Eng islamic economics islamic banking and maqasid syariah (2)

•Als PPTX, PDF herunterladen•

3 gefällt mir•1,223 views

Empfohlen

Weitere ähnliche Inhalte

Ähnlich wie Eng islamic economics islamic banking and maqasid syariah (2)

Ähnlich wie Eng islamic economics islamic banking and maqasid syariah (2) (20)

Mehr von Zahid Aziz

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Eng islamic economics islamic banking and maqasid syariah (2)

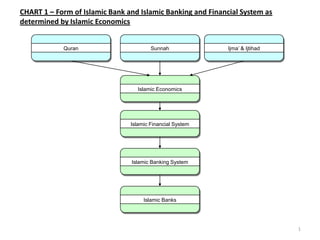

- 1. Quran Sunnah Ijma’ & Ijtihad Islamic Economics Islamic Financial System Islamic Banking System Islamic Banks CHART 1 – Form of Islamic Bank and Islamic Banking and Financial System as determined by Islamic Economics 1

- 2. Islamic Economics 1st Pillar World literally owned by God Man holds wealth on Trust for Allah swt and accountable for it in the Hereafter Islamic Bank Deposits are wealth they hold on Trust for Allah swt. 2nd Pillar God is One and all else are created All humans are equal and the best in the eyes of God is one with the highest Taqwa Islamic Bank The best Islamic Bank is not the most profitable one but one which exemplify highest Taqwa 3rd Pillar Belief in the Day of Judgement Time horizon of Man extends to the Hereafter. What he does in the world determines by consequences in Hereafter Islamic Bank Long term planning extends to the Hereafter CHART 2 – Implication of Pillars of Economics on Islamic Banks 2

- 3. Islamic Economics Principle of Ownership Ownership by Man confined to life, on death wealth distributed as specified by Allah swt. Principle of Balance Moderation in all aspects including Consumption. Consumption is not an end in itself Principle of Justice Justice in all aspects of economic activity. Justice expected to be observed in all aspects of Islamic Banking CHART 4 – Implication of Principles of Islamic Economics on Islamic Banks 3

- 4. Ownership by Man confined to life, on death wealth distributed as specified by Allah swt 4 Objective of Far’aid is to deconcentrate wealth Islamic Banking cannot have activities that leads to concentration of wealth Example, debt financing with bias towards people/companies with high collateral and equity

- 5. Moderation precludes profit maximisation as the primary objective. Moderation in all aspects including Consumption. Consumption is not an end in itself 5

- 6. Including: 1) Justice in relationship between Bank and Customer. 2) Justice in the allocation of risks between Bank and Customer. 3) Justice in the clauses of legal agreements between Banks and Customer Justice expected to be observed in all aspects of Islamic banking 6

- 7. Islamic Economics Prohibition by Law of Riba No dual system. Islamic Banking operates as a Sole Single System in a Sole Single Islamic Financial System. Qirad Driven Economy No lending in the economy. All will operate on Profit Sharing. Islamic Banks take deposits on Mudharabah and extends financing on Mudharabah Guarantee of Debt by the State Guarantee of consumption loans taken by Ummah Is there debt financing in an Islamic Economy? Will government guarantee all of debts owned by Ummah to banks? CHART 5 – Implications of Three Principal Parameters of Islamic Economics on Islamic Banking 7

- 8. Guarantee of minimum standard of living by the State Islamic Economics Implemented via Zakah CHART 6 – Implications of another Parameter of Islamic Economics – Guarantee of Minimum Standard of Living by the State. 8

- 9. Responsibility of Islamic Banks in guaranteeing minimum standard of living 9 Pay Zakah Assist in guaranteeing minimum standard of living Islamic Bank

- 10. 10 Therefore, Profit maximization must be replaced How? Not compatible with profit maximisation With what? Human Welfare

- 11. Al Ghazali & Al Shatibi Islam sets Goal for Human Life Maqasid Syariah Establishment of Justice Education of Mankind Prevention of Evil and Corruption. Maintenance of Balance in Human Nature. Islah Achievement of Maslahah. Human Welfare CHART 7 – What is Human Welfare Formula? 11

- 12. Achievement of Maslahah. Human Welfare Exigencies Essentials Religion Life Property Intellect Lineage Embellishments 12

- 13. Property Protection of Wealth and Prohibition of destruction of Wealth Prohibition of Transgression against property of others Equitable Distribution of Wealth Wealth should benefit owner and society Good circulation of wealth Spending on needy 13

- 14. Protection of wealth and Prohibition of destruction of wealth Required to take extra good care of customer’s property Prohibition of transgression against property of others Cannot operate in fiat money system Equitable distribution of wealth Financing allocated equitably to all big and small enterprises Good circulation of wealth Abandon debt financing focus on equity financing Wealth should benefit owner and society Financing to activities that maximizes benefits to society Encourage spending on needy Extend microfinance Implication of Syariah objectives on Property to Islamic Bank 14