+97470301568>>buy weed in qatar,buy thc oil in qatar doha>>buy cannabis oil i...

Qatari Banks Lead Asset and Loan Growth

1. QNB Economics

economics@qnb.com

February 23, 2014

Weekly Commentary

Qatari Banks Lead Asset and Loan Growth in the GCC

In Qatar, higher lending associated with large

infrastructure projects, a low cost of funding

and foreign acquisitions have all supported

banks’ growth. Loan growth in Qatar was 23%

in 2013. With the acceleration of investment

projects ahead of the 2022 FIFA World Cup,

these trends are likely to continue going

forward. Meanwhile, deposit growth continued

at a rapid pace, rising by around 24% in 2013,

with the public sector being the key driver for

overall gains, reflecting the large fiscal

surplus. Higher lending, a low cost base and

low provisioning requirements have all

supported the banks’ overall profitability, with

a return on equity of 16.0% in 2013.

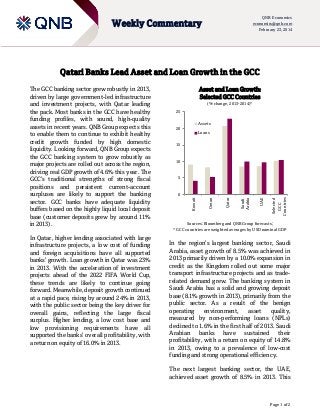

Asset and Loan Growth:

Selected GCC Countries

(% change, 2013-2014)*

25

Assets

20

Loans

15

10

5

Selected

GCC

Countries

UAE

Saudi

Arabia

Qatar

Oman

0

Kuwait

The GCC banking sector grew robustly in 2013,

driven by large government-led infrastructure

and investment projects, with Qatar leading

the pack. Most banks in the GCC have healthy

funding profiles, with sound, high-quality

assets in recent years. QNB Group expects this

to enable them to continue to exhibit healthy

credit growth funded by high domestic

liquidity. Looking forward, QNB Group expects

the GCC banking system to grow robustly as

major projects are rolled out across the region,

driving real GDP growth of 4.6% this year. The

GCC’s traditional strengths of strong fiscal

positions and persistent current-account

surpluses are likely to support the banking

sector. GCC banks have adequate liquidity

buffers based on the highly liquid local deposit

base (customer deposits grew by around 11%

in 2013).

Sources: Bloomberg and QNB Group forecasts;

* GCC countries are weighted averages by USD nominal GDP

In the region’s largest banking sector, Saudi

Arabia, asset growth of 8.5% was achieved in

2013 primarily driven by a 10.0% expansion in

credit as the Kingdom rolled out some major

transport infrastructure projects and as traderelated demand grew. The banking system in

Saudi Arabia has a solid and growing deposit

base (8.1% growth in 2013), primarily from the

public sector. As a result of the benign

operating

environment,

asset

quality,

measured by non-performing loans (NPLs)

declined to 1.6% in the first half of 2013. Saudi

Arabian

banks

have sustained their

profitability, with a return on equity of 14.8%

in 2013, owing to a prevalence of low-cost

funding and strong operational efficiency.

The next largest banking sector, the UAE,

achieved asset growth of 8.5% in 2013. This

Page 1 of 2

2. Weekly Commentary

was driven by strong growth in lending to the

government (around 11%). Credit to private

sector companies and households expanded

moderately (5%). However, lending to the real

estate sector was flat as the government

introduced macro-prudential lending limits to

help prevent overexposure to the real estate

market, particularly in Dubai where property

prices rose 26% in 2013. Overall improvements

in asset quality with NPLs of 9.4% witnessed

in the first half of 2013 drove down loan-loss

provisions which in turn have supported UAE

banks’ return on equity of 12.6% last year.

Kuwait's banking sector continues to remain

moderate, supported by high oil revenues and

government spending. The banking system

continues to remain heavily deposit funded

and benefits from access to government

related deposits. As a result, banking sector

asset growth was 9.0% in 2013. Moderate

credit growth and margin pressures have

constrained revenue growth and thus return

on equity fell to 5.6% in 2013 from 6.6% in

2012. Kuwaiti banks have made considerable

progress in rehabilitating their loan books

following the 2008-09 crisis, and this along

with the healthy operating environment, has

meant that NPLs fell to 3.9% in the third

quarter of last year.

QNB Economics

economics@qnb.com

February 23, 2014

The banking system in Oman remained benign

in 2013 reflecting stable macroeconomic

conditions that have supported low NPLs

(2.2% in the third quarter of 2013), healthy

levels of capitalization and a stable deposit

funding base. Prospects for Omani asset

growth have been sound on the back of the

increase in government spending on

infrastructure – asset growth was an

estimated 8.2% in 2013. In addition, Omani

banks have maintained solid profitability with

a return on equity of 13.1% in 2013.

Furthermore, high government spending has

boosted bank lending in recent years (up 5.2%

in 2013), and a favorable economic

environment will continue to support bank

credit conditions and create lending

opportunities going forward.

Looking ahead, the GCC’s positive economic

growth

outlook,

supported

by

high

hydrocarbon prices and strong government

spending, is expected to support the continued

expansion of the regional banking sector, with

Qatar leading the way.

Contacts

Joannes Mongardini

Head of Economics

Tel. (+974) 4453-4412

joannes.mongardini@qnb.com.qa

Rory Fyfe

Senior Economist

Tel. (+974) 4453-4643

rory.fyfe@qnb.com.qa

Ehsan Khoman

Economist

Tel. (+974) 4453-4423

ehsan.khoman@qnb.com.qa

Hamda Al-Thani

Economist

Tel. (+974) 4453-4646

hamda.althani@qnb.com.qa

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend

on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a

complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.

Page 2 of 2