EXAMINABLE SUPPLEMENT

•

0 gefällt mir•308 views

The document summarizes key aspects of an examinable supplement issued by ICAP related to auditing. It covers 5 learning objectives: 1. Elements of an auditor's report under ISA 700 (revised). 2. Differences between report formats under ISA 700 versus Form 35A. 3. Determining and communicating key audit matters to those charged with governance. 4. Communication of key audit matters in the auditor's report for listed entities. 5. Revised definition and examples of emphasis of matter.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie EXAMINABLE SUPPLEMENT

Ähnlich wie EXAMINABLE SUPPLEMENT (20)

Mehr von MUHAMMAD HUZAIFA CHAUDHARY

Mehr von MUHAMMAD HUZAIFA CHAUDHARY (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

EXAMINABLE SUPPLEMENT

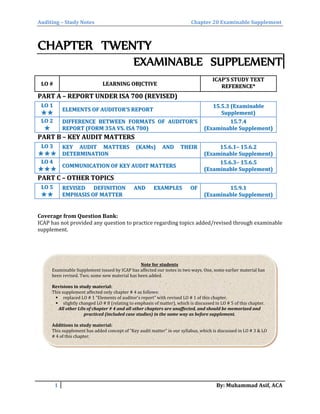

- 1. Auditing – Study Notes Chapter 20 Examinable Supplement CHAPTER TWENTY EXAMINABLE SUPPLEMENT LLOO ## LLEEAARRNNIINNGG OOBBJJCCTTIIVVEE IICCAAPP''SS SSTTUUDDYY TTEEXXTT RREEFFEERREENNCCEE** PPAARRTT AA –– RREEPPOORRTT UUNNDDEERR IISSAA 770000 ((RREEVVIISSEEDD)) LLOO 11 ✯✯✯✯ EELLEEMMEENNTTSS OOFF AAUUDDIITTOORR’’SS RREEPPOORRTT 1155..55..33 ((EExxaammiinnaabbllee SSuupppplleemmeenntt)) LLOO 22 ✯✯ DDIIFFFFEERREENNCCEE BBEETTWWEEEENN FFOORRMMAATTSS OOFF AAUUDDIITTOORR’’SS RREEPPOORRTT ((FFOORRMM 3355AA VVSS.. IISSAA 770000)) 1155..77..44 ((EExxaammiinnaabbllee SSuupppplleemmeenntt)) PPAARRTT BB –– KKEEYY AAUUDDIITT MMAATTTTEERRSS LLOO 33 ✯✯✯✯✯✯ KKEEYY AAUUDDIITT MMAATTTTEERRSS ((KKAAMMss)) AANNDD TTHHEEIIRR DDEETTEERRMMIINNAATTIIOONN 1155..66..11–– 1155..66..22 ((EExxaammiinnaabbllee SSuupppplleemmeenntt)) LLOO 44 ✯✯✯✯✯✯ CCOOMMMMUUNNIICCAATTIIOONN OOFF KKEEYY AAUUDDIITT MMAATTTTEERRSS 1155..66..33–– 1155..66..55 ((EExxaammiinnaabbllee SSuupppplleemmeenntt)) PPAARRTT CC –– OOTTHHEERR TTOOPPIICCSS LLOO 55 ✯✯✯✯ RREEVVIISSEEDD DDEEFFIINNIITTIIOONN AANNDD EEXXAAMMPPLLEESS OOFF EEMMPPHHAASSIISS OOFF MMAATTTTEERR 1155..99..11 ((EExxaammiinnaabbllee SSuupppplleemmeenntt)) Coverage from Question Bank: ICAP has not provided any question to practice regarding topics added/revised through examinable supplement. Note for students Examinable Supplement issued by ICAP has affected our notes in two ways. One, some earlier material has been revised. Two, some new material has been added. Revisions in study material: This supplement affected only chapter # 4 as follows: replaced LO # 1 “Elements of auditor’s report” with revised LO # 1 of this chapter. slightly changed LO # 8 (relating to emphasis of matter), which is discussed in LO # 5 of this chapter. All other LOs of chapter # 4 and all other chapters are unaffected, and should be memorized and practiced (included case studies) in the same way as before supplement. Additions in study material: This supplement has added concept of “Key audit matter” in our syllabus, which is discussed in LO # 3 & LO # 4 of this chapter. 1 By: Muhammad Asif, ACA

- 2. Auditing – Study Notes Chapter 20 Examinable Supplement PART A – REPORT UNDER ISA 700 (REVISED) LLOO 11:: EELLEEMMEENNTTSS OOFF AANN UUNNMMOODDIIFFIIEEDD AAUUDDIITTOORR’’SS RREEPPOORRTT:: Title: The auditor’s report shall have a title that clearly indicates that it is the report of an independent auditor. Title is necessary to differentiate auditor’s report from other type of reports issued by others. Addressee The auditor’s report shall be addressed, as appropriate, based on the circumstances of the engagement. Law, regulation or the terms of the engagement may specify to whom the auditor’s report is to be addressed. Normally report is addressed to shareholders or those charged with governance. Opinion: The first section of the auditor’s report shall include the auditor’s opinion, and shall have the heading “Opinion.” The Opinion section of the auditor’s report shall also: (a) State that the financial statements have been audited; (b) Identify the entity whose financial statements have been audited; (c) Identify the title of each statement comprising the financial statements; (d) Refer to the notes, including the summary of significant accounting policies; and (e) Specify the date of, or period covered by, each financial statement comprising the financial statements. Basis for Opinion: The auditor’s report shall include a section, directly following the Opinion section, with the heading “Basis for Opinion”, that: (a) States that the audit was conducted in accordance with International Standards on Auditing; (b) Refers to the section of the auditor’s report that describes the auditor’s responsibilities under the ISAs; (c) Includes a statement that the auditor is independent of the entity in accordance with the relevant ethical requirements relating to the audit, and has fulfilled the auditor’s other ethical responsibilities in accordance with these requirements. (d) States whether the auditor believes that the audit evidence the auditor has obtained is sufficient and appropriate to provide a basis for the auditor’s opinion. Material uncertainty related to Going Concern (if applicable): This section is required in the auditor’s report to highlight the existence of any material uncertainties related to going concern (if any). Key Audit Matters: For listed entities, the auditor shall communicate key audit matters in the auditor’s report. Responsibilities of Management and TCWG for the Financial Statements: 1. This section of the auditor’s report shall describe management’s responsibility for: a. Preparing the financial statements in accordance with the AFRF, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error; and b. Assessing the entity’s ability to continue as a going concern and whether the use of the going concern basis is appropriate. If applicable, matters relating to going concern will also be disclosed. 2. This section shall also identify those responsible for the oversight of the financial reporting process. Auditor’s Responsibilities for the Audit of the Financial Statements: This section of the auditor’s report shall state that: 1. objectives of the auditor are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement (whether due to fraud or error), and to issue report that includes the auditor’s opinion on financial statements. 2. reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists; and misstatements can arise from fraud or error which could be material (also provide definition of materiality here) 2 By: Muhammad Asif, ACA

- 3. Auditing – Study Notes Chapter 20 Examinable Supplement This section shall further: 1. State that auditor exercises professional judgment and maintains professional skepticism throughout the audit 2. Describe an audit by stating that auditor is responsible: i. To identify and assess risk of material misstatement (whether due to fraud or error), to design and perform audit procedures responsive to those risks, and to obtain sufficient appropriate audit evidence on which to base opinion. ii. To obtain an understanding of internal control relevant to the audit to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. iii. To evaluate the appropriateness of accounting policies and the reasonableness of accounting estimates and related disclosures made by management. iv. To conclude on the appropriateness of management’s use of the going concern basis of accounting, and whether a material uncertainty exists related to events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern. v. To evaluate whether financial statements present true and fair view (if fair presentation framework is used by management) Regarding communication with TCWG, responsibilities of the auditor shall also state that auditor communicates following to TCWG: 1. Scope and timing of audit. 2. Significant audit findings (including significant deficiencies in internal control that auditor identifies) 3. Statement that auditor has complied with ethical requirements regarding independence, and also communicates all relationships and other matters that may impair independence with related safeguards (for listed entities) 4. Key audit matters (for listed entities). In case of group audit, responsibilities of auditor shall also state that auditor is responsible: for the direction, supervision and performance of the group audit (i.e. to develop audit strategy covering risk assessment, materiality levels, and type of work to be performed on components); to obtain sufficient appropriate audit evidence regarding financial information of components within the group, and to issue report which includes auditor’s opinion on group financial statements.. Name of the Engagement Partner: The name of the engagement partner shall be included in the auditor’s report for listed entities unless, in rare circumstances, such disclosure is reasonably expected to lead to a significant personal security threat. Other Reporting Responsibilities (if any): If auditor is required by local laws and regulations to report on matters other than financial statements, such matter shall also be covered in a separate section in audit report with a heading titled “Report on Other Legal and Regulatory Requirements” or otherwise as appropriate. Signature of the Auditor: The auditor’s report shall be signed: in the name of the audit firm, or in the personal name of the auditor or both, as appropriate for the particular jurisdiction Law or regulation may allow for the use of electronic signatures in the auditor’s report. Location of the description of the auditor’s responsibilities The description of the auditor’s responsibilities shall be included: (a) Within the body of the auditor’s report; (b) Within an appendix to the auditor’s report, in which case the auditor’s report shall include a reference to the location of the appendix; or (c) on a website of an appropriate authority, where law, regulation or national auditing standards expressly permit the auditor to do so, in which case the auditor’s report shall include a specific reference to the location of such a description 3 By: Muhammad Asif, ACA

- 4. Auditing – Study Notes Chapter 20 Examinable Supplement Date of the Auditor’s Report: The date of audit report should not be earlier than the date on which auditor obtains sufficient appropriate evidence on which his report is based (including evidence that financial statement have been prepared completely and recognized authority has taken its responsibility). Date also indicates that auditor has considered the effect of events and transactions upto that date. Auditor’s Address: The auditor’s report shall name the location in the jurisdiction where the auditor practices. CONCEPT REVIEW QUESTION List down the basic elements of an audit report. (05 marks) (CA Inter -Autumn 2004) ISA 700 Forming an Opinion and Reporting on Financial Statements provides guidance on the form and content of the auditor’s report and should contain a number of elements. Required: Describe FIVE elements of an unmodified auditor’s report. (05 marks) (ACCA F8 – December 2011) An audit report contains title, addressee, date, auditor’s opinion, auditor’s address and auditor’s signature. Describe the other essential elements of audit report. (06 marks) (CA Inter, Autumn 2006) The date is an important element of audit report. What date should the auditor put on the audit report and what does it represent? (03 marks) (CA Inter, Spring 2007) The auditor is required to issue an audit report at the end of the audit, which sets out his opinion on the financial statements. An important element of the audit report is the statement of auditor’s responsibility. Required: Narrate the matters that should be contained in the statement of auditor’s responsibility as included in an audit report issued under ISA-700 ‘The Independent Auditor’s Report on a Complete Set of General Purpose Financial Statements’. (08 marks) (CA Inter, Spring 2010) LLOO 22:: DDIIFFFFEERREENNCCEE BBEETTWWEEEENN FFOORRMMAATTSS OOFF AAUUDDIITTOORR’’SS RREEPPOORRTT ((FFOORRMM 3355AA VVSS.. IISSAA 770000)):: The matters which are required to be included in the audit report issued under the Companies Ordinance, 1984 only (i.e. not specified by ISA 700 ): 1. It is mentioned that the Auditor has obtained all the information and explanations which to the best of his knowledge and belief, were necessary for the purpose of his audit. 2. It is mentioned that the management is responsible to present the financial statements in conformity with the requirements of the Companies ordinance, 1984. 3. Whether the financial statements give the information required by the Companies Ordinance, 1984, and in the manner so required. 4. Opinion relating to maintenance of proper books of account as required by the Companies Ordinance, 1984. 5. Opinion whether the balance sheet and profit and loss account are drawn-up in conformity with the Companies Ordinance, 1984; 6. Opinion whether the balance sheet, profit and loss account and notes are: a. in agreement the books of account and b. are further in accordance with accounting policies consistently applied Exam Tip In Pakistan, Form 35A is used to issue reports, which has not been revised by SECP. Therefore, you should learn elements of the revised report under ISA 700 but there is no need to memorize report under ISA 700 (revised). 4 By: Muhammad Asif, ACA

- 5. Auditing – Study Notes Chapter 20 Examinable Supplement 7. Opinion whether the expenditure incurred during the year was for the purpose of the Company’s business 8. Opinion whether the business conducted, investments made and the expenditure incurred during the year were in accordance with the objects of the Company 9. Opinion as regards deduction and deposit of Zakat Matters which are required to be mentioned in the Audit Report prescribed under the ISA 700 only (i.e. not mentioned in Audit Report under the Companies Ordinance, 1984): 1. Basis for opinion paragraph which includes reference to auditor’s responsibilities under ISAs and a statement that auditor is independent. 2. A separate section for uncertainties related to Going Concern. 3. Key audit matters (in case of listed entities) 4. Responsibility of management to assess going concern status, and identification of those responsible for oversight of financial reporting process. 5. Auditor’s responsibilities: a. To explain reasonable assurance and materiality in audit report b. to exercise professional judgment and professional scepticism c. to identify and assess risk of material misstatement. d. to obtain understanding of internal control. e. to conclude on going concern f. to communicate scope, timing, significant audit findings, statement of independence and key audit matters to TCWG. 6. Responsibilities as Group Auditor CONCEPT REVIEW QUESTION State the key differences between an unmodified audit report issued in accordance with ISA 700 ‘Forming an Opinion and Reporting on Financial Statements’ and the audit report issued under the Companies Ordinance, 1984. (13 marks) (CA Inter, Autumn 2013) PART B – KEY AUDIT MATTERS LLOO 33:: KKEEYY AAUUDDIITT MMAATTTTEERRSS ((KKAAMMss)) AANNDD TTHHEEIIRR DDEETTEERRMMIINNAATTIIOONN:: Key audit matters are included in auditor’s report in case of listed entities, or in case of unlisted entities if it is required by law or regulation, or if auditor judges necessary to communicate it. What are “Key audit matters”: Those matters that, in the auditor’s professional judgment, are of most significance in the audit of the financial statements of the current period. Key audit matters are selected from matters communicated with those charged with governance. Determining the key audit matters: The auditor shall determine, from the matters communicated with TCWG, those matters that required significant auditor attention in performing the audit considering: Areas of higher assessed risk of material misstatement, or significant risks identified in accordance with ISA 315, or Significant auditor judgments relating to areas in the financial statements that involved significant management judgment (e.g. accounting estimates that have high estimation uncertainty), or The effect on the audit of significant events or transactions that occurred during the period. (e.g. significant transactions with related parties, or significant transactions outside the normal course of business). The auditor shall determine which of the matters determined in accordance with above paragraph were of most significance in the audit of the financial statements of the current period and therefore are the key audit matters. Other considerations that may be relevant in determining a key audit matter include: 1. The importance of the matter to intended users’ understanding. 2. The complexity or subjectivity involved in management’s selection of an appropriate policy compared to other entities within its industry. 5 By: Muhammad Asif, ACA

- 6. Auditing – Study Notes Chapter 20 Examinable Supplement 3. The nature and extent of audit effort needed to address the matter, including: a. The extent of specialized skill or knowledge needed to apply audit procedures to address the matter or evaluate the results of those procedures, if any. b. The nature of consultations outside the engagement team regarding the matter. 4. The severity of any control deficiencies identified relevant to the matter. LLOO 44:: CCOOMMMMUUNNIICCAATTIIOONN OOFF KKEEYY AAUUDDIITT MMAATTTTEERRSS:: Communication/Description/Presentation of Key Audit Matters in Audit Report: Key Audit Matters are described in audit report under the heading “Key Audit Matters”. Descriptions of Introductory Language: The introductory language of this section shall state that, “Key audit matters are those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements of the current period; and these matters were addressed in the context of the audit of the financial statements as a whole, and the auditor does not provide a separate opinion on these matters”. Descriptions of Individual Key Audit Matters: Thereafter, auditor shall describe each key audit matter one by one. For each key audit matter auditor is required to describe: 1. Why the matter was considered to be one of most significance in the audit 2. How the matter was addressed in the audit, including a brief overview of procedures performed; or an indication of the outcome of the auditor’s procedures; or key observations with respect to the matter, or some combination of these elements. 3. Reference to the related disclosure(s) in financial statements Communication of Key Audit Matters to TCWG: The auditor shall communicate with those charged with governance: (a) Those matters the auditor has determined to be the key audit matters; or (b) If applicable, the auditor’s determination that there are no key audit matters to communicate in the auditor’s report. Exception to the requirement of communication of Key Audit Matters: In following cases, key audit matters are not communicated in audit report: 1. If law or regulation precludes public disclosure about the matter 2. If, in extremely rare circumstances, the auditor determines that adverse consequences of such communication are more than public interest benefits of such communication 3. If auditor expresses disclaimer of opinion. Study Tip If the auditor determines that there are no key audit matters to communicate, the auditor shall include a statement to this effect in auditor’s report under the heading “Key Audit Matters.” Exam Tip Key Audit Matters are Not a Substitute for Expressing a Modified Opinion Matter requiring modification in opinion, or requiring emphasis of matter or other matter paragraph, and uncertainties relating to going concern are separately included in audit report; these are NOT included in key audit matters. 6 By: Muhammad Asif, ACA

- 7. Auditing – Study Notes Chapter 20 Examinable Supplement PART C – OTHER TOPICS LLOO 55:: RREEVVIISSEEDD DDEEFFIINNIITTIIOONN AANNDD EEXXAAMMPPLLEESS OOFF EEMMPPHHAASSIISS OOFF MMAATTTTEERR:: Revised Definition of Emphasis of matter paragraph/when to add in auditor’s report: Emphasis of Matter Paragraph is included if auditor considers it necessary to draw users’ attention to a matter which is disclosed in financial statement that is fundamental to users’ understanding of the financial statements, provided: The auditor is NOT required to modify his opinion because of the matter (i.e. matter is neither a misstatement nor scope limitation). Matter is not a key audit matter to be communicated in the auditor’s report (when relevant) Examples of Situations/ Circumstance when Emphasis of Matter paragraph is included: Example of doubt about going concern has been deleted, and following example has been added: If there is uncertainty relating to the future outcome of an exceptional litigation or regulatory action pending against company. A significant subsequent event that occurs between the date of the financial statements and the date of the auditor’s report When a major catastrophe has significantly affected or continues to affect entity’s financial position. Early application of a new accounting standard that has a material effect on financial statements. CONCEPT REVIEW QUESTION Define an ‘Emphasis of Matter paragraph’ and explain, providing examples, the use of such a paragraph; (06 marks) Note: You are not required to produce draft paragraph. (ACCA P7 – June 2010) 7 By: Muhammad Asif, ACA