Andreas Schleicher presents at the launch of What does child empowerment mean...

Acnts peckin

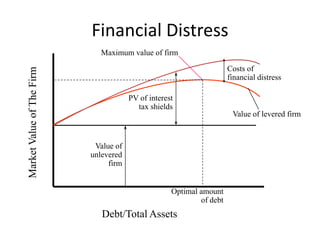

1. Financial Distress

Maximum value of firm

Costs of

Market Value of The Firm

financial distress

PV of interest

tax shields

Value of levered firm

Value of

unlevered

firm

Optimal amount

of debt

Debt/Total Assets

2. Capital Structure and Financial Distress

Costs of Financial Distress - Costs arising from bankruptcy

or distorted business decisions before bankruptcy.

Market Value = Value if all Equity Financed

+ PV Tax Shield

- PV Costs of Financial Distress

3. Financial Choices

Trade-off Theory - Theory that capital structure is

based on a trade-off between tax savings and distress

costs of debt.

Pecking Order Theory - Theory stating that firms prefer

to issue debt rather than equity if internal finance is

insufficient.

4. Pecking Order Theory

The announcement of a stock issue drives down the stock price because

investors believe managers are more likely to issue when shares are

overpriced.

Therefore firms prefer internal finance since funds can be raised without

sending adverse signals.

If external finance is required, firms issue debt first and equity as a last

resort.

The most profitable firms borrow less not because they have lower

target debt ratios but because they don't need external finance.

5. Pecking Order Theory

Some Implications:

Internal equity may be better than external equity.

Financial slack is valuable.

If external capital is required, debt is better. (There

is less room for difference in opinions about what

debt is worth).

6. Pecking Order Theory

Stewart Myers (1984)

• Managers are better informed than investors.

Investors might see an external equity

issuance a bad news about the

company, assuming that managers want

outside shareholders to share the loss, thus

investors will react to this issuance

negatively, increasing the issuance cost of

external equity. 6

7. Firms therefore prioritize their sources of

financing according to the law of least

effort, or of least resistance: internal funds are

used first, and when that is depleted, debt is

issued, and when it is not sensible to issue any

more debt, equity is issued.

This theory maintains that businesses adhere to

a hierarchy of financing sources and prefer

internal financing when available, and debt is

preferred over equity if external financing is

required.

7

8. MM Version Three: with Multiple Frictions

• Taxes: mentioned earlier (in MM Version Two).

• Bankruptcy cost: direct costs (such as legal costs)

and indirect costs (such as reputation loss and

financial distress).

• Agency problems: [e.g.] risk-shifting firm may

increase risk and thereby extract value from

existing bondholders. (Covenants could reduce

the problems)

• Free cash flow reduction: debt might reduce extra

cash in the firms hence alleviate management

deviations.

8

9. PECKING ORDER THEORY

• Firm do not have any target capital structure and

there is no optimum capital structure.

• Assumption

Asymmetric information-Professional managers of the

firm are well equipped with more information when

compared to investors.

10. Why to prefer retained earnings more??

• Easy to use , cheaper & no transaction cost

• Avoid capital market regulations.

• Don’t have adequate reliable information about

capital market.

• The announcement of a stock issue drives down the

stock price because investors believe managers are

more likely to issue when shares are overpriced.

• Therefore firms prefer internal finance since funds

can be raised without sending adverse signals.

• Shareholders need not pay any personal taxes.

• No Interest - steady cash flow.

•

11. Why to prefer debt more??

• Tax deductibility of interest charges.

12. Outcome of the theory

• The most profitable firms borrow less not

because they have lower target debt ratios

but because they don't need external finance.

• Negative inverse relationship between

profitability and debt ratio.