Federal Debt Projected to Decline Under Current Law But Rise Under Alternative Scenario

•

4 likes•40,638 views

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (16)

Similar to Federal Debt Projected to Decline Under Current Law But Rise Under Alternative Scenario

Similar to Federal Debt Projected to Decline Under Current Law But Rise Under Alternative Scenario (20)

More from Congressional Budget Office

More from Congressional Budget Office (20)

Recently uploaded

Recently uploaded (10)

Federal Debt Projected to Decline Under Current Law But Rise Under Alternative Scenario

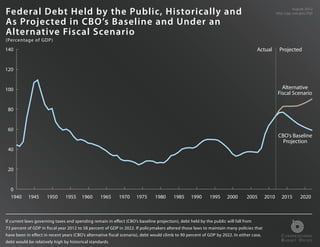

- 1. Federal Debt Held by the Public, Historically and August 2012 http://go.usa.gov/7QY As Projected in CBO’s Baseline and Under an Alternative Fiscal Scenario (Percentage of GDP) 140 Actual Projected 120 100 Alternative Fiscal Scenario 80 60 CBO’s Baseline Projection 40 20 0 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 If current laws governing taxes and spending remain in effect (CBO’s baseline projection), debt held by the public will fall from 73 percent of GDP in fiscal year 2012 to 58 percent of GDP in 2022. If policymakers altered those laws to maintain many policies that have been in effect in recent years (CBO’s alternative fiscal scenario), debt would climb to 90 percent of GDP by 2022. In either case, C ONGRESSIONAL debt would be relatively high by historical standards. B UDGET O FFICE

- 2. Congressional Budget Office An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 August 2012 The Budget Outlook

- 3. Def i cits Projected in CBO’s Baseline and August 2012 http://go.usa.gov/7QY Under an Alternative Fiscal Scenario (Percentage of GDP) 8 7 6 5 Additional Debt Service 4 Prevent Spending Cuts 3 Extend Tax Policies 2 1 Baseline 0 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Deficits under CBO’s current-law baseline projection average about 1 percent of GDP over the 2013–2022 period. By comparison, under an alternative scenario, in which some changes specified in current law would not occur and many tax and spending policies that have been in effect in recent years would continue instead, deficits over that period would average about 5 percent of GDP. C ONGRESSIONAL B UDGET O FFICE

- 4. Total Discretionary Budget Authority Excluding War August 2012 http://go.usa.gov/7QY Funding, Disaster Relief, and Program Integrity Initiatives (Percentage of GDP) 12 Actual Projected 10 Historical Funding and CBO’s Baseline 8 Funding for 2012 Adjusted for Inflation 6 4 Excluding Enforcement Procedures 2 0 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 The caps on discretionary spending—either with the required automatic reductions (as in CBO’s baseline) or without them (as in the alternative fiscal scenario)—will necessitate a reduction in the real resources available for many government programs, compared with the funding provided for 2012. If, instead, funding was allowed to grow at the rate of inflation, it would be 17 percent higher in 2022 C ONGRESSIONAL than the amounts projected in the baseline. B UDGET O FFICE

- 5. Congressional Budget Office An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 August 2012 The Economic Outlook

- 6. Federal Debt Held byProduct Real Gross Domestic the Public, Historically and January 2012 August 2012 http://go.usa.gov/7QY http://go.usa.gov/nPi As Projected in CBO’s Baseline and Under an (Percentage change, fourth quarter to fourth quarter) Alternative Fiscal Scenario (Percentage of GDP) 4 Recession 3.9 Recession 2.9 2.9 3 2.8 2.4 2.4 First 2.2 Half 2 1.9 2.0 1.7 1 0.4 0 -0.1 -1 -2 -3 -3.3 -4 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Witheconomydeficits anticipated for much of the 10-year projection period of CBO’s GDP rose at an average annual rate the1.7 percent in The modest has continued to expand modestly this year. Real (inflation-adjusted) current-law baseline, debt held by of public the first half of the year, of GDP. However, than in 2011 changes specified in current law did not occur and certain current policies recedes as a percentage somewhat slower if some of theand less than its average rate during the previous expansion. CBO anticipates werethe pace of instead, debt held by will increase slightly during percent of GDP by the end of 2022, the highest figure since just that continued economic expansion the public would rise to 94 the rest of 2012. C ONGRESSIONAL B UDGET O FFICE after World War II.

- 7. Real Business Fixed Investment August 2012 http://go.usa.gov/7QY (Percentage change from same quarter of previous year) 20 12.5 11.0 10 10.2 0 -10 -9.5 -20 -20.1 -30 2000 2002 2004 2006 2008 2010 2012 Business investment has grown rapidly over the past year. Real (inflation-adjusted) business fixed investment—in structures, equipment, and software—grew by 10.2 percent over the year that ended in the second quarter of 2012. Despite that growth, the total amount of net investment (fixed investment minus depreciation) as a fraction of GDP remains unusually low. C ONGRESSIONAL B UDGET O FFICE

- 8. Housing Market Indicators August 2012 http://go.usa.gov/7QY (Percentage change from same quarter of previous year) 20 10.7 House Prices 10 2.2 0 Real Residential Investment -10 -20 -30 2000 2002 2004 2006 2008 2010 2012 A recovery in the housing market appears to be under way. Real (inflation-adjusted) residential investment—spending on home construction and improvements, mobile homes, and brokers’ commissions—was almost 11 percent higher in the second quarter of 2012 than in the same quarter last year. House prices seem to have reached their bottom and have been rising in 2012. C ONGRESSIONAL B UDGET O FFICE

- 9. Economic Growth in the United States and August 2012 http://go.usa.gov/7QY Among Its Leading Trading Partners (Percentage change from same quarter of previous year) 6 Actual Projected 4 Leading Trading Partners 2 United States 0 -2 -4 -6 2000 2005 2010 2015 2020 Economic growth among the nation’s leading trading partners, which peaked in mid-2010, has continued to slow, while the U.S. economy has continued to grow at a modest pace since mid-2011. That different pattern of growth is a primary factor behind CBO's forecast of weaker net exports in the second half of 2012. (Actual data include the July 2012 revisions to the national income and C ONGRESSIONAL B UDGET O FFICE product accounts; projected data do not.)

- 10. Long-Term Unemployment August 2012 http://go.usa.gov/7QY (Percent) 50 Recession Recession First 43.8 Half 43.3 42.2 40 31.5 30 22.1 21.8 20 19.6 19.7 18.4 17.6 17.6 11.4 11.8 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 The share of unemployment accounted for by the long-term unemployed—people who have been seeking work for more than 26 consecutive weeks—has topped 40 percent for the past two and a half years. By comparison, that share was about 22 percent in 2003, in the aftermath of the 2001 recession. C ONGRESSIONAL B UDGET O FFICE

- 11. Inf l ation August 2012 http://go.usa.gov/7QY (Percentage change in prices from same quarter of previous year) 5 4 Overall 3 2 Core 1 0 -1 2000 2002 2004 2006 2008 2010 2012 Inflationary pressures remain subdued: The average rate of inflation in consumer prices during the year ending in the second quarter of 2012 was less than 2 percent. C ONGRESSIONAL B UDGET O FFICE

- 12. Unemployment Rate August 2012 http://go.usa.gov/7QY (Percent) 12 Actual Projected 9.9 2009, 4Q 10 9.1 2013, 4Q CBO’s 8 8.2 Baseline 2012, 2Q Projection 5.8 2003, 4Q 8.0 6 2013, 4Q Alternative Fiscal Scenario 4 4.4 3.9 2006, 4Q 2000, 4Q 2 0 2000 2005 2010 2015 2020 Because of the sharp deficit reduction that will occur under current law, CBO projects that the unemployment rate will rise to about 9 percent in the fourth quarter of 2013. Under an alternative scenario, in which some changes specified in current law would not occur and many tax and spending policies that have been in effect in recent years would continue instead, unemployment would remain near 8 percent in 2013. C ONGRESSIONAL B UDGET O FFICE

- 13. GDP and Potential GDP August 2012 http://go.usa.gov/7QY ( Trillions of 2005 dollars) 20 Actual Projected 18 16 Potential GDP 14 GDP 12 10 0 2000 2005 2010 2015 2020 CBO expects that real (inflation-adjusted) GDP will stay below the economy’s potential—a level that corresponds to a high rate of use of labor and capital—until 2018. Potential GDP is projected to grow at an average annual rate of 2.4 percent between 2018 and 2022 and by an average of 2.2 percent for the 2012–2022 projection period. (Actual data include the July 2012 revisions to the national C ONGRESSIONAL B UDGET O FFICE income and product accounts; projected data do not.)

- 14. Labor Income August 2012 http://go.usa.gov/7QY (Percentage of gross domestic income) 65 Actual Projected 64 63 Average, 1980 to 2011 62 (61.9%) 61 60 59 0 1980 1985 1990 1995 2000 2005 2010 2015 2020 Since the end of the recession, labor income has fallen as a share of gross domestic income—the sum of all income earned in the production of GDP—reinforcing its downward trend since 1980. In CBO’s projections, labor income grows faster over the next decade, bringing its share to about 61 percent by 2022, just below the historical average since 1980. (Actual data include the July 2012 revisions C ONGRESSIONAL B UDGET O FFICE to the national income and product accounts; projected data do not.)