Shriram Transport Finance Company Q1FY15: Buy for a target of Rs1130

•

1 gefällt mir•418 views

Shriram Transport’s 1QFY15 PAT declined 10% YoY and (up 4% QoQ to INR3b (In line). Moderation in AUM growth (+4% YoY to INR544b), decline in disbursements (7% YoY), and improvement in margins (10bp QoQ) are key highlights of the quarter; buy.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Shriram Transport Finance Company Q1FY15: Buy for a target of Rs1130

Ähnlich wie Shriram Transport Finance Company Q1FY15: Buy for a target of Rs1130 (20)

Mehr von IndiaNotes.com

Mehr von IndiaNotes.com (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Shriram Transport Finance Company Q1FY15: Buy for a target of Rs1130

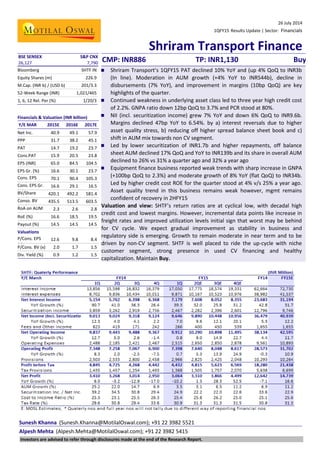

- 1. 26 July 2014 1QFY15 Results Update | Sector: Financials Shriram Transport Finance Sunesh Khanna (Sunesh.Khanna@MotilalOswal.com); +91 22 3982 5521 Alpesh Mehta (Alpesh.Mehta@MotilalOswal.com); +91 22 3982 5415 BSE SENSEX S&P CNX CMP: INR886 TP: INR1,130 Buy26,127 7,790 Bloomberg SHTF IN Equity Shares (m) 226.9 M.Cap. (INR b) / (USD b) 201/3.3 52-Week Range (INR) 1,021/465 1, 6, 12 Rel. Per (%) 1/20/3 Financials & Valuation (INR billion) Y/E MAR 2015E 2016E 2017E Net Inc. 40.9 49.1 57.9 PPP 31.7 38.2 45.1 PAT 14.7 19.2 23.7 Cons.PAT 15.9 20.5 23.8 EPS (INR) 65.0 84.5 104.5 EPS Gr. (%) 16.6 30.1 23.7 Cons. EPS (INR) 70.1 90.4 105.3 Cons. EPS Gr. ( ) 16.6 29.1 16.5 BV/Share (INR) 420.1 492.2 581.4 Conso. BV ( ) 435.5 513.5 603.5 RoA on AUM (%) 2.3 2.6 2.8 RoE (%) 16.6 18.5 19.5 Payout (%) 14.5 14.5 14.5 Valuations P/Cons. EPS ( ) 12.6 9.8 8.4 P/Cons. BV (x) 2.0 1.7 1.5 Div. Yield (%) 0.9 1.2 1.5 Shriram Transport’s 1QFY15 PAT declined 10% YoY and (up 4% QoQ to INR3b (In line). Moderation in AUM growth (+4% YoY to INR544b), decline in disbursements (7% YoY), and improvement in margins (10bp QoQ) are key highlights of the quarter. Continued weakness in underlying asset class led to three year high credit cost of 2.2%. GNPA ratio down 12bp QoQ to 3.7% and PCR stood at 80%. NII (incl. securitization income) grew 7% YoY and down 6% QoQ to INR9.6b. Margins declined 47bp YoY to 6.54%. by a) interest reversals due to higher asset quality stress, b) reducing off higher spread balance sheet book and c) shift in AUM mix towards non CV segment. Led by lower securitization of INR1.7b and higher repayments, off balance sheet AUM declined 17% QoQ and YoY to INR139b and its share in overall AUM declined to 26% vs 31% a quarter ago and 32% a year ago Equipment finance business reported weak trends with sharp increase in GNPA (+100bp QoQ to 2.3%) and moderate growth of 8% YoY (flat QoQ) to INR34b. Led by higher credit cost ROE for the quarter stood at 4% v/s 25% a year ago. Asset quality trend in this business remains weak however, mgmt remains confident of recovery in 2HFY15 Valuation and view: SHTF’s return ratios are at cyclical low, with decadal high credit cost and lowest margins. However, incremental data points like increase in freight rates and improved utilization levels initial sign that worst may be behind for CV cycle. We expect gradual improvement as stability in business and regulatory side is emerging. Growth to remain moderate in near term and to be driven by non-CV segment. SHTF is well placed to ride the up-cycle with niche customer segment, strong presence in used CV financing and healthy capitalization. Maintain Buy. Investors are advised to refer through disclosures made at the end of the Research Report.

- 2. 26 July 2014 2 Shriram Transport Finance Quarterly performance and reason for deviation Y/E March 1QFY15A 1QFY15E Var (%) Comments Net Income 9,646 9,544 1 Net income in line with estimates % Change (Y-o-Y) 7.0 5.9 Other Income 266 400 Total Net Income 9,912 9,944 0 Operating Expenses 2,515 2,650 -5 Higher than expected employee expense Operating Profit 7,398 7,294 1 Provisions 2,966 2,825 5 Higher provisioning for standard assets Profit before Tax 4,432 4,469 -1 Tax Provisions 1,368 1,352 1 Net Profit 3,064 3,117 -2 PAT In lIne with estimate % Change (Y-o-Y) -10.2 -8.6 Source: MOSL/Company Moderation in growth continues, AUM mix further increases towards old vehicles AUMs growth moderated to 4% YoY and 2.4% QoQ at INR544b. While used vehicle loans growth was healthy (+12% YoY, 3.3% QoQ), moderation in new vehicle loans (down 38% YoY and 10% QoQ) led to overall moderation in growth. Sharp new vehicles in overall AUM declined to 10.5% v/s 11.4% in FY14 and 17.4% a year ago. Disbursements declined by 6.7% YoY (up 6.5% QoQ) to INR74.1b; New CV disbursements were down 49% YoY but grew 39% QoQ, whereas disbursements in the old CV segment stood at INR70b (down 2% YoY and up 5% QoQ). Off-books AUMs de-grew 16.4% YoY and 16.6% QoQ; led by lower securitization of INR 1.7b during the quarter. Off books proportion of AUM declined to 25.5% v/s 31.3% in FY14 and 31.6% in 1QFY14. Margins improve 10bp QoQ; Likely to improve from hereon NII (including securitization income) grew 7% YoY and 6% QoQ to INR9.6b. Margins improved 8bp QoQ to 6.54%. On a YoY basis margins have declined 47bp on the back of interest reversals (due to high asset quality stress), reducing high spread off balance sheet book and shift in AUM mix further towards old vehicles. GNPA declines QoQ still high; Coverage ratio remain healthy at +79% GNPAs during the quarter declined 7% QoQ, GNPAs in percentage terms declined 65bps YoY and 12bp QoQ at 3.74%. Provisioning expenses (including for standard assets) stood at INR2.9b, increased 18% YoY and 21% QoQ basis. PCR remained healthy at +79%. Credit cost increased to 214bp in 1Q v/s 187bp in 4QFY14. This quarter witnessed the highest credit in last three years. Stress levels have remained high on the back of weak economic environment, low freight rates and increasing fuel costs. However, we expect environment to improve in the 2HFY15. Other highlights Securitization during the quarter at INR1.7b (lowest in last 8 quarters). CAR remained healthy at 22.9% with a tier 1 of 17.5%.

- 3. 26 July 2014 3 Shriram Transport Finance Valuation and view SHTF’ return ratios are at cyclical low, with decadal high credit cost and lowest margins. However, incremental data points like increase in freight rates, improved utilization levels and collection rates and improving IIP etc all point towards worse of the CV cycle is behind. We expect gradual improvement as stability in business and regulatory side is emerging. Sharp decline in economic growth resultant impact on asset quality (cyclical high credit cost and bottom margins) and regulatory changes led to risk adjustment margins falling to five-year low and sharp decline in return ratios (RoE down to 16% from 30% in FY09). Near terms margins are likely to be under pressure due to higher cost of funds led by budget proposals related to debt mutual funds. However, improvement in cycle and lower stress addition, traction in used CV portfolio and higher securitization will support margins in the medium term. Growth to remain moderate in near term and to be driven by non-CV segment. While yields in passenger vehicle portfolio are near to CV segment, operating cost is relatively high which will lead to some pressure on profitability in the near term. While SHTF’s return ratios have moderated compared to its historical trends, we expect ROA’s of ~2% and ROE of ~15% over FY14/16E. Increasing diversification coupled with the initiatives of penetrating deeper in rural location, financing other vehicles like tractors, Passenger vehicles etc (30% of the AUM vs 15% in FY10) augurs well in the long term Subsidiary profits have become sizeable and now contribute ~7% of consolidated PAT. We expect contribution to rise further on a lower base and growth rate is likely to be much higher than standalone business as the environment will revive. SHTF is well placed to ride the up-cycle with niche customer segment, strong presence in used CV financing and healthy capitalization. SHTF trades at 2x/1.7x FY15/16E consolidated BV and 12.6x/9.8x FY15/16E consolidated EPS. Maintain Buy with FY16E-based target price of INR1,130 (2.2x FY16E P/Consol Book).

- 4. 26 July 2014 4 Shriram Transport Finance Story in charts Disb. growth declined 7% YoY during the quarter (INRb) Proportion of off-book assets declined ~500bp QoQ (%) 60 64 60 55 61 67 67 63 68 70 71 69 74 40 36 40 45 39 33 33 37 32 30 29 31 26 1QFY12 1HFY12 9MFY12 FY12 1QFY13 1HFY13 9MFY13 FY13 1QFY14 1HFY14 9MFY14 FY14 1QFY15 OnBooks Off Books AUM mix shifted further in favor of old CVs (%) 76 76 77 77 78 79 79 81 83 84 87 88 90 24 24 23 23 22 21 21 19 17 16 13 12 10 1QFY12 1HFY12 9MFY12 FY12 1QFY13 1HFY13 9MFY13 FY13 1QFY14 1HFY14 9MFY14 FY14 1QFY15 UsedCVs (%) New CVs (%) Securitization during the quarter stand at INR2b 2 5 33 43 0 4 30 54 14 28 23 43 2 1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 Assets Securitized(INR b) NIMs (% on AUM) improve marginally sequentially 8.2 7.7 7.2 7.4 7.7 7.5 7.2 7.0 6.7 6.5 6.5 6.5 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 ReportedNIM (%) Opex management led to control over C/I ratio despite moderation in income growth 20 21 22 21 22 21 22 21 25 23 26 26 25 1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15

- 5. 26 July 2014 5 Shriram Transport Finance Quarterly performance FY13 FY14 FY15 Variation (%) 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q QoQ YoY Profit and Loss (INR m) Net Income 2,702 4,087 4,696 5,037 5,154 5,762 6,398 6,368 7,179 13 39 Operating Expenses 1,940 1,872 1,999 2,040 2,488 2,185 2,421 2,467 2,515 2 1 Employee 1,037 935 899 977 1,239 855 949 1,023 1,012 -1 -18 Others 903 937 1,100 1,063 1,250 1,329 1,473 1,444 1,502 4 20 Operating Profits 6,787 7,119 7,248 7,459 7,348 7,258 7,067 6,900 7,398 7 1 Provisions 2,026 2,106 2,126 2,193 2,503 2,533 2,800 2,458 2,966 21 18 NPAs/ Bad debts 1,946 2,018 2,081 2,179 2,392 2,494 2,788 2,493 2,874 15 20 Standard assets 80 89 45 14 111 39 12 -35 92 NA -17 PBT 4,761 5,013 5,122 5,266 4,845 4,725 4,268 4,442 4,432 0 -9 Taxes 1,543 1,638 1,662 1,713 1,435 1,457 1,254 1,493 1,368 -8 -5 PAT 3,219 3,376 3,460 3,552 3,410 3,268 3,014 2,950 3,064 4 -10 Asset Quality GNPA 7,776 8,553 9,087 10,254 11,317 12,543 13,872 14,505 15,466 7 37 NNPA 1,576 1,754 1,921 2,416 2,412 2,517 2,817 3,029 3,135 3 30 Gross NPAs (%) 3.0 2.9 2.9 3.2 3.1 3.3 3.6 3.9 3.7 Net NPAs (%) 0.6 0.6 0.6 0.8 0.7 0.7 0.8 0.8 0.8 PCR (Calculated, %) 79.7 79.5 78.9 76.4 78.7 79.9 79.7 79.1 79.7 Ratios (%) Cost to Income 24.2 21.6 22.3 22.8 27.6 24.2 26.0 27.0 26.1 Provision to operating profit 29.8 29.6 29.3 29.4 34.1 34.9 39.6 35.6 40.1 Tax Rate 32.4 32.7 32.5 32.5 29.6 30.8 29.4 33.6 30.9 Total CAR 21.3 20.5 19.2 20.7 20.3 19.9 22.2 23.4 22.9 Business Details (INR b) AUM 419 441 465 497 525 538 534 531 544 2 4 On book Loans 256 294 311 314 359 375 379 365 405 11 13 Off book (Securitization) 163 147 155 182 166 163 155 166 139 -17 -16 Total Borrowings 213 238 282 310 339 360 362 359 364 1 7 AUM Mix (b) New CV Loans 22 21 21 19 17 16 13 12 10 Used CV loans 78 79 79 81 83 84 87 88 90 Disbursements Details (INR b) Total 53.7 61.7 70.0 77.0 79.4 72.5 64.6 69.5 74.1 12 13 New CV Loans 10.0 11.2 11.2 11.0 8.1 4.8 1.6 2.9 4.1 87 -50 Used CV loans 43.7 50.5 58.8 66.0 71.4 67.6 63.0 66.6 70.0 10 24 Securitization Details Done during quarter (INR B) 0.0 3.9 30.4 53.6 13.7 27.8 22.7 42.7 1.7 Securitization inc as a % to net inc 66.3 52.9 47.5 43.6 42.8 36.1 31.3 30.2 25.6 Total Borrowing Mix (%) Banks / FIs 76.0 77.9 81.2 81.6 81.2 82.3 81.4 80.5 79.9 Retail 24.0 22.1 18.8 18.4 18.8 17.7 18.6 19.5 20.1 Other Details Branches 513 513 530 537 569 620 630 654 666 Employees 14,156 14,159 14,936 16,178 17,045 18,240 18,078 18,122 17,075 Source: Company, MOSL

- 6. 26 July 2014 6 Shriram Transport Finance EPS: MOSL forecast v/s consensus (INR) MOSL Consensus Variation Forecast Forecast (%) FY15 70.1 67.8 3.3 FY16 90.4 83.1 8.8 Shareholding pattern (%) Jun-14 Mar-14 Jun-13 Promoter 26.1 26.1 25.8 DII 2.0 1.0 1.2 FII (FII Incl. depository receipts) 53.2 53.9 53.8 Others 18.7 19.0 19.1 Stock performance (1-year)

- 7. 26 July 2014 7 Shriram Transport Finance Financials and valuations

- 8. 26 July 2014 8 Shriram Transport Finance Disclosures This research report has been prepared by MOSt to provide information about the company(ies) and sector(s), if any, covered in the report and may be distributed by it and/or its affiliated company(ies). This report is for personal information of the select recipient and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducement to invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your general information and should not be reproduced or redistributed to any other person in any form. This report does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, investors should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. MOSt and its affiliates are a full-service, integrated investment banking, investment management, brokerage and financing group. We and our affiliates have investment banking and other business relationships with a significant percentage of the companies covered by our Research Department Our research professionals provide important input into our investment banking and other business selection processes. Investors should assume that MOSt and/or its affiliates are seeking or will seek investment banking or other business from the company or companies that are the subject of this material and that the research professionals who were involved in preparing this material may participate in the solicitation of such business. The research professionals responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. Our research professionals are paid in part based on the profitability of MOSt which include earnings from investment banking and other business. MOSt generally prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. Additionally, MOSt generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all o the foregoing, among other things, may give rise to real or potential conflicts of interest . MOSt and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOSt or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays. The information contained herein is based on publicly available data or other sources believed to be reliable. Any statements contained in this report attributed to a third party represent MOSt’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. This Report is not intended to be a complete statement or summary of the securities, markets or developments referred to in the document. While we would endeavor to update the information herein on reasonable basis, MOSt and/or its affiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates or employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. MOSt or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of Interest Statement in this document. This should, however, not be treated as endorsement of the views expressed in the report. Disclosure of Interest Statement SHRIRAM TRANSPORT FINANCE Analyst ownership of the stock No Analyst Certification The views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsible for preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues. Regional Disclosures (outside India) This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions. For U.K. This report is intended for distribution only to persons having professional experience in matters relating to investments as described in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (referred to as "investment professionals"). This document must not be acted on or relied on by persons who are not investment professionals. Any investment or investment activity to which this document relates is only available to investment professionals and will be engaged in only with such persons. For U.S. Motilal Oswal Securities Limited (MOSL) is not a registered broker - dealer under the U.S. Securities Exchange Act of 1934, as amended (the"1934 act") and under applicable state laws in the United States. In addition MOSL is not a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the "Acts), and under applicable state laws in the United States. Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by MOSL, including the products and services described herein are not available to or intended for U.S. persons. This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutional investors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major institutional investors and will be engaged in only with major institutional investors. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S., MOSL has entered into a chaperoning agreement with a U.S. registered broker-dealer, Motilal Oswal Securities International Private Limited. ("MOSIPL"). Any business interaction pursuant to this report will have to be executed within the provisions of this chaperoning agreement. The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker-dealer, MOSIPL, and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account. For Singapore Motilal Oswal Capital Markets Singapore Pte Limited is acting as an exempt financial advisor under section 23(1)(f) of the Financial Advisers Act(FAA) read with regulation 17(1)(d) of the Financial Advisors Regulations and is a subsidiary of Motilal Oswal Securities Limited in India. This research is distributed in Singapore by Motilal Oswal Capital Markets Singapore Pte Limited and it is only directed in Singapore to accredited investors, as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. In respect of any matter arising from or in connection with the research you could contact the following representatives of Motilal Oswal Capital Markets Singapore Pte Limited: Anosh Koppikar Kadambari Balachandran Email:anosh.Koppikar@motilaloswal.com Email : kadambari.balachandran@motilaloswal.com Contact(+65)68189232 Contact: (+65) 68189233 / 65249115 Office Address:21 (Suite 31),16 Collyer Quay,Singapore 04931 Motilal Oswal Securities Ltd Motilal Oswal Tower, Level 9, Sayani Road, Prabhadevi, Mumbai 400 025 Phone: +91 22 3982 5500 E-mail: reports@motilaloswal.com