Internal audit checklist process purchasing category exicise

•Download as DOC, PDF•

1 like•2,043 views

Internal audit checklist process purchasing category exicise

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Internal audit checklist process purchasing category exicise

Similar to Internal audit checklist process purchasing category exicise (20)

Recently uploaded

Recently uploaded (20)

Internal audit checklist process purchasing category exicise

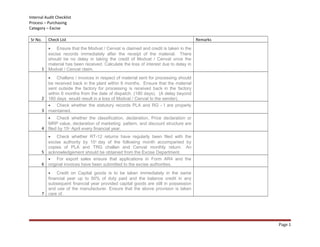

- 1. Internal Audit Checklist Process – Purchasing Category – Excise Sr No. Check List Remarks 1 • Ensure that the Modvat / Cenvat is claimed and credit is taken in the excise records immediately after the receipt of the material. There should be no delay in taking the credit of Modvat / Cenvat once the material has been received. Calculate the loss of interest due to delay in Modvat / Cenvat claim. 2 • Challans / invoices in respect of material sent for processing should be received back in the plant within 6 months. Ensure that the material sent outside the factory for processing is received back in the factory within 6 months from the date of dispatch. (180 days). (A delay beyond 180 days would result in a loss of Modvat / Cenvat to the sender). 3 • Check whether the statutory records PLA and RG - I are properly maintained. 4 • Check whether the classification, declaration, Price declaration or MRP value, declaration of marketing pattern, and discount structure are filed by 15th April every financial year. 5 • Check whether RT-12 returns have regularly been filed with the excise authority by 10th day of the following month accompanied by copies of PLA and TRG challan and Cenvat monthly return. An acknowledgement should be obtained from the Excise Department. 6 • For export sales ensure that applications in Form AR4 and the original invoices have been submitted to the excise authorities. 7 • Credit on Capital goods is to be taken immediately in the same financial year up to 50% of duty paid and the balance credit in any subsequent financial year provided capital goods are still in possession and use of the manufacturer. Ensure that the above provision is taken care of. Page 1

- 2. Internal Audit Checklist Process – Purchasing Category – Excise 8 • Further the cenvat credit is allowed even if the goods (Input / Capital) are acquired by the manufacturer on lease, hire purchase or loan agreement from a financing company. The credit is not allowed if the manufacturer claims depreciation under Section 32 of the Income Tax Act on the amount of duty paid. Check whether the above provisions have been considered while considering the Modat / Cenvat Credit. 9 • The Excise law / rules should be referred from time to time as the provisions change every year. 10 • Ensure that full Credit for Modvat / Cenvat / PLA has been taken by 20th of every month in respect of duty debited for despatches made during 10/15th day of the month and full credit is taken by the 5th of the next month in respect of duty debited for dispatches made between 16th to 30/31st of the month. Ensure that there is no lapse on this account and that the duty credited is equivalent to the duty debited on fortnightly basis. 11 • Ensure that Cenvat account debit should be limited to the Credit balance available on the 15th day and the last day of the month respectively. Page 2