Bajaj Finance: Strong growth momentum; hold

•

1 gefällt mir•218 views

Bajaj Finance reported net profit of Rs 211.4 cr (+20.3% YoY) in Q1FY15 which was above expectations primarily due to higher than expected Net Interest Income (NII). NII increased 23.2% YoY and 23.0% QoQ with increase in consumer durable segment.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Bajaj Finance: Strong growth momentum; hold

Ähnlich wie Bajaj Finance: Strong growth momentum; hold (20)

Mehr von IndiaNotes.com

Mehr von IndiaNotes.com (20)

Bajaj Finance: Strong growth momentum; hold

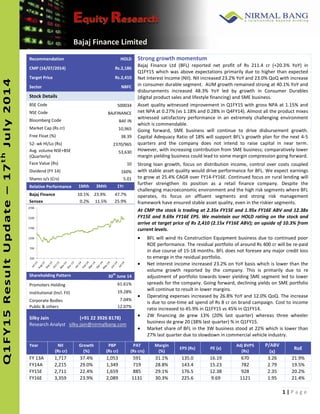

- 1. 1 | P a g e IInniittiiaattiinnggCCoovveerraaggee ttiiaattiinnggCCoovveerraaggee ttiinnggCCoovveerraaggee ggCCoovveerraaggee CCoovveerraaggee vveerraaggee rraaggee ggee Bajaj Finance Limited QQ11FFYY1155RReessuullttUUppddaattee––1177tthh JJuullyy22001144 4 Recommendation HOLD Strong growth momentum Bajaj Finance Ltd (BFL) reported net profit of Rs 211.4 cr (+20.3% YoY) in Q1FY15 which was above expectations primarily due to higher than expected Net Interest Income (NII). NII increased 23.2% YoY and 23.0% QoQ with increase in consumer durable segment. AUM growth remained strong at 40.1% YoY and disbursements increased 48.3% YoY led by growth in Consumer Durables (digital product sales and lifestyle financing) and SME business. Asset quality witnessed improvement in Q1FY15 with gross NPA at 1.15% and net NPA at 0.27% (vs 1.18% and 0.28% in Q4FY14). Almost all the product mixes witnessed satisfactory performance in an extremely challenging environment which is commendable. Going forward, SME business will continue to drive disbursement growth. Capital Adequacy Ratio of 18% will support BFL’s growth plan for the next 4-5 quarters and the company does not intend to raise capital in near term. However, with increasing contribution from SME business; comparatively lower margin yielding business could lead to some margin compression going forward. Strong loan growth, focus on distribution income, control over costs coupled with stable asset quality would drive performance for BFL. We expect earnings to grow at 25.4% CAGR over FY14-FY16E. Continued focus on rural lending will further strengthen its position as a retail finance company. Despite the challenging macroeconomic environment and the high risk segments where BFL operates, its focus on affluent segments and strong risk management framework have ensured stable asset quality, even in the riskier segments. At CMP the stock is trading at 2.35x FY15E and 1.95x FY16E ABV and 12.38x FY15E and 9.69x FY16E EPS. We maintain our HOLD rating on the stock and arrive at target price of Rs 2,410 (2.15x FY16E ABV); an upside of 10.3% from current levels. BFL will wind its Construction Equipment business due to continued poor ROE performance. The residual portfolio of around Rs 400 cr will be re-paid in due course of 15-18 months. BFL does not foresee any major credit loss to emerge in the residual portfolio. Net interest income increased 23.2% on YoY basis which is lower than the volume growth reported by the company. This is primarily due to re adjustment of portfolio towards lower yielding SME segment led to lower spreads for the company. Going forward, declining yields on SME portfolio will continue to result in lower margins. Operating expenses increased by 26.8% YoY and 12.0% QoQ. The increase is due to one-time ad spend of Rs 8 cr on brand campaign. Cost to income ratio increased to 45.9% in Q1FY15 vs 45% in Q1FY14. 2W financing de grew 13% (20% last quarter) whereas three wheeler business de grew 20 (38% last quarter) % in Q1FY15. Market share of BFL in the 3W business stood at 22% which is lower than 27% last quarter due to slowdown in commercial vehicle industry. CMP (16/07/2014) Rs.2,186 Target Price Rs.2,410 Sector NBFC Stock Details BSE Code 500034 NSE Code BAJFINANCE Bloomberg Code BAF IN Market Cap (Rs cr) 10,965 Free Float (%) 38.39 52- wk HI/Lo (Rs) 2370/965 Avg. volume NSE+BSE (Quarterly) 53,630 Face Value (Rs) 10 Dividend (FY 14) 160% Shares o/s (Crs) 5.01 Relative Performance 1Mth 3Mth 1Yr Bajaj Finance 10.1% 23.9% 47.7% Sensex 0.2% 11.5% 25.9% 200 700 1200 1700 2200 2700 Shareholding Pattern 30 th June 14 Promoters Holding 61.61% Institutional (Incl. FII) 19.28% Corporate Bodies 7.04% Public & others 12.07% Silky Jain (+91 22 3926 8178) Research Analyst silky.jain@nirmalbang.com Year NII (Rs cr) Growth (%) PBP (Rs cr) PAT (Rs crs) Margin (%) EPS (Rs) PE (x) Adj BVPS (Rs) P/ABV (x) RoE FY 13A 1,717 37.4% 1,053 591 31.1% 135.0 16.19 670 3.26 21.9% FY14A 2,215 29.0% 1,349 719 28.8% 143.4 15.23 782 2.79 19.5% FY15E 2,711 22.4% 1,659 885 29.1% 176.5 12.38 928 2.35 20.2% FY16E 3,359 23.9% 2,089 1131 30.3% 225.6 9.69 1121 1.95 21.4%

- 2. 2 | P a g e IInniittiiaattiinnggCCoovveerraaggee ttiiaattiinnggCCoovveerraaggee ttiinnggCCoovveerraaggee ggCCoovveerraaggee CCoovveerraaggee vveerraaggee rraaggee ggee Bajaj Finance Limited QQ11FFYY1155RReessuullttUUppddaattee––1177tthh JJuullyy22001144 Source: Company data, Nirmal Bang Research Asset under management grew by 40.1% YoY and 12.0% on QoQ basis. The growth was primarily driven by the SME segment followed by consumer durables segment. Going forward, management expects balance sheet to grow at 20-25%+ for FY15E. Overall disbursements witnessed growth of 48.3% YoY largely driven by SME which increased 53.9% and Consumer Durable which grew by 48% YoY. In consumer electronics financing, the company has retained its market share at 15%. The pace of growth in Loan against property moderated this quarter after fraud was reported in the segment in May 2014. BFL has taken various steps to ensure that such type of occurrence does not arise again. It is in the process of hiring operational risk head for newly formed division and will closely monitor the activities. In the current quarter the growth in LAP has picked up again. Commercial Infra business continued to de-grow due to sectoral stress. BFL continued to grow its auto component finance business. Lifestyle financing witnessed robust 216% growth with disbursement of 56,000 loans in Q1FY15. Quarterly comparison Financial Details (Rs cr) Q1FY15 Q1FY14 YoY (%) Q4FY14 QoQ (%) AUM 26,943 19,229 40.1% 24,061 12.0% Customers acquired 1,252,294 969,447 29.2% 768,137 63.0% Disbursements 9,266 6,250 48.3% 7,042 31.6% Consumer Durables 5,052 3,413 48.0% 3,179 58.9% SME business 3,279 2,130 53.9% 3,019 8.6% Commercial 885 707 25.2% 808 9.5% Rural 50 0 N/A 36 N/A Net Interest Income 680.5 552.3 23.2% 553.2 23.0% Non interest income 65.9 48.7 35.2% 91.8 (28.2%) Total Income 746.3 601.0 24.2% 645.0 15.7% Total operating expenses 342.8 270.3 26.8% 306.1 12.0% Cost to income ratio 45.9% 45.0% 47.5% Operating profit 403.5 330.7 22.0% 338.9 19.1% Provisions 82.9 63.9 29.8% 62.2 33.4% Profit before tax 320.6 266.9 20.1% 276.8 15.8% Tax 109.2 91.1 19.9% 94.7 15.4% Profit after tax 211.4 175.7 20.3% 182.1 16.1% EPS 42.2 35.3 19.4% 36.3 16.1% Capital adequacy ratio 18.0% 21.5% 19.1% Gross NPA 1.13% 1.14% 1.18% Net NPA 0.27% 0.25% 0.28% Provision coverage ratio 76.0% 78.0% 76.0%

- 3. 3 | P a g e IInniittiiaattiinnggCCoovveerraaggee ttiiaattiinnggCCoovveerraaggee ttiinnggCCoovveerraaggee ggCCoovveerraaggee CCoovveerraaggee vveerraaggee rraaggee ggee Bajaj Finance Limited QQ11FFYY1155RReessuullttUUppddaattee––1177tthh JJuullyy22001144 Cross sell momentum across businesses continued to perform good. Digital product sales contributed 10% to total Consumer durable business. Within the Rural Lending business BFL disbursed 50 Crs in Q1FY14. It also launched 14 new branches & 52 spokes in central Maharashtra & Gujarat. Distribution fee based income continues to remain strong with growth in fee based products like life and general insurance, wealth management and CRISIL ratings. BFL continued to increase its focus on garnering fixed deposit. Fixed Deposit during the quarter stood at Rs 137 cr taking the total deposit book to 345 Crs. Average deposit size is 2.78 lakhs and tenor is 26 months. The average cost stands at 9.84%. Current mix of bank & debt markets for BFL stands at 56:42. Balance 2% is from retail deposits. Gross NPA and net NPA remained broadly stable at lower levels. Provision coverage ratio stood at 76%. The company made an accelerated provision of 5 Crs for stressed Infra account in Q1FY14. Furthermore provision of Rs 5 cr was made for misrepresentation of LAP account in the month of May. As per the management, the actual liability should be around Rs 1.5 cr and the balance Rs 3.5 cr is likely to be reversed going forward. Capital consumption was higher in the quarter with rapid growth in the consumer durable segment. Source: Company data, Nirmal Bang Research Source: Company data, Nirmal Bang Research 19,229 19,829 22,461 24,061 26,943 11,000 15,000 19,000 23,000 27,000 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 AssetUnder Management 54.5%35.4% 9.6% 0.5% Break up of disbursement Consumer SME Commercial Rural 40.0% 53.0% 7.0% Break up of AUM Consumer SME Commercial 82% 18% Portfolio composition Secured Unsecured

- 4. 4 | P a g e IInniittiiaattiinnggCCoovveerraaggee ttiiaattiinnggCCoovveerraaggee ttiinnggCCoovveerraaggee ggCCoovveerraaggee CCoovveerraaggee vveerraaggee rraaggee ggee Bajaj Finance Limited QQ11FFYY1155RReessuullttUUppddaattee––1177tthh JJuullyy22001144 Source: Company data, Nirmal Bang Research Source: Company data, Nirmal Bang Research 0 500 1000 1500 2000 2500 3000 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 P/E - Forward CMP 3.0 X 6.0X 9.0 X 12.0X 15.0 X 0 500 1000 1500 2000 2500 3000 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14 P/BV- Forward CMP 0.5X 1.0X 1.5X 2.0X 2.5X 0.25% 0.26% 0.23% 0.28% 0.27% 78.0% 78.0% 80.0% 76.0% 76% 74.0% 75.0% 76.0% 77.0% 78.0% 79.0% 80.0% 81.0% 0.00% 0.05% 0.10% 0.15% 0.20% 0.25% 0.30% Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Movement of NPA Net NPA Provisioncoverage ratio 45.0% 47.6% 44.3% 47.5% 45.9% 42.0% 44.0% 46.0% 48.0% Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Costto Income Ratio

- 5. 5 | P a g e IInniittiiaattiinnggCCoovveerraaggee ttiiaattiinnggCCoovveerraaggee ttiinnggCCoovveerraaggee ggCCoovveerraaggee CCoovveerraaggee vveerraaggee rraaggee ggee Bajaj Finance Limited QQ11FFYY1155RReessuullttUUppddaattee––1177tthh JJuullyy22001144 Financials Profitability (Rs. Crs) FY13 FY14 FY15E FY16E Balance Sheet (Rs. Crs) FY13 FY14 FY15E FY16E Interest earned 2,923 3,789 4,898 6,045 Equity capital 50 50 50 50 Interest expended 1,206 1,573 2,187 2,686 Warrants money 0 0 0 0 Net interest income 1,717 2,215 2,711 3,359 Reserves and surplus 3,317 3,941 4,721 5,734 Non interest income 187 285 330 378 Net worth 3,367 3,991 4,770 5,784 Total income 1,904 2,500 3,041 3,736 Secured Loans 7,503 10,478 13,732 16,840 Marketing exp 183 231 284 349 Unsecured Loans 2,080 5,473 6,462 7,217 Staff costs 245 341 426 528 Total Loans 9,583 15,950 20,193 24,057 Other Op Exp 423 580 672 770 Curr Liab 4,764 4,509 5,955 8,329 Profit before prov 1,053 1,349 1,659 2,089 Long Term Liab 107 168 176 185 Provisions 182 258 317 374 Total liab and equity 17,821 24,618 31,095 38,355 Profit before tax 872 1,091 1,342 1,715 Cash and bank bal 416 777 477 649 Taxes 280 372 457 584 Investments 5 28 28 28 Net profit 591 719 885 1,131 Receivables 16,744 22,971 29,696 36,729 Quarterly (Rs. Crs) Sep.13 Dec.13 Mar.14 June.14 Fixed assets 176 220 242 266 Net interest income 519 618 553 680 Other assets 303 371 389 409 Non interest income 63 54 92 66 Other Long Term Assets 177 252 263 275 Total income 582 672 645 746 Total assets 17,821 24,618 31,095 38,355 Operating expenses 277 298 306 343 Operating profit 305 374 339 404 Key Ratios FY13 FY14 FY15E FY16E Provisions 52 79 62 83 Yield Ratios Profit before tax 253 295 277 321 Avg Yield on Assets 20.1% 19.1% 18.6% 18.2% Taxes 86 101 95 109 Cost of Int Bearing Liab 12.8% 12.3% 12.1% 12.1% Net profit 167 194 182 211 NIM/ Spread 7.3% 6.8% 6.5% 6.1% Profitability Ratios FY13 FY14 FY15E FY16E Gross NPA 1.3% 1.2% 1.3% 1.4% Cost / Income Ratio 44.7% 46.0% 45.4% 44.1% Net NPA 0.25% 0.28% 0.30% 0.35% Net profit margin 31.1% 28.8% 29.1% 30.3% Per share data FY13 FY14 FY15E FY16E RONW 21.9% 19.5% 20.2% 21.4% EPS 135.0 143.4 176.5 225.6 Return on Assets 3.8% 3.4% 3.2% 3.3% BVPS 679 796 951 1154 Growth Ratios FY13 FY14 FY15E FY16E Adj BVPS 670 782 928 1121 Advances growth 36.3% 37.2% 29.3% 23.7% DPS 15 16 18 20 NII growth 37.4% 29.0% 22.4% 23.9% Valuation Ratios FY13 FY14 FY15E FY16E PAT growth 45.5% 21.6% 23.1% 27.8% P/E 16.19 15.23 12.38 9.69 Pre prov profit growth 39.2% 28.1% 23.0% 25.9% P/BV 3.22 2.75 2.30 1.89 Non interest inc growth 6.2% 52.6% 15.7% 14.6% P/ABV 3.26 2.79 2.35 1.95 Source: Company data, Nirmal Bang Research

- 6. 6 | P a g e IInniittiiaattiinnggCCoovveerraaggee ttiiaattiinnggCCoovveerraaggee ttiinnggCCoovveerraaggee ggCCoovveerraaggee CCoovveerraaggee vveerraaggee rraaggee ggee Bajaj Finance Limited QQ11FFYY1155RReessuullttUUppddaattee––1177tthh JJuullyy22001144 NOTES Disclaimer: This Document has been prepared by Nirmal Bang Research (A Division of Nirmal Bang Securities PVT LTD). The information, analysis and estimates contained herein are based on Nirmal Bang Research assessment and have been obtained from sources believed to be reliable. This document is meant for the use of the intended recipient only. This document, at best, represents Nirmal Bang Research opinion and is meant for general information only. Nirmal Bang Research, its directors, officers or employees shall not in anyway be responsible for the contents stated herein. Nirmal Bang Research expressly disclaims any and all liabilities that may arise from information, errors or omissions in this connection. This document is not to be considered as an offer to sell or a solicitation to buy any securities. Nirmal Bang Research, its affiliates and their employees may from time to time hold positions in securities referred to herein. Nirmal Bang Research or its affiliates may from time to time solicit from or perform investment banking or other services for any company mentioned in this document. Nirmal Bang Research (Division of Nirmal Bang Securities PVT LTD) B-2, 301/302, Marathon Innova, Nr. Peninsula Corporate Park Lower Parel(W), Mumbai-400013 Board No. : 91 22 3926 8000/8001 Fax. : 022 3926 8010