Call Girls Kengeri Satellite Town Just Call 👗 7737669865 👗 Top Class Call Gir...

Voip Map V10 Small

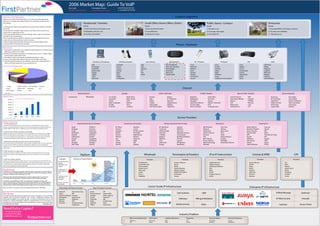

1. 2006 Market Map: Guide To VoIP

FirstPartner

FirstPartner www.firstpartner.net

Kurt Lyall Christopher Owen

t. +44 (0)870 874 8700

klyall@firstpartner.net cowen@firstpartner.net

Customer Segments

Welcome to VoIP Market Map

Welcome to the 2006 Q3 VoIP Market Map. It is an overview of the global VoIP

industry on one page and includes key facts and underlying trends that drive

Residential / Families Small Office Home Office (SoHo) Public Space / Campus Enterprise

this industry.

Needs: Needs: Needs: Needs:

1) Starting at the top, the map identifies four main customer segments and their

1) Out of the box and simple to use 1) Ease of administration 1) Simple to use 1) Interoperability with legacy systems

key needs.

2) It presents the complete range of phones and devices that customers can

2) Reliability and low cost 2) Cost efffective 2) Coverage and range 2) Security and reliability

choose from to adopt VoIP service.

3) Number portability 3) Network of users 3) Fast hand-off 3) Operating cost

3) The map identifies different channels through which customers buy phones

and VoIP services and solutions.

4) The map distinguishes between traditional service providers like fixed line

carriers and new Internet telecom service providers.

5) It lists leading players that offer infrastructure and technologies to both

service providers and enterprise customers.

Phones / Hardware

Market Facts

1. Subscribers to retail VoIP service worldwide rose by 83% from 10.3 million at the

beginning of 2005 to 18.7 million.

2. Number of subscribers paying for PC to phone service is over 4.7 million. Skype

has the largest market share at 45%.

3. Time Warner Cable in USA signed up 900,000 subscribers in 2005.

4. France is the largest VoIP market in Europe with 2.8 million subscribers.

5. The VoIP market for hardware and software is led by Cisco, which had 24.3 %

Soft Phone / IM Software USB Phone Vendors Smart Phones Hybrid Devices Wi - Fi Phones IP Phones ATA Other

share in the Q106. Avaya came in second with 23.4 %.

AOL Actiontec Dell AOL Portable IM Cisco Cisco Cisco VoIP Voice

US Pure-Play VOIP Market Share BT Voyager Atcom Eten Nintendo GameBoy Motorola Alcatel Digium BillKey

20%

CallComm Canyon Flipstart Nokia NGage NetGear Siemens D-Link Edgecore

Express Talk Clarisys HP Sony Mylo Sony Cidico Grandstream Logitech

1%

1%

Google Ipevo HTC Xbox Live! Symbol Mitel Linksys Motorola

2%

2%

Jabber Onyx iMate Hitachi Cable Toshiba SIPPhone Vegastream Netgear

2%

Lipz4 Philips UT Starcom Snom Zoom Polycom

Microsoft US Robotics Vocera Unidata Comms Systems Zyxel Sierra Wireless

55%

3%

4%

5%

5%

Vonage Verizon VoiceWing AT&T CallVantage SunRocket

Channel

Lingo NetZero Voice Broadvoice AOL

8x8 (Packet8) Earthlink Other

Mobile Operators Retailers Online / Mail Order IT VARS / Resellers Telecoms VARS / Resellers System Integrators

Source: Telephia

Market Drivers 3 (Hutchison) KPN Mobile Circuit City Radio Shack Amazon Firebox Brightstar Smith Micro Central Telecom ABP Accenture Atos Origin

VoIP Penetration into Broadband Market (US) CompUSA Micro Centre Dabs PC Telephone Brightpoint Tech Data Data Sharp Telecom Scantalk BT Consulting CommVerge

30.00%

Dixons CDW Kelkoo Play.com Dangaard Synnex Equant VoIPBitz CapGemini Satyam Computers

25.00%

Mesh Computers Walmart Firebox Shopping.com Data Sharp Telecom Global IT Networks L3N Vonexus Fujitsu Services Tata Consultancy

PC Mall Tesco VoIP Supply Talkip4u El Corte Ingles GTSI Netservices Lirex HP Services Orca Group

20.00%

PC World Carrefour VoIP Phone Depot TigerDirect Micro Computer Computacenter SouthernCom STS Logica CMG Quentris

15.00%

10.00%

5.00%

0.00%

2004 2005 2006 2007 2008

Service Providers

Source: The Yankee Group, 2004

Market Commentary

Internet Telecom Service Providers Internet Service Providers Wireless Internet Service Providers Alternatives Fixed Carriers

1. Service provider race

Low barriers to participation allow new entrants to launch services. Business models vary from

Skype CallServe BT Yahoo AvantGo BT OpenZone Azulstar 360 Networks Tech Terra British Telecom Comcast

provider to provider. Ultimately survivors must have strong funding, good marketing strategy and

willing to fight for market share as traditional carriers are also launching competing services. Vongage iConnect Easynet Covad Concourse Mobiboo Albacom TelCove Deutsche Telekom Hanara

Lingo InPhoneix Kingston ISP Net Canada Liberty Europe Clearwire CableVision Wave Crest France Telecom MCI

2. Infrastructure vendors have been over funded

SunRocket Telappliant Mistral FranceNet Swisscom Speednet Services Gamma Telecom Thus Telecom Italia Sprint

Multiple specialist vendors, funded by VCs, have launched platforms and infrastructure to support

Packet8 Earthlink Plusnet Road Runner T-Mobile Commspeed Inmarsat Viatel KPN Time Warner Cable

VoIP services. Ultimately too many suppliers are currently in the market and very few will be able

CallVantage PlusNet Nildram NetZero Wayport NextPhase Wireless iTXC Modus Telecom SingTel NTT

carve out a sustainable niche in the long-term. As technologies standardise, vendors will need to

consolidate technologies to deliver better value propositions to carriers and enterprises. Google Symphony Sky Virgin.net Fiberlink FreshTel KMC Telecom Inclarity Telefonica Verizon

Yahoo VoiceWing Tiscali Pipex iPass Avantel Primus Telecom NewEdge Telia Sonera VSNL

3. Mainstream networking vendors are the main beneficiaries

NetLogic Voiceglo Orange AOL GoRemote ERF Wireless Rapid Technology Alternative Telecom Telenor Qwest

Driven by the need for more bandwidth in order to deliver acceptable quality of service, mainstream

VoIP Street Go2Call Demon Datanet Boingo Net2Phone VoiceNet Cable & Wireless PCCW

network vendors are likely to benefit from VoIP helping to triggering customer up-grade and

replacement cycles. ISPs will also benefit as businesses and consumers look to increase their network

requirements.

4. VoIP over Wi-Fi is in hype mode

Unclear service delivery models, lack of hotspots and poor handset performance means that the

Wholesale Termination & Preselect IP to IP Interconnect Centrex & VPBX CPE

Platform

combination of these two technologies will take longer than expected to become a meaningful

service.

Example: Evolution of Skype Platform

5. VoIP over cellular networks Providers Providers

Providers Providers Providers

Solutions are being developed to enable customers to access buddy lists and make VoIM calls from

A viral network for

BT Wholesale Annecto Telecom Cable & Wireless Aastra Telecom C4L

their cellphone without incurring any long distance or per minute mobile charges in some cases. Tier

sharing

2 mobile operators are taking a lead through marketing arrangements with ITSPs to differentiate

Castle Networks Bactel Global Crossing Alcatel Belco

information and

their consumer propositions and boost data ARPU.

First European BandX InfinRoute Networks Avaya Digium

content

Global Source Cable & Wireless ITXC Nortel Speed Touch

FirstPartnergrowing strategic marketing and research agency. No other agency Largest peer to

Infocomm Global Crossing iBasis Polycom Nortel

peer system ever

FirstPartner is a fast

Level3 Global Termination Level3 Samsung Tandberg

built

has the strength of understanding of technology and its impact on changing customer

Primus ICX Europe Progress Telecom Siemens Toshiba

behaviour, combined with marketing know-how.

Teleglobe Verizon Qwest Sylantro Unisys

Presence on over

We take on big marketing challenges for our clients, helping them to, launch new

100 million

technology based propositions and better optimise their marketing strategies.

desktops

FirstPartner was established in 2001 and is growing on average more than 50%

year-on-year. We have a unique and successful culture, thanks to our multi-disciplined Draws 1% of www

teams covering marketing, creative, finance and research. Our track record speaks for bandwidth

itself and spans working with global brands through to the most innovative start-ups.

Carrier Grade IP Infrastructure Enterprise IP Infrastructure

Why not contact us to get your team up to speed and to build on the debate. Technology and Platform Providers Skype Developer Ecosystem

Global IP Voice Processing Voxeo IVR

Unified Message Gateways

Soft Switches CRM

Disclaimer Voxeo IVR Pamela Systems Inbound PBX

Ubiquity Software Content Voxpilot Video response

The map includes information compiled from various reputable sources and other

Mindspeed Opensource Scodor Voicemail

methods like structured interviews and surveys, conference material and

Gateways Billing & Mediation IP PBXs/Centrex Firewalls

information available in the public domain. As data and information sources are Sylantra Platforms 4Teambiz PIM

outside our control, FirstPartner makes no representation as to its accuracy or Netwise PIM VApps Conferencing

completeness. All responsibility for any interpretation or actions based on this map

Video

ShoreTel Antispam & App. VideoIM

Media Services

lies solely with the reader. Copyright 2007

Other Access Points

Switches

Voice portal

integration Tellme

Need Extra Copies?

t. +44 (0) 870 874 8700

f. +44 (0) 870 874 9888 Industry Enablers

e. hello@firstpartner.net

firstpartner.net Web Service Market Place VoIP Experts Leading Publications Regulators Standard Bodies Research & Advisory

Strike Iron Pulver.com VNU FCC H.323 (ITU) Gartner

SAP Patton VON Ofcom SIP (IETF) FirstPartner