Malad Call Girl in Services 9892124323 | ₹,4500 With Room Free Delivery

The World Economy On a Bumpy Road to Recovery

1. Page 1 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

April 12, 2014

-8

-6

-4

-2

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013e 2014f 2015f

China

Sub-Saharan Africa

GCC

EmergingMarkets

Japan

UnitedStates

Euro Area

The World Economy On a Bumpy Road to Recovery

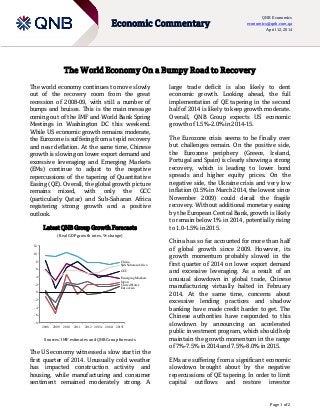

The world economy continues to move slowly

out of the recovery room from the great

recession of 2008-09, with still a number of

bumps and bruises. This is the main message

coming out of the IMF and World Bank Spring

Meetings in Washington DC this weekend.

While US economic growth remains moderate,

the Eurozone is suffering from a tepid recovery

and near deflation. At the same time, Chinese

growth is slowing on lower export demand and

excessive leveraging and Emerging Markets

(EMs) continue to adjust to the negative

repercussions of the tapering of Quantitative

Easing (QE). Overall, the global growth picture

remains mixed, with only the GCC

(particularly Qatar) and Sub-Saharan Africa

registering strong growth and a positive

outlook.

Latest QNB Group Growth Forecasts

(Real GDP growth rates, % change)

Sources: IMF estimates and QNB Group forecasts

The US economy witnessed a slow start in the

first quarter of 2014. Unusually cold weather

has impacted construction activity and

housing, while manufacturing and consumer

sentiment remained moderately strong. A

large trade deficit is also likely to dent

economic growth. Looking ahead, the full

implementation of QE tapering in the second

half of 2014 is likely to keep growth moderate.

Overall, QNB Group expects US economic

growth of 1.5%-2.0% in 2014-15.

The Eurozone crisis seems to be finally over

but challenges remain. On the positive side,

the Eurozone periphery (Greece, Ireland,

Portugal and Spain) is clearly showing a strong

recovery, which is leading to lower bond

spreads and higher equity prices. On the

negative side, the Ukraine crisis and very low

inflation (0.5% in March 2014, the lowest since

November 2009) could derail the fragile

recovery. Without additional monetary easing

by the European Central Bank, growth is likely

to remain below 1% in 2014, potentially rising

to 1.0-1.5% in 2015.

China has so far accounted for more than half

of global growth since 2009. However, its

growth momentum probably slowed in the

first quarter of 2014 on lower export demand

and excessive leveraging. As a result of an

unusual slowdown in global trade, Chinese

manufacturing virtually halted in February

2014. At the same time, concerns about

excessive lending practices and shadow

banking have made credit harder to get. The

Chinese authorities have responded to this

slowdown by announcing an accelerated

public investment program, which should help

maintain the growth momentum in the range

of 7%-7.5% in 2014 and 7.5%-8.0% in 2015.

EMs are suffering from a significant economic

slowdown brought about by the negative

repercussions of QE tapering. In order to limit

capital outflows and restore investor

2. Page 2 of 2

Economic Commentary

QNB Economics

economics@qnb.com.qa

April 12, 2014

confidence, most EMs have had to tighten

macroeconomic policies. As a result, growth

has significantly weakened in countries like

Brazil, India, Russia, South Africa, Thailand,

Turkey and, to a lesser extent, Indonesia. This

is likely to continue as QE tapering is fully

implemented and long-term interest rates in

advanced economies start rising. EM growth

will therefore slow to an average 4.0%-4.5% in

2014 and 3.5%-4.0% in 2015.

Against this global trend, growth in the GCC

region continues to strengthen. A strong push

for diversification through strong

infrastructure spending is pushing up non-

hydrocarbon growth. Qatar is leading the

region with projected double digit growth in

the non-hydrocarbon sector, leading to 6.8%

overall growth in 2014 and 7.8% in 2015.

Overall, growth in the GCC region is expected

to average 4.5%-5.0% in 2014 and 5.0%-5.5%

in 2015.

Last but not least, Sub-Saharan Africa

continues to be the fastest growing region.

Following the much anticipated rebasing of its

GDP, Nigeria has become the biggest economy

in the subcontinent (26th

largest in the world)

at USD509bn in 2013. It is expected to grow

nearly 8% in 2014 and 7% in 2015 on a strong

diversification drive. Large investment

spending is also boosting growth in countries

like Ghana, Mozambique and Tanzania.

On the other hand, conflict in Central African

Republic, South Sudan, and the Democratic

Republic of Congo is hampering economic

development. Overall, the subcontinent is

expected to grow by 6.5% in 2014 and 7.0% in

2015.

Overall, the global growth picture continues to

be mixed. While advanced economies are

slowly recovering from the global recession,

their recovery looks fragile and still bumpy.

China’s growth momentum is slowing, but the

authorities have already taken measures to

address the slowdown. EM growth is likely to

weaken further in 2014 on tighter

macroeconomic policies and the negative

impact of further QE tapering. The only bright

spots remain the GCC and Sub-Saharan Africa.

Hopefully, no further bumps will derail the

weak global recovery.

Contacts

Joannes Mongardini

Head of Economics

Tel. (+974) 4453-4412

Rory Fyfe

Senior Economist

Tel. (+974) 4453-4643

Ehsan Khoman

Economist

Tel. (+974) 4453-4423

Hamda Al-Thani

Economist

Tel. (+974) 4453-4646

Ziad Daoud

Economist

Tel. (+974) 4453-4642

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.