Cross Currency Swaps - An Introduction

•

12 likes•12,574 views

An introduction to ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Cross Currency Swaps - An Introduction

Similar to Cross Currency Swaps - An Introduction (20)

Recently uploaded

Recently uploaded (20)

Cross Currency Swaps - An Introduction

- 1. Cross Currency Swaps An Introduction Version 1.0 (Draft), May 2014 by Werner Broennimann werner.broennimann@gmail.com

- 2. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 3. by werner.broennimann@gmail.com Motivation Cross Currency Swaps (CCS) are an important Financial Instrument in the OTC markets. Their features are often not fully understood, which can lead to confusion, especially in times of market distress. They are also a great tool to learn about rates and FX mechanics. Interest rate swaps, deposits, loans, FX swaps and FX forwards can all be regarded as special cases of CCS for economical and pricing purposes.

- 4. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 5. by werner.broennimann@gmail.com Introduction Cross Currency Swaps (CCS) are basically a long position in a bond in one currency and a short position in a bond of the same tenor in another currency. On the long position one receives coupons and on the short positions the coupons are paid.

- 6. by werner.broennimann@gmail.com Unlike in a single currency Interest Rate Swap (IRS), the bond notionals/principals* do not cancel out. These principals have to be funded and deposited respectively, at the appropriate rate. So the CCS has both derivatives and cash features. (Technically speaking bonds have notionals, swaps have principals. As swaps are explained with bonds in this presentation, the distinction of the terms will not be 100% strict.) Introduction - Differences

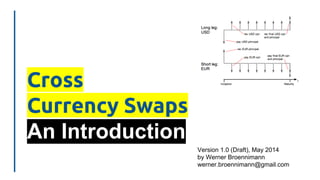

- 7. by werner.broennimann@gmail.com Introduction - Diagram Example: USD - EUR CCS Long leg: USD Short leg: EUR t As in the life of any bond, there are 3 phases: 1. Pay notional/principal upfront at Inception. 2. Receive coupons during lifetime. 3. Receive final coupon with notional/principal at Maturity. In the short leg the directions are reversed. MaturityInception pay USD principal rec EUR principal pay EUR cpn rec USD cpn rec final USD cpn and principal pay final EUR cpn and principal

- 8. by werner.broennimann@gmail.com Introduction - Use Cases The most common use cases of CCS are 1. hedging of foreign currency fixed income assets and liabilities (i.e. swapping foreign currency coupons in domestic ones) and 2. speculative carry trades (receiving high coupons in a high yielding currency and paying low coupons in a low yielding one).

- 9. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 10. by werner.broennimann@gmail.com Variants ● The two legs comprising the CCS can each be either floating or fixed. ● The most standard cross currency swap is a 3s-3s basis swap - both legs are floating 3-month LIBOR (or the common money market rate in the respective currency, such as EURIBOR in EUR). ● Any other variants of cross currency swaps can be understood as a 3s-3s basis swap with a single currency swap overlay on one or both of the legs.

- 11. by werner.broennimann@gmail.com Variants - Example Example: 5y EUR-USD CCS, client rec fix USD 1.6%, ann, 30/360 vs. client pay float EUR 6m EURIBOR - xx, semi-ann, a/360

- 12. by werner.broennimann@gmail.com Variants - Deconstruction This can be deconstructed into three 5y swaps: 1. USD IRS: client rec fix USD 1.6%, ann, 30/360 vs. client pay float 3m LIBOR, quart, a/360 2. Cross Currency Basis Swap: client rec float 3m LIBOR, quart, a/360 vs. client pay float 3m EURIBOR -yy, quart, a/360 3. EUR Intra Currency Basis Swap: client pay float 3m EURIBOR -yy, quart, a/360 vs client pay float EUR 6m EURIBOR -xx, semi-ann, a/360

- 13. by werner.broennimann@gmail.com Variants - Deconstruction Economically the blue and the green legs cancel out: 1. USD IRS: client rec fix USD 1.6%, ann, 30/360 vs. client pay float 3m LIBOR, quart, a/360 2. Cross Currency Basis Swap: client rec float 3m LIBOR, quart, a/360 vs. client pay float 3m EURIBOR -yy, quart, a/360 3. EUR Intra Currency Basis Swap: client pay float 3m EURIBOR -yy, quart, a/360 vs client pay float EUR 6m EURIBOR -xx, semi-ann, a/360

- 14. by werner.broennimann@gmail.com Variants - Deconstruction ● The deconstruction shows how the mid values in a more complex cross currency swap can be derived. ● Apart from the spread charged on the basis, the bank may or may not charge an additional spread on the IRS and on the Intra Currency Basis Swap.

- 15. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 16. by werner.broennimann@gmail.com Intra Currency Basis ● Intra Currency Basis is a difference in market prices and cannot be derived through TVM calculations. ● Swap rates reflect, among other things, the expectation of the relevant future money market fixings. ● In a world where 6s tends to fix consistently higher than 3s, one would expect the swap rate vs. 6s to be higher than vs. 3s.

- 17. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 18. by werner.broennimann@gmail.com Cross Currency Basis ● The cross currency basis (or just ‘basis’) is the mid “price” of entering a basis swap. ● The basis is a market price and cannot be derived mathematically in a traditional LIBOR discounting framework. ● Pre financial crisis, it was often not well understood. ● Explanations typically focussed purely on supply and demand in the cross currency market. ● The main drivers are the funding and depositing of the cash principals.

- 19. by werner.broennimann@gmail.com Cross Currency Basis ● The concept of basis was difficult to reconcile with single currency IRS. Example: ● In an EUR IRS, a 3 months EURIBOR flat leg was worth Par (100% of principal). ● In a EUR-USD CCS, a 3 months EURIBOR leg +/- the respective currency basis was was worth Par. The two are contradicting.

- 20. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 21. by werner.broennimann@gmail.com Funding Valuation Adjustment ● One of the main changes in interest rate markets and general time value of money calculations is the introduction of Funding Valuation Adjustment (FVA) and its sibling Differential Discounting (DD). ● The key point is to use the true cost of funding as a basis of discounting and other time value of money calculations.

- 22. by werner.broennimann@gmail.com ● Banks’ true funding cost was always known to be different from the swap rates or LIBOR/EURIBOR. ● However, before the financial crisis any LIBOR based discounting was a reasonably good approximation. ● After the fall of Lehman that did no longer work. ● When trying to determine that true cost of funding, it turns out that things get a bit more complicated. Funding Valuation Adjustment

- 23. by werner.broennimann@gmail.com Funding Valuation Adjustment ● It is in the hand of the bank treasurer to determine, at what levels he can fund or deposit cash. ● The rates offered by the respective central bank are typically a good start, but often the treasurer achieves slightly different rates. ● These are the rates that should be used for discounting in the bank. ● For a corporate client as a price taker from the bank they have to agree on such a discounting rate.

- 24. by werner.broennimann@gmail.com Funding Valuation Adjustment ● Funding Valuation Adjustment (FVA) makes the currency basis both more complicated and also more cohesive. ● The principles of valuing a leg of a CCS in a FVA environment are also valid for a leg in a single currency swap.

- 25. by werner.broennimann@gmail.com FVA - deriving the Basis Example: 5y CCS (no CSA involved) ● Assumptions: ○ USD funding: 3 months LIBOR + xx ○ EUR funding 3 months EURIBOR + yy

- 26. by werner.broennimann@gmail.com FVA - deriving the Basis Example: 5y CCS (no CSA involved) ● Instead of quoting 3m$ + xx vs. 3m€ + yy the standard way to quote is 3m$ flat vs. 3m€ + zz, such that PV(3m$ + xx vs. 3m€ + yy) = PV(3m$ flat vs. 3m€ + zz). ● zz is the 5y EUR Currency Basis (no CSA involved). ● Depending on xx and yy it can be negative.

- 27. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 28. by werner.broennimann@gmail.com Credit Support Annex ● A Credit Support Annex (CSA) is an extension to a standard ISDA contract between OTC counterparties. ● A CSA is similar to a margin account but for OTC products. ● If cash is posted as collateral, it will earn a certain interest, which is defined in the terms of the CSA. ● The collateral can also consist of bonds, which will just earn their coupon payments.

- 29. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Value Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 30. by werner.broennimann@gmail.com Differential Discounting ● A lot of OTC instruments, like CCSs, are traded under an ISDA containing a CSA. ● MtM fluctuations in the swap are met by the posting of collateral by the debtor counterparty. ● This collateral earns interest at a rate which is often different from the funding rate of the bank. ● This changes the opportunity cost of a future cash flow. ● Therefore the correct rate to use for discounting is the rate defined in the CSA.

- 31. by werner.broennimann@gmail.com Differential Discounting ● If the CSA allows for collateral in several currencies, then there is embedded optionality (similar to the cheapest to deliver option on a bond future). ● The debtor counterparty can always choose to post in the cheapest collateral currency. ● Changes in the Cross Currency Basis can change which collateral currency is the cheapest. ● This embedded optionality has value and further complicates determining the effective funding rate.

- 32. by werner.broennimann@gmail.com Differential Discounting ● As seen in the example of the 5y CCS, the funding levels drive the currency basis. ● Different funding levels because of a CSA will change the currency basis as well.

- 33. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 34. by werner.broennimann@gmail.com Credit Valuation Adjustment ● Credit Valuation Adjustment (CVA) is the difference between the risk free position value and the true position value that takes credit risk into account. ● There are different ways of modelling CVA and it is beyond the scope of this presentation to go into details of models. ● CVA is impacted by the features of an OTC swap, such as tenor, notional, application of a CSA, credit spread of counterparty etc.

- 35. by werner.broennimann@gmail.com Credit Valuation Adjustment ● Depending on the counterparty any potential CVA may be waived if certain business reasons apply. ● The main reason is significant 2-way business (and hence offsetting risk). ● Transacting an OTC swap under a CSA will typically reduce the CVA by a lot.

- 36. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 37. by werner.broennimann@gmail.com FX Impact ● At inception, floating swap legs and fixed rate swap legs with at-market rates have a PV of close to zero, when including the initial and final principal payment. ● If both swap legs in a CCS have a PV of close to zero each, then there is only a small FX position created. ● Depending on the effective FX rate used (the ratio of the principals), there is the need for a small FX hedge.

- 38. by werner.broennimann@gmail.com FX Impact ● Fixed rate CCS are often used to swap bond or loan notionals and coupons into another currency. ● Depending on the credit quality of the borrower, the fixed rate may be significantly different from a market swap rate of that tenor. ● At inception, the fixed leg in such a CCS would have a PV which is different from zero, which can create a bigger FX position.

- 39. by werner.broennimann@gmail.com ● If CCS are used for carry trades, they are typically done at market rates. ● The CCS should be done at the market FX rate, when it is executed. ● Using the at-market FX rate assures, that the two principals have identical value at that point in time. ● Therefore the initial exchange of principals has zero economical impact. FX Impact

- 40. by werner.broennimann@gmail.com ● For speculative carry trades, clients often trade without the initial principal exchange. ● However, this often creates a significantly bigger FX position on the swap, as both legs are now worth in the region of 100% of the respective principal, and not 0. ● If the client decides to use a predetermined FX rate, then this can create massive swings in the upfront value of the CCS (without initial exchange). FX Impact

- 41. by werner.broennimann@gmail.com ● In a CCS without initial exchange, there is a simple possibility to create large upfront values when using an off-market FX rate. ● Intermediary banks that deal with corporate clients and hedge with investment banks sometimes use that, to source their fee and potential credit charge on client trades. ● It can also be used for outright derivatives based financing, as happened in the case of Greece. FX Impact

- 42. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 43. by werner.broennimann@gmail.com Cross Currency Swaptions There has never been a liquid market in currency basis volatility. Hence, most interest rate option trading desks decline to quote on cross currency swaptions. Some trading desks quote a small variety of swaptions, but these are more akin to bespoke, exotic transactions. Also, they tend to be more accepting of buying the options. The transaction costs for clients will be significantly higher than in the highly competitive CCS and Interest Rate Swaption markets.

- 44. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 45. by werner.broennimann@gmail.com Summary ● The pricing of CCS is mainly driven by the funding rate of the market maker. ● The correct funding to use is not LIBOR. ● If there is no CSA involved, it is a rate determined by the market maker’s treasury. ● Otherwise the interest rate determined in the CSA terms drive the funding cost.

- 46. by werner.broennimann@gmail.com Table of Contents ● Motivation ● Introduction ● Variants ● Intra Currency Basis ● Cross Currency Basis ● Funding Valuation Adjustment ● Credit Support Annex ● Differential Discounting ● Credit Valuation Adjustment ● FX Impact ● Cross Currency Swaptions ● Summary ● Conclusions

- 47. by werner.broennimann@gmail.com Conclusions ● Cross Currency Swaps are not complicated. ● In the end it all boils down to discounting a set of future cash flows at the correct rates. ● The currency basis is a reflection of this discounting. ● To use the correct rates, Funding Valuation Adjustment and potentially Differential Discounting have to be understood and implemented.