1. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 1

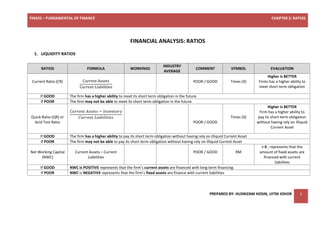

FINANCIAL ANALYSIS: RATIOS

1. LIQUIDITY RATIOS

RATIOS FORMULA WORKINGS

INDUSTRY

AVERAGE

COMMENT SYMBOL EVALUATION

Current Ratio (CR) Current Assets

Current Liabilities

POOR / GOOD Times (X)

Higher is BETTER

Firms has a higher ability to

meet short term obligation

If GOOD The firm has a higher ability to meet its short term obligation in the future

If POOR The firm may not be able to meet its short term obligation in the future

Quick Ratio (QR) or

Acid Test Ratio

𝐶𝑢𝑟𝑟𝑒𝑛𝑡 𝐴𝑠𝑠𝑒𝑡𝑠 − 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦

𝐶𝑢𝑟𝑟𝑒𝑛𝑡 𝐿𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑖𝑒𝑠

POOR / GOOD

Times (X)

Higher is BETTER

Firm has a higher ability to

pay its short term obligation

without having rely on illiquid

Current Asset

If GOOD The firm has a higher ability to pay its short term obligation without having rely on illiquid Current Asset

If POOR The firm may not be able to pay its short term obligation without having rely on illiquid Current Asset

Net Working Capital

(NWC)

Current Assets – Current

Liabilities

POOR / GOOD RM

< 0 , represents that the

amount of fixed assets are

financed with current

liabilities

If GOOD NWC is POSITIVE represents that the firm’s current assets are financed with long term financing.

If POOR NWC is NEGATIVE represents that the firm’s fixed assets are finance with current liabilities

2. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 2

2. ACTIVITY / ASSET MANAGEMENT RATIOS

RATIOS FORMULA WORKINGS

INDUSTRY

AVERAGE

COMMENT SYMBOL EVALUATION

Inventory Turnover

(ITO) or

Inventory Utilization

Ratio

𝐶𝑂𝐺𝑆 @ 𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠

𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦

POOR / GOOD Times (X)

Higher is BETTER

Firms is effectively using its

inventory to generate sales

If GOOD The firms is effectively using its inventory to generate sales

If POOR The firms is ineffectively using its inventory to generate sales and holding excess and unproductive stocks.

Average Collection

Period (ACP)

𝐴𝑐𝑐𝑜𝑢𝑛𝑡 𝑅𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠

𝑥 360

POOR / GOOD Days

Lower is BETTER

Firm is good in managing its

credit sales & more cash in

hands

If GOOD (Shorter) The firm is good in managing its credit sales & more cash in hands

If POOR (Longer) The firm is not good in managing its credit sales & less cash in hands

Fixed Assets

Turnover (FATO)

Net Sales

Net Fixed Assets

POOR / GOOD Times (X)

Higher is BETTER

Firm is able to utilize its fixed

assets and good in managing

its assets.

If GOOD The firm is able to utilize its fixed assets and good in managing its assets and more revenues generated per Ringgit of the investment.

If POOR The firm unable to utilize its fixed assets and not good in managing its assets and less revenue generated per Ringgit of the investment.

Total Assets

Turnover (TATO)

Net Sales

Total Assets

POOR / GOOD Times (X)

Higher is BETTER

Firm is able to utilize its

overall assets and good in

managing its assets

If GOOD The firm is able to utilize its overall assets and good in managing its assets.

If POOR The firm is unable to utilize its overall assets and not good in managing its assets.

3. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 3

3. LEVERAGE / DEBT RATIOS

RATIOS FORMULA WORKINGS

INDUSTRY

AVERAGE

COMMENT SYMBOL EVALUATION

Debt Ratio

(DR)

Long Term Debt

Total Assets

x 100

POOR / GOOD %

Lower is BETTER

Firms is good in managing

its debt & low financial risk

If GOOD (Lower) The firm is good in managing its debt & low financial risk.

If POOR (Higher) The firms is not good in managing its debt & indicates higher financial risk

Debt to Equity Ratio

(DER)

𝐿𝑜𝑛𝑔 𝑇𝑒𝑟𝑚 𝐷𝑒𝑏𝑡

𝑇𝑜𝑡𝑎𝑙 𝐸𝑞𝑢𝑖𝑡𝑖𝑒𝑠 POOR / GOOD Times (X)

< 1, represents that more

funds provided by owners

If MORE THAN 1 It indicates that the creditor provided more funds compared to owners.

If LESS THAN 1 It indicates that more funds provided by owners compared to creditors.

Times Interest

Earned (TIE)

EBIT

Interest

POOR / GOOD Times (X)

Higher is BETTER

Firm is good in meeting

their interest payment

obligation

If GOOD The firm is good in meeting their interest payments obligation and higher capability and lower risks of default.

If POOR The firm is not good in meeting their interest payments obligation and lower capability and higher risks of default.

4. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 4

4. PROFITABILITY RATIOS

RATIOS FORMULA WORKINGS

INDUSTRY

AVERAGE

COMMENT SYMBOL EVALUATION

Gross Profit Margin

(GPM)

Gross Profit

Net Sales

x 100

POOR / GOOD %

Higher is BETTER

Firm is able to control COGS

relative to its sales revenue

If GOOD The firm is able to control COGS relative to its sales revenue.

If POOR The firm unable to control COGS relative to its sales revenue.

Operating Profit

Margin (OPM)

𝐸𝐵𝐼𝑇

𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠

𝑥 100

POOR / GOOD %

Higher is BETTER

Firm is able to provide more

return because the firm is

productively managing its

assets.

If GOOD (Shorter) The firm is able to provide more return because the firm is productively manage its assets

If POOR (Longer) The firm unable to provide more return because the firm is unproductively manage its assets

Net Profit Margin

(NPM)

Earning After Taxes

Net Sales

x 100

POOR / GOOD %

Higher is BETTER

Firm has a better growth

prospect & able to generate

net earnings to shareholders

(earn more ringgit).

If GOOD The firm has a better growth prospect & able to generate net earnings to shareholders (earn more ringgit)

If POOR The firm don’t have a better growth prospect & unable to generate net earnings to shareholders.

5. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 5

Return On Assets

(ROA)

Earnings After Taxes

Total Assets

𝑥 100

POOR / GOOD

%

Higher is BETTER

Firm is able to control costs

in its operation (assets are

productive) and provide

more return.

If GOOD The firm is able to control costs in its operation (assets are productive) and provide more return.

If POOR The firm is unable to control costs in its operation (assets are productive) and didn’t provide more return.

Return On Equity

(ROE)

Earnings After Taxes

Total Equity

x 100

POOR / GOOD %

Higher is BETTER

Firm is able to maximize the

owner’s wealth

If GOOD The firm is able to maximize the owner’s wealth and give higher return for the owners of the firm.

If POOR The firm is unable to maximize the owner’s wealth and didn’t give higher return for the owners of the firm.

6. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 6

5. MARKET RATIOS

RATIOS FORMULA WORKINGS

INDUSTRY

AVERAGE

COMMENT SYMBOL EVALUATION

Earnings per Share

(EPS)

Net Income − 𝑃𝑆 𝐷𝑖𝑣

No. of Shares POOR / GOOD RM

Higher is BETTER

Firms is profitable enough

to pay out more money to

its shareholders.

If GOOD The firm is profitable enough to pay out more money to its shareholders.

If POOR The firm is unprofitable enough to pay out more money to its shareholders.

Dividend per Share

(DPS)

Total Dividend

No. of Shares

POOR / GOOD RM

Higher is BETTER

Shows the great way for a

company to signal strong

performance and great

portion of company’s

earnings to its

shareholders.

If GOOD The firm is able to give signal strong performance and great portion of the company’s earnings that is paid out to each shareholders

If POOR The firm unable to give signal strong performance and lower portion of the company’s earnings that is paid to each shareholders.

Dividend Payout

Ratio

(DPR)

Dividend per Share (DPS)

Earnings per Share (EPS)

x 100

Dividend paid

Net Income

x 100

POOR / GOOD

%

Higher is BETTER

How much money a

company is returning to

shareholders versus how

much it is keeping on hand

to reinvest in growth, pay

off debt, or add to cash

reserves (retained

earnings).

7. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 7

If GOOD The firm is able to pay out all their earnings to shareholders as dividend, while only small pay out portion is retained by the business.

If POOR The firm is unable to pay out all their earnings to shareholders as dividend, but portion remaining retained by the business.

Dividend Yield

(DY)

Dividend per Share (DPS)

Market Price per Share (MPS)

𝑥 100

POOR / GOOD %

Higher is BETTER

Measures the quantum of

cash dividends paid out to

shareholders relative to

the market value per share

If GOOD The firm is able to pays a substantial share of its profits in the form of dividends.

If POOR The firm is unable to pays a substantial share of its profits in the form of dividends..

Price Earnings

Ratio

(PER)

Market Price per Share (MPS)

Earnings per Share (EPS)

POOR / GOOD times

Higher is BETTER

Firm is able to maximize

the owner’s wealth

If GOOD The investors are anticipating higher growth in the future.

If POOR The investors are not anticipating higher growth in the future.

8. FIN242 – FUNDAMENTAL OF FINANCE CHAPTER 2: RATIOS

PREPARED BY: HUSNIZAM HOSIN, UITM JOHOR 8

ITEMS IN CURRENT ASSETS ITEMS IN

FIXED ASSETS

ITEMS IN

CURRENT LIABILITIES

ITEMS IN LONG TERM

LIABILITIES ITEMS IN EQUITIES

1. Cash

2. Cheque or Bank Draft or

other Negotiable

Instruments

3. Deposits

4. Marketable Securities

5. Account Receivable

6. Inventories

7. Prepaid Expenses

8. Prepayment

1. Land

2. Building

3. Motor vehicles

4. Equipment

5. Plant

6. Pattern

7. Goodwill

1. Account payable

2. Tax payable

3. Tax accrual

4. Accrued Expenses

5. Short Term Debt

6. Accounts Liabilities

7. Notes payable

8. Short term borrowing

1. Long term debt

2. Mortgage

3. Bonds

4. Leases

5. Debentures

1. Retained Earnings

2. Paid in capital

3. Common shares

4. Preferred Shares

5. Shareholders’ Equity