Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Ähnlich wie United States face retirement tsunami .Will it hit Europe and Asia next?

Ähnlich wie United States face retirement tsunami .Will it hit Europe and Asia next? (20)

United States face retirement tsunami .Will it hit Europe and Asia next?

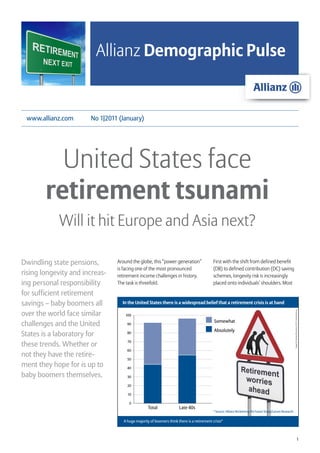

- 1. Allianz Demographic Pulse www.allianz.com No 1|2011 (January) United States face retirement tsunami Will it hit Europe and Asia next? Dwindling state pensions, Around the globe, this “power generation” First with the shift from defined benefit is facing one of the most pronounced (DB) to defined contribution (DC) saving rising longevity and increas- retirement income challenges in history. schemes, longevity risk is increasingly ing personal responsibility The task is threefold. placed onto individuals’ shoulders. Most for sufficient retirement savings – baby boomers all In the United States there is a widespread belief that a retirement crisis is at hand over the world face similar Image © Anthony Richardson, 2010 / shutterstock.de 100 Somewhat challenges and the United 90 Absolutely States is a laboratory for 80 these trends. Whether or 70 60 not they have the retire- 50 ment they hope for is up to 40 baby boomers themselves. 30 20 10 0 Total Late 40s * Source: Allianz Reclaiming the Future Study/Larson Research A huge majority of boomers think there is a retirement crisis* 1

- 2. Allianz Demographic Pulse No. 1|2011 (January) social security systems in Europe used to United States first to face “baby boomer tsunami” – but Europe and Asia follow closely feature generous Pay-As-You-Go approach- Percentage of population aged 60–65 es in the public pillar, yet recent reforms 10 reduced this generosity and increased the importance of non-public pillars. In the 9 Hongkong United States, the home of DC, less than Germany Hungary 10 percent of companies still offer DB 8 Italy Spain China Austria plans and in the UK, the number of DB pension funds open to new members has 7 Switzerland Belgium decreased to 27 percent1 in 2009. Hong UK Turkey Kong has reformed its pension system 6 U.S.A. France Thailand as well, intending to have a mandatory DC plan as the main pillar for retirement 5 provisions. 2015 2020 2025 2030 2035 2040 2045 2050 Year of biggest peak Source: UN World Population Prospects, 2008 Second, individuals experience the pleasure and the pain of increasing life The rectangles show the year with the highest percentage of the population in the pensionable age (60–65) in the respective countries expectancies. When Chancellor Otto von Bismarck introduced one of the first nation- wide social security system in Germany As the above graph shows, baby boomer Retirement crisis at hand in the late 19th century, life expectancy entry into retirement will peak at different One of the most striking findings of the for men amounted to 45 years while the points in time across the countries. The Reclaiming the Future study was the almost retirement age was 70 years. Today, men United States acts as a trailblazer and is universal agreement that the United States can expect to live to age 72.3 in Europe followed by Central European countries is facing a retirement crisis. When asked, (68.4 in Asia; 77.8 in North America)2 and and Hong Kong. Southern and Eastern “Do you believe there is a retirement crisis will probably live even longer in the future. European countries as well as Thailand will in this country?” an overwhelming 92 per- Time spent in retirement and the required succeed a few years later. cent of the respondents answered affirma- funding will therefore grow unless the tively. Among those in their late 40s, that retirement age is increased proportionally. When entering into retirement, the number rose to 97 percent. To mitigate the effects of this development, sheer magnitude of baby boomers will Germany, the Netherlands and the UK significantly increase the number of While this finding points to a startlingly raised their retirement age to at least 67 people dependent on contributions from universal concern, the study revealed years. France increased the earliest retire- the working population and will thereby even greater significance in the personal ment age from 60 to 62. accentuate the above mentioned issues. ripple effect it had on many respondents. The realization that there is a crisis has left The third challenge savers face is invest- Consequently, current US develop- them feeling unsure of their own retire- ment risk. The shift from DB to DC transfers ments can serve as a crystal ball for ment in two primary areas: preparedness the responsibility for investment decisions other nations and Reclaiming the Future, and adequacy of savings. onto the saver and during market down- the study developed by Allianz Life, turns like the recent financial crisis, DC plan helps understand what we see in it. Respondents’ confidence in their retire- participants can suffer heavy losses. In the ment preparedness was shaky, at best. United States, where DC schemes are The study digs deep into the changing Among those aged 44–54, more than half widely used, savers lost 30 to 40% of their attitudes and examines baby boomers’ (51 percent) said they feel unprepared for value virtually overnight3 and although preparation for and expectations of retire- retirement. The study’s participants also some European countries require plan ment in the United States. More than providers to offer minimum guarantees, 3,200 US adults, aged 44–75, were exposure to investment risk increased for surveyed to discover the unique needs, 1 Source: Pension Policy Institute Europeans savers as well. While markets perceptions, and strategies that define this 2 UN World Population Prospects, 2008 are currently recovering, the continued generation’s need to rethink retirement. 3 Investment Company Institute, Enduring volatility has stirred some deep-seated It also looked into consumer and financial Confidence in the 401(k) System, U.S. Retirement fears for many people. professional attitudes toward annuities Assets, January 2010 and their role in providing lifetime income. 2

- 3. Allianz Demographic Pulse No. 1|2011 (January) expressed concerns about their savings. Most Americans fear outliving their retirement income more than death Overall, 57 percent said they are worried Image © Pavel Shchegolev, 2010 / shutterstock.de that their nest egg may not be large Death Outliving my money enough in retirement. In fact, 47 percent are afraid of not being able to cover their basic living expenses in retirement. 39% Americans affected deeply 61% Adding to the fears about savings is the market uncertainty of the past two years. The recent downturn affected many Americans deeply – and they are continuing to feel those effects today. Of the people surveyed, 56 percent of those aged 44–54 agree that the “recent market events created major questions * Source: Allianz Reclaiming the Future Study/Larson Research around when, and whether, I can retire.” Question: Which do you fear most? Death or outliving money in retirement? * Yet, despite these fears, the global retire- ment market is expected to grow to $45 trillion until 2020 – led by the United death?” A surprising 61 percent of the viduals surveyed were allowed to choose States, where pension assets are expected respondents said they were more scared from a wide selection of variables that to grow at 3.6 percent compound annual of outliving their assets than they were included high returns, low fees, access to growth rate to reach 20.9 trillion by 2020. of dying. Among people aged 44–49, that money, and so forth. Increasingly, these assets will come from number climbed to 77 percent. And a the 401(k) plans of US workers since the whopping 82 percent of those in their late Reclaiming the future shift from defined benefit to defined 40s who had dependents were more afraid The most-selected feature was “the ability contribution plans has led to an indi- of outliving their money than they were to create a stable, predictable standard vidualization of retirement savings. This of death. of living throughout retirement.” In second trend toward increased savings and more and third place, respectively, was the responsibility for those savings indicates The study also explored other areas of “ability to provide a guaranteed income that Americans are beginning to take con- retirement insecurity, asking respondents to stream for life” and “guaranteed not to trol of their retirement planning, but data consider which is likelier: getting their full lose value.” When asked to choose be- from the study suggest that they are still due from Social Security or getting struck tween high returns or guarantees, 69 per- uncertain about their retirement income by lightning. More than one-third (39%) cent of those surveyed said they’d prefer and whether or not it will be there when said it’s more likely to be hit by lightning. a product that was “guaranteed not to they need it. This all points to the reality that retirement lose value,” while only 31 percent chose planning in the United States needs to a product whose goal was “providing a Increasing life expectancies mean that change, and boomers need more options high return.” Americans are spending more years in to help ensure the safety of their retire- retirement. Unfortunately – as pension ment savings. When planning for retire- An overwhelming 80 percent of the plans disappear and Social Security ment, Americans must now address three people surveyed preferred a product benefits dwindle – they’re also funding challenges. First they must look beyond with 4 percent return and a guarantee more of their own retirement. The defined benefit plans or Social Security for against losing value over a product with result – Americans are increasingly at their retirement income. Second, they 8 percent return and vulnerability to risk of outliving their assets. must guard against outliving their assets. market downturns. When asked to choose And third, they must find a way to protect between putting money into an annuity- Outliving assets their assets from market downturns. like product (moderate growth oppor- Consumers are aware of this risk – when tunity, monthly income, guaranteed for surveyed, an average of 59 percent of With these themes as a backdrop, the life, but limited access to the lump sum) all age groups reported worrying about Reclaiming the Future study asked con- vs. a similar instrument that provides total longevity. The study tackled the question sumers to consider the features that would access but risks running out of money, by asking, “which do you fear the most: be most important to them, if they could 56 percent chose the annuity-like product. outliving your money in retirement or build the ideal financial product. The indi- 3

- 4. Allianz Demographic Pulse No. 1|2011 (January) Despite the desire for the benefits these purchase, citing the protection of their income will disappear. They’ll risk out- products can provide, the study showed nest egg, protection from market down- living their savings. And they’ll be more that a surprising 54 percent of the respon- turns and guaranteed income for life vulnerable to market downturns. dents expressed distaste for the word as the key benefits. In fact, consumers “annuity.” Perhaps this is because more ranked annuities highest in satisfaction There are options than 50 percent formed their opinion among all financial instruments, beating As the Allianz Reclaiming the Future study of annuities more than 10 years ago. out mutual funds at 38 percent, stocks has demonstrated, Americans are aware Another 28 percent of respondents said at 36 percent, US Savings Bonds at of this looming crisis – and they are scared. they formed their opinion between 10 35 percent and CDs at 25 percent. (Gold Fortunately, there is hope. As the study and 20 years ago. And of those respon- and precious metals came in first, with also demonstrated, Americans do have dents, 64 percent admit that they haven’t a satisfaction rating of 62 percent) options as they face these challenges and researched annuities in the years since. plan for retirement. Further, the study An unprecedented number of Ameri- also found that annuities may be one of Distaste for the word annuity cans are preparing to retire, and they the most relevant of these options: Only At the same time, for those that own will face unprecedented challenges. annuities can offer the combination of annuities, 76 percent are happy with their Once-reliable sources of retirement principal protection and income for life. Editor: Katie Libbe, Allianz Life Minneapolis Publisher: Allianz SE, Königinstrasse 28, 80802 Munich, Germany | Claudia Mohr-Calliet, claudia.mohr-calliet@allianz.com I http://www.allianz.com Why does Allianz care about demography? Why does it matter to journalists and the public? What are the benefits of Allianz Demographic As a global financial service provider, Allianz believes Demographic change is challenging today’s societies Pulse? demographic change to be of crucial importance. in many ways: People are getting older, and this raises Allianz Demographic Pulse is based on the latest Identified as one of the major megatrends, demo- the issue e.g. of long-term care and dementia. research into various aspects of demographic change. graphic change will hold the key to many upcoming Furthermore in the future there will be a significant Conducted and written by Allianz experts, it highlights social challenges, whether with regard to health, old- decline in the workforce in all of the world’s markets, current and globally relevant demographic data and age provision, education, consumption or capital triggering for example a challenge in pension fund- provides an insight into their impact on worldwide markets. ing. Only information, awareness and discussion on economies and societies. To ensure up-to-date the topic will help to change attitudes, behavior and coverage of major developments in this field, Allianz situations, so hopefully solve urgent needs and come Demographic Pulse is published on a regular basis, up with innovative solutions. thus providing ongoing and detailed information about a major trend that is shaping the world we live in. More publications at: Do you have any comments, Allianz Group Economic Research & Corporate Development suggestions or questions? We look https://www.allianz.com/en/economic_research/publications/index.html forward to your feedback! International Pensions at Allianz Global Investors Please contact: Claudia Mohr-Calliet, http://publications.allianzgi.com/en/PensionResearch/Pages/PensionResearch.aspx ++49 89 3800 18797 Allianz Knowledge Site claudia.mohr-calliet@allianz.com http://knowledge.allianz.com/ These assessments are, as always, subject to the disclaimer provided below. Cautionary note regarding forward-looking statements: The statements contained herein may include statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertain-ties that could cause actual results, performance or events to differ materially from those expressed or implied in such state- ments. In addition to statements which are forward-looking by reason of context, the words “may”, “will”, “should”, “expects”, “plans”, “intends”, “anticipates”, “believes”, “estimates”, “predicts”, “potential”, or “continue” and similar expressions identify forward-looking statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (i) general economic conditions, including in particular economic conditions in the Allianz Group’s core business and core markets, (ii) performance of financial markets, including emerging markets, and including market volatility, liquidity and credit events (iii) the frequency and severity of insured loss events, including from natural catastrophes and including the development of loss expenses, (iv) mortality and morbidity levels and trends, (v) persistency levels, (vi) the extent of credit defaults, (vii) interest rate levels, (viii) currency exchange rates including the Euro/U.S. Dollar exchange rate, (ix) changing levels of competition, (x) changes in laws and regulations, including monetary convergence and the European Monetary Union, (xi) changes in the policies of central banks and/or foreign governments, (xii) the impact of acquisitions, including related integration issues, (xiii) reorganization measures, and (xiv) general competitive factors, in each case on a local, regional, national and/or global basis. Many of these factors may be more likely to occur, or more pronounced, as a result of terrorist activities and their consequences. The company assumes no obligation to update any forward-looking statement. No duty to update: The company assumes no obligation to update any information contained herein. 4