Introducing Yellen

•

1 gefällt mir•351 views

An overview at Yellen's way to look at the US economy

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (19)

Andere mochten auch

Andere mochten auch (20)

Ähnlich wie Introducing Yellen

Ähnlich wie Introducing Yellen (20)

Mehr von Cristiana Corno

Mehr von Cristiana Corno (12)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Introducing Yellen

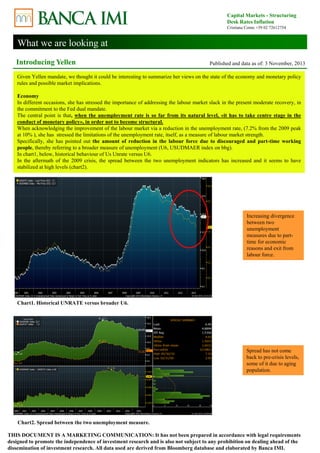

- 1. What we are looking at Capital Markets - Structuring Desk Rates Inflation Cristiana Corno +39 02 72612754 Introducing Yellen Published and data as of: 3 November, 2013 Given Yellen mandate, we thought it could be interesting to summarize her views on the state of the economy and monetary policy rules and possible market implications. Economy In different occasions, she has stressed the importance of addressing the labour market slack in the present moderate recovery, in the commitment to the Fed dual mandate. The central point is that, when the unemployment rate is so far from its natural level, «it has to take centre stage in the conduct of monetary policy», in order not to become structural. When acknowledging the improvement of the labour market via a reduction in the unemployment rate, (7.2% from the 2009 peak at 10% ), she has stressed the limitations of the unemployment rate, itself, as a measure of labour market strength. Specifically, she has pointed out the amount of reduction in the labour force due to discouraged and part-time working people, thereby referring to a broader measure of unemployment (U6, USUDMAER index on bbg). In chart1, below, historical behaviour of Us Unrate versus U6. In the aftermath of the 2009 crisis, the spread between the two unemployment indicators has increased and it seems to have stabilized at high levels (chart2). Chart1. Historical UNRATE versus broader U6. Chart2. Spread between the two unemployment measure. Increasing divergence between two unemployment measures due to part-time for economic reasons and exit from labour force. Spread has not come back to pre-crisis levels, some of it due to aging population. THIS DOCUMENT IS A MARKETING COMMUNICATION: It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. All data used are derived from Bloomberg database and elaborated by Banca IMI.

- 2. What we are looking at Capital Markets - Structuring Desk Rates Inflation Cristiana Corno +39 02 72612754 Introducing Yellen Published and data as of: 3 November, 2013 Yellen stresses the importance of addressing a high prolonged unemployment, which eroding skill (unemployed less employable) rises the natural rate of unemployment, with the final result of shifting the unemployment from cyclical to structural. In the debate over the nature of present high unemployment (cyclical rather than structural), she concludes that the most of it is cyclical and, therefore, can be addressed by stimulating aggregate demand without stoking inflation. When speaking about employment, she gives a broad perspective and stresses the importance to consider a range of labour market indicators in order to judge the strength of the market. We summarize, below, the main indicators she has pointed out in different conferences: 1. U6 unemployment rate for a more complete picture (USUDNMAER index in Bloomberg): to take in account phenomena like part time for economic reasons and labour force exit (chart1 and 2 previous page). 2. Actual unemployment rate less CBO estimate of NAIRU, we have re-built and plotted it in chart3 below. 3. Consumer confidence ration between people who find hard/easy to find job (Concjobh Index less Concjobp Index in Bloomberg, chart3 below) 4. Firms ability to fill jobs from NFIB survey: to identify lack of skill in the market. 5. Quit rate (Joljquit Index): to appreciate strength in labour demand (chart4). 6. Pace of employment growth. 5.00 4.00 3.00 2.00 1.00 0.00 ‐1.00 ‐2.00 50.00 40.00 30.00 20.00 10.00 0.00 ‐10.00 ‐20.00 ‐30.00 ‐40.00 ‐50.00 hard versus easy to find gap unrate‐nairu 01/03/1990 01/10/1990 01/05/1991 01/12/1991 01/07/1992 01/02/1993 01/09/1993 01/04/1994 01/11/1994 01/06/1995 01/01/1996 01/08/1996 01/03/1997 01/10/1997 01/05/1998 01/12/1998 01/07/1999 01/02/2000 01/09/2000 01/04/2001 01/11/2001 01/06/2002 01/01/2003 01/08/2003 01/03/2004 01/10/2004 01/05/2005 01/12/2005 01/07/2006 01/02/2007 01/09/2007 01/04/2008 01/11/2008 01/06/2009 01/01/2010 01/08/2010 01/03/2011 01/10/2011 01/05/2012 01/12/2012 Chart3. Unemployment gap and labour confidence (jobs hard to find – plenty of jobs) 5.00 4.00 3.00 2.00 1.00 0.00 ‐1.00 ‐2.00 gap unrate‐nairu quit rate 01/12/2000 01/04/2001 01/08/2001 01/12/2001 01/04/2002 01/08/2002 01/12/2002 01/04/2003 01/08/2003 01/12/2003 01/04/2004 01/08/2004 01/12/2004 01/04/2005 01/08/2005 01/12/2005 01/04/2006 01/08/2006 01/12/2006 01/04/2007 01/08/2007 01/12/2007 01/04/2008 01/08/2008 01/12/2008 01/04/2009 01/08/2009 01/12/2009 01/04/2010 01/08/2010 01/12/2010 01/04/2011 01/08/2011 01/12/2011 01/04/2012 01/08/2012 01/12/2012 01/04/2013 Chart4. Unemployment gap and quit rate Indicators point in same direction: job market has improved and seems to have stabilized. 3.00 2.50 2.00 1.50 1.00 0.50 0.00 THIS DOCUMENT IS A MARKETING COMMUNICATION: It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. All data used are derived from Bloomberg database and elaborated by Banca IMI.

- 3. What we are looking at Capital Markets - Structuring Desk Rates Inflation Cristiana Corno +39 02 72612754 Introducing Yellen Published and data as of: 3 November, 2013 Yellen also highlights the increase in poverty rate, young unemployment and low real wage growth (delinquency rate still high). As further tailwinds on the economic recovery she indicates the housing sector, pointing at small residential investment contribution to growth (housing starts has rebounded slowly due to massive inventory chart5) in recent recovery and wealth effects. Chart5. Housing units starts (privately owned) and inventory Going forward the housing sector contribution to Us growth could increase, given strong depletion of the housing inventory. Monetary policy rules The Taylor rule in its classical formulation, has been systematically overruled since the early 2000s («Taylor rule and monetary policy: a global great deviation», Bis paper). The attempts to improve the understanding of central banks reaction function have followed 2 directions: 1. lower level of equilibrium real rates 2. larger output gap coefficients (balanced approach or aggressive Taylor rule). The debate has become more important in recent years in order to provide a theoretical guide and justification for quantitative easing and unconventional tools, once the zero lower bound has been reached. In Yellen’s words («Perspectives on monetary policy» June2012, pag13) a balanced Taylor rule, defined as: 2% 0.5*( 2%) 1*( ) t t t t R Y where Yt is the output gap (the model is available also on BBG under Tayl, choosing as model aggressive Taylor rule) is more consistent with Fed commitment to promote the dual mandate of maximum employment and 2% inflation target. Yellen has gone even further showing the superiority in reaching the unemployment goal of the «optimal control policy rule», which minimize a quadratic loss function related to both the inflation and output gap (Woodford, chart6). The quadratic term gives an increasing weight to the output gap when it is wide and vice versa, thereby prescribing lower rates for longer when the output gap is wide and a quicker reaction when the output gap closes (example in chart 7, next page). At present, Fed speeches, the use of unconventional tools like forward guidance and asset purchases seem consistent with an optimal control policy rule regime. In the committee words (Dec12, BoG, press release): ”When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 per cent”, therefore, it seems, we will go back to a balanced Taylor rule, when unemployment rate goes towards 6.5%. Based on Fed forecast, this will happen in 2014 or 2015 at latest. THIS DOCUMENT IS A MARKETING COMMUNICATION: It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. All data used are derived from Bloomberg database and elaborated by Banca IMI.

- 4. What we are looking at Capital Markets - Structuring Desk Rates Inflation Cristiana Corno +39 02 72612754 Introducing Yellen Published and data as of: 3 November, 2013 Different monetary rules and they results: optimal control seems superior in achieving lower and quicker unemployment rate in a context of stable inflation. Chart6. Different monetary policy rule and achievements in term of inflation and unemployment rate Chart7. Monetary rules and rate prescriptions Different monetary rules and different reaction functions: optimal control reacts more when the unemployment gaps closes. In Dec12 statement Fed said it will follow a balanced approach once the 6.5% threeshold is achieved. Summarizing we have a dove Yellen, well focused on unemployment situation and supporter of an “optimal control” policy rule. The risk, I see as we get to know our new Fed chairman (welcome!!!), is some volatility and risk premium getting priced in the market if the economy surprises on the upside. In that case, probably, the 2015 area will suffer more. THIS DOCUMENT IS A MARKETING COMMUNICATION: It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. All data used are derived from Bloomberg database and elaborated by Banca IMI.

- 5. What we are looking at Capital Markets - Structuring Desk Rates Inflation Cristiana Corno +39 02 72612754 Introducing Yellen Published and data as of: 3 November, 2013 “Monetary policy: many targets, many instruments. Where do we stand?”, J.L.Yellen 16th April 2013 “A painfully slow recovery for America’s workers: causes, implications and the Federal reserve’s response”, J.L.Yellen 11th February 2013 “Perspective on monetary policy”, J.L.Yellen 6th June 2012 “Taylor rule and optimal monetary policy”, M. Woodford January 2001 “Methods of policy accommodation at the interest rate lower bound”, M.Woodford 16th September 2012 THIS DOCUMENT IS A MARKETING COMMUNICATION: It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. All data used are derived from Bloomberg database and elaborated by Banca IMI.

- 6. What we are looking at Capital Markets - Structuring Desk Rates Inflation Cristiana Corno +39 02 72612754 Introducing Yellen Published and data as of: 3 November, 2013 Disclaimer This marketing communication has been prepared and is distributed by Banca IMI, a bank belonging to the Intesa Sanpaolo Banking Group which is authorised to carry out investment services in Italy and is regulated by the Bank of Italy and Consob. The information contained in this document: constitutes a marketing communication and, as such, it has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research; may differ from the recommendations prepared by financial analysts of the Servizio Studi e Ricerche of Intesa Sanpaolo and distributed by Banca IMI. The information contained herein does not constitute investment research or an implicit or explicit recommendation or advice in relation to any investment strategy on the financial instruments or on the issuers referred to herein, or a solicitation or invitation, or investment advice, and does not purport to offer legal, tax or any other advice. Neither the Intesa Sanpaolo Banking Group, nor any officer, representative or employee thereof accepts any liability (for neglicence or otherwise) for any direct or consequential losses arising from any use of information including, without limitation, the reliance on any such information contained in this communication. The information and views contained in this communication are based on sources believed to be reliable and in good faith. Accordingly, Banca IMI does not implicitly or explicitly guarantee their accuracy, completeness or correctness. The views, forecasts and estimates contained in this communication reflect the personal view of the author as of the date of its publication. The views may differ from those of others within the Intesa Sanpaolo Banking Goup. All prices and rates included herein are shown for indication only and should not be relied upon to re-evaluate any positions held by any recipient of this document. For specific quotations, please contact your Banca IMI usual contact. There is no guarantee that the future results or any other future events will be consistent with the views, forecasts and estimates contained in this communication. Furthermore, any information included herein is subject to change by the author after the date of its publication without any notice by Banca IMI to the person to whom this communication has been distributed. This document is intended for distribution in Italy and in the Member States of the European Union only to professional clients and eligible counterparties, as defined in the MiFID Directive 2004/39/EC, either as a printed document and/or electronic form. Conflicts of interest. The companies belonging to the Intesa Sanpaolo Group, their officers, employees or representatives and/or their relatives may from time to time have an interest in the financial instruments, including related financial instruments, and in the issuers or transactions referred to in this communication. Such interests may include having long or short positions and, at any time, trading the financial instruments, including related financial instruments, or financial instruments whose value is dependent upon, or is linked to, the financial instruments, issuers, parameters or indices referred to herein. Such interests may also include holding significant shareholdings, holding an office, participating in shareholders’ agreements, providing banking, credit or other financial services to the issuers of the financial instruments referred to herein, including their controlling companies or other companies belonging to the issuer’s group. Banca IMI may act in the capacity of sponsor, specialist, listing partner, market maker, corporate broking and/or liquidity provider or in any other similar capacity with regard to the financial instruments, including related financial instruments, referred to herein. Banca IMI, in the carrying out of trading activities, may have significant directional positions in the financial instruments referred to herein or positions which are contrary to the views expressed herein. In consideration of the above, the companies belonging to the Intesa Sanpaolo Banking Group, its officers, employees or representatives and/or their relatives may have positions in conflict of interest with the positions held by any investor. This communication is for exclusive use by the person to whom has been distributed by Banca IMI and may not be reproduced or redistributed, directly or indirectly, to any other person or published, fully or partially, for any reason whatsoever, without the prior written consent of Banca IMI. The copyright and any other intellectual rights on data, information, opinions and estimates referred to herein belong to the Intesa Sanpaolo Banking Group, unless otherwise stated. Such data, information, opinions and estimates may not be fully or partially distributed or reproduced in any form, and by any means, without the prior written consent of Banca IMI. Any recipient of this communication is required to comply with the above requirements. THIS DOCUMENT IS A MARKETING COMMUNICATION: It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is also not subject to any prohibition on dealing ahead of the dissemination of investment research. All data used are derived from Bloomberg database and elaborated by Banca IMI.