Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to Swan aug-15

Similar to Swan aug-15 (20)

More from Frank Ragol

More from Frank Ragol (20)

Recently uploaded

Recently uploaded (20)

Swan aug-15

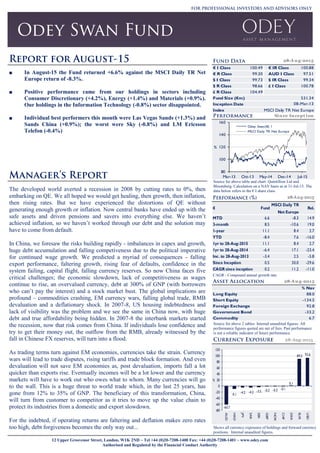

- 1. 12 Upper Grosvenor Street, London, W1K 2ND ~ Tel +44 (0)20-7208-1400 Fax: +44 (0)20-7208-1401 ~ www.odey.com Authorised and Regulated by the Financial Conduct Authority ■ In August-15 the Fund returned +6.6% against the MSCI Daily TR Net Europe return of -8.3%. ■ Positive performance came from our holdings in sectors including Consumer Discretionary (+4.2%), Energy (+1.4%) and Materials (+0.9%). Our holdings in the Information Technology (-0.8%) sector disappointed. ■ Individual best performers this month were Las Vegas Sands (+1.3%) and Sands China (+0.9%); the worst were Sky (-0.8%) and LM Ericsson Telefon (-0.4%) 28-Aug-2015 The developed world averted a recession in 2008 by cutting rates to 0%, then embarking on QE. We all hoped we would get healing, then growth, then inflation, then rising rates. But we have experienced the distortions of QE without generating enough growth or inflation. Now central banks have ended up with the safe assets and driven pensions and savers into everything else. We haven’t achieved inflation, so we haven’t worked through our debt and the solution may have to come from default. In China, we foresaw the risks building rapidly - imbalances in capex and growth, huge debt accumulation and falling competiveness due to the political imperative for continued wage growth. We predicted a myriad of consequences - falling export performance, faltering growth, rising fear of defaults, confidence in the system failing, capital flight, falling currency reserves. So now China faces five critical challenges; the economic slowdown, lack of competitiveness as wages continue to rise, an overvalued currency, debt at 300% of GNP (with borrowers who can’t pay the interest) and a stock market bust. The global implications are profound – commodities crashing, EM currency wars, falling global trade, RMB devaluation and a deflationary shock. In 2007-8, US housing indebtedness and lack of visibility was the problem and we see the same in China now, with huge debt and true affordability being hidden. In 2007-8 the interbank markets started the recession, now that risk comes from China. If individuals lose confidence and try to get their money out, the outflow from the RMB, already witnessed by the fall in Chinese FX reserves, will turn into a flood. As trading terms turn against EM economies, currencies take the strain. Currency wars will lead to trade disputes, rising tariffs and trade block formation. And even devaluation will not save EM economies as, post devaluation, imports fall a lot quicker than exports rise. Eventually incomes will be a lot lower and the currency markets will have to work out who owes what to whom. Many currencies will go to the wall. This is a huge threat to world trade which, in the last 25 years, has gone from 12% to 35% of GNP. The beneficiary of this transformation, China, will turn from customer to competitor as it tries to move up the value chain to protect its industries from a domestic and export slowdown. For the indebted, if operating returns are faltering and deflation makes zero rates too high, debt forgiveness becomes the only way out... € Fund MSCI Daily TR Net Europe Rel. MTD 6.6 -8.3 14.9 3-month 8.5 -10.6 19.0 1-year 11.1 8.4 2.7 YTD -8.4 7.6 -16.0 1yr to 28-Aug-2015 11.1 8.4 2.7 1yr to 28-Aug-2014 -6.4 17.1 -23.4 Inc. to 28-Aug-2013 -3.4 2.5 -5.8 Since Inception 0.5 30.0 -29.6 CAGR since inception 0.2 11.2 -11.0 28-Aug-2015 € I Class 100.49 € IR Class 100.88 € R Class 99.30 AUD I Class 97.51 $ I Class 99.73 $ IR Class 99.34 $ R Class 98.66 £ I Class 100.78 £ R Class 104.49 Fund Size (€m) 531.34 Inception Date Index MSCI Daily TR Net Europe 28-A ug-2015 08-Mar-13 Since Incept ion 80 100 120 140 160 Mar-13 Oct-13 May-14 Dec-14 Jul-15 % Odey Swan(€) I MSCI Daily TR Net Europe 28-A ug-2015 % Nav Long Equity 88.0 Short Equity -134.5 Foreign Exchange 92.8 Government Bond -33.2 Commodity 6.7 -60.7 -9.1 -4.2 -4.2 -3.5 -0.3 -0.3 -0.1 0.1 89.5 92.6 -80 -60 -40 -20 0 20 40 60 80 100 120 AUD HKD JPY SAR SEK GBP NOK CHF DKK EUR USD % Shows all currency exposures of holdings and forward currency positions. Internal unaudited figures. Source for above 2 tables: Internal unaudited figures. All performance figures quoted are net of fees. Past performance is not a reliable indicator of future performance. CAGR - Compound annual growth rate Source for above table and chart: Quintillion Ltd and Bloomberg. Calculation on a NAV basis as at 31-Jul-15. The data below refers to the € I share class.

- 2. 12 Upper Grosvenor Street, London, W1K 2ND ~ Tel +44 (0)20-7208-1400 Fax: +44 (0)20-7208-1401 ~ www.odey.com Authorised and Regulated by the Financial Conduct Authority In Developed Market (DM) equities, we have high valuations and earnings risk. Not many assets are currently in distress but there is evidence everywhere of the downturn. Three years after the replacement cycle began, we see growth faltering - commodity capex is falling, the oil price is killing new aircraft demand, cars have already been replaced using cheap credit. As demand weakens, we find ourselves on peak multiples of peak margins. Everyone has stayed in equities because there is nowhere else to go, yet our short equity book has made money when it shouldn’t have done, in a world chasing carry. The alpha in our short book has come from the sectors that broke early such as the Miners, but in August the whole market broke down and, unlike last October, the technicals have turned, as short-term moving averages broke below their long-term equivalents. We are not guaranteed a DM recession, but we are certainly not priced for any risk of one. Workaday stocks like Kellogg are priced at 18-20x after a seven-year QE-fuelled market up cycle and the market is narrowing. Valuations are so extended that they will need to fall 30-40% to be compelling in terms of carry. So for investors, after a tumultuous August, the question is whether these shocks and adjustments are largely complete. Our overriding conviction is that we are nearer the beginning of this process than the end. As discussed, China has huge adjustments to make in terms of debt, competitiveness and lower growth (which will feel like recession to them), all the while needing to stabilise the stock market, retain confidence in the system, keep the Party and people happy and manage a migration from capex-led to service-biased growth. A virtually impossible task. We are already in a deflationary downdraft amidst currency wars, yet China, the most bellicose country with the biggest army, has just fired the first shot. In our view the cycle is no more abolished now than it was in 2007, when Bear Stearns and Northern Rock were seen as containable. As Andy Haldane says, there is a recession every decade. We are now due ours. It is too late to chase the QE happy trade, but not to enjoy the deflationary bust.

- 3. 12 Upper Grosvenor Street, London, W1K 2ND ~ Tel +44 (0)20-7208-1400 Fax: +44 (0)20-7208-1401 ~ www.odey.com Authorised and Regulated by the Financial Conduct Authority This communication is for information purposes only and not intended to be viewed as a piece of independent investment research. © 2015 Odey Asset Management LLP (“OAM”) has approved this communication which is for private circulation only, and in the UK is directed to persons who are professional clients or eligible counterparties for the purposes of the FCA’s Conduct of Business Sourcebook and it is not intended for and must not be distributed to retail clients. It does not constitute an offer to sell or an invitation to buy or invest in any of the securities or funds mentioned herein and it does not constitute a personal recommendation or investment taxation or any other advice. The information and any opinions have been obtained from or are based on sources believed to be reliable, but accuracy cannot be guaranteed. Past performance does not guarantee future results and the value of all investments and the income derived therefrom can decrease as well as increase. Investments that have an exposure to currencies other than the base currency of the fund may be subject to exchange rate fluctuations. This communication and the information contained therein may constitute a financial promotion for the purposes of the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”) and the rules of the FCA. This communication is not subject to any restrictions on dealing ahead. The distribution of this communication may, in some countries, be restricted by law or regulation. Accordingly, anyone who comes into possession of this communication should inform themselves of and observe these restrictions. OAM is not liable for a breach of such restrictions or for any losses relating to the accuracy, completeness or use of information in this communication, including any consequential loss. Please always refer to the fund’s prospectus. OAM whose company No. is OC302585 and whose registered office is at 12 Upper Grosvenor Street, London, W1K 2ND, is authorised and regulated by the Financial Conduct Authority. Enquiries: Andrew King Tel: +44 20 7208-1454 Email: a.king@odey.com Sarah St. George Tel: +44 20 7208-1432 Email: s.stgeorge@odey.com 28-Aug-15 For the month ending 28-Aug-1528-Aug-15 Crispin Odey Portfolio Manager The investment objective of the sub-fund is to achieve long term capital appreciation by investing principally in a portfolio of equities and equity related securities, debt securities and currencies. The funds investments will tend, over time, to be weighted towards European Securities but investments in non-European securities will not be subject to any limit. The fund will invest in asset classes including equities, equity related securities (such as warrants, convertible bonds and exchange traded funds), derivatives (including those simulating short positions), government and corporate debt securi- ties, collective investment schemes (including exchange traded funds), commodities, currencies and cash. Derivatives may be used for investment purposes and to manage the risk profile of the fund. Comparative benchmark Primary: Cash, Secondary: MSCI Daily TR Net Europe Fund inception date 08 March 2013 Fund type Irish long-short UCITS IV Base currency € Share classes I (€, £, $, AUD), R (€, £, $), IR (€, $) Hedging Non-base currencies are unhedged Dealing / Valuation Daily forward to 2pm / COB Front end fee Up to 5%. Annual Management fee I (€, £, $, AUD) & IR (€, $) 1.0%, R (€, £, $) 1.5%. Performance fee 20% of the increase in the value per share of the fund between the beginning and the end of the year. Fees crystallise annually. Losses carried forward. Anti-dilution fee Applies to subs/reds if net subs/reds >5% of NAV Min. investment I class €1,000,000 (or equivalent in £, $, AUD) R class €5,000 (or equivalent in £, $) Dividends Reporting and accumulation share classes available Administrator Quintillion Ltd. Custodian J.P. Morgan Bank (Ireland) Ltd Auditor Deloitte & Touche LLP Price reporting Prices published daily in Financial Times SEDOL: €I B4WC409, £I B87KFG9, $I B8B7QR4, €R B988MM4, £R B7W59X7, $R B8MJTS1 €IR B6YRXK9, AUD I BFTCNC48 $IR B8MJTS1 ISIN: €I IE00B4WC4097, £I IE00B87KFG99, $I IE00B8B7QR45 €R IE00B988MM46, £R IE00B7W59X71, $R IE00B8MJTS18 €IR IE00B6YRXK9, $IR IE00B8MJTS18, AUD I IE00BFTCNC48 28-Aug-15 Rank Security Strategy Notional Exposure (%) 1 JPN 10Y Bond(Ose) Sep15 Short 46.3 2 ACGB 2 3/4 04/21/24 Long 13.2 3 FTSE 100 IDX FUT Sep15 Long 5.1 4 DAX INDEX FUTURE Sep15 Long 5.0 5 ETFS Cotton Long 3.8 Rank Security Strategy Notional Exposure (%) 1 Sky Long 9.2 2 Las Vegas Sands Short 6.0 3 Swatch Short 5.7 4 Adidas Short 5.2 5 Intu Properties Short 4.2 -300 -200 -100 0 100 200 300 Mar-13 Jul-13 Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 % Long Equity Exposure Short Equity Exposure Net Equity Exposure FX Exposure Government Bond Exposure -15 -10 -5 0 5 10 15 20 25 ConsumerDiscretionary ConsumerStaples Energy Financials HealthCare Industrials InformationTechnology Materials Telecommunication Services Utilities % Fund Index -2 -1 0 1 2 3 4 5 Consumer Discretionary ConsumerStaples Energy Financials HealthCare Industrials Information Technology Materials Telecommunication Services Utilities % Fund Index Internal unaudited figures Internal unaudited figures Internal unaudited figures Internal unaudited figures