry under the federal tax law is whether the activity is in furtherance of CRF's exempt purposes. Peter Kulick