2. Most reports analyse past

results (lag indicators)

instead of the factors that

will determine the future

performance and

profitability (lead

indicators).....

The nature of doing business and

competing is currently changing

dramatically. Quality, innovation

and service are just as essential

as costs to survive and grow, but

are hardly mentioned in existing

reports.....

The reports sometimes

stimulate actions that have a

positive impact on the short

term results, but a negative

effect on the long term.....

Only looking at financial measurements often

doesn’t provide complete steering information

3. Who are our profitable customers?

Do we pay the most attention to those customers?

Do we know what these customers expect from us now and

in the (near) future?

Do we develop the products and services that will keep us in

the running?

Do our employees develop the knowledge and skills that the

markets (will) ask?

Do we recruit the right people?

4. Reliance on only financial measures of performance as

the one true way to gauge success, &

Inability of many organizations to successfully execute

their strategies.

the need for a Balanced

Scorecard system

Reasons

6. BSC IS A PERFORMANCEManagement TECHNIQUE

DEVELOPEDBY :

ROBERT S KAPLAN

AND

DAVIDNORTON

PROFESSORS AT

HARVARDBUSINESS SCHOOL

IN 1992

7. Where did the BSC come from?

THEN NOW

Industrial revolution Information age

Financial measures Non-financial measures

Tangible assets Intangible assets

Lagging indicators Leading indicators

8. “The balanced scorecard retains traditional financial

measures. But financial measures tell the story of past

events, an adequate story for industrial age companies for

which investments in long-term capabilities and customer

relationships were not critical for success.

These financial measures are inadequate, however, for

guiding and evaluating the journey that information age

companies must make to create future value through

investment in customers, suppliers, employees, processes,

technology, and innovation.“ -Norton and Kaplan

BSC translates an organization’s mission and strategy into a set of

performance measures that provides the framework for

implementing the strategy.

9. “Balanced Score Card" as a set of measures that gives top

managers a fast but comprehensive view of the business.

The balanced scorecard includes financial measures that

tell the results of actions already taken.

It complements the financial measures with operational

measures on customer satisfaction, internal processes,

and the organization's innovation and improvement

activities- operational measures that are the drivers of

future financial performance.

- Kaplan and Norton (1992)

10. What is a Balanced Score Card?

1) A measurement system

2) A strategic management system

3) A communication tool

11. Translating with the BSC

Desired state

Differentiating activities

What must be done

well to implement

strategies

How strategic

success is

measured

Mission

Vision

Strategy/Goals

Objectives

In each perspective

Measures

In each perspective

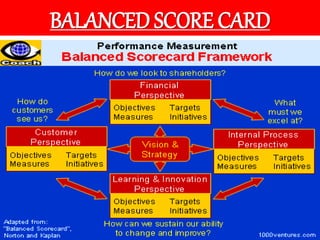

12. BSC as a Measurement System

Translates mission, vision and

strategy through objectives and

measures

Provides a framework to describe the

key elements in the achievement of

the strategy

Measures four perspectives:

- Financial

- Customer Relations

- Internal Business Processes

- Learning, Innovation and Growth

14. INTERNAL VALUE CHAIN

CUSTOMER

NEED

IDENTIFIED

Innovation cycle:

-Identify the market

-Create the product

Operating cycle:

-Build the product

-Deliver the product

Post sales services cycle:

Service the customer

CUSTOMER

NEED

FULFILLED

15. Knowledge, Skills, Systems, and Tools

Financial

Results

To Build the Strategic Capabilities..

Needed to Deliver Unique

Sets of Benefits to Customers...

To Drive Financial

Success...

And Realize

the Vision

Equip our People...

Internal

Capabilities

Customer

Benefits

INTERRELATIONSHIP BETWEEN FOUR

PERSPECTIVES OF BSC

16. FINANCIAL: Revenue generated, ROS, ROI, RI,

EVA, MVA

CUSTOMERS:

INTERNAL BUSINESS PROCESSES :

Customer acquisition, Customer satisfaction &

delight, Customer retention, Market share

-Processes adopted to enhance EVA

-Processes to serve the customer better e.g.

Internal Value Chain

LEARNING &GROWTH : Employees, Infrastructure, Systems

18. BSC as a StrategicManagement System

Translates strategy

into:

Objectives

Measures

Targets

Initiatives

19. Perspectives Objectives

FINANCIAL

To increase financial

growth

CUSTOMER

To increase Customer

satisfaction

INTERNAL BUSINESS

PROCESSES

To reduce cycle time,

To reduce defects &

costs

LEARNING AND GROWTH

To increase core

skills and systems

availability.

Vision &

Strategy

20. Perspective Objectives Measurements

Financial To increase

financial growth.

Revenue growth, Return of Capital Employed, Return on investment,

Operating income, Economic value added, gross margin, Cash flow etc.

Customer To increase

customer

satisfaction .

Customer satisfaction ratings, Customer-retention percentage, Market

share, Time taken to fulfil customers’ requests , no. of customer

complaints etc.

Internal To reduce cycle

business time,

Process To reduce defects

&

costs

Innovation - measures of how well the company identifies the

customers’ future needs, new-product development times, no. of new

products, etc.

Operations - Measures of quality, Cycle time, and costs, Defect rates,

Average time taken to respond to orders, etc.

Post sales service - measures for warranty, repair and treatment of

defects and returns, hours of customer training for using the product

etc.

Learning and To increase core

Growth skills and systems

availability.

People - employee retention, training, skills, morale, employee-

satisfaction ratings, employee turnover rates, percentage of employee

suggestions implemented etc.

Systems - measure of availability of critical real time information

21. 8. Sample Generic Scorecard

Perspectives Objectives Measurements

Learning &

Growth

Develop process skills

Align the employee & org’s goals

% of employees trained in process

management

Employee satisfaction ratings

Internal

Business

Process

Increase quality. Number of defects and

number of items reworked.

Improve post sales service Service response time

Customer

Increase on time delivery.

Percentage of deliveries

on time.

Reduce customer

complaints.

Number of customer

complaints.

Financial

Return on capital employed

Increase shareholders value

Return on investment

22. Perspectives Objectives Measurements

2012 2013

Financial Maximise Returns

Utilization of Assets

Revenue Growth

Return on Equity

Utilization Rates

% Change in

Revenues

12%

7%

+11%

13%

8%

+11%

Customer Customer Retention

Customer Relations

Retention %

% Self Initiated Calls

75%

35%

75%

40%

Internal

Processes

Fast Delivery

Effective Service

Turnaround Time

1st Time Resolvement

15m

68%

14m

69%

Learning &

Growth

High Skill Levels

Employee Satisfaction

Skill set ratio

Survey Index

65%

75%

68%

77%

Targets

23. Perspectives Objectives Measurements 2012 2013 Initiatives

Financial Maximum Returns

Utilization of Assets

Revenue Growth

Return on Equity

Utilization Rates

% Change in

Revenues

12%

7%

+11%

13%

8%

+11%

Customer Customer

Retention

Customer Relations

Retention %

% Self Initiated

Calls

75%

35%

75% Customer

40% Relation mgt.

Internal

Processes

Fast Delivery

Effective Service

Turnaround Time

1st Time

Resolvement

15m

68%

14m Cycle process

system

69% Customer

relations mgt.

Learning &

Growth

High Skill Levels

Employee

Satisfaction

Skill set ratio

Survey Index

65%

75%

68%

77% corporate

initiatives

Targets

24. IMPLEMENTATION OF THE BSC

AT INDIA LEVEL

1.Infosys Technologies

2.Philips Electronics

3.Nerolac Paints Limited

4.Gorej-GE Appliances

limited

5.Tata Consultancy

Services

AT GLOBAL LEVEL

1.ABB

2.Skandia

3.Analog Device, Inc.

4.Compaq

5.Halifax

6.Eletrolux