Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (12)

Ähnlich wie Planning Document SAMPLE July 2015

Ähnlich wie Planning Document SAMPLE July 2015 (20)

Planning Document SAMPLE July 2015

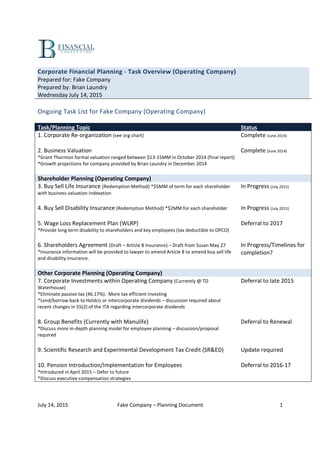

- 1. July 14, 2015 Fake Company – Planning Document 1 Corporate Financial Planning - Task Overview (Operating Company) Prepared for: Fake Company Prepared by: Brian Laundry Wednesday July 14, 2015 Ongoing Task List for Fake Company (Operating Company) Task/Planning Topic Status 1. Corporate Re-organization (see org chart) Complete (June 2014) 2. Business Valuation *Grant Thornton formal valuation ranged between $13-15MM in October 2014 (final report) *Growth projections for company provided by Brian Laundry in December 2014 Complete (June 2014) Shareholder Planning (Operating Company) 3. Buy Sell Life Insurance (Redemption Method) *$5MM of term for each shareholder with business valuation indexation In Progress (July 2015) 4. Buy Sell Disability Insurance (Redemption Method) *$2MM for each shareholder In Progress (July 2015) 5. Wage Loss Replacement Plan (WLRP) *Provide long term disability to shareholders and key employees (tax deductible to OPCO) Deferral to 2017 6. Shareholders Agreement (Draft – Article 8 Insurance) – Draft from Susan May 27 *Insurance information will be provided to lawyer to amend Article 8 to amend buy sell life and disability insurance. In Progress/Timelines for completion? Other Corporate Planning (Operating Company) 7. Corporate Investments within Operating Company (Currently @ TD Waterhouse) *Eliminate passive tax (46.17%). More tax efficient investing *Lend/borrow back to Holdco or intercorporate dividends – discussion required about recent changes in 55(2) of the ITA regarding intercorporate dividends Deferral to late 2015 8. Group Benefits (Currently with Manulife) *Discuss more in-depth planning model for employee planning – discussion/proposal required Deferral to Renewal 9. Scientific Research and Experimental Development Tax Credit (SR&ED) Update required 10. Pension Introduction/Implementation for Employees *Introduced in April 2015 – Defer to future *Discuss executive compensation strategies Deferral to 2016-17

- 2. July 14, 2015 Fake Company – Planning Document 2 Corporate Financial Planning - Task Overview (Individual Holdco’s) A complete list of past, present and future conversations about Shareholder Holdco’s Ongoing Task List for Individual Planning (Holding Company/Family Trust) Task/Planning Topic Status 1. Individual Financial Plan(s) *Each shareholder requires an individual financial plan and individual recommendations To Discuss Investment Planning 2. RRSP & TFSA *Are there currently RRSP or TFSA account? What are the annual contributions? To Discuss 3. Corporate Investments/Savings *Why this is preferred over RRSP/TFSA/RESP *Tax efficiency of growth within the corporation and income in retirement is essential *Introduction of Corporate Class investment strategies *Eligible Dividends education is required (~$48,000/yr tax-free) *Effective management of LIRA account (Amanda) To Discuss 4. Corporate Insured Retirement Program (CIRP) – Universal or Whole Life *An overfunded insurance strategy for the Holdco *Provides tax-free growth and income *Valuable at a young age and very low risk In Progress 5. Corporate Estate Bond (CEB) – Universal or Whole Life To Discuss *An insurance strategy for the Holdco that transitions corporate accumulation to the children tax-free (saves 35-40% taxable dividend at death) *Can be used as an investment strategy if parents are insurable and shareholder of a corporation (CDA strategy) – See attached document Insurance Planning 6. Term Life Insurance (Includes spouse) *What happens at death? Is the proper coverage inforce? Review current plans *Ensure ownership, payor and beneficiary is structured to the Holdco properly. Why? To Discuss 7. Disability Insurance (Includes spouse) *What happens if somebody can’t work? Educate about group benefits. What happens to the plan? To Discuss 8. Critical Illness Insurance (includes spouse) **What happens if somebody can’t work? What impact does this have on the financial plan? Can it be used as a cash-like investment strategy inside of the Holdco? To Discuss 9. Long Term Care Insurance (includes spouse) *What happens if somebody requires care? This is an important discussion about the value of ‘locking in’ while young. Education required To Discuss

- 3. July 14, 2015 Fake Company – Planning Document 3 10. Insuring Children *Why this has been a popular strategy for generations *Talk about the different options *Education is required To Discuss 11. Personal Health Savings Plan (PHSP) *Make personal/family medical expenses (orthodontics, drugs, etc.) corporate deductions To Discuss Tax Planning 12. Salary or Dividends *Education about dividend sprinkling from Holdco or Family Trust To Discuss 13. Funding Children’s Education from Holdco or Trust *Education about dividend sprinkling from Holdco or Family Trust To Discuss 14. Corporately /Owned Paid Insurance *How to have personal/family coverage paid by the corporation To Discuss Family Planning 15. Multiple Wills and Powers of Attorney *Personal and corporate wills are required (for Holdco) To Discuss 16. Personal Snapshots Document *Provides a 1-stop place for all relevant information if an emergency occurs To Discuss 17. Mortgage/Banking Efficiency *Introduction of Manulife One Estate Planning 18. Corporate Estate Bond (CEB) – Universal or Whole Life *Same as #5 above To Discuss 19. Estate Planning for Parents *Who is the executor? Who will pay for costs for care? Considerations for pro-active estate planning for parents To Discuss