Mysore Call Girls 8617370543 WhatsApp Number 24x7 Best Services

24 June Daily market report

1. Page 1 of 7

QE Intra-Day Movement

Qatar Commentary

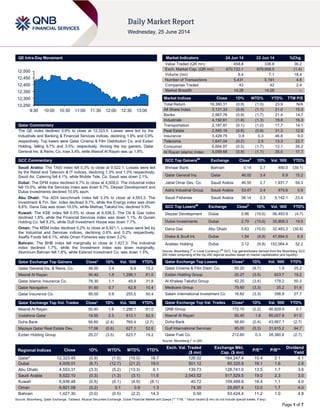

The QE index declined 0.9% to close at 12,323.5. Losses were led by the

Industrials and Banking & Financial Services indices, declining 1.9% and 0.9%

respectively. Top losers were Qatar Cinema & Film Distribution Co. and Ezdan

Holding, falling 9.7% and 3.5%, respectively. Among the top gainers, Qatar

General Ins. & Reins. Co. rose 3.4%, while Masraf Al Rayan was up 1.8%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.3% to close at 9,522.1. Losses were led

by the Retail and Telecom & IT indices, declining 1.3% and 1.0% respectively.

Saudi Air. Catering fell 4.1%, while Mobile Tele. Co. Saudi was down 2.1%.

Dubai: The DFM index declined 6.7% to close at 4,009.0. The Industrial index

fell 10.0%, while the Services index was down 9.7%. Deyaar Development and

Dubai Investments declined 10.0% each.

Abu Dhabi: The ADX benchmark index fell 3.3% to close at 4,553.3. The

Investment & Fin. Ser. index declined 9.7%, while the Energy index was down

8.6%. Dana Gas was down 10.0%, while Methaq Takaful Ins. declined 9.9%.

Kuwait: The KSE index fell 0.5% to close at 6,936.5. The Oil & Gas index

declined 1.8%, while the Financial Services index was down 1.1%. Al Qurain

Holding Co. fell 8.3%, while Gulf Investment House was down 7.7%.

Oman: The MSM index declined 0.2% to close at 6,921.1. Losses were led by

the Industrial and Services indices, declining 0.6% and 0.2% respectively.

Asaffa Foods fell 6.1%, while Oman Fisheries was down 3.2%.

Bahrain: The BHB index fell marginally to close at 1,427.3. The Industrial

index declined 1.7%, while the Investment index was down marginally.

Aluminum Bahrain fell 1.8%, while Esterad Investment Co. was down 1.5%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar General Ins. & Reins. Co. 46.00 3.4 6.9 15.2

Masraf Al Rayan 50.40 1.8 1,298.1 61.0

Qatar Islamic Insurance Co. 76.30 1.1 49.9 31.8

Qatar Navigation 91.60 0.7 62.8 10.4

Qatar Insurance Co. 80.00 0.6 255.5 50.4

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Masraf Al Rayan 50.40 1.8 1,298.1 61.0

Vodafone Qatar 19.55 0.3 813.1 82.5

Doha Bank 56.60 (2.4) 765.4 (2.7)

Mazaya Qatar Real Estate Dev. 17.06 (0.6) 627.1 52.6

Ezdan Holding Group 20.27 (3.5) 623.7 19.2

Market Indicators 24 Jun 14 23 Jun 14 %Chg.

Value Traded (QR mn) 458.8 336.8 36.2

Exch. Market Cap. (QR mn) 670,722.1 679,958.5 (1.4)

Volume (mn) 8.4 7.1 18.4

Number of Transactions 5,431 5,191 4.6

Companies Traded 43 42 2.4

Market Breadth 14:28 14:26 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,380.31 (0.9) (1.0) 23.9 N/A

All Share Index 3,131.33 (0.9) (1.1) 21.0 15.0

Banks 2,967.76 (0.9) (1.7) 21.4 14.7

Industrials 4,192.61 (1.9) (1.3) 19.8 16.3

Transportation 2,187.87 (0.1) (1.0) 17.7 14.1

Real Estate 2,565.19 (0.8) (0.9) 31.3 12.8

Insurance 3,429.75 0.9 0.3 46.8 9.0

Telecoms 1,647.04 (0.2) 2.5 13.3 22.7

Consumer 6,664.87 (0.5) (1.7) 12.1 26.2

Al Rayan Islamic Index 4,099.68 (0.9) (1.7) 35.0 17.7

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ithmaar Bank Bahrain 0.14 3.7 490.0 (39.1)

Qatar General Ins. Qatar 46.00 3.4 6.9 15.2

Jabal Omar Dev. Co. Saudi Arabia 46.50 2.7 1,931.7 59.3

Astra Industrial Group Saudi Arabia 53.47 2.4 475.6 0.9

Saudi Fisheries Saudi Arabia 38.14 2.3 5,142.1 23.4

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Deyaar Development Dubai 0.96 (10.0) 56,493.9 (4.7)

Dubai Investments Dubai 2.79 (10.0) 35,908.3 19.9

Dana Gas Abu Dhabi 0.63 (10.0) 32,493.3 (30.8)

Drake & Scull Int. Dubai 1.54 (9.9) 47,894.5 6.9

Arabtec Holding Dubai 3.12 (9.8) 152,064.4 52.2

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distri. Co. 50.20 (9.7) 1.9 25.2

Ezdan Holding Group 20.27 (3.5) 623.7 19.2

Al Khaleej Takaful Group 42.20 (3.4) 178.2 50.3

Medicare Group 79.60 (3.3) 25.2 51.6

Salam International Investment Co 16.62 (3.3) 356.9 27.7

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

QNB Group 172.10 (2.2) 66,829.9 0.1

Masraf Al Rayan 50.40 1.8 65,027.9 61.0

Doha Bank 56.60 (2.4) 43,667.1 (2.7)

Gulf International Services 95.00 (0.3) 31,615.2 94.7

Qatar Fuel Co. 212.60 0.3 28,380.8 (2.7)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,323.45 (0.9) (1.0) (10.0) 18.7 126.02 184,247.4 15.4 2.1 4.1

Dubai 4,009.01 (6.7) (12.7) (21.2) 19.0 501.12 80,325.9 16.1 1.6 2.6

Abu Dhabi 4,553.31 (3.3) (5.2) (13.3) 6.1 139.73 128,741.0 13.5 1.7 3.6

Saudi Arabia 9,522.10 (0.3) (1.3) (3.1) 11.6 2,043.52 517,529.5 19.0 2.3 3.0

Kuwait 6,936.48 (0.5) (0.1) (4.9) (8.1) 40.72 109,489.8 16.4 1.1 4.0

Oman 6,921.08 (0.2) 0.1 0.9 1.3 74.30 25,697.4 12.0 1.7 4.0

Bahrain 1,427.30 (0.0) (0.5) (2.2) 14.3 0.50 53,424.4 11.2 1.0 4.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,250

12,300

12,350

12,400

12,450

12,500

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QE index declined 0.9% to close at 12,323.5. The Industrials

and Banking & Financial Services indices led the losses. The

index fell on the back of selling pressure from non-Qatari

shareholders despite buying support from Qatari shareholders.

Qatar Cinema & Film Distribution Co. and Ezdan Holding Group

were the top losers, falling 9.7% and 3.5%, respectively. Among

the top gainers, Qatar General Insurance & Reinsurance Co.

rose 3.4%, while Masraf Al Rayan was up 1.8%.

Volume of shares traded on Tuesday rose by 18.4% to 8.4mn

from 7.1mn on Monday. However, as compared to the 30-day

moving average of 24.0mn, volume for the day was 65.0% lower.

Masraf Al Rayan and Vodafone Qatar were the most active

stocks, contributing 15.4% and 9.7% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Al Bayan Holding

Group

RAM

Saudi

Arabia

LT CCR/ST CCR AA3/P1 AA3/P1 – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency, CCR – Corporate Credit Ratings)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

06/24 US FHFA FHFA House Price Index MoM April 0.00% 0.50% 0.70%

06/24 US S&P/Case-Shiller S&P/CS 20 City MoM SA April 0.19% 0.80% 1.25%

06/24 US S&P/Case-Shiller S&P/CS Composite-20 YoY April 10.82% 11.50% 12.37%

06/24 US S&P/Case-Shiller S&P/CaseShiller Home Price Index NSA April 168.71 169.09 166.8

06/24 US Conference Board Consumer Confidence Index June 85.2 83.5 82.2

06/24 US Richmond Fed Richmond Fed Manufact. Index June 3.0 7.0 7.0

06/24 Germany IFO Institute IFO Business Climate June 109.7 110.3 110.4

06/24 Germany IFO Institute IFO Current Assessment June 114.8 115.0 114.8

06/24 Germany IFO Institute IFO Expectations June 104.8 106.0 106.2

06/24 UK BBA BBA Loans for House Purchase May 41,757 41,000 41,934

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QNBK: Global exports fall on weak EM demand – The QNB

Group (QNBK) said that world exports are stalling on a weak

global recovery. According to data released last week by the

World Trade Organization (WTO), world merchandise export

volumes declined by 1.0% in the fourth quarter of 2013

compared to the previous quarter on a seasonally-adjusted

basis. This represents the largest quarterly decline since the

Great Recession of 2008-09. Weak export demand from

emerging markets (EMs) and sluggish growth in advanced

economies (AEs) are the main factors behind this large decline.

Unless world export growth picks up again, the global recovery

is likely to falter in 2014. (Gulf-Times.com)

MDPS: Qatari economy expected to grow 6.3% in 2014,

7.8% in 2015 – According to the Ministry of Development

Planning & Statistics (MDPS), Qatar is expected to report solid

economic growth in 2014 and 2015, driven by the non-

hydrocarbon sector owing to accelerated investment spending

and population growth. The country’s real GDP (adjusted for

inflation) is slated to grow 6.3% in 2014 from 6.5% in 2013, and

7.8% in 2015, said the Qatar Economic Outlook (QEO) 2014-15,

which was released by MDPS. HE the Minister of Development

Planning and Statistics Dr. Saleh Mohamed Salem al-Nabit said

that the impulse to growth from hydrocarbon production in past

years is receding, and growth is increasingly dependent on solid

performance of the other sectors. According to the QEO, output

from the hydrocarbon sector is set to shrink 2.5% in 2014 largely

due to declining production from maturing oil fields. Gas output

is expected to remain largely unchanged in 2014, having

saturated in 2013. Flat gas production and receding oil output

are expected to check overall growth in 2014, but with the

commissioning of the Barzan gas project in 2015, the gas output

is anticipated to increase, taking the aggregate growth higher.

Also, the construction activity is projected to expand 14.1% in

2014, up from 13.6% in 2013, and may well accelerate a shade

faster in 2015. The QEO added that the main driver is the

government’s heavy investments in economic infrastructure,

especially local roads, expressways, the Doha metro & rail, and

drains & sanitation at a pace that is likely to pick up over 2014

and 2015. (Gulf-Times.com)

MDPS: Domestic demand to heighten inflationary pressures

– According to the MDPS, domestic inflationary pressures are

expected to heighten over the remainder of 2014 and in 2015 on

strong domestic demand. As per the MDPS’ QEO 2014-15,

annual inflation, as measured by the change in the consumer

price index, is expected to average 3% in 2014, similar to 2013’s

outcome, and increase modestly to 3.4% in 2015. However, the

Overall Activity Buy %* Sell %* Net (QR)

Qatari 55.81% 47.95% 36,073,767.78

Non-Qatari 44.19% 52.05% (36,073,767.78)

3. Page 3 of 7

QEO added that the moderate inflation in 1H2014 will restrain

the year’s average, and a benign global inflation outlook will help

offset domestic sources of inflationary pressures over the near-

term. (Gulf-Times.com)

Qatar’s CA surplus slated to fall; forex reserves to cover 6.5

months of imports – According to official estimates, Qatar’s

current account (CA) surplus is slated to fall in 2014 and 2015

but remain sizeable at 25.1% and 19.5% of GDP. Foreign

exchange reserves are adequate to cover more than 6.5 months

of imports. The MDPS also expects Qatar’s fiscal surplus to

narrow to 9.3% of the GDP and then to fall to 5.5% in 2015,

down from a preliminary estimate of a 12.9% surplus in 2013.

MDPS said in its QEO 2014-15 that the shrinkage is owing to a

combination of expenditure growth, as the public investment

program gathers pace, and the expected decline in hydrocarbon

revenue. (Gulf-Times.com)

Woqod in process of finalizing its five year plan 2014-2018 –

Woqod’s (QFLS) CEO, Ibrahim Jaham Al - Kuwari, revealed the

main features of its upcoming five years plan (2014 - 2018). The

plan which is in its final stages of preparations is in line with the

Qatar’s National Vision 2030 and the huge modernization and

development efforts at the various levels in Qatar, and in

preparation for the upcoming global event, World Cup 2022, to

be hosted by Qatar. The plan emphasizes on expanding the

current stations, addition of new technical centers, developing

and modernizing infrastructure for Q-JET, expanding the

operational capacity of WOQOD Marine Services' fleet by

increasing the number of new vessels ( expected to reach 8-10

vessels by the end of 2018 from the current five vessels), and

investing QR70mn to expand the storage facilities at Mesaieed

area and increase its operational capacity to exceed 20,000

metric tons of Bitumen to deal with the new demand during the

coming five years. (QE)

Woqod to import 300,000 Shafaf cylinders – Woqod’s (QFLS)

CEO Ibrahim Jaham Al-Kuwari said that some 300,000

transparent (Shafaf) cooking gas cylinders are being imported to

help ease their shortage ahead of Ramadan. Orders for the

supply of the cylinders have already been placed with the

exporters, local petroleum products distributor and cooking gas

supplier. A top QFLS official said that the corporation is

encouraging ‘Shafaf’ retailers to accept metal cylinders from

buyers in exchange (for the new cylinder) and give them a

discount of QR50. (Peninsula Qatar) first page

Qatar, ICANN sign MoU on supporting cooperation in

internationalized domain names – Qatar’s Ministry of

Information & Communications Technology (MICT) and the

Internet Corporation for Assigned Names and Numbers (ICANN)

have signed a MoU to cooperate with the aim of supporting the

development of the domain name industry and internationalized

domain names (such as those in Arabic script) in the region, as

well as to promote the multi-stakeholder model of internet

governance. The agreement also calls for the collaboration in

joint projects & activities in areas related to ICANN's mission

and mandate. (Bloomberg)

QE suspends QIGD share trading on June 25, to disclose

1H2014 results on July 9 – The Qatar Exchange (QE) has

announced trading suspension of Qatari Investors Group’s

(QIGD) shares on June 25, 2014 due to the latter’s scheduled

EGM on that day. Meanwhile, QIGD announced that the

company will disclose the financial reports for the period ending

June 30, 2014 on July 9, 2014. (QE)

IHGS to disclose results on July 09, 2014 – Islamic holding

Group (IHGS) will disclose the financial reports for the period

ending June 30, 2014 on July 9, 2014. (QE)

Realty transactions worth over QR800mn between June 15-

19 – The real estate registration department at the Ministry said

that the real estate transactions between June 15 and 19 for the

real estate sales contracts registered at the Ministry of justice

are worth QR811.8mn. The list of properties that were traded by

sale includes open plots of land, two floors villas, annexes,

houses and residential buildings which are located in the

municipalities of Umm Salal, Al Khor, Al Dhakira, Doha, Al

Rayyan, Al Shamal, Al Daayen and Al Wakra. (Bloomberg)

International

Consumer confidence, housing data bolster US growth

outlook – US consumer confidence jumped to its highest level

in nearly 6-1/2 years in June, while sales of new homes surged

in May, indicating latest signs that the economy has regained

momentum. Growth is accelerating after crumbling in the first

quarter, but Tuesday's robust reports are likely to exaggerate

strength. Nevertheless, they added to data on employment,

factory and services sector activities suggesting a sharp growth

rebound. The Conference Board said its consumer confidence

index rose to 85.2, the highest reading since January 2008, from

82.2 in May as households grew more optimistic about the labor

market. However, the reading was at odds with another survey

published last week, which showed consumer sentiment ticking

down in early June. Still, economists said it was in line with other

data showing an improvement in job market conditions. In

another report, the Commerce Department said new home sales

vaulted 18.6 percent to a seasonally adjusted annual rate of

504,000 units, the highest level since May 2008. (Reuters)

Fed grants four banks more time to resubmit capital

distribution plans – The US Federal Reserve gave four banks

more time to resubmit capital distribution plans it had earlier

objected to, saying this would give the firms more time to

address capital planning weaknesses. The four banks, which

had asked for the extension, are Citigroup Inc. (C.N), HSBC

North America Holdings, Inc. (HSBA.L), RBS Citizens, Inc.

(RBS.L) and Santander Holdings USA, Inc. (SAN.MC). These

banks were originally scheduled to submit their plans by June

26, but now have time until January 5, 2015 to carry out the

same. The firms will not be able to raise their capital

distributions to shareholders, such as dividends and share buy-

backs, until the new plans are approved. Citigroup Chief

Executive Mike Corbat has said that the bank would not make a

new request this year for permission to buy back stock and pay

more dividends. Instead, the bank would focus on preparing its

application for next year’s scheduled review of its capital plan.

(Reuters)

Fed's Dudley sees mid-2015 rate hike as 'reasonable' – An

influential Fed policymaker said the US Federal Reserve can

reasonably wait to raise interest rates until mid-2015 without

risking an undesirable rise in inflation. President of the New York

Federal Reserve Bank, William Dudley said they can get the

unemployment rate considerably lower and still not have an

inflation problem. The US jobless rate stood at 6.3% in May, the

lowest level since the end of 2008, and unchanged from April.

Inflation has been running below the Fed's 2% goal, although

some recent readings have been firmer. Dudley added that the

market is expecting the Federal Reserve to raise short-term

interest rates around the middle of 2015, which according to him

sounds like a reasonable forecast, but added that forecasts

often go astray. (Reuters)

Insee: French GDP Growth to Miss Hollande’s Target in

2014 – The French economy will expand less than President

Francois Hollande’s government expects this year and

unemployment will climb as consumer spending and exports fail

4. Page 4 of 7

to accelerate, the national statistics office predicted. Insee said

the GDP will grow 0.7% in 2014. The government is counting on

growth of 1% to help fulfill its promise of reducing the budget

deficit to 3.8% of GDP. Insee stated that the purchasing power

of households has improved, of course, but too modestly to

bring a real acceleration in spending. Faced with low demand

and low margins, companies are not inclined to invest and

French exports will not fully benefit from the improved world

trade. The remarks show how Hollande is struggling to revive

Europe’s second-largest economy after two years in office. The

Socialist president has pledged to cut public spending by €50bn

over the next three years and halt tax increases in an effort to

bolster confidence and investment. So far, the business

sentiment has failed to improve. The Bank of France’s index of

manufacturing sentiment fell to 97 from 98 in May, while the

Markit Economics Purchasing Managers Index for services and

industries declined to 47.8 this month from 49.6. The national

statistics office predicts that unemployment will continue to climb

in the second half of 2014, reaching 10.2% by the end of the

year. (Bloomberg)

Japan PM Abe says 'positive cycle' emerging in economy;

urges businesses to mobilize women power for economy –

Japanese Prime Minister Shinzo Abe said that a "positive cycle"

was appearing in the country's economy as rising corporate

revenues led to higher wages and household income. But Abe

said the recovery has yet to reach broader sectors of the

economy, stressing the need to ensure the positive economic

cycle does not end up as a temporary phenomenon. He said the

mandate of 'Abenomics' is to make people across Japan feel the

benefits of the economic recovery. Meanwhile, Abe urged the

nation's business leaders to do more to boost the role of working

women, a key plank of a new growth strategy he was set to

unveil later in the day. Abe, who took office 18 months ago

pledging to end deflation and generate sustainable growth with a

three-pronged strategy of monetary easing, fiscal spending and

reform, is due to outline the latest tranche of his so-called "Third

Arrow" of long-term economic policies. The package will include

steps to boost the role of working women - seen as vital to

address the shrinking workforce in one of the world's most

rapidly aging societies. In a meeting with business executives,

Abe urged companies to set targets for promoting female

workers to senior jobs and disclose information on progress in

annual earnings reports. He also said the government would

make necessary legal changes to promote female participation

in the workforce in central and local governments, as well as in

the private sector. (Reuters)

S&P's Kraemer: Eurozone countries have much to do to cut

debt, boost growth – A senior Standard & Poor’s(S&P) official

said Eurozone countries still have much work to do to cut debt &

boost growth and their credit ratings are unlikely to rise until they

get their economies in better shape. S&P's head of sovereign

ratings for Europe, Middle East and Africa, Moritz Kraemer said

that he saw a "calm period ahead" for ratings actions in Europe.

He stated that much of the homework still needs to be done.

The over-indebtedness in a very low inflation environment poses

huge risks to the growth outlook for the Eurozone. There is no

need to raise the ratings until the (economic) fundamentals

improve. Kraemer added that the countries that had made most

progress in cutting debts included Ireland & Spain, and both had

seen their ratings upgraded. (Reuters)

PBOC: A flexible Yuan can help China cope with bigger

capital flows – A senior researcher at the People's Bank of

China (PBOC) said China needs to make the Yuan more flexible

to cope with possible rises in capital flows. Ma Jun, the chief

economist at the central bank's research bureau, told a forum

that China's net capital flows may not be as big as some expect

once the country frees its closed capital account. However, he

said capital inflows into China’s bond market could increase as

domestic bond yields are higher relative to overseas markets.

This provides an arbitrage opportunity for investors compared

with the Yuan, which has limited scope to move. Ma also added

that as China's capital account is already partially open, there

could be "a substantial increase" in outbound foreign direct

investment (FDI) if China further loosens its grip on capital flows.

(Reuters)

Regional

OPEC sees no shortage of oil; Saudi Arabia ready to pump

extra supplies – The OPEC is ready to pump extra oil in the

event of any supply disruptions caused by Iraq and its biggest

producer, Saudi Arabia, can ramp up to capacity if needed. The

OPEC Secretary General Abdullah al-Badri said that for now the

market is well-supplied and prices above $114 a barrel are the

result of market nervousness. An official from Saudi Arabia, the

only OPEC member with significant spare capacity, said it was

committed to supplying the market if needed. Saudi Arabia,

which produces around 9.7mn bpd, has the ability to pump to its

full capacity of 12.5mn bpd. The OPEC earlier this month

agreed to keep its output ceiling unchanged at 30mn bpd. Since

then, concerns that violence in Iraq could disrupt supplies have

stoked volatility and driven international benchmark Brent above

$114 a barrel. Disruption in Iraq would aggravate the impact of

outages in Libya, Syria and sanctions on Iran, which have

already curbed production by almost 3mn bpd, or more than 3%

of daily global demand. (Gulf-Times.com)

SGPB appoints new CEO for MidEast – France-based Societe

Generale Private Banking (SGPB) – the wealth management

arm of Societe Generale Group – has appointed Gonzague de

Cerval as the Chief Executive Officer and Commercial Director

for Middle East. (Bloomberg)

Petrochem completes SR1.2bn Sukuk issue – Saudi Arabia’s

National Petrochemical Company (Petrochem) has completed a

SR1.2bn debut Sukuk issue. The Islamic bond, which has a five-

year lifespan, was priced at 170 basis points over the six-month

Saudi interbank offered rate (Saibor). Deutsche Bank’s Saudi

Arabian arm and the investment banking arm of Riyad Bank

were the lead arrangers for the issue. (GulfBase.com)

Maaden to tender $240mn Waad Al Shamal WWTP – Saudi

Arabian Mining Company (Maaden) will tender the $240mn

water & waste water treatment plant (WWTP) at Waad Al

Shamal Mining City in Al Hail in July 2014. The detailed design

of the WWTP project is expected to be completed later this

month and Maaden is expected to float the tender by the first

week of July 2014. The plant will serve the Waad Al Shamal

Mining City, a 440-square-kilometers industrial city being built by

Maaden. Radicon Gulf Consult Kentz (RGCK) is the main

consultant, while Byrne Looby Partners (BLP) is the concept

design consultant for the project. Construction work is expected

to start by end of November 2014 and is likely to be completed

by 2Q2016. (GulfBase.com)

SABIC unveils first polycarbonate BIPV panels – Saudi Basic

Industries Corporation (SABIC) has launched the first

polycarbonate (PC) building-integrated photovoltaic (BIPV)

panels for roofing, cladding and glazing applications. The

innovative solution from SABIC’s innovative plastics business,

called LEXAN BIPV panel, provides architects & builders with

enhanced design freedom, thermal insulation, easy installation

and energy production in a single, integrated solution. These

panels, which are created through a close collaboration between

SABIC and Solbian Energie Alternative, combine tough,

5. Page 5 of 7

lightweight, transparent LEXAN Thermoclear PC sheet with

flexible PV laminated crystalline cells from Solbian and are

available in a broad range of structures, configurations and

colors. (GulfBase.com)

EY: Jeddah, Riyadh, Madinah hotel occupancy expands –

According to a report by Ernst & Young (EY), Jeddah witnessed

an 8.8% expansion in hotel rooms' yield to $207 on a 6.7%

growth in average room rate to $266 and 1% in occupancy to

77%, during the first four months of 2014. Riyadh witnessed a

7.9% rise in hotel rooms' yield to $162 on account of a 7%

growth in occupancy to 73% even as average room rate fell

3.1% to $220. The hotel rooms' yield rose 2.6% to $151 in

Madinah as an 8.4% plunge in average room rate to $182 was

made good by a 9% jump in occupancy to 82%. Makkah

witnessed a 4.7% slump in rooms' yield to $136 as average

room rate plunged 16.7% to $165; while there was a 10% surge

in occupancy to 82%. (GulfBase.com)

Saudi Arabia becomes major importer of hard, soft wheat –

The Grain Silos and Flour Mills Organization (GSFMO) said that

Saudi Arabia has bought 780,000 tons of hard and soft wheat in

a tender for shipment periods between September 10 and

November 30, 2013. Of the total, it bought 660,000 tons of hard

wheat and 120,000 tons of soft wheat. The accepted origins are

the European Union, North & South America and Australia at the

sellers’ option. The wheat is to be shipped in 13 consignments,

with 420,000 tons for shipment to the port of Jeddah and

360,000 tons for the port of Dammam. (GulfBase.com)

Maaden Aluminum starts production at rolling mill plant –

Saudi Arabian Mining Company’s (Maaden) subsidiary –

Maaden Aluminum Company – has started initial production of

aluminum sheets from rolling mill from June 24, 2014. The

aluminum sheets will be used in the manufacture of aluminum

cans and other end-use products. The rolling mill will be in its

ramp-up stage until gradually reaching its designed capacity of

380 kmt per year. (Tadawul)

SAAC German subsidiary faces legal actions in Iraq – The

Saudi Arabian Amiantit Company (SAAC) announced that its

German subsidiary, PWT Wasser-und Abwassertechnik GmbH

(PWT), is facing certain legal actions concerning its Al Samawa

Unified Water Treatment Plant located south of Iraq. (Tadawul)

IDB to finance $447.6mn for new projects – Islamic

Development Bank (IDB) has approved $447.6mn toward

financing new development projects in member countries. The

bank also approved three grants under the IDB Waqf fund for

educational projects for Muslim communities in Kenya, Lesotho,

and Trinidad and Tobago. IDB will invest $304mn in the energy

sector, $220mn for a power grid extension project in Bangladesh

and $83.75mn for a 132KV Mirama-Kable transmission line and

distribution project in Uganda, while other approvals include

$87.5mn for improvement of wastewater management and

sanitary services in Al Ghadir drainage basin, Lebanon, an

additional $25mn for the second phase of the Queen Alia Airport

expansion project; $15mn for a primary healthcare services

expansion project in Chad; and $15mn to support the

development of technical & vocational schools project in Guinea.

(Bloomberg)

MoE: UAE needs to roll back energy subsidies – The UAE

Minister of Energy (MoE), Suhail al-Mazrouei, said that the

country needs to roll back subsidies on fuel & power to help limit

its energy consumption and imports of natural gas. He added

that the government has yet to determine changes in prices and

subsidy levels. The UAE would retain some subsidies for its

citizens, who comprise about a 10th of its population.

(GulfBase.com)

Aramex to inaugurate new Egypt facility in August – Aramex

announced that it will inaugurate its new 14,000 square meters

logistics and warehousing facility in the industrial complex of 6th

of October City, in August 2014. This facility will bring Aramex

Egypt’s cumulative warehousing capacity to 106,000 square

meters with an option to expand to a total of 134,000 square

meters in the near future. This logistics and warehousing facility

is Aramex Egypt’s third biggest investment of its kind.

(GulfBase.com)

Emirates to consider A350, Dreamliner for ME routes –

Emirates Airline may still consider the Airbus Group A350 after

scrapping a contract for 70 of the wide-body planes valued at

$16bn two weeks ago. The A350 and Boeing’s rival 787

Dreamliner could meet the need for planes to operate routes

within the Middle East. Both types are smaller than the A380s

around which the current fleet is built, as well as the larger

version of the planned Boeing 777X Emirates plans to purchase.

(Bloomberg)

Arabtec former CEO receives three offers for stake sale –

Arabtec’s CEO Hasan Abdullah Ismaik has three offers for his

28.85% stake, but is looking to sell his holding in the company

for more than AED6 or AED 7 per share. Hasan Ismaik, who

resigned as CEO on June 19, 2014 has offers from government

entities and an international construction firm. (Reuters)

Borse Dubai refinances $500mn loan – Borse Dubai, the

UAE’s holding for its stock exchanges has refinanced a $500mn

three-year Shari’ah -compliant loan from Dubai Islamic Bank.

This replaced a maturing three-year loan arranged by Emirates

NBD. Reportedly, an ultra-low rate loan cost 90 basis points

over the London interbank offered rate, as compared to 210-220

bps for the previous loan. (Reuters)

Mubadala Petroleum makes gas discovery in Malaysia –

Abu Dhabi’s Mubadala Petroleum has made a new gas

discovery with significant commercial potential in Malaysia, its

fourth discovery within its operating block. Mubadala Petroleum,

a unit of Abu Dhabi’s investment fund Mubadala said it found

substantial gas in the Pegaga well in its operating block SK320.

The four gas discoveries are in proximity, including the original

M-5 well success. (GulfBase.com)

NDC inaugurates 7 new rigs in Upper Zakum – The National

Drilling Company (NDC) has inaugurated seven new rigs

assigned for drilling operations on artificial islands at the Upper

Zakum offshore oilfield. The rigs are part of NDC’s fleet

expansion plans that cover land, offshore and island rigs, to

serve the oil & gas industry in Abu Dhabi and keep abreast of

the long-term plans of its clients. NDC CEO, Abdullah Saeed Al

Suwaidi, said that the expansion plans have resulted in a

doubling of the rig fleet over the past three years.

(GulfBase.com)

AHB raises $500mn from Sukuk issuance – Al Hilal Bank

(AHB) has raised $500mn from the sale of perpetual bonds as it

seeks funds to boost capital. The Sukuk has no maturity and will

pay a coupon of 5.5%. Pricing was tightened from an original

guidance of about 6% as bids of about $5bn were received. Al

Hilal Bank (AHB), Citigroup, Emirates NBD Capital, HSBC

Holdings, National Bank of Abu Dhabi and Standard Chartered

managed AHB’s bond sale. (Bloomberg)

MCC, ADUG plans to form JV entity, Manchester Life

Development – Manchester City Council (MCC) is planning to

enter into a joint venture (JV) with Abu Dhabi United Group

(ADUG) to establish a new JV entity Manchester Life

Development Company or the regeneration of neighborhoods in

east Manchester, with the aim of building more than 6,000 new

6. Page 6 of 7

homes over ten years. As part of MCC’s 'Manchester Life'

initiative the newly-established JV entity will oversee

redevelopment & housebuilding in the city, with an initial focus

on the Ancoats and New Islington districts. (Bloomberg)

Kuwait, Britain sign MoU – Kuwait and Britain have signed a

MoU for scientific research and higher education, along with a

six-month official plan of action for the joint steering group,

which aims to promote bilateral cooperation. Under the MoU,

both the countries agreed to consolidate bilateral cooperation in

the fields of defense, security, immigration, health care,

education, culture, trade, investment and energy, according to a

joint press release issued following the meeting. Furthermore,

both parties discussed the sharing of experience in the area of

oil, gas, renewable energy, investment and training.

(Bloomberg)

Oman MoTC floats tender for Diba-Lima-Khasab road &

tunnel consultancy – Oman Ministry of Transport and

Communications (MoTC) has floated a tender to select a

consultant for preparing tender documents for Diba-Lima-

Khasab road and tunnel, which is on a design, build, operate

and maintain basis. The road is considered to be one of the

strategic linking roads in Oman that will enhance trade and

facilitate the flow of traffic between the wilayats of Musandam

governorate and contribute toward revitalizing tourism in the

governorate. The consultancy tender will be opened by July 15,

2014, while the documents will be distributed up to July 8, 2014.

The estimated cost will be in the range of $1bn, while the project

is among the most complex roads to be undertaken in the

Sultanate. As many as 31 local and international companies are

looking to pre-qualify for the construction work of the Diba-Lima-

Khasab road project. (GulfBase.com)

SEZAD to seek fresh bids for design of Bulk Liquid Berths

project – The Special Economic Zone Authority at Duqm

(SEZAD) is seeking fresh bids for a contract to undertake the

front-end engineering design (FEED) of a major Bulk Liquid

Berths project at the Port of Duqm. Earlier, the offers submitted

by three bidders were cancelled by SEZAD on the ground that

the firms in question failed to comply with pricing criteria set out

in the tender. Liquids comprising crude oil, refined petroleum

products, chemicals and petrochemicals, will constitute a

significant part of Port of Duqm’s cargo mix. A dedicated area

for liquid berths is under development along the Northern Lee

Breakwater. (GulfBase.com)

UNCTAD: Bahrain reports $989mn FDI in 2013 – According to

United Nations Conference on Trade and Development

(UNCTAD) World Investment Report 2014, total foreign direct

investment (FDI) to Bahrain in 2013 was $989mn, reflecting an

increase of 11% on 2012, outpacing global FDI flows which rose

by 9%. Earlier, Bahrain reported a FDI of $891mn in 2012,

reflecting a 14% increase on 2011. According to the report, 2013

Bahrain’s inward FDI stocks as a percentage of gross domestic

product (55.3%), FDI inflows as a percentage of nominal GDP

(3%), and FDI inflows as a percentage of gross fixed capital

formation (15.7%) were the highest in the GCC. (Bloomberg)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (*Market closed on June 24, 2014) Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13

QE Index S&P Pan Arab S&P GCC

(0.3%)

(0.9%)

(0.5%)

(0.0%) (0.2%)

(3.3%)

(6.7%)(7.5%)

(6.0%)

(4.5%)

(3.0%)

(1.5%)

0.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,318.40 0.1 0.3 9.4 DJ Industrial 16,818.13 (0.7) (0.8) 1.5

Silver/Ounce 20.93 0.2 0.2 7.5 S&P 500 1,949.98 (0.6) (0.7) 5.5

Crude Oil (Brent)/Barrel (FM

Future)

114.46 0.3 (0.3) 3.3 NASDAQ 100 4,350.36 (0.4) (0.4) 4.2

Natural Gas (Henry

Hub)/MMBtu

4.49 0.4 (0.4) 3.5 STOXX 600 345.57 (0.2) (0.7) 5.3

LPG Propane (Arab Gulf)/Ton* 108.00 0.0 (0.7) (14.6) DAX 9,938.08 0.2 (0.5) 4.0

LPG Butane (Arab Gulf)/Ton* 127.50 0.0 (0.8) (6.1) FTSE 100 6,787.07 (0.2) (0.6) 0.6

Euro 1.36 0.0 0.0 (1.0) CAC 40 4,518.34 0.1 (0.5) 5.2

Yen 101.97 0.0 (0.1) (3.2) Nikkei 15,376.24 0.0 0.2 (5.6)

GBP 1.70 (0.2) (0.2) 2.6 MSCI EM 1,048.14 0.6 0.4 4.5

CHF 1.12 0.1 0.1 (0.1) SHANGHAI SE Composite 2,033.93 0.5 0.4 (3.9)

AUD 0.94 (0.6) (0.2) 5.1 HANG SENG 22,880.64 0.3 (1.4) (1.8)

USD Index 80.33 0.1 (0.1) 0.4 BSE SENSEX 25,368.90 1.3 1.0 19.8

RUB 33.77 (1.1) (2.0) 2.7 Bovespa 54,280.78 0.1 (0.7) 5.4

BRL 0.45 (0.3) 0.3 6.3 RTS 1,421.07 3.8 4.6 (1.5)

177.1

147.2

133.7