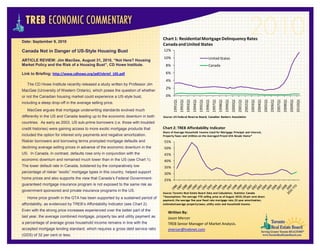

1. Chart 1: Residential Mortgage Delinquency Rates

Date: September 9, 2010

Canada and United States

Canada Not in Danger of US-Style Housing Bust 12%

10% United States

ARTICLE REVIEW: Jim MacGee, August 31, 2010, “Not Here? Housing

Market Policy and the Risk of a Housing Bust”, CD Howe Institute. 8% Canada

Link to Briefing: http://www.cdhowe.org/pdf/ebrief_105.pdf 6%

4%

The CD Howe Institute recently released a study written by Professor Jim

2%

MacGee (University of Western Ontario), which poses the question of whether

or not the Canadian housing market could experience a US-style bust, 0%

1991Q1

1992Q1

1993Q1

1994Q1

1996Q1

1998Q1

2000Q1

2002Q1

2004Q1

2006Q1

2008Q1

2009Q1

2010Q1

1995Q1

1997Q1

1999Q1

2001Q1

2003Q1

2005Q1

2007Q1

including a steep drop-off in the average selling price.

MacGee argues that mortgage underwriting standards evolved much

differently in the US and Canada leading up to the economic downturn in both Source: US Federal Reserve Board; Canadian Bankers Association

countries. As early as 2003, US sub-prime borrowers (i.e. those with troubled

credit histories) were gaining access to more exotic mortgage products that Chart 2: TREB Affordability Indicator

Share of Average Household Income Used for Mortgage Principal and Interest,

included the option for interest only payments and negative amortization. Property Taxes and Utilities on the Averaged Priced GTA Resale Home*

Riskier borrowers and borrowing terms prompted mortgage defaults and 55%

declining average selling prices in advance of the economic downturn in the 50%

US. In Canada, in contrast, defaults rose only in conjunction with the 45%

economic downturn and remained much lower than in the US (see Chart 1). 40%

The lower default rate in Canada, bolstered by the comparatively low 35%

percentage of riskier “exotic” mortgage types in this country, helped support 30%

home prices and also supports the view that Canada’s Federal Government- 25%

guaranteed mortgage insurance program is not exposed to the same risk as

government sponsored and private insurance programs in the US.

Source: Toronto Real Estate Board Data and Calculation; Statistics Canada

*Assumptions: The average YTD selling price as of August 2010; 20 per cent down

Home price growth in the GTA has been supported by a sustained period of

payment; the average five year fixed rate mortgage rate; 25 year amortization;

affordability, as evidenced by TREB’s Affordability Indicator (see Chart 2). estimated average property taxes, utility costs and household income.

Even with the strong price increases experienced over the better part of the

Written By:

last year, the average combined mortgage, property tax and utility payment as Jason Mercer

a percentage of average gross household income remains in line with the TREB Senior Manager of Market Analysis.

accepted mortgage lending standard, which requires a gross debt service ratio jmercer@trebnet.com

(GDS) of 32 per cent or less.