Quick Doctor In Kuwait +2773`7758`557 Kuwait Doha Qatar Dubai Abu Dhabi Sharj...

Nigeria risk

1. Nigeria

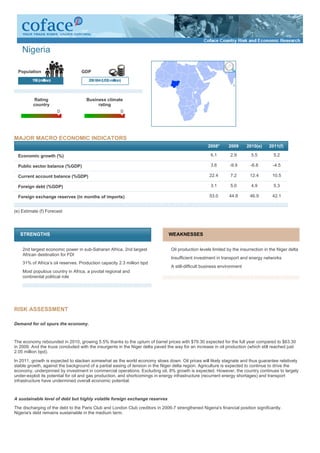

Population GDP

156(million) 206664(US$million)

Rating Business climate

country rating

MAJOR MACRO ECONOMIC INDICATORS

2008* 2009 2010(e) 2011(f)

Economic growth (%) 6.1 2.9 5.5 5.2

Public sector balance (%GDP) 3.6 -9.9 -6.8 -4.5

Current account balance (%GDP) 22.4 7.2 12.4 10.5

Foreign debt (%GDP) 3.1 5.0 4.9 5.3

Foreign exchange reserves (in months of imports) 53.0 44.8 46.9 42.1

(e) Estimate (f) Forecast

STRENGTHS WEAKNESSES

2nd largest economic power in sub-Saharan Africa, 2nd largest Oil production levels limited by the insurrection in the Niger delta

African destination for FDI

Insufficient investment in transport and energy networks

31% of Africa’s oil reserves. Production capacity 2.3 million bpd

A still-difficult business environment

Most populous country in Africa, a pivotal regional and

continental political role

RISK ASSESSMENT

Demand for oil spurs the economy.

The economy rebounded in 2010, growing 5.5% thanks to the upturn of barrel prices with $79.30 expected for the full year compared to $63.30

in 2009. And the truce concluded with the insurgents in the Niger delta paved the way for an increase in oil production (which still reached just

2.05 million bpd).

In 2011, growth is expected to slacken somewhat as the world economy slows down. Oil prices will likely stagnate and thus guarantee relatively

stable growth, against the background of a partial easing of tension in the Niger delta region. Agriculture is expected to continue to drive the

economy, underpinned by investment in commercial operations. Excluding oil, 8% growth is expected. However, the country continues to largely

under-exploit its potential for oil and gas production, and shortcomings in energy infrastructure (recurrent energy shortages) and transport

infrastructure have undermined overall economic potential.

A sustainable level of debt but highly volatile foreign exchange reserves

The discharging of the debt to the Paris Club and London Club creditors in 2006-7 strengthened Nigeria's financial position significantly.

Nigeria's debt remains sustainable in the medium term.

2. However, the crisis has highlighted the extreme volatility in the level of foreign exchange reserves, which would not suffice to overcome a

permanent shock to growth, especially one resulting from a long-term drop in oil production. In addition, money is siphoned off from the Nigerian

oil fund, as political tensions ebb and flow, by the local governors who believe it unlawful for the federal government to retain the funds. The fund

has melted away from $20 billion in 2007 to under $500 million in August 2010. It is thus expected to be virtually exhausted by 2011.

A banking sector in the process of reconsolidation

Recapitalization of the banking sector by the CBN has prevented a systemic crisis. The establishment of a defeasance structure at the end of

2010 will likely speed up the consolidation of banks' balance sheets, in particular by bolstering the confidence of potential foreign investors.

However, increased concentration in the sector is likely, as is the expansion of those banks spared by the crisis. These two trends are expected

to result in deterioration in the quality of the banks' portfolios.

The business environment remains shaky, but some progress has been made in the political arena

Nigeria's political and institutional shortcomings constitute a critical risk factor. Governance deficiencies were the root cause of the banking crisis

and have deterred investment, particularly in oil. The death of President Umaru Yar'Adua in May 2010 brought Vice-President Goodluck

Jonathan to power temporarily. He has initiated a series of reforms, which, if successful, could eliminate the bottlenecks restricting growth in the

country. The interim President also seems committed to developing and pacifying the Niger delta region, which is where he was born. These

prospects will only pan out if, as appears likely, he is elected in April 2011.