3. HUB

�e

P I VOT P OINT

M A G A Z I N E

Razor Sharp JANUARY/FEBRUARY 2010

A lmost 15 years ago, I started asking the best and

brightest in marketing questions about the future of

22

this business, first on Reveries.com and now in the Hub.

That probably translates into thousands of questions

asked. But, in fact, I’ve really only posed variations of

one, pivotal probe: Where’s it all headed? COVER STORY

Some of the answers have been more memorable

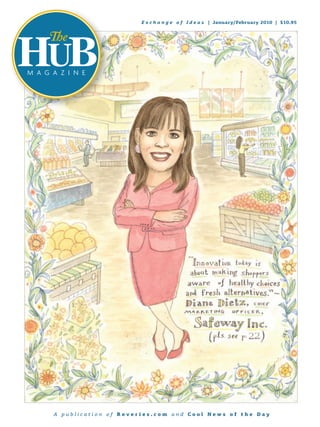

than others, obviously. If there’s one I recall best, it was Positively Safeway

the response from Geoffrey Safeway chief marketing officer Diane Dietz gets

Remembering Frost, a former chief marketing inspiration from innovation. An exclusive Q&A

interview by Tim Manners.

the late, great officer of Motorola, during late

Geoffrey Frost. summer, 2005.

It’s memorable partly

8

because, tragically, Geoffrey passed away within weeks

of our conversation. But it’s more because he was so

damn clear about what he saw coming.

He was remarkably prescient when he referred to ROUNDTABLE

his product as “the device formerly known as the cell

phone.” He also suggested we should think about our Better Things

business as “the industry formerly known as advertising.” Innovation just isn’t what it used to be. A discussion

But my favorite part of the interview was when featuring Claudia Poccia of Avon mark, Jevin

Eagle of Staples, Randy Carlson of Diageo, and

Geoffrey talked about the famous William Gibson

Jim Porçarelli of Active International.

quote: “The future has already arrived; it’s just not

evenly distributed.”

As Geoffrey explained, “What he’s saying is that

16

there are people of the future, already here, walking

among us. If you can figure out who they are and

co-create with them, you’re actually doing a rather

amazing job of not only anticipating, but also shaping W H I T E PA P E R

where the world can go.”

It’s a new year, and a new decade. What’s new, for Map the Gap

you, in the industry formerly known as advertising? Winning at retail requires innovation across

Where’s it all headed? bundles of brand benefits. By Vinit Doshi.

Tim Manners

tim@hubmagazine.com

4. Editor-in-Chief

Tim Manners

Senior Editors

Peter F. Eder

Jane Harris

ALSO

Managing Publisher

Joseph McMahon

5

Art Director COOL NEWS

Julie Manners

Consumer Intelligence, Twittovation, Keds Collective, Little Nike,

Design Concept Here/Nau/NYC and Full Yield.

Alexander Isley Inc.

Illustrator

John S. Dykes 12 R ESEARCH R EPORT

The New Super | What makes a supermarket innovative? An executive

summary of a Reveries.com survey.

Circulation Director

Bertha Rosenberg

Brain Trust

Active International

Arc Worldwide

14 S U RV E Y A NA LY S I S

Supermarket Savvy | Innovative supermarkets tap into emotional and

functional desires. By Randi Moore.

Catapult Marketing

EURO RSCG Discovery

20

Henry Rak Consulting Partners E SSAY

Hoyt & Company

Insight Out of Chaos Popping for Shoppers | The “pop-up” trend is driving retail innovation.

Landor Associates By Beth Ann Kaminkow.

McGuinn.com

Marketing Drive

Mars Advertising

Triad Digital Media

TracyLocke

WomanWise

27 W H I T E PA P E R

The Shopper Aperture | Let’s put a new lens on the future of shopper

marketing. By Anne Howe.

Hub Club

PMA

RPM Connect

Upshot

30 W H I T E PA P E R

The “We” Decade | Creating community and higher purpose will elevate

our brands in the 2010s. By Dori Molitor.

The Hub

David X. Manners Co.

107 Post Road East

Westport, CT 06880

34 W H I T E PA P E R

Smooth Selling | Integrated Selling drives bottom-line sales and better

brand performance. By Paul Kramer.

203-227-7060 ext. 227

hub@hubmagazine.com

n Brought to you by the editors of Reveries.

com and Cool News of the Day, The Hub

magazine is dedicated to exploring insights,

36 R ESEARCH R EPORT

The Socialized Shopper | New research shows how social media is changing

shopping behavior. By Mark Renshaw.

ideas and innovation as the ultimate drivers

of business success.

n Published bi-monthly since July

2004, The Hub’s circulation is exclusive

to Reveries’ proprietary database of

40 E SSAY

Beauty in Virtue | Luxury brands can make us look (and feel) truly good.

By Cable Daniel-Dreyfus.

approximately 3,500 senior-level, client-

side executives in Fortune 1000 marketing

42

departments and major ad agencies.

COOL BOOKS

n Advertising: For more information on

The Hub’s collaborative sponsorship and

Makers, Think Twice and Start-Up Nation.

advertising opportunities, please contact

Joseph McMahon (joseph@hubmagazine.

com) or 845-238-3516.

5. COOL NE W S

Consumer Intelligence Keds Collective

The defense industry has a long history of feeding innovations to consumer markets — the Keds is engaged in a “wholesale

internet, satellite navigation systems and the computer itself originated as military projects, business-model change” in which its

for instance. consumers not only design footwear,

but can also sell it. “Marketing has

Now, the consumer-electronics industry is returning the favor. For example, the U.S. Air

evolved into a conversation with

Force just ordered some 2,200 Sony PlayStation 3 videogame consoles, which it will use as

the consumers,” says Kristin Kohler

“building-blocks of a supercomputer.”

Burrows, president of Keds.

Meanwhile, in Iraq and Afghanistan, soldiers “are using Apple iPods and iPhones to run

To keep that conversation going,

translation software and calculate bullet trajectories. Xbox videogame controllers have

Keds has launched a site, called Keds

been modified to control reconnaissance robots and drone aircraft.”

Collective, where consumers can

This is occurring because the military spends “only a small fraction” of its $1.5 trillion choose from a palette or upload their

budget on electronics, leaving it outspent on R&D by the consumer-electronics industry. own design elements.

Electronics firms are also able to “move much faster than the slow, If Keds likes a design, it makes a deal

multi-year grind of military procurement programs ... And with the consumer, who receives

the emergence of open-standards and open-source a 10 percent cut on any sales. The

software make it easier to re-purpose off-the-shelf shoes can either be ordered online by

technologies or combine them in novel ways.” consumers or stocked by retailers for

Leaving such innovations to the private sector sale in stores.

meanwhile enables the military to “focus their

So far, this hasn’t exactly made

spending on the development of new technologies,

anyone rich, but that’s not the point.

rather than reinventing the wheel.”

“I’m totally thrilled,” says Jeriana

[S o u r c e : The Economist, 12/12/09] San Juan, who has “sold six pairs of

Keds with her designs.”

For Keds, its all about turning

Twittovation “custom sneakers into an advertising

juggernaut when the designers ...

proudly holler about them from the

“Twitter’s smart enough, or lucky

rooftops of the internet.” Jeriana,

enough, to say, ‘Gee, let’s not try to

for instance, “has posted her Keds

compete with our users ... let’s outsource

designs on Facebook and is adding a

design to them,’” says Eric von Hippel,

Keds link to her website.”

author of Democratizing Innovation.

Similarly, Nike not only publishes

Twitter CEO Evan Williams agrees:

a “gallery” of consumer designs

“Most companies or services on the web

on NikeiD, but also provides

start with wrong assumptions about what they

“convenient icons to click to ‘share’

are and what they’re for,” he says. “Twitter struck an interesting balance of flexibility

them on Twitter, Facebook and

and malleability that allowed users to invent uses for it that weren’t anticipated.”

MySpace.”

Among other things, Twitter users invented the idea of putting the @ symbol before their

Champion, meanwhile, asked its

user names (e.g., @cool_news). They also picked up the idea of using the # symbol to

“consumers to design hoodies and

categorize topics — another innovation Twitter initially resisted.

submit them for votes.” Darren Paul

The # idea came from open-source advocate, @chrismessina, who says Twitter thought of Night Agency, the social-media

the # concept was too nerdy for mass appeal. Well, now Twitter “hyperlinks the hash consultancy that helped create the

tags so readers can click and see all the other posts on a topic.” Keds Collective, comments: “People

feel much more connected to the

Evan Williams says Twitter’s plan is to keep following its followers. “You get a bunch

brand because they’re part of the

of users interacting and it’s hard to predict what they’re going to do,” he says. “We say,

advertising, in reality.”

‘Why are people using this and how could we make that better?’”

[S o u r c e : Christina Binkley,

[Source: Claire Cain Miller, The New York Times, 10/26/09]

The Wall Street Journal, 12/10/09]

Cool News of the Day, a daily e-mail newsletter of marketing insights, ideas and inspiration, is edited by TIM MANNERS. For a free subscription, visit www.reveries.com

6. COOL NE W S W S

COOL NE

Little Nike

Mark Parker thinks acting smaller will help Nike grow bigger. It’s not as

though Nike, now 37 years old, is having any problems growing; its “stock is

up 50 percent over the past five years while the S&P 500 is down 7.7 percent.”

According to Interbrand, Nike’s brand value “has jumped from 31st to 26th”

in the four years since Mark assumed leadership at the company. Despite

this, Mark sees the Nike brand as something of a liability, particularly among

younger consumers in action-sports categories.

Jeanne Jackson, president of Nike’s retail division agrees: “Kids think it’s cool

not to have a big, hairy name over the store,” she says. And so Nike’s latest

retail venture not only doesn’t carry the Nike name, it has no name at all.

Instead, the action-sports store, dedicated to skateboarding and snowboarding,

simply displays the logos of “its three key brands at the entrance: Hurley,

Converse and 6.0 (an action sports line that does have a Swoosh on it).”

“The hardest thing for a company to do is to change when it doesn’t seem

like change is necessary,” says Mark. One thing that hasn’t changed is Nike’s

connections with celebrity athletes.

“We always want to be connected with the world’s top athletes,” says

Mark, himself a distance runner. “Our relationships with athletes fuel the

innovations,” he says.

And, of course, there’s China, where Nike invested some $1.5 billion in 2009,

and may invest even more in the year ahead. “No matter how much you’re

investing there, it’s not enough,” says Mark.

[S o u r c e : Bruce Horovitz, USA Today, 12/7/09]

Here/Nau/NYC Full Yield

Jean-Pierre Veillet is creating a pop-up boutique “using materials ... “We need to put food back in the heart of health care,” says Zoe

almost entirely rooted in New York City’s waste stream.” Finch Totten, chief executive of Full Yield. “It’s the cheapest way

to deal with health and the simplest, and definitely the most

This includes “fallen tree limbs found on the street, timber and

pleasurable,” she adds.

metal pipes from derelict Brooklyn factories and piles of discarded

cardboard boxes — so that when the store closes, at least the Zoe’s focus is on the way people eat in the workplace. Her solution

garbage won’t be new.” is a branded “12-month nutritional program” that’s designed to

“take the guesswork out of what constitutes a healthy diet” and

The boutique is called Here/Nau/NYC and naturally “will carry

help reduce health-care costs.

products from several environmentally minded companies,

including shoes from Timberland and Toms, organic dresses and The Full Yield menu features “fresh items made with natural, whole

sweaters from Stewart + Brown, bags made of recycled truck tarps ingredients” and “will be sold in corporate cafeterias and in the

from Freitag and the sleek, athletic designs of Nau.” prepared-foods section of local supermarkets” in the Boston area.

John Hancock, the insurance company, is among Zoe’s first customers,

And so Jean-Pierre is busy fashioning displays out of cardboard

with some 300 of its employees adopting Full Yield next year.

and trying to turn bubble-wrap into lampshades. He’s got clothes

“hanging from a rolling rack made of old pipes, timber and Meals are priced at $6 to $7 a meal, and employees will receive

mismatched wagon wheels.” His main worry, he says, “is that it “$100 worth of coupons that can be used in John Hancock’s

could end up looking clunky and cheap.” cafeteria and at 18 local Roche Brothers grocery stores.”

Gordon Seabury, who owns Nau, refers to Jean-Pierre’s approach as Full Yield plans to take various biometric measurements of

“dumpster-diving” but is “confident that the resulting decor would Hancock participants throughout the year, and then “analyze the

ultimately reflect the company’s approach to considered design.” data against insurance claims to gauge improvements in health.”

[S o u r c e : Eric Wilson, The New York Times, 11/5/09] [S o u r c e : Melanie Warner, The New York Times, 11/29/09]

Cool News of the Day, a daily e-mail newsletter of marketing insights, ideas and inspiration, is edited by TIM MANNERS. For a free subscription, visit www.reveries.com

7. 95

| $10.

20 09

M ay /June

de a s |

of I

ange

Exch

HUB

�e

HUB �e Excha

nge o

f Ide

as | Se pt

em ber/

Oc tobe

r 2009

| $10

N E

A Z I

M A G M A G A

Z I N E

HUB

Exchange o

�e

f I d e a s | July

/Aug ust 2009

| $10.95

M A G A Z I N E

THE HUB

12

TOP

Shoppeng

r

Marketi ce

Excellen

D ay

the

s of

New

Cool

and

s .com

ev erie

of R

ion

bl icat

A pu

A pub

li catio

n of R

ever ies.c

om an

d Coo

l News

of th

e Da y

A publicati

on of Reve

ries.com a

nd Cool Ne

ws of the Day

Get the Hub!

Keep up with marketing’s

boldest and brightest.

Subscribe today.

It’s easy. Just visit:

http://hubmagazine.com/subscribe

8. ROUNDTABL E

Innovation just isn’t what it used to be.

Better Things

What are you trying up. Every single Staples store in always been that it’s not innovative

the United States has easy-tech if it’s a solution in search of a

to accomplish with technicians who can provide a free problem. The goal of innovation is

innovation? tune-up of your PC. really to ferret out a keen insight,

to deliver something that is

Claudia Poccia: With new products, A product innovation is our Mailmate

needed, wanted or lacking.

we constantly challenge ourselves Shredder. Our customers were

to look outside of the cosmetic opening their mail in their kitchens The word “innovation” clearly is

industry into the broader landscape but their shredders were in their overused. So many people use it

of change. We try to leverage offices. So, we made a shredder as “give me something different

inspiration across the convergence that’s just perfect for the kitchen. to save me for six months” or

of media, technology and other There are many more examples of “something different for the sake of

A product forms. solving problems for customers being different,” so that I can say

R oundtAble We also engage with our customer

embedded in our culture. that I have fostered innovation.

F eAtuRing or representative because, for the

Claudia Poccia

most part, she is one and the same. We try to leverage inspiration across

That’s why bringing our product

Avon mark

to her, where she lives, and where the convergence of media, technology

Jevin Eagle she’s most receptive to receiving and other product forms.

Staples our message, is so important.

C L Au DI A P o C C I A

Randy Carlson We bring direct selling into the

Diageo digital age through social media and

other nascent technologies. We’re Randy Carlson: The goal of But innovation really is about

Jim Porçarelli going to her in a place where she’s innovation should be to bring new paying attention and looking for

Active International open to receiving our message and ways to delight consumers that are sometimes the simplest things that

engaging with our brand. relevant for them. For Diageo, and solve the issue in a way that no one

a lot of mature businesses, maybe else has done before.

Jevin Eagle: At Staples, the goal

that’s more “renovation” than

of innovation is to provide customers

with value, product or an experience

“innovation,” but it’s really about How do you create a

breathing new life into our brands.

that solves a problem or helps make culture of innovation?

their lives easier. That’s the link Some people look at innovation

between the customer, the innova- as inventing the un-invented. But Poccia: Talent is the key ingredient

tion, Staples and its shareholders. our obligation, as companies, is to to creating a culture of innovation.

deliver business results. Inventing If you have a team of forward-

For example, we offer free delivery

the un-invented is a nice, long- thinking individuals who can

that, in almost all cases, arrives

term aspiration, but innovation had look at things with a fresh, new

the next day. That would be an

better create revenues and profits. lens, it creates an environment

experience innovation. A service

that fosters innovation throughout

innovation is our free PC tune- Jim Porçarelli: My mantra has

8 THE HUB JANUARY/FEBRUARY 2010

9. the company. High emotional Proven results are what get the organization

intelligence is also paramount.

gelled around innovation.

You need people with great,

cutting-edge ideas, but equally R A N Dy C A R L S oN

important is a team that has the

ability to initiate and execute

You also need an element of In fact, she demands it. She inspires

those ideas in a strategic manner.

pragmatism. Rather than just us. She co-creates with us because

It’s important to build a team of

thinking about an idea, you need we’re both a brand and a channel.

creative thinkers who reach for

to go and do it and focus on results. So, whenever we ideate a product,

the stars, but also keep one foot

Otherwise, your innovation is not our favorite expression here is,

firmly planted on the ground so

going to have a long life. Proven “let’s take it to the Girl Lab.” That

that everything aligns with the

results are what get the organization means going to our consumer and

business objective.

gelled around innovation. our representative and engaging

Eagle: We not only have a market her in the ideation and decision-

Porçarelli: You have to give people

research department at Staples, but making process up front.

honest-to-goodness permission

also groups of people who are not

to fail. If people aren’t afraid of This co-creation partnership

exactly in “market research,” but

making mistakes, they are going enables us to bring forth products

are constantly doing, testing and

to come up with more and more that allow for our consumers’ and

trying new things. For example, we

creative and interesting ideas. representatives’ self-expression. So,

have what we call our “usability

she’s got a more immersive brand

group.” Their job is to observe how You need people who say things that

experience at a higher level of

customers use things, either online you hadn’t thought of yourself. If

emotional engagement with us.

or in person. people are just repeating everything

I already know, they are not right Eagle: I have a strong point-of-view

At any given time, we have

for my team. Leaders need to allow on this. We used to run a contest

dozens of tests going on of either

themselves to be challenged by at Staples called Invention Quest,

new products, new ways to display

their teams. where we asked customers and

products or to develop offers. The

employees to create new product

culture when we go out into the Managers have a responsibility

ideas. I’m so glad we did this — I

field is the culture of listening, whenever someone comes to them

was one of the judges — but I don’t

whereas in traditional retail it’s with an idea — no matter how big

think it was the most effective way

a culture of telling. We have or how small — to sit with them

to get insights because customers

tremendous respect and awe for and help tweak the idea until it

are not product developers.

our store managers, and when works. It’s imperative to continue

they give us ideas we take the conversation because it can A better way to get customers

voracious notes. foster other ideas in other arenas engaged is for us to listen to them.

that will solve bigger problems. How do you live your life? How do

Carlson: Innovation really starts

you work? How do you play? How

at the top. There may be a heretic

who’s trying to push innovations How should consumers do you use products today? That’s

where the much bigger ideas come

uphill, but heretics have a very be involved in the from. We listen, observe, and take

low probability of getting anything

innovation process? it from there.

done without leadership support.

Poccia: Bonding over beauty and Carlson: For us, the involvement

Second, you need people who

fashion fosters community and is three-tier, including consumers,

believe in possibilities and are

brings young women together. customers and distributors. If you

willing to beat their heads against

Because direct selling is inherently have a brokered sales organization,

the wall. With innovation, you are

participatory, it’s really natural for you should include them, as well.

going to hear “no” a lot. You have

us to engage with our customers It’s critical.

to have people who are willing to

work in that kind of environment and representatives to create a co- I personally find that the trade —

and aren’t brought down by it. branding experience. including distributors and sales

JANUARY/FEBRUARY 2010 THE HUB 9

10. organizations — has a kind of

What is the most taking any money you make and

“fingertip feel” for what’s right or applying it to lower prices, and

wrong with your product offerings. innovative idea then focusing everything in your

It’s a great thing to get that kind of you’ve seen? culture on leveraging scale to get

feedback sooner than later. lower prices. I think Starbucks was

Poccia: True innovators create the first to not require a signature

On the other hand, your customers, products or services that customers at the register when you use your

your consumers or the trade are not can personalize to meet their credit card. That was brilliant.

going to come to you with the next, needs. I find TiVo fascinating. For

big breakthrough idea. That’s just decades, all of us were happy to I do think that Staples’ ink

not going to happen. So, hopefully view pre-determined and recycling program is breathtaking.

that’s where the innovator’s thinking scheduled programming and then We give three dollars back for

comes in. It’s really up to the out of the blue comes TiVo. every cartridge you bring back to

innovator to identify the problem recycle. This meets the customer’s

being solved, and how to solve it. Now we have the power to need for doing something good for

decide when we want to watch the environment, while also giving

Porçarelli: First of all, their this programming. This TV-by- them money for it. We’re going to

involvement is about the due appointment culture has created a recycle more than 50 million ink

diligence of the marketer. seismic shift in consumers. jet cartridges this year.

There’s so much information

and data available to us today, Something that we’ve done at mark Carlson: My favorite innovator

but you need to understand the is a franchise called Hook Ups. Hook right now is Tesla Motors.

attitudes, concerns and buying Ups are dual ended, customizable What Tesla has done is make a

behaviors that are intrinsic to your makeup products for eyes, lips completely electric car using cell-

consumers. So, don’t be afraid to and cheeks. We provide a wide phone battery technology. It’s the

preview ideas with your audience. assortment of textures, tones and same kind of battery you have in

product forms. The consumer can your Blackberry, just stacked up.

Procter & Gamble had a wonderful put together over 2,000 combinations

formula where every single brand and make it their own. That has They make a sports car that’s

super light, looks a lot like the

Lotus, and can go from zero to 60

mph in 3.9 seconds, with a 250-

The culture when we go out into the field is mile range. It costs $100,000, but

the culture of listening, whereas in traditional it is twice as efficient as a Prius.

They are also making a 4-door

retail it’s a culture of telling. sedan for 2011 delivery.

J E v I N E AgL E What Tesla has done is turn the

efficiency issue on its ear. They’re

taking this notion of a car you

had to set aside a little bit of its really gotten the industry’s attention want to be in and the right thing

budget every year for testing — even because it puts creativity in the to be doing for the world, and

though they knew that 80 percent of hands of the consumer. put them together. And they’ve

the results may not give them an actually executed it. It’s brilliant!

Eagle: With Amazon, one innovation

insight worth acting on. But the

was giving away shipping and Porçarelli: There’s a product

other 20 percent was invaluable. As

tying that to extremely low prices. called New Energy Solutions — it’s

a result, they had the greatest insight

Most business people would have this pad that you can put on your

into the package-goods consumer.

said “no” to that. Another innovation dresser, and it charges all of your

While consumers generally don’t was buying back used books and electronic devices without having

really know what they do want, then reselling them, which to plug them in. That really adds

they pretty much know what they GameStop does with games. to your quality-of-life because

don’t want. By knowing what to they’ve solved an everyday

At Walmart, the innovation

eliminate, it’s often a lot easier to problem.

was Sam Walton’s concept of

figure out what to offer.

10 THE HUB JANUARY/FEBRUARY 2010

11. T HOUGHT L E ADER S

In a very different realm, there’s for us — if not at the moment,

a technology in radiology called then over the life of customer.

micro-bubbles that are injected

There are plenty of things we do

into the bloodstream to take better

where we’re not maximizing profits

“pictures” of a specific organ. -

on a transaction basis, but we are

The idea is that if you inject the

on a customer basis. That’s the key. CLAUDIA POCCIA is global

bubbles with chemotherapy, you

president of mark, Avon’s trend

might be able to treat cancer more For example, during back-to-

beauty and fashion boutique brand,

effectively. It’s still being tested, school season, we offered free

where she is reinventing the direct

but could have a huge impact. backpacks — 100 percent back in selling business model for the

Staples rewards on any backpack. next generation by tapping into

How do you Why did we do that? Not because

the world of social media.

measure the return we thought we were going to

JEVIN EAGLE is executive vice

make money that day. The

on innovation? president of merchandising and

innovation is in how we create marketing for Staples. Jevin was

Poccia: R.O.I., at mark, means value for customers. It all comes a principal architect in developing

“Return On Innovation.” It’s a back to our customer economics. the Staples brand promise to make

buying office products easy.

metric for success that has never Carlson: At Diageo, we have

been more critical to the bottom business performance metrics

line. We measure it through our that are attributed to innovation. RANDY CARLSON is global

most important asset, and that’s the In fact, in our annual report, innovation director for Diageo.

mark representative. That’s because half of our growth last year Previously with Ralston Purina,

not only is she our consumer, but came from innovation. It’s a real Tropicana and PepsiCo, Randy has

she’s also our retailer. a diverse perspective on common

number. There’s real bookkeeping

success factors for innovations

So, for us, the innovation imperative and accounting associated with

across marketplaces.

is to deliver an entrepreneurial innovation that’s done both in

platform to this representative aggregate and individually.

JIM PORÇARELLI is chief strategy

officer at Active International,

a global marketing and business

If people aren’t afraid of making mistakes, solutions firm. He can be reached at

jporcare@activeinternational.com.

they are going to come up with more and more

creative and interesting ideas.

J I M P oRç A R E L L I

that reinvents direct selling for In a broader context, your return on innovation and reinventing

them, and allows them to play on innovation requires short-term themselves. Is there a return on

in a digital space through their metrics in addition to the long- innovation? You bet your life

social networking platform. As term investments, and you have to there is, because innovation is the

her engagement and connection roll them up together. If you start lifeblood of every business.

through these platforms rises, so doing activity-based costing on each

There’s a huge return because

does her sales productivity. So, it individual innovation, there will

innovation fosters innovation.

generates organic growth. be more things you kill than you

When someone comes up with an

launch. When that happens, then

Eagle: Innovation is all about the innovative idea it becomes almost

somebody else invents the future.

notion that if we do things for our addictive because as you begin to

customers that meet their needs, Porçarelli: Without innovation, have success with innovation you

they will reward us. Our underlying a company will begin to die. want to have more success, and more

assumption is that doing good Great companies falter because innovations follow. Innovation is its

things for customers is also good they didn’t put enough emphasis own impetus for greater innovation. n

JANUARY/FEBRUARY 2010 THE HUB 11

12. RE SE ARCH REP ORT

What makes a supermarket innovative?

Where would shoppers most like to see

innovation? Which supermarkets are

most innovative?

The New

How innovative is the supermarket you shop most often?

Conventional wisdom has it that many — if

not most — supermarkets haven’t changed much Somewhat 55.0%

for about 50 years. True, there’s more in the way

of prepared meals. And the number of products Very 21.7%

offered has grown. Store brands may have

improved in quality, too. Not at all 17.1%

But has the basic construct of aisles of

ingredients really budged all that much? We put Extremely 6.3%

this question to Reveries.com readers and the

answer came back somewhere down the middle:

A majority of 55 percent said the supermarket

In which ways is your supermarket innovative?

they shop most frequently is only “somewhat”

(pick as many as apply)

innovative.

As one respondent put it: “It seems grocery

Product Selection 54.3%

retailers perceive innovation as being creative with

inventory and don’t give enough consideration to Prepared Foods 46.6%

environment and space.”

The only area a majority deemed innovative Private Labels 38.9%

was “product selection” (54 percent), followed

by “prepared foods” (47 percent) and “private Store Layout 31.7%

labels” (39 percent).

However, in nine out of ten areas, survey Checkout 31.7%

more in the way of innovation: product selection;

respondents suggested they would like to see

Customer Service 29.8%

format/store layout; checkout; customer service;

promotions; new services; online tools; and

Promotions 17.3%

displays. The only area shoppers indicated they

Displays 17.3%

are satisfied is “private labels.”

Online shopping tools appear to be especially

Online Tools 13.5%

ripe for innovation, as an overwhelming majority

of respondents (74 percent) said they do not use New Services 12.0%

retailer websites. An even larger majority of 80

percent said they do not use “any other online

planning tools for grocery shopping.”

Some remarked that they weren’t aware that How important is a supermarket’s prices versus its

such tools exist, while others confirmed that this innovations to you?

may well be the case: “I wish I could get ads via

my phone and use mobile coupons. I would also Somewhat 39.6%

love to be able to upload coupons to my loyalty

Very 37.1%

card and not have to deal with paper coupons.”

Frustrations were many, with crowded

Extremely 18.3%

stores and slow checkouts being the most

frequently cited complaints. Others aimed their Not at all 5.0%

ire at stores that rearrange aisles for no apparent

reason: “Shuffling where categories are found,

12 THE HUB JANUARY/FEBRUARY 2010

THE HUB JANUARY/FEBRUARY 2010

13. Super

Where would you most like to see innovation at your

supermarket? (pick as many as apply)

sometimes just from the right to the left are

annoyances, not innovations.”

Self-checkouts also received mixed reviews.

others said they only benefit retailers. One

Some said they liked the convenience while

respondent had a similar complaint about store

formats: “I’m tired of grocery stores being laid out

to help the grocer and the vendors.”

Product Selection 51.5% Overall, there was no shortage of suggestions

on where supermarkets could improve in ways

Store Layout 50.6% both big and small:

Checkout 41.6% “ Why can’t grocery bakeries make good,

healthful, preservative-free breads?”

Prepared Foods 35.5%

“ This business of forcing me up and down aisles

and across the store to find the things I need is

Customer Service 33.3%

tiresome and makes me tired and angry.”

Promotions 31.6% “ I wish I didn’t have to go to three different stores

in order to supply our home.”

New Services 31.6%

“ So many carts with wheels that don’t work right!”

Online Tools 29.9% Despite such grievances, a perhaps surprisingly

large majority of 70 percent said they generally

Displays 25.5% enjoy grocery shopping, especially discovering

new items. And even though most do not consider

Private Labels 15.2%

their supermarkets to be innovative, a plurality

of 43 percent felt their grocers were up-to-date.

But as one respondent observed, the

In general, do you enjoy grocery shopping? innovations of the future may well be rooted

in the past: “I shop at a small, family-owned

Yes 70.3% supermarket that prides itself on personal service.

Another hinted that maybe it isn’t up to

Its innovation is old-fashioned customer service.”

No 29.7%

supermarkets to be innovative at all: “Since I

purchase groceries from three stores and one farmer’s

market each month, maybe I’m the innovator.”

Overall, which era does the supermarket at which you

And this comment may provide the greatest

usually shop most resemble?

insight of all: “Here’s the deal, when money is

2000s 42.7% in short supply and entertainment dollars are

small or non-existent, grocery shopping becomes

1990s 21.4% entertainment … When money is flowing and we

can eat out more often and I’m cooking less, then

1980s 11.5% grocery shopping goes back to being a chore.”

The supermarket picked at the number-one

2010s & beyond 10.7% most innovative? Whole Foods, followed by Trader

Joe’s and Wegmans. Curiously, nowhere near as

the supermarkets they shop most frequently. n

1970s 7.7% many respondents selected these same stores as

1950s 3.8%

Complete survey results can be found at:

1960s 2.1% www.hubmagazine.com/survey/supermarkets

JANUARY/FEBRUARY 2010 THE HUB 13

JANUARY/FEBRUARY 2010 THE HUB

14. SURVE Y ANALY S I S

Supermarket

Savvy

T

he latest Reveries.com survey asked a I m pl I c at I o n s : Improve navigation — beginning

savvy shopping crowd whether today’s in the parking lot and continuing through the store

supermarkets are innovative. What we and checkout. Create a shopper-centric store layout

heard back was how shoppers want us to with intuitive assortments and adjacencies in an

innovate today’s shopping experience. uncluttered environment.

What do they want? Well, as one respondent Fix the broken carts. Smooth the checkout

succinctly said, “I want it all.” And today, to get it all, experience — if not with technology with good, old

shoppers go everywhere. fashioned, helpful, happy, engaged employees.

When asked, our shoppers reported that they Relevant Rewards. This means delivering more

patronize an average of three different supermarkets, than price incentives in a format that is relevant to

making one or two trips per week. But that’s not today’s shoppers. It is about innovating both in terms

the whole story. When we dig into where they are of content and delivery. It is about informing and

shopping, we unearth an eclectic, channel-blurring motivating shoppers along their paths-to-purchase.

I m pl I c at I o n s : Provide relevant, convenient

rewards and tools that are customized to shoppers’

Innovative supermarkets tap into needs and localized to their markets. It is about

consistently reinforcing that membership in retail

emotional and functional desires. reward programs has privileges.

To do this, retailers need to build in additional

value and convenience. To help communicate, augment

list that includes traditional supermarkets, specialty outbound retail email campaigns with innovative

stores, club, mass and drug. product information, planning tools, recipes and a link to

What drives them? From a functional perspective, coupons. Consider extending to mobile applications.

shoppers want: From an emotional perspective, shoppers connect

Product selection. Provide affordable, one-stop with retailers and brands that:

shopping without sacrifices. This starts with providing Understand them by having the right assortment,

quality produce — including both local and organic right offers and then something extra. Strive to

choices. It extends to value-added product options, understand the cooking-shopping-nurturing connection

with shoppers looking for specialty, gourmet and that drives both the function and emotion around

prepared-foods offerings. many shopping trips. Don’t underestimate shopper

I m pl I c at I o n s : Provide an array of quality products commitment to more sustainable and green solutions,

that meet their needs and their wants to build baskets. even in a down economy.

Be consistent in your product offerings and eliminate I m pl I c at I o n s : Understand your shoppers and

the critical out-of-stocks that drive shoppers out of their preferences. Become a resource for more than

your store. merchandise, and become a partner that helps provide

Convenience. It’s not all about location, location, innovative solutions that entertain and nurture their

location. It is about time: Get shoppers in, get them families.

out — fast, with everything on their list. Provide them Engage them personally with communications

with helpful and happy personal service. that inform and educate — before and during the

14 THE HUB JANUARY/FEBRUARY 2010

15. shopping trip. Shoppers are looking for information

that provides ideas and inspiration. Ask them their

opinions! Truly Super Markets

I m pl I c at I o n s : Understand your shoppers’ paths-

to-purchase and engage them along the way. Don’t In survey respondents’ own words, here’s what

undervalue the role of personal service. Create simple, makes supermarkets super:

relevant planning tools that integrate with how Whole Foods: Product Selection; Convenience

they plan today. Engage them visually in-store with (Store Layout and Service); Engagement

attractive displays and signage — remembering that (Communications and Causes).

value is much more than price.

Entertain them. Take the mundane out of the Trader Joes: Product Selection; Convenience

shopping experience — make shopping an event. You (Checkout and Service); Entertainment

have a live audience. Make it fun for them and for (Sampling and Surprises).

family members in tow. Wegmans: Shopping Experience; Product

I m pl I c at I o n s : Add music, demonstrations, Selection; Convenience (Layout and Signage);

sampling, wine tastings, product specialists and good, Engagement (Communications, Causes, Recipes

old-fashioned customer service to add a personal and Service); Entertainment (Sampling).

element. Introduce them to new products and invite

Tesco Fresh & Easy: Product Selection;

them to explore.

Convenience (Checkout Options and Layout);

Success requires solutions that drive the mutual

Engagement (Social Media).

goals of both the retailer and the manufacturer. This

means listening to the shopper and delivering against

multiple shopper needs.

Manufacturers need to find connecting points

between their brands and the retailer. If your Build programs to deliver against shoppers’

product benefit is about convenience or speed, partner multiple needs. For example, when we create

with retailers to deliver convenient solutions and programs that inform and educate (e.g., recipes, meal

services. For example: This checkout or checker plans, activities, in home entertaining tips, healthy

brought to you by Brand X. living guides, etc.) We show that we understand that

If your product makes folks smile, sponsor an our shoppers are looking for ideas and solutions.

employee recognition program that delivers improved When these ideas include complimentary (and

customer service that engages shoppers and improves potentially private-label) products, we are building

convenience. If your brand entertains, find a way to baskets in a way that leverages the retailer’s product

bring that into store in a way that builds on both the selection. When we overlay incentives in a tips booklet,

brand and retail platform. or through shopper targeting, we are providing relevant

Listen to the voice of the shopper and understand rewards.

the impact of changing shopper behavior. Irrespective By collaborating with retailers to develop in

of any shortcomings, 70 percent of our survey store “solution centers” with attractive fixtures and

respondents say they like shopping and discovering informative signage, we maximize convenience while

new things. engaging shoppers. Add an educated, animated

So, create events that encourage shoppers to go demonstrator, and we entertain the shopper, as well.

on a “treasure hunt.” Purposefully drive consumers When we bring these elements together, we are on the

throughout the store to fulfill their missions to discover road to true super marketing. n

something new — it both engages and entertains.

Shoppers are pre-planning as never before, but

according to this survey 60 percent of them are RANDI MOORE is vice-president

not using retail circulars and 74 percent are not and account director with

leveraging retail websites. Marketing Drive. She leads the

Engage consumers where they plan by integrating agency’s shopper-marketing

into relevant online activities like popular cooking practice. Randi can be reached at

randi.moore@marketingdrive.com.

(Epicurious, Food Network) and couponing sites to

build on planning behavior.

JANUARY/FEBRUARY 2010 THE HUB 15

16. WHI T E PAPER

Map the

Gap By Vinit DoShi

h e n r y r a k c o n S u l t i n g Pa r t n e r S

T

he real story behind the growth of store brands is less often about price gaps

than the shrinking value gap between national and store brands. This narrowing

value gap is real, and marketers anticipating an economic recovery to lift their

sales in a “rising tide” effect are bound to be disappointed.

Consumers are fundamentally changing their consumer behavior that holds as true today as ever:

attitudes towards more conscientious consumption National brand manufacturers need to innovate across

on matters of environment, health and value. The the entire value bundle that comprises the brand —

heightened importance of value-for-money is leading positioning, product, packaging, pricing, etc. — in

them to rethink their attitudes and behaviors order to deliver relevant benefits to the right targets in

concerning the value of branded products and the a superior way and align with consumers’ needs and

price premiums they are willing to pay for frequently desired benefits.

consumed necessities. Mature markets demonstrate these principles

of consumer preferences all the time. In the last

five years, for example, marketers have successfully

Winning at retail tapped into consumers’ health and wellness needs

with a variety of innovatively-positioned and

requires innovation precisely-targeted beverage products that promise

to deliver specific functional benefits such as quick

across bundles and lasting energy, meal replacement, or vegetable

nutrition — often to selected targets during specific

of brand benefits. parts of the day.

These consumer preferences lead to consistent

behaviors that collectively create markets organized

The trend is further reinforced by better consumer around bundles of relevant benefits. This results in

perception of store brands, backed by improvements product groupings that deliver primarily against one

in the quality and range of these products (according of those benefit areas and compete closely with other

to a recent study, 70 percent of millennial women products in the same group.

perceive the quality of store brands to be “excellent”). Regardless of the market, price-value invariably

This portends the potential continuation of store manifests itself somewhere in the structure, although

brand sales and share growth, and a steep challenge the role of price-value relative to the role of brand

to the growth of branded products. varies considerably across different markets. The

To look for answers, we turn to a key principle of price-value dynamic depends on the importance and

16 THE HUB JANUARY/FEBRUARY 2010

17. types of consumer needs, nature of product usage, A market map provides a precise understanding

role of trust and imagery in the category, the presence of how consumers are behaving, for what reasons,

and strength of dominant brands and levels of and with what trade-offs. It is a proven platform for

marketing and innovation. evaluating and predicting the impact of different

Ultimately, however, the price-value relationship marketing strategies. As such, it is an essential

depends on how well marketers have managed to define foundation for managing a brand to a better outcome.

and deliver relevant benefits. In some cases, marketers Unfortunately, many organizations do not fully

have created benefit-structured markets based on years appreciate or understand the power of a correct,

of advertising, innovation, and effective positioning precise, and behaviorally-based understanding of

against relevant functional and emotional benefits. their market. Too often, a brand’s competitive frame is

In these situations, brands or brand groups play a based on category definitions, consumers’ opinions, or

significant higher-order role in which they effectively a less-than-rigorous evaluation of consumer behavior.

stand for and own key benefits to the exclusion of As a result, the hierarchy of benefits may be

other brands. Store brands may play a smaller role — out of order, or the spheres of influence through

existing but interacting in an undifferentiated way — which consumers make choices and trade-offs may

or in a limited way that does not preclude the growth of be misrepresented. Managing a brand with a flawed

branded players. The example of soy milk demonstrates understanding of the market is bound to inhibit or

how branded products used precise positioning, even derail growth.

marketing, and innovation to establish and own a value- So, the first challenge is to understand how the

added position as a tasty, healthy, nutritious, dairy- market is organized, what your brands really compete

free alternative to conventional milk, leaving behind with, and on what basis. After developing a precise,

the commodity dynamics of the dairy milk category. behavior-based understanding of the market, you

At the other extreme, markets that lack meaningful are ready to understand how to guide your brands

differentiation of relevant benefits to consumers, to more advantageous positions of sustainable and

significant marketing, and effective innovation, profitable growth. You can also identify and prioritize

predictably degrade into attribute-driven markets in the most viable innovation opportunities among many

which form, flavor, price-tiers, or easily replicable seemingly reasonable options.

factors become the primary organizing principle of

the market (for example, conventional dairy milk). Finding growth opportunities

In such cases, national brands often play a The logical first place to look for growth is among

weakened role in the structure, and store brands do your established brands in their current, competitive

well as consumers reward the brands that deliver the frames-of-reference. In some cases, a brand may have

only differentiating benefit of relevance — price-value. significant upside potential in terms of consumer

Most markets fall into a continuum between these behavior that can be accessed. Well-differentiated

extremes in which many national brands are fighting a brands often find that their strong loyalty puts them

losing battle, struggling to stem losses or eke out small in the enviable position of being able to bring in new

gains. Some are dealing with the added burden of budget buyers or increase usage simply by increasing media

cuts and cost reductions that affect product quality. spending.

All the while, store brands are racking up growth. More often than not, however, brands have not

Fortunately, the picture is not all gloom-and-doom fully optimized their potential from a positioning

for marketers of national brands. If they are committed standpoint. Many brands may be competing in an

to understanding and leveraging the principles of undifferentiated way with other brands, representing

consumer preferences and benefit-structured markets, the same benefits to the same consumers in more or

they have good reason for optimism. In a previous less similar ways.

issue of The Hub, my colleague Eric Greifenberger Insights based on the market map can provide

introduced the concept of a market map (see: Map the a breakthrough understanding of how to deliver the

Market, July/August, 2009). functional and emotional benefits of a market in a

JANUARY/FEBRUARY 2010 THE HUB 17

18. Concentric spheres of competitive interaction illustrate

the range of competition from close-in to furthest-out

Fruit-flavor All flavors of Desserts/ Desserts in other

Ice Cream Ice Cream Sweet treats situations

S o u r c e : Henry Rak Consulting Partners

more compelling, effective or different way. Or, it differentiated itself as a high-quality, more effective

can show how to expand the benefit appeal to more laundry care product. Chanel owns a certain mystique

consumers, or across more occasions. in perfumes and luxury accessories. Victoria’s Secret

In recent years, some brands have leveraged and Starbucks have come to stand for distinct benefits

consumer trends by emphasizing the simplicity and to selected consumers that allow each to transcend the

freshness of their ingredients to consumers who are products themselves to own an experience.

most motivated by health and wellness. One particular An integrated view of the market with consumer

brand of lunch and dinner products has done well by needs and usage behaviors can also help identify

elevating its appeal from basic product attributes to a emerging opportunities to meet unaddressed or

sharper connection with old-world Italian sentiments. unknown needs. The bigger and further out the idea,

In other cases, positioning a brand to bridge multiple the more likely it is to require significant product

benefits has proven effective in improving relative innovation. The process begins by examining the

value perceptions versus store brands. different needs that people experience across occasions

A market map represents “concentric spheres and their satisfaction with the current solutions, all of

of consumer interaction,” in which each sphere which helps identify problem areas and gaps.

represents gradually broader sets of needs being met For example, the basic “hydration” benefit of

by a wider array of competitors (see chart). In this beverages has been redefined and segmented to meet

sense, a brand can look for growth by extending its different nuances of the basic need, including portable

positioning to stand for something bigger and broader. hydration for everyone/everywhere/anytime (bottled

Taken to its logical conclusion, such brands can water), hydration with replenishment (isotonics),

begin to own a “benefit platform” to a sufficiently hydration with nutritional benefits (vitamin and

distinct degree that they command greater loyalty and enhanced waters), and so forth.

source volume from brands in other segments of a Exploiting the sufficiently large and viable white-

market. This is known as “partitioning the market.” spaces can sometimes provide more significant and

A brand that has partitioned the market is sustainable growth opportunities than battling for

characterized not only by strong market-share, but share within crowded areas of the market. Effective

also by strong loyalty and a price premium. Tide has innovation requires brands to extend their positioning

18 THE HUB JANUARY/FEBRUARY 2010

19. platforms and equities to reach further out (or develop competitive frame includes Subway and Quiznos,

new brands), secure larger marketing budgets, and then product testing on that brand should include

manage to a longer-term investment horizon. the sandwich chains’ products. Following that,

An effective portfolio plan that balances risks simulating the trade-offs between different levels of

and rewards by optimizing the shorter-term and product positioning, quality, pricing, and margins can

longer-term opportunities of established brands and provide management a quantitative range of options to

innovation simultaneously, can enjoy significant factually determine what size business is most viable

competitive advantages and drive sustainable growth. from a total perspective of volume, revenue and margin.

Drive ROI at the Expense of Growth. Optimizing

Av o i d Q u i c k F i x e s the marketing mix is a powerful way to understand the

Having examined some examples of how to drivers of the business, to quantify what works and

use the market map to one’s advantage, it is equally what doesn’t, and to evaluate the mix of tactics and

important to note some principles of what not to do, campaigns. However, when used in an isolated fashion

or what to avoid as singular quick-fixes. to reduce costs or improve ROI without effective growth

Fight Fire with Fire. The temptation to fight strategies to guide the decisions, such “optimization”

store brand growth by “right-pricing” the brand, or does nothing more than facilitate a more efficient

increasing price promotion, may yield short-term deterioration of the brand (using proven tactics to do it!).

relief. However, unless the brand aspires to become Of course, continuous improvement in execution

just like a store brand, this is unlikely to drive is important, but effective marketers seldom use the

profitable, long-term growth. It may even focus the efficiencies only to cut costs, reduce risk, or make

brand on fighting an unwinnable battle in the wrong minor corrections to the mix. Effective marketers

part of the competitive frame. use it primarily to fund their most promising top-line

That said, pricing and promotion clearly play growth strategies — and to do it smarter along the way.

critical roles in the overall marketing mix. Our

•••

recommendation is to simulate and test pricing and

promotion strategies. This should be done as part of a Marketers need a precise, fact-based understanding

comprehensive growth strategy in which these levers of the market to determine the linkage between consumer

play a precise supporting role to the main storyline of needs, benefits and behaviors. Knowing the basis of

a consumer benefit-centered strategy. competition is critical, not only against store brands,

Undermine Product Effectiveness. Every but against the entire relevant frame of reference.

promising strategy is ultimately predicated on the A market map is a dynamic reflection of the ever-

assumption that the product must deliver on consumer changing ways that consumers prioritize needs and

expectations. Reducing costs to improve margin can organize behavior. With this knowledge, the marketer

be risky. For some brands, years of small, seemingly will understand the benefits a brand should reasonably

innocuous cost reductions affecting ingredients, strive to own through positioning and innovation.

packaging, amount, and quality have compounded Markets can be changed by the actions or inactions

themselves into noticeable changes in overall product of marketers — to the benefit of some brands and the

appeal. It is clear that the growth of store brands detriment of others. Only the fittest will survive. n

in several categories is due to years of gradual cost

reductions by the branded products.

Without meaningful product differentiation VINIT DOSHI is a principal with Henry

versus store brands, justifying a price advantage Rak Consulting Partners, a growth-

becomes difficult for a branded product. For this strategy consulting firm. Vinit can be

reason, we recommend testing for relative product reached at vdoshi@hrcpinsights.com

preference in the context of a brand’s full competitive or (203) 540-5524. To learn more about

HRCP, visit www.hrcpinsights.com.

frame-of-reference.

For example, if a frozen sandwich brand’s true

JANUARY/FEBRUARY 2010 THE HUB 19