Tech Startup Growth Hacking 101 - Basics on Growth Marketing

Zydus Wellness reports a subdued quarter, hold - Nirmal Bang

1. 1 | P a g e

IInniittiiaattiinnggCCoovveerraaggee

ttiiaattiinnggCCoovveerraaggee

ttiinnggCCoovveerraaggee

ggCCoovveerraaggee

CCoovveerraaggee

vveerraaggee

rraaggee

ggee

Zydus Wellness Ltd.

QQ44FFYY1144RReessuullttUUppddaattee––2233MMaayy22001144

4

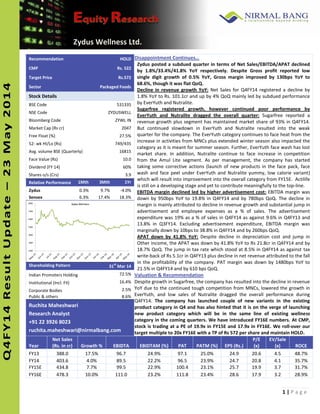

Recommendation HOLD Disappointment Continues…

Zydus posted a subdued quarter in terms of Net Sales/EBITDA/APAT declined

by 1.8%/33.4%/41.8% YoY respectively. Despite Gross profit reported low

single digit growth of 0.5% YoY, Gross margin improved by 130bps YoY to

68.6%, though it was flat QoQ.

Decline in revenue growth YoY: Net Sales for Q4FY14 registered a decline by

1.8% YoY to Rs. 101.1cr and up by 4% QoQ mainly led by subdued performance

by EverYuth and Nutralite.

Sugarfree registered growth, however continued poor performance by

EverYuth and Nutralite dragged the overall quarter: Sugarfree reported a

revenue growth plus segment has maintained market share of 93% in Q4FY14.

But continued slowdown in EverYuth and Nutralite resulted into the weak

quarter for the company. The EverYuth category continues to face heat from the

increase in activities from MNCs plus extended winter season also impacted the

category as it is meant for summer season. Further, EverYuth face wash has lost

market share. In addition, Nutralite continue to face increase in competition

from the Amul Lite segment. As per management, the company has started

taking some corrective actions (launch of new products in the face pack, face

wash and face peel under EverYuth and Nutralite yummy, low calorie variant)

which will result into improvement into the overall category from FY15E. Actilife

is still on a developing stage and yet to contribute meaningfully to the top-line.

EBITDA margin declined led by higher advertisement cost: EBITDA margin was

down by 950bps YoY to 19.8% in Q4FY14 and by 780bps QoQ. The decline in

margin is mainly attributed to decline in revenue growth and substantial jump in

advertisement and employee expenses as a % of sales. The advertisement

expenditure was 19% as a % of sales in Q4FY14 as against 9.6% in Q4FY13 and

13.8% in Q3FY14. Excluding advertisement expenditure, EBITDA margin was

marginally down by 10bps to 38.8% in Q4FY14 and by 260bps QoQ.

APAT down by 41.8% YoY: Despite decline in depreciation cost and jump in

Other income, the APAT was down by 41.8% YoY to Rs 21.8cr in Q4FY14 and by

18.7% QoQ. The jump in tax rate which stood at 8.5% in Q4FY14 as against tax

write-back of Rs 5.1cr in Q4FY13 plus decline in net revenue attributed to the fall

in the profitability of the company. PAT margin was down by 1480bps YoY to

21.5% in Q4FY14 and by 610 bps QoQ.

Valuation & Recommendation

Despite growth in Sugarfree, the company has resulted into the decline in revenue

YoY due to the continued tough competition from MNCs, lowered the growth in

EverYuth, and low sales of Nutralite dragged the overall performance during

Q4FY14. The company has launched couple of new variants in the existing

product category in Q4 and has also hinted that it is on the verge of launching

new product category which will be in the same line of existing wellness

category in the coming quarters. We have introduced FY16E numbers. At CMP,

stock is trading at a PE of 19.9x in FY15E and 17.9x in FY16E. We roll-over our

target multiple to 20x FY16E with a TP of Rs 572 per share and maintain HOLD.

CMP Rs. 522

Target Price Rs.572

Sector Packaged Foods

Stock Details

BSE Code 531335

NSE Code ZYDUSWELL

Bloomberg Code ZYWL IN

Market Cap (Rs cr) 2047

Free Float (%) 27.5%

52- wk HI/Lo (Rs) 749/435

Avg. volume BSE (Quarterly) 16815

Face Value (Rs) 10.0

Dividend (FY 14) 60%

Shares o/s (Crs) 3.9

Relative Performance 1Mth 3Mth 1Yr

Zydus 0.3% 9.7% -4.0%

Sensex 6.3% 17.4% 18.3%

Shareholding Pattern 31

st

Mar 14

Indian Promoters Holding 72.5%

Institutional (Incl. FII) 16.4%

Corporate Bodies 2.5%

Public & others 8.6%

Ruchita Maheshwari

Research Analyst

+91 22 3926 8023

ruchita.maheshwari@nirmalbang.com

Year

Net Sales

(Rs. in cr) Growth % EBIDTA EBIDTAM (%) PAT PATM (%) EPS (Rs.)

P/E

(x)

EV/Sale

(x) ROCE

FY13 388.0 17.5% 96.7 24.9% 97.1 25.0% 24.9 20.6 4.5 48.7%

FY14 403.6 4.0% 89.5 22.2% 96.5 23.9% 24.7 20.8 4.1 35.7%

FY15E 434.8 7.7% 99.5 22.9% 100.4 23.1% 25.7 19.9 3.7 31.7%

FY16E 478.3 10.0% 111.0 23.2% 111.8 23.4% 28.6 17.9 3.2 28.9%

2. 2 | P a g e

IInniittiiaattiinnggCCoovveerraaggee

ttiiaattiinnggCCoovveerraaggee

ttiinnggCCoovveerraaggee

ggCCoovveerraaggee

CCoovveerraaggee

vveerraaggee

rraaggee

ggee

Zydus Wellness Ltd.

QQ44FFYY1144RReessuullttUUppddaattee––2233MMaayy22001144

Q4FY14 Consolidated Result Analysis

Rs. in crore

Particulars Q4FY14 Q4FY13 YoY% Q3FY14 QoQ%

Net Sales 101.1 103.0 -1.8% 97.2 4.0%

Other Operating Income 0.0 0.4 0.2

Total Income 101.1 103.4 -2.2% 97.3 3.9%

Increase / Decrease in Stock 0.2 -7.9 3.9

Consumption of raw material 30.3 33.3 -9.0% 26.0 16.5%

Purchase of traded goods 1.4 8.7 -84.3% 0.9 60.0%

Employees Cost 7.6 7.1 7.0% 7.5 2.0%

Advertisement Expenditure 19.2 9.9 94.1% 13.4 43.0%

Other Expenditure 22.4 22.2 1.1% 19.0 18.1%

Total Expenditure 81.0 73.3 10.6% 70.6 14.9%

EBIDTA 20.1 30.1 -33.4% 26.8 -25.1%

Interest 0.0 0.0 100.0% 0.0 33.3%

Other Income 5.6 4.3 30.1% 4.7 18.8%

EBDT 25.6 34.4 -25.6% 31.4 -18.6%

Depreciation 1.3 1.3 -4.5% 1.1 12.4%

PBT 24.3 33.1 -26.5% 30.3 -19.8%

Tax 2.1 -5.1 3.0

Reported Profit After Tax 22.3 38.2 -41.7% 27.3 -18.5%

Minority Interest 0.5 0.8 -35.5% 0.5 -9.3%

Adjusted Profit After Extra-ordinary item 21.8 37.4 -41.8% 26.8 -18.7%

AEPS (Unit Curr.) 5.6 9.6 6.9

Equity 39.1 39.1 39.1

Face Value 10.0 10.0 10.0

BPS BPS

EBIDTAM(%) 19.8% 29.3% -950 27.6% -780

EBDTM(%) 25.3% 33.4% -810 32.4% -710

PATM(%) 21.5% 36.3% -1480 27.6% -610

Source: Company & Nirmal Bang Research

3. 3 | P a g e

IInniittiiaattiinnggCCoovveerraaggee

ttiiaattiinnggCCoovveerraaggee

ttiinnggCCoovveerraaggee

ggCCoovveerraaggee

CCoovveerraaggee

vveerraaggee

rraaggee

ggee

Zydus Wellness Ltd.

QQ44FFYY1144RReessuullttUUppddaattee––2233MMaayy22001144

Consolidated Financials

Profitability (Rs. In Cr) FY13 FY14 FY15E FY16E Balance Sheet (Rs. In Cr) FY13 FY14 FY15E FY16E

Y/E - March Share Capital 39.1 39.1 39.1 39.1

Revenues - Net 388.0 403.6 434.8 478.3 Reserves & Surplus 217.5 286.5 359.6 444.0

% change 17.5% 4.0% 7.7% 10.0% Net Worth 256.5 325.6 398.6 483.0

EBITDA 96.7 89.5 99.5 111.0 Total Loans 0.0 0.0 0.0 0.0

% change 27.2% -7.4% 11.2% 11.5% Minority Interest 2.9 4.7 6.7 8.8

Interest 0.1 0.1 0.2 0.2 Net Deferred Tax Assets 3.9 4.9 4.9 4.9

Other Income 15.8 18.9 19.9 21.4 Total Liabilities 263.3 335.2 410.2 496.8

EBDT 112.4 108.3 119.2 132.2 Net Fixed Assets 94.3 95.4 95.7 95.7

Depreciation 4.5 4.7 4.8 5.0 Investments 0.0 5.0 5.0 5.0

Extraordinary/Exceptional 0.0 0.0 0.0 0.0 CWIP 0.0 0.0 0.0 0.0

PBT 107.9 103.6 114.4 127.2 Inventories 40.9 27.9 37.9 44.4

Tax 8.8 5.3 12.0 13.4 Sundry Debtors 1.5 2.6 3.2 3.5

PAT 99.0 98.3 102.4 113.9 Cash & Bank 190.8 262.8 329.1 410.1

Minority Interest 1.9 1.9 2.0 2.1 Loans & Advances 21.8 31.0 40.4 48.6

PAT after minority interest 97.1 96.5 100.4 111.8 C A L&A 254.9 324.4 410.5 506.6

Shares o/s ( No. in Cr.)* 3.9 3.9 3.9 3.9 CL & P 85.9 89.7 100.9 110.6

EPS 24.9 24.7 25.7 28.6 Working Capital 169.0 234.7 309.6 396.0

Cash EPS 26.5 26.4 27.4 30.4 Total Assets 263.3 335.2 410.2 496.8

DPS (Rs.) 6.0 6.5 7.0 6.5 Cash Flow (Rs. In Cr) FY13 FY14E FY15E FY16E

Quarterly (Rs. In Cr) June.13 Sept.13 Dec.13 Mar.14 Operating

Revenue including OI 107.5 97.7 97.3 101.1 Profit Before Tax 107.9 103.6 114.4 127.2

EBITDA 17.2 25.5 26.8 20.1 Direct Taxes paid -8.8 -5.3 -12.0 -13.4

Interest 0.0 0.0 0.0 0.0 Depreciation 4.5 4.7 4.8 5.0

Other Inc. 3.8 4.8 4.7 5.6 Change in WC -18.1 0.3 -8.6 -5.4

EBDT 20.9 30.3 31.4 25.6 Interest Expenses 0.1 0.1 0.2 0.2

Dep 1.1 1.1 1.1 1.3 Other Operating Activities 0.0 0.0 0.0 0.0

Extraordinary 0.0 0.0 0.0 0.0 CF from Operation 85.5 103.4 98.8 113.6

PBT 19.8 29.2 30.3 24.3 Investment

Tax -3.3 3.6 3.0 2.1 Capex -2.7 -5.8 -5.0 -5.0

PAT from ordinary activities 23.1 25.7 27.3 22.3 Other Investment 0.0 0.0 0.0 0.0

Minority Interest 0.4 0.5 0.5 0.5 Total Investment -2.7 -5.8 -5.0 -5.0

PAT 22.7 25.2 26.8 21.8 Free Cash Flow 82.8 97.6 93.8 108.6

EPS (Rs.) 5.9 6.6 7.0 5.7 Financing

Adjusted EPS (Rs.) 5.8 6.4 6.9 5.6 Equity raised/(repaid) 0.0 0.0 0.0 0.0

Operational Ratio FY13 FY14 FY15E FY16E Debt raised/(repaid) 0.0 0.0 0.0 0.0

EBITDA margin (%) 24.9% 22.2% 22.9% 23.2% Dividend (incl. tax) paid -23.4 -25.4 -27.3 -27.3

Adj.PAT margin (%) 25.0% 23.9% 23.1% 23.4% Deferred Revenue Exp. 0.0 0.0 0.0 0.0

Adj.PAT Growth (%) 43.5% -0.7% 4.1% 11.3% Interest Expenses -0.1 -0.1 -0.2 -0.2

Price Earnings (x) 20.6 20.8 19.9 17.9 Cash Flow from Financing Activities -23.5 -25.5 -27.5 -27.5

Book Value (Rs.) 65.7 83.3 102.0 123.6 Net Cash Flow 59.3 72.0 66.3 81.0

ROCE (%) 48.7% 35.7% 31.7% 28.9% Beginning Cash Flow 131.5 190.8 262.8 329.1

RONW (%) 44.7% 33.8% 28.3% 25.8% Cash as reported in Balance Sheet 190.8 262.8 329.1 410.1

Debt Equity Ratio 0.0 0.0 0.0 0.0

Price / Book Value (x) 8.0 6.3 5.1 4.2

EV / Sales 4.5 4.1 3.7 3.2

EV / EBIDTA 16.4 16.4 14.3 12.3

Source: Company & Nirmal Bang Research

4. 4 | P a g e

IInniittiiaattiinnggCCoovveerraaggee

ttiiaattiinnggCCoovveerraaggee

ttiinnggCCoovveerraaggee

ggCCoovveerraaggee

CCoovveerraaggee

vveerraaggee

rraaggee

ggee

Zydus Wellness Ltd.

QQ44FFYY1144RReessuullttUUppddaattee––2233MMaayy22001144

Disclaimer:

This Document has been prepared by Nirmal Bang Research (A Division of Nirmal Bang Securities PVT LTD). The information, analysis and

estimates contained herein are based on Nirmal Bang Research assessment and have been obtained from sources believed to be reliable. This

document is meant for the use of the intended recipient only. This document, at best, represents Nirmal Bang Research opinion and is meant for

general information only. Nirmal Bang Research, its directors, officers or employees shall not in anyway be responsible for the contents stated

herein. Nirmal Bang Research expressly disclaims any and all liabilities that may arise from information, errors or omissions in this connection. This

document is not to be considered as an offer to sell or a solicitation to buy any securities. Nirmal Bang Research, its affiliates and their employees

may from time to time hold positions in securities referred to herein. Nirmal Bang Research or its affiliates may from time to time solicit from or

perform investment banking or other services for any company mentioned in this document.

Nirmal Bang Research (Division of Nirmal Bang Securities Pvt. Ltd.)

B-2, 301/302, Marathon Innova,

Opp. Peninsula Corporate Park

Off. Ganpatrao Kadam Marg

Lower Parel (W), Mumbai-400013

Board No. : 91 22 3926 8000/8001

Fax. : 022 3926 8010