1. Bills of Exchange (including Accommodation Bill) Unit - 3

Bill of Exchange

Definition of Bills of Exchange;

A bill of exchange is defined under Section 5 of the

Negotiable Instrument Act 1881, “ as an instrument in

writing containing an unconditional order, signed by the

maker directing a certain person to pay a certain sum of

money only to, or to the order of a certain person or to the

bearer of the instrument”. When such an order is accepted by

the buyer is becomes a valid bill of exchange. Before

acceptance, the bill is called a draft.

Feature of bills of exchange:

i. It must be in writing;

ii. It must be signed by the maker or drawer;

iii. It must be an unconditional order and not a request;

iv. The amount of the bill must be certain;

v. The amount must be paid within a specified period or

on demand;

vi. The payment must be made in legal tender money in

India;

vii. The drawer, drawee and the payee must be definite;

viii. It must be accepted by the drawee;

ix. A bill of exchange must be properly stamped as per

Stamps Act;

x. The bill may be payable on demand or after the expiry

of definite period.

Parties to a Bill of Exchange

There are three parties to a bill of exchange:

1. Drawer: The person who draws the bill is called drawer.

The drawer is the creditor or the seller of the goods. Ram

Prasad is the drawer.

2. Drawee: The person on whom the bill is drawn is called

drawee. The drawee is the debtor or the buyer of the

goods. Vinodh Sahani is the drawee.

3. Payee: The person to whom the sum stated in the bill is

payable is called payee. Either the drawer or any other

person may be the payee. Ram Prasad is the payee.

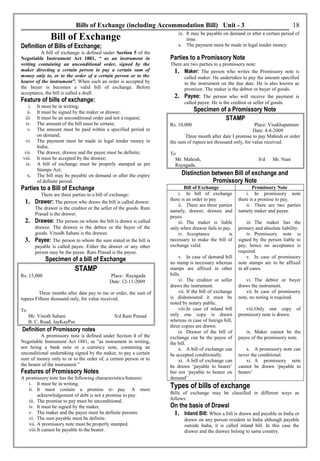

Specimen of a bill of Exchange

STAMP

Rs. 15,000 Place: Rayagada

Date: 12-11-2009

Three months after date pay to me or order, the sum of

rupees Fifteen thousand only, for value received.

To

Mr. Vinoth Sahani S/d Ram Prasad

B. C. Road, JayKayPur.

Definition of Promissory notes

A promissory note is defined under Section 4 of the

Negotiable Instrument Act 1881, as “as instrument in writing,

not being a bank note or a currency note, containing an

unconditional undertaking signed by the maker, to pay a certain

sum of money only to or to the order of, a certain person or to

the bearer of the instrument.”

Features of Promissory Notes

A promissory note has the following characteristics/features:

i. It must be in writing.

ii. It must contain a promise to pay. A mere

acknowledgement of debt is not a promise to pay.

iii. The promise to pay must be unconditional.

iv. It must be signed by the maker.

v. The maker and the payee must be definite persons.

vi. The sum payable must be definite.

vii. A promissory note must be properly stamped.

viii.It cannot be payable to the bearer.

18

ix. It may be payable on demand or after a certain period of

time.

x. The payment must be made in legal tender money.

Parties to a Promissory Note

There are two parties to a promissory note:

1. Maker: The person who writes the Promissory note is

called maker. He undertakes to pay the amount specified

in the instrument on the due date. He is also known as

promisor. The maker is the debtor or buyer of goods.

2. Payee: The person who will receive the payment is

called payee. He is the creditor or seller of goods.

Specimen of a Promissory Note

STAMP

Rs. 10,000 Place: Visakhapatnam

Date: 4-8-2009

Three month after date I promise to pay Mahesh or order

the sum of rupees ten thousand only, for value received.

To

Mr. Mahesh, S/d Mr. Nani

Rayagada.

Distinction between Bill of exchange and

Promissory Note

Bill of Exchange Promissory Note

i. In bill of exchange

there is an order to pay

ii. There are three parties

namely, drawer, drawee and

payee.

iii. The maker is liable

only when drawee fails to pay.

iv. Acceptance is

necessary to make the bill of

exchange valid.

v. In case of demand bill

no stamp is necessary whereas

stamps are affixed in other

bills.

vi. The creditor or seller

draws the instrument.

vii. If the bill of exchange

is dishonoured it must be

noted by notary public.

viii.In case of inland bill

only one copy is drawn

whereas in case of foreign bill,

three copies are drawn.

ix. Drawer of the bill of

exchange can be the payee of

the bill.

x. A bill of exchange can

be accepted conditionally.

xi. A bill of exchange can

be drawn ‘payable to bearer’

but not ‘payable to bearer on

demand’

i. In promissory note

there is a promise to pay.

ii. There are two parties

namely maker and payee.

iii. The maker has the

primary and absolute liability.

iv. Promissory note is

signed by the person liable to

pay, hence no acceptance is

required.

v. In case of promissory

note stamps are to be affixed

in all cases.

vi. The debtor or buyer

draws the instrument.

vii. In case of promissory

note, no noting is required.

viii.Only one copy of

promissory note is drawn.

ix. Maker cannot be the

payee of the promissory note.

x. A promissory note can

never the conditional.

xi. A promissory note

cannot be drawn ‘payable to

bearer’

Types of bills of exchange

Bills of exchange may be classified in different ways as

follows:

On the basis of Drawal

1. Inland Bill: When a bill is drawn and payable in India or

drawn on any person resident in India although payable

outside India, it is called inland bill. In this case the

drawer and the drawee belong to same country.

2. Bills of Exchange (including Accommodation Bill) Unit - 3

2. Foreign Bill: When a bill is drawn in one country and

payable in another country, it is called foreign bill,. In

this case the drawer and the drawee belong to two

different countries.

On the basis of Consideration

1. Trade Bill: When a bill is drawn in connection with a

genuine trade transaction such as sale of goods or

services, it is called trade bill.

2. Accommodation Bill: When a bill is drawn to help a

friend in his financial difficulty or for mutual benefit. It

is called accommodation bill. In this case the drawee

accepts the bill which is not supported by consideration.

Distinction between Trade Bill and Accommodation Bill

Trade Bill Accommodation Bill

1. Such bills are drawn for the

balance due in genuine

trade transaction.

2. The proceeds of discounted

bill is used by the drawer.

3. These bills are profit of

debt.

4. These bills are drawn for

consideration.

5. Legal action can be taken

by drawer against drawee

for the non-payment of bill

amount.

1. Such bills are drawn to help

a friend or for mutual

benefit.

2. The proceeds of discounted

bill is used by the drawer or

the drawee and drawer both.

3. These bills are not the proof

of debt.

4. These bills are drawn for no

consideration.

5. Legal action cannot be taken

by the drawer against

drawee for the non-payment

of bill amount.

On the basis of Time of Payment

1. Demand Bills: When a bill is payable on demand or at

sight (on presentation or on acceptance) it is called

demand bill.

2. Time Bill: When a bill is payable after the expiry of

certain period or on a specified date it is called time bill.

Such time bills may be further classified into:-

· After date bills: In case of after date bill, the

date of maturity of the bill is calculated from the

date of drawal.

· After sight bills: In case of after sight bill, the

date of maturity is calculated from the date of

acceptance of the bill.

Important Terms:

1. Terms of Bill: The time, after which the bill

becomes nominally, due is known as terms of bill. It is

also known as tenure of the bill.

2. Nominal Due Date: It is the date on which the

term of the bill expires.

3. Days of Grace: Three (3) days are allowed to the

drawee after the nominal due date to make payment of

bill amount. These three days are called ‘Days of Grace’.

4. Legal Due date or Date of Maturity: Date of

maturity is the date on which the payment of instrument

(bill of exchange of promissory note) falls due. If the

instrument is payable at a specified period after date, the

date of maturity is calculated from the date of its

drawing. But in case of after sight bills, maturity date is

calculated from the date of accepting the bill.

5. Hundis: Hundis are negotiable instruments written in

vernacular (Hindustani) language. They are usually

similar to bill of exchange. But sometimes they are in the

form of Promissory notes. Hundis are very popular in

India because they were in use by the Indian merchants

from the very old days.

6. Holder: A holder is a person who is entitled to the

possession of an instrument in his own name and

receives the amount from the parties associated. If a

person finds a negotiable instrument from the road or is

simply a thief, he cannot be called a holder because he is

not the legal owner of the instrument.

7. Holder in due course: A holder in due course is

a person who becomes possessor of the negotiable

instrument in good faith for valuable consideration

before the date of maturity. The holder in due course

enjoys certain privileges. The holder in due course gets a

better title than that of the transferor. Suppose, A’

transfers an instrument to ‘B’ which ‘A’ has obtained by

theft. If ‘B’ has obtained the instrument in good faith and

for consideration, B as a holder in due course can receive

payment on such instrument. The defective title of A

shall have no impact on the right of B to receive

payment.

8. Dishonour of Bill: if the drawee fails to meet the

bill on the date of maturity, the bill is said to be

dishonoured. When an endorsed bill is dishonoured, the

endorsee can recover the bill amount from the

draer/endorser. Similarly when a discounted bill is

dishonoured the banker has the right to recover the bill

amount from the drawer.

9. Notary Public, Noting and Noting

Charges: When a bill is dishonoured, it is preferable

to certify the dishonour by an officer called Notary

Public. He is the officer appointed by the Government to

give enquiry report on bill disputes. The party at whose

end the bill is dishonoured (drawer or Banker or

Endorsee) has to inform Notary Public about the matter.

The Notary Public investigates the matter and gives a

note regarding fact of dishonour, the date of dishonour,

the reason of dishonour, etc. on the back of the bill. This

is called Noting. If necessary, a separate paper called

‘allonge’ may be attached for that. For the noting on the

bill, the Notary Public charges some fee. Such fee is

called Noting Charges. Noting charges is paid initially

by the party at whose end the bill is dishonoured. But the

ultimate payer is the drawee. Noting charges is the

expense for the drawee.

10. Retirement of Bill: The drawer welcomes the

desire of the drawee to meet the bill before its maturity.

When the drawee desires to pay the amount before the

due date, the drawer allows him some discount for early

payment. Such discount is called rebate. This rebate is

equal to the interest on bill value for the unexpired

period of the bill at a given rate. The rebate is a loss to

the drawer and gain to the drawee. This process of

withdrawal of bill is called retirement of bill.

11. Renewal of Bill: Sometimes the drawee may have

financial difficulty in making payment of bill amount on

the due date. In this case, he may request the drawer to

give him some more time for the payment of dues. If the

drawer agrees with the proposal of drawee, the old bill is

cancelled / dishonoured and a new bill is drawn for the

extended period. This process is called Renewal of bill.

At the time of renewal, the drawer charges

interest for the extended period. This interest may be

paid by the drawee immediately in cash or it remains

due. If interest is paid in cash, the new bill is drawn for

the amount of old bill. If interest remains due the new

bill is drawn for the amount of old bill plus interest. In

some cases the drawee pays a part of amount due at the

time of renewal. Such part payment is taken into

consideration while calculating the interest and amount

of new bill.

12. Insolvency of drawee: Insolvency means the

inability to meet the liabilities. A person is called

19

3. Bills of Exchange (including Accommodation Bill) Unit - 3

insolvent if his liabilities exceed his assets. When the

drawee becomes insolvent and unable to meet his

liabilities including the bill amount, his properties are

sold and the sale proceeds is equitably distributed among

the creditors including the drawer. The unpaid portion of

dues is a loss (named as Bad Debts) for the drawer and it

is a gain (named as deficiency) for the drawee.

Practical Problems:

Trade Bill Honoured:

1. On 1-1-2009, Ram sold goods to Gopal for Rs. 8,000 for

which Ram drew on Gopal a bill for 4 months after date. It

was duly accepted by Gopal. Ram retained the bill till the

due date. The bill was duly honoured by Gopal at maturity.

Pass journal entries in the books of Ram and Gopal.

2. On 1-3-2009, Ram sold to Raghu goods of the value of Rs.

50,000 for which Ram drew a bill on Raghu for 2 months;

Raghu accepted the bill on 15-6-2009. On the due date, the

bill was honoured. Pass journal entries in the books of Ram

and Raghu.

3. Viswanath draws on Jagannath a bill of exchange for 2

months for Rs. 25,000 which Jagannath accepts on 1-4-

2009. the bill is discounted on 1-5-2009 for Rs. 24,900

Jagannath meets the bill on the due date. Pass journal

entries in the books of Viswanath and Jagannath.

4. Manoj owes to Saroj Rs. 10,000 for which be gives to Saroj,

a bill of exchange dated 10-3-2009 payable 3 months after

date. Saroj discounts the bill immediately at a discount of

Rs. 125. The bill is duly honoured on the due date. Pass

journal entries in the books of Manoj and Saroj.

5. On 1-1-2006 Kasinath draws a bill on Dwarikanath for Rs.

40,000 for 3 months Dwarikanath accepts the bill and

returns it to Kasinath. Pass journal entries in the books of

Kasinath in each of the following circumstances.

i. Kasinath retains the bill till the due date.

ii. Kasinath discounts the bill for Rs. 39,750.

iii. Kasinath endorses the bill in favour of Badrinath.

iv. Kasinath sends the bill to the banker for collection.

Assume that the bill dishonoured on the due date.

6. Naresh sells goods to Mahesh of the value of Rs. 15,000 on

1-3-2009. Mahesh accepts a bill dated 4-3-2009 payable 3

months after date. Naresh endorses the bill to Yogesh on

10-3-2009. The bill is duly met when due. Pass journal

entries in the books of naresh, Mahesh and Yogesh.

7. On 1-2-2009, Jayant sells to Susant goods valued at Rs.

30,000 and draws upon the latter two bills for Rs. 20,000

and Rs. 10,000, both payable 3 months after date. The bills

are duly accepted. The first bill is discounted on 10-2-2009

for Rs. 19905 and the second is endorsed to Hemant on 12-

2-2009. both the bills are honoured on the due date. Pass

journal entries in the books of Jayant, Susant and Hemant.

8. On 1-3-2009, Susma sold goods to Nilima for Rs. 10,000

and drew upon her a three months bill for the amount due.

Nilima accepted the bill. On 1-3-2009, Susma purchased

from Mamta goods worth Rs. 15,000 and endorsed Nilima’s

acceptance to Mamta along with a cheque for Rs. 4,750, Rs.

250 to be taken as discount. On the due date, the bill was

duly honoured. Pass journal entries in the books of all the

parties.

9. Sardha receives Madhav’s acceptance for Rs. 22,000 on 1-

3-2009 payable 3 months after date. It is sent to the bank for

collection. The bill is met by Madhav on the due date. Pass

journal entries in the books of both the parties.

10. Akash draws a bill on sun for Rs. 14,500. Sun accepts and

returns it to Akash. Akash endorses the bill in favour of

Moon, thereafter, endorses the bill in favour of Star. Star

discounts the bill for Rs. 13,900. Pass journal entries in the

books of all the parties, assuming that the bill is honoured at

maturity.

20

Bill Dishonoured

11. X sells goods to Y for Rs. 1,000 and draws a bill on Y on 1-

1-2009 for 4 months. On 4-1-2009, the bill is discounted by

X @ 10% p.a. At maturity, the bill is dishonoured Pass

journal entries in the books of X and y.

12. Geeta draws a bill on Bhagwat on 1-3-2009 for Rs. 18,000

for 3 months. Bhagwat accepts the bill and returns that to

Geeta. Geeta discounts the bill immediately @ 9% p.a. At

maturity, the bill is dishonoured and noting charges paid by

the banker Rs. 225. Pass journal entries in the books of

Geeta and Bhagwat.

13. A draws on a bill for Rs. 60,000 on 1-4-2009. The bill is

accepted by B payable 3 months after date. Show what

entries would be passed in the books of A under each of the

following circumstances:

i. If he retains the bill till the due date;

ii. If he discounts the same with the banker for Rs. 58950;

iii. If he endorse the same to his creditor C;

iv. If he sends the same to his banker for collection.

Assume that the bill is dishonoured at maturity.

14. A draws a bill B for Rs. 28,000. The bill is accepted by B.

Show what entries would be passed in the books of A under

each of the following circumstances

i. If he retains the bill till due date and then realizes it.

ii. If he discounts the same with his bankers for Rs. 27840;

iii. If he endorses the same to his creditor C;

iv. If he sends the same to his bankers for collection.

You assume:

· That the bill is met on the due date;

· That the bill is dishonoured on due date, no noting

charges being incurred.

15. X draws a bill on Y for Rs. 9,500. Y accepts and returns it

to X. X endorses the bill in favour of Z. Z, thereafter,

endorses the bill in favour of K. K discounts the bill for Rs.

9,550. At maturity, the bill is dishonoured and banker

paying for the noting charges Rs. 80. Pass journal entries in

the books of all the parties.

16. On 1-4-2009, Ganga draws on Yamuna a bill for Rs. 4,000

payable 2 months after date. Yamuna duly accepts the bill.

Ganga endorses the bill on 4-4-2009 to Saraswati, who

further endorses it over to Nagavali on 15-4-2009. Nagavali

discounts it with the banker on 18-4-2009 for Rs. 3,950.

The bill is dishonoured on the due date, the noting charges

paid by banker Rs. 70. Pass journal entries in the books of

all the parties.

17. On 1-4-2009, Yellow sold goods to Green for Rs. 50,000 on

credit. As per agreement between the parties. Yellow sold

goods to Green on 10-4-2009 for the amount due plus

interest @ 10% p.a., for 2 months. Green accepted the bill

on the same date. Yellow, thereafter, endorsed the bill in

favour of Brown on 1-5-2009. At maturity, the bill was

dishonoured and noting charges paid by Brown Rs. 100.

Pass journal entries in the books of Yellow, Green and

Brown.

Retirement of Bill

18. On 1st March, 2009 A sells goods to b valued at Rs. 8,500

and draws a Bill for 5 months for the same months for the

same. B accepts it and returned it to A. On 4th May, B

retires his acceptance under the rebate at 6% p.a. Give

Journal entries in the books of A and B.

19. On 1st February, 2009, Ram sells goods to Ramesh valued at

Rs. 1,500 and draws a bill for 4 months for the same.

Ramesh accepts it and returned it to Ram. Ram discounted

the bill @ 8% p.a. On 4th March, Ramesh retires his

acceptance under the rebate at 8% p.a. Give Journal entries

in the books of Ram and Ramesh.

20. On 1st January, 2009, X sells goods to y valued at Rs. 5,000

and draws a bill for 3 months for the same. Y accepts it and

returned it to X. X endorsed the bill to Z for the settlement

4. Bills of Exchange (including Accommodation Bill) Unit - 3

of dues. On 4th February, Y retires his acceptance under the

rebate at 7% p.a. Give journal entries in the books of X &

Y.

Renewal of the Bill

21. Brown sold goods to Smith on 1-1-2009 for Rs. 2000 and

drew a 4 months bill of exchange which Smith accepted. On

the due date, Smith requested that the bill be renewed for a

further period of 2 months with interest @ 12% p.a. Brown

agreed to this. Pass journal entries in the books of Brown

and Smith.

22. On 1-1-2009, Lotus sold to Lily goods of the value of Rs. 1,

00,000 and drew upon him a bill for 4 months for the

amount due. Lily accepted the bill. On the due date, Lily

expressed his inability to meet the bill and offered to pay

Rs. 30,000 in cash and to accept a new bill for the balance

plus interest @ 10 p.a., for 2 months. Lotus agreed to the

proposal. At maturity, the bill was duly honoured by Lily.

Pass journal entries in the books of Lotus and Lily.

23. For goods supplies, A draws a bill on B for Rs. 80,000 on 1-

3-2009 for 3 months. B accepts the bill and A discounts it

with the banker, paying Rs. 2000 as discounting charges.

On the due date, the banker presents the bill for payment to

B who is unable to meet it. B, then, meets the bill himself

after paying Rs. 500 for noting charges and B accepts

another bill for Rs. 81,750 due one month from the date of

maturity of the first bill. The second bill is duly met by B.

Pass journal entries in the books of A.

24. On 1st January, 2009, A sells goods to B on credit to the

value of Rs. 20,000 and draws a bill on him at three months

after date for the same amount B accepts the bill and returns

it to A on the same date. On 4th January, 2009. A discounts

the bill with his bank at 8% p.a. The acceptance is

dishonoured on the due date, the noting charges paid by

Bank being Rs. 150. On 5th April, 2009, B paid Rs. 5,000 in

cash and accepts a new bill for two months for the amount

due to A together with interest at 10% p.a. Give journal

entries to record the above transactions in the books of both

A & B.

25. On 1-1-2009, Chiranjivi sold goods to Anuska for Rs. 1,

00,000 and draws a bill on him for the same amount for 4

months. Anuska requests Chiranjivi to cancel the bill.

Instead, he wants to pay Rs. 30,000 immediately as part

payment and to accept a fresh bill for the balance plus

interest for a further period of 3 months from the due date of

the original bill. Chiranjivi agrees to the proposal. The new

bill is dishonoured on the due date. The rate of interest is

13% p.a. Pass journal entries in the books of Chiranjivi.

26. Bhism sold goods to Arjun for Rs. 5000 and draws a bill on

Arjun for the same amount. Before the due date. Arjun

requests Bhism to cancel the bill and a draws a fresh bill on

him. Bhism agrees to the proposal. Arjun pays Rs. 1000 in

cash and accepts a fresh bill for Rs. 4300 for a further

period of time. The new bill is dishonoured and Bhism pays

Rs. 50 as noting charges. Thereafter, Arjun becomes

insolvent and a dividend of 50 paise in the rupee is received

from her estate Pass journal entries in the books of

Lopamudra.

27. A bought goods from B on 15-1-2009 for Rs. 45,000 for

which he accepted a bill for 5 months drawn on him for Rs.

40,000 and paid Rs. 5000 by cheque. On 21-1-2009 B

discounted the bill @ 12% p.a. A, being unable to meet the

bill at maturity, requested B to accept Rs. 20,000 in cash

and to draw another bill for 2 months for the balance sum

plus interest at 15% p.a. and B agreed. But before the

maturity of the second bill. A became insolvent and a

dividend of 75 paise in the rupee was realized from his

estate on 30-11-2009. Pass the necessary Journal entries in

the books of B.

Accommodation Bill

28. For mutual accommodation Abdul accepts a bill for Rs.

32000 for 4 months draws on him on 1st January, 2009 by

Babul, Babul discounts the bill on the same date for R.

31500 and sends 50% of the proceeds to Abdul. Before the

bill becomes due Babul remits the balance to Abdul

wherewith the latter meets the bill on due date. You are

required to give the journal entries in the books of Abdul

and Babul to record the above transactions.

29. Rohit and Mohit for their mutual accommodation draw on

each other on 1st March 2009, at three months for Rs.

17000. They discounted their respective bills after

acceptance on the same date at 12%. On due date they

honour their bill by payment. Give the journal entries in the

books of both the parties to record the above transaction.

30. Grass draws a bill for Rs. 6,000 and Blade accepts the same

for mutual accommodation of both in the ratio 2:1. Grass

discounts the same for Rs. 5,640 and remits 1/3rd of the

proceeds to Blade. Before due date Lade draws another bill

for Rs. 8,400 on Grass is order to provide funds to meet the

bill. The second bill is discounted for Rs. 8160 by Blade

and a sum of Rs. 1,440 is remitted, to Grass after meeting

the first bill. The second bill is duly met. Show the account

in the books of both Grass and Blade.

31. On 1st January, 2009, Rose drew a bill on Lily for Rs.

50,000 and Lily drew a bill on Rose for similar amount,

both the bills being due after 4 months. Both the bills were

discounted at the bank at 12%. On maturity, Lily met his

bills. But Rose notified Lily of his inability to meet the bill

and Rose therefore, accepted a bill drawn on him by lily at

three months after date from the due date. Pass journal

entries in the books of both the parties.

32. A draws a bill for Rs. 13,500 on B on 2nd January, 2009 for

three months. A get it discounted with bank for Rs. 13,230

and remits one third of the amount to B. on the due date, A

fails to remit the amount due to B but the accepts a bill for

Rs. 18,900 for three months which B discounts for Rs.

18495 and remits Rs. 3,330 to A. before the maturity of the

renewed bill, A becomes insolvent and only 60% was

realized from his estate on July, 10th. Pass journal entries in

the books of A.

33. Mitu for the mutual accommodation of himself and Tutu to

the extent of 2/3 rd and 1/3rd respectively, draws on the

latter a bill for Rs. 15,000 payable after one month. The bill

being accepted by Tutu. Before the due date. Tutu in order

to provide funds to meet the first bill draws another bill for

Rs. 21,000 on Mitu. The second bill is discounted by Tutu

for Rs. 20,400 with the help of which he meets the first bill

and remits Rs. 3,600 to Mitu. Before the due date, Mitu

becomes bankrupt and tutu receives first and final dividend

of 75 paise in the rupee. Pass the necessary journal entries

in the books of Mitu and Tutu.

34. Durga for mutual accommodation draws a bill for Rs.

21,000 on Devi. Durga discounts the bill for Rs. 20,475 and

remits Rs. 6,825 to Devi. On the due date Durga is unable

to remit his dues to Devi to enable her to meet the bill. She,

however, accepts a bill for Rs. 26,250 which Devi discounts

for Rs. 24,675. Devi sends Rs. 1,235 to Durga. Durga

becomes insolvent and a dividend of 50 paisa in the rupee is

received from her estate. Pass journal entries and show the

account of Devi in the books of Durga.

21