1. http://www.scribd.com/doc/56594792/Azgard-9

INTRODUCTION Of AZGARD NINE

The Origins and the inception in the ancient legend “AZGARD” was one of none worlds in Norse

Mythology- it was protected by “Heimdall” the son of nine different Mothers each attributing him

with a particular skill and power – and thus He would protect Azgard from the powers that be.

The significance of nine for our company is not just based on this Mythology but also connected

with the auspicious nature of this number throughout many different elements in and out of the

world today that is an auspicious and important number in Indian, Chinese, Japanese and Greek

cultures for various different reasons.

In Chinese culture the number Nine represents „Change‟ and „Transformation‟, as in the case with

Azgard Nine which is changing and Transforming itself into an entity with new goals, aspirations

and targets.

Nine in much of ancient Greek methodology also has represented gestation and fulfillment of

creation as it does for us at Azgard Nine. The „fulfillment of creation‟ for us being the forming of

this global entity by nine members on the ninth day of February sowing the seeds for an

auspicious and rewarding future.

HISTORY:

The Azgard Nine Limited Group was started as a family business over four generations ago. The

Sheikh family, Now in its Fourth generation, in one of the oldest business families in the sub

continent with experience in many different sectors and having a proven track record of

successful leadership in four continents. The gamily began its first operations in 1886 in

shamkot, in the Asian sub continent.

Although, now, A Public company the family still remains behind the company in every way,

supporting and nurturing its growth into the future and beyond.

The current specialized yarn operation was set up in 1972 with the open end spinning and denim

weaving operations following in 1995. The final frontier was the garments operation, which

came in to being in 1997.

2. The concept behind the group‟s textile ambitions was to be a fully vertical apparel solution

provider based in a country that would be able to maintain its competitive advantage in this field

for the yards to come (Pakistan is the fourth largest denim producer in the world with an annual

production of 200,000,000 meters). This has now been achieved and Azgard in able to offer

these services as a single source supplier for all denim and specialized yarn customers.

The future is squeezing the brand customers toward a sourcing solution that stems from as small

a global map as will allow. We believe it is feasible, in order to not be spread too thin‟, to

consolidate a position in as few regions as possible in the quest of r practical and economical

global sourcing – Azgard Nine limited is that perfect vehicle which can accommodate and

achieve this position, therefore realizing the vision that was incepted so many years ago by the

guardians of the Azgard group bring the resultant advantages to you the customer.

MISSION

TEXTILE & APPAREL

To retain a leadership position as the largest value added denim Products Company in Pakistan.

VISION

TEXTILE & APPAREL

TO BECOME A MAJOR GLOBAL FASHION APPARECOMPANY

3. FINANCIAL ANALYSIS OF THE COMPANY

PURPOSE OF FINANCIAL ANALYSIS

1) In our course of financial management we are required to make a financial analysis of any

manufacturing company. The main purpose of these analyses is that we are the business graduate

and it is very necessary for us to apply our knowledge in the practical way. For example if in

future we are the manager of any bank and a company wants to obtain a loan from our bank then

we make analysis of the company‟s financial statement to access the capacity of paying us

interest on time as well as the principle which we lend that company through analyzing the

different ratio analyses, and to know that what is capital structure of the company.

2) Then through the cash flow statement we are able to know that how much cash is available

with the company because profitability does not mean that the company has the equal amount of

cash. We also able to know that how much cash is generated by the company from its operating

activities, and how much amount of cash is investing in the asset through which we can access the

future performance of the company.

3) Being as an investor if we are able to make an analysis of financial statement then we can

invest in that venture which is the best in terms of our purpose.

4) Being as an investor before investing in any company we can analyze the performance of

the company through the vertical analyses and horizontal analyses with the current and previous

year or we can also comparison of the company with the other company of the same age

(Competitors) and applying the same accounting techniques.

1. Short Term Debt-Paying Ability

Receivables 2005 2006 2007 2008 2009

1 Days' Sales in Receivables 83.68 84.72 91.26 64.14 97.23

2 Account Receivable turnover 4.52 4.55 4.75 5.89 4.79

3 Account Receivable turnover in 80.84 80.20 76.88 61.97 76.25

days

4. Receivables

120.00

100.00

80.00 Days' Sales in

Receivables

60.00 Account Receivable

40.00 Turnover

Account Receivable

20.00 Turnover in Days

-

2005 2006 2007 2008 2009

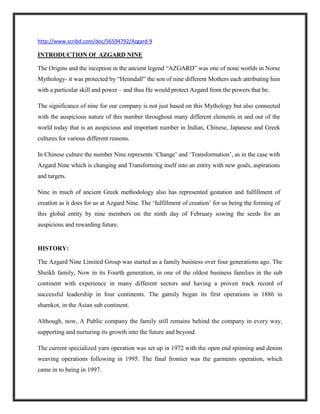

In the table and chart we see that day‟s sales in receivables are 83.68 days and it further increase

in the year of 2006 and 2007. An internal analyst compares day‟s sales in receivables with the

company credit terms as an indication of how efficiency the company manages its receivables.

We see that company have high sales in the years 2006 and 2007 but due to low credit policy

day‟s sales in receivables are increased in the years 2006 and 2007. In the year 2008 the days

sales in inventory were 64.14 which mean company control its credit policy. In the year 2009

receivables reached its highest position of 97.23 days which shows against company low credit

policy and poor management. In the year 2008 company have 64.14 days of minimum days and

shows a good credit policy within five years. If day‟s sales in receivables are materially more

than the credit terms, the company has a collection problem. An effort should be made to keep

the days sales in receivables close to the credit terms.

We see that company have increased account receivables turnover from 2005 to 2008, which

shows a good credit policy and efficient management. In the year of 2009 receivables decrease

which shows company inefficiency low credit policy. In the year 2005 receivables turnovers are

4.52 times which shows a low credit policy and poor management.

We see that account receivables turnover in days decrease from 2005 to 2008, which shows a

good credit policy of the company. In the year 2008 turnover in days are 61.97 days which are

minimum days in receivable turnover. In the year 2009 receivables turnover in days were 76.25

days which shows company low credit policy.

Inventory 2005 2006 2007 2008 2009

4 Day's sales in inventory 225.76 199.34 177.42 221.08 188.55

5 Inventory turnover 1.92 1.83 2.17 2.12 2.02

5. 6 Inventory turnover in 190.28 199.91 168.58 172.09 180.42

days

Inventory

250.00

200.00

Days Sale in Inventory

150.00

Inventory Turnover

100.00

50.00 Inventory Turnover in

Days

-

2005 2006 2007 2008 2009

We see that day‟s sale in inventory decrease from 2005 to 2007, which shows company

efficiency and good management .in the year 2007 inventory was 177.42 days which shows

efficient management and good company policy in this year. And it shows a positive trend. In the

year 2008 days sales in inventory reach to 221.08 days which shows a company bad policy and

management. In the year2005 company have day‟s sales in inventory of 225.76 days which mean

that company in this year take more days to sell the current inventory. In the year 2009 days sale

in inventory again decrease to 188.55 days which again shows company good management and

efficiency.

Inventory turnover increase in the year 2006 to 199.91 day‟s shows a positive trend. In the year

2007 it decrease which shows inefficiency and in last year it again increase, which mean

company sale more inventory in days.

2005 2006 2007 2008 2009

7 Net Working 323,461,546 1,187,508,778 3,163,296,118 789,374,554 (2,684,061,320)

Capital

6. Net Working Capital

4,000,000,000

3,000,000,000

2,000,000,000

1,000,000,000

Net Working Capital

-

2005 2006 2007 2008 2009

(1,000,000,000)

(2,000,000,000)

(3,000,000,000)

As we know that working capital is equal to current assets minus current liabilities so From the

above table and charts we see that current asset are increased from 2005 to 2007 as it shows

current assets were 45.26% in 2005 and liabilities were 42.19% in this year, and it shows a

highest current assets in this year and lowest of 38.91&% in the year of 2006. Current assets are

increased because company made more investments in these years. In the year 2009 current

liabilities are greater than current assets shows 32% current assets and 38.96% current liabilities.

There is increase in payables in this year. It shows a negative trend in the company.

2005 2006 2007 2008 2009

8 Current Ratio 1.07 1.15 1.51 1.08 0.82

9 Acid-test Ratio 0.41 0.80 0.99 0.61 0.45

10 Cash Ratio 0.01 0.07 0.01 0.01 0.01

Current, Acid test & CASH Ratio

2.00

1.50

Current Ratio

1.00

Acid _ Test Ratio

0.50 Cash Ratio

-

2005 2006 2007 2008 2009

7. From the above table and chart we see that current ratio shows a positive trend from 2005 to

2007. current asset are increased from 2005 to 2007 as it shows current assets were 45.26% in

2005 and liabilities were 42.19% in this year, and it shows a highest current assets in this year

and lowest of 38.91&% in the year of 2006. Current assets are increased because company made

more investments. Company has a good current ratio of 1.51 in the year of 2007 which shows of

company efficiency. In the year 2009 current liabilities are greater than current assets shows 32%

current assets and 38.96% current liabilities. There is increase in payables in this year. It shows a

negative trend in the company. In 2009 current ratio remains 0.82.

The acid test ratio relates the most liquid assets to current liabilities. And inventory is removed

from current assets when computing the acid test ratio. So we can see that from above table and

chart that acid test ratio increase from 2005 to 2007. And it has a maximum position of 0.99 in

the year of 2007. And in last year it decrease to 0.45 in 2009.

When we need to view liquidity of a firm from an extremely conservative point of view, then we

use cash ratio. We see that it minor increase of .07 in the year of 2006 and then decrease

onwards, and remain at .01 in the last year.

1. Long-term Debt Paying Ability

2005 2006 2007 2008 2009

11 Times Interest Earned 2.80 1.23 1.48 1.15 1.08

12 Fixed Charge Coverage 2.80 1.23 1.48 1.15 1.08

Time Interest Earned & Fixed Charge

Coverage Ratio

3.00

2.50

2.00

1.50 Time interest

Earned ratio

1.00

Fixed Charge

0.50 Coverage Ratio

-

2005 2006 2007 2008 2009

8. From the table and chart we see that time interest earned ratio and fixed charge coverage ratio

both are decreased in the year of 2006. These ratios indicate the firm‟s long term debt paying

ability and in this situation we see a change from 2.80 times to 1.23 times show that the firm will

not be able to meet its interest obligation. In the year 2007 firm little betters its ratio to 1.48

times than before. And again it‟s decreased to 1.08 times per year in the year 2009. A relatively

high, stable coverage of interest over the year indicate has a good record and a low fluctuating

coverage from year to year indicate a poor record. In this situation we see that company has a

ratio of 2.80 times shows a good record and debt paying ability and 1.08 times show a bad

performance and record of the company.

In 2005 a good record shows that the company has a high proportion of debt in relation to

stockholders equity and at the same time, obtains funds at the favorable rates. Fixed charge

coverage ratio indicate that a firm‟s ability to cover fixed charges.

2005 2006 2007 2008 2009

13 Debt Ratio 0.68 0.59 0.58 0.62 0.52

14 Debt/Equity Ratio 2.32 1.48 1.41 1.68 1.38

2.5

2

1.5

Debt Ratio

1

Debt/Equity Ratio

0.5

0

2005 2006 2007 2008 2009

Debt ratio indicates the firm‟s long term debt paying ability. This ratio indicates the percentage

of assets financed by the creditors, and it helps to determine how well creditors are protected in

case of insolvency. If creditors are not well protected, the company is not in a position to issue

9. additional long term debt. So from table and chart we see that debt ratio is decreased in 2006

indicates a better company position. In 2008 it again increases to .62%. In last year it again

decrease to 0.52%.

From chart and table we see that debt/equity ratio of the company was 2.32% in the year 2005.

And it decrease to 1.48% in 2006 indicate the company good performance. 2005 shows a very

danger position and it shows that creditors are not protected and they are going to insolvency. In

the last year 2009 ratio reach to 1.38% indicates a good position of the company and debt paying

ability. In 2005 company have more debt ratio then equity ratio indicate a danger sign for

creditors and in 2009 lower this ratio give protection to the creditors.

3. Profitability Ratios

2005 2006 2007 2008 2009

16 Net Profit Margin 0.17 0.23 0.16 0.09 0.01

17 Return on Assets 0.06 0.87 0.64 0.59 0.07

18 Operating Income Margin 0.18 0.16 0.24 0.28 0.21

19 Return on Operating Assets 0.18 0.51 - - -

20 Gross Profit Margin 0.26 0.24 0.30 0.34 0.27

1.00

0.90

Net Profit Margin

0.80

0.70

Return on Asset

0.60

0.50 Operating income

Margin

0.40

Return on operating

0.30

Assets

0.20

Gross Profit Margin

0.10

-

2005 2006 2007 2008 2009

10. From above table and chart we see that net profit margin increase in the year 2006. And then it

continuously decreases. Different factors like competitive force within the industry, economic

condition, debt financing, and high fixed cost affect the net profit margin. Due to some increase

in debt ratio and other factors profit margin reach to .01% in last year.

Return on assets increase from .06% to .87% which shows that the firm‟s best utilize its assets to

create profits by comparing with the assets that generate the profits. In the year 2007 it start

decreases and in th year 2009 it reach to .07% which mean that firm inefficiency in utilization of

its resources to generate profit. In the year 2005 company have a very low return on assets then

some growth and then again decrease till the last year which shows that company was not in the

position to maintain its policies, better management and best use of resources.

Operating income margin shows a minor fluctuation within years. At 2008 it was at high position

of 0.28%. Gross profit margin equal the difference between sale revenue and cost of goods sold.

From the following data it shows that gross profit margin decreases in 2006 and then some

increase in two years then it again decrease. It shows a high profit margin in 2008 of .34%. Some

factors like cost of buying inventory, selling price decline and other situation in the company

cause effect on the gross profit margin.

2005 2006 2007 2008 2009

21 Total Assets Turnover 0.38 0.22 0.19 0.27 0.25

22 Operating Assets Turnover 1.00 3.14 - - -

23 Sales to Fixed Assets 0.75 0.38 0.31 0.45 0.40

Total Assets , Operating Asset Turnover&

Sales to Fixed Assets

3.50

3.00

2.50

Total Asset Turnover

2.00

1.50 Operating Asset

Turnover

1.00 Sale to Fixed Assets

0.50

-

2005 2006 2007 2008 2009

11. From above table and chart we see that operating assets turnover are increased in the year 2006

reach to 3.14 times. It shows that company use of utilizing operating assets to generate sale. And

company in good position in this year. And then it starts to decrease and reach to zero in the

years of 2007 to 2009. Because company were not able to use its assets properly to generate

sales.

Sale to fixed assets decreases from 2005 and reach to .31. In the year 2005 sale to fixed assets

was .75 times which mean that company has a better ability to make productive use of its

property, plant and equipment by generating sale dollars. And in the year 2007 company have

ratio of .31 times which shows company were not use fixed assets to generate sales.

2005 2006 2007 2008 2009

24 Return on Investment 0.20 0.15 0.11 0.15 0.09

25 Return on Total Equity 0.24 0.12 0.11 0.09 0.00

26 Return on Common Equity 0.28 0.32 0.19 0.16 0.01

27 Return on Total Assets 0.09 2.92 1.82 1.47 0.67

Variation

3.50

3.00

2.50 Return on

Investment

2.00 Return on Total

Equity

1.50

Return on Comman

1.00 Equity

Return on Total

0.50 Asset Variation

-

2005 2006 2007 2008 2009

From the above table and chart the return on investment decreasing within two years and then

increase in 2008 and then again decrease in last year. It shows high ratio at year 2005 which

12. mean the ability of the firm to reward those who provide long term funds and to attract providers

of future funds.

Return on total equity was .24% in the year 2005 and then it starts decrease and become negative

in 2009. It measure the both return to common stock and preferred stockholder.

Return on common equity show the common stockholder, the residual owner. It has the same

case as with the return on total equity.

Vertical Analysis

ITEMS V 05 V 06 V 07 V 08 V 09

Vertical Analysis (Values in %)

Sales- 100.00% 100.00% 100.00% 100.00% 100.00%

Net

Cost of sales -74.37% -75.74% -69.72% -65.85% -72.81%

GROSS PROFIT 25.63% 24.26% 30.28% 34.15% 27.19%

Selling and distribution -2.75%

expenses

Administrative and general expenses -4.26%

ADMINISTRATIVE AND SELLING 7.25% 8.00% 6.57% -5.97%

EXPENSES

Net other income 1.68%

OPERATING 18.38% 16.26% 23.72% 28.18% 22.29%

PROFIT

Other income 6.92% 22.96% 9.67% 6.13%

25.30% 39.22% 33.39% 34.31%

OTHER

CHARGES

Finance Cost 6.57% 13.27% -16.02% -24.43% -20.65%

Workers' Profit 0.55% 0.16%

13. Participation Fund

Others 0.27% 0.02% -0.11%

7.39% 13.45%

Profit before 17.91% 25.77% 17.37% 9.88% 1.52%

taxation

Provision for -1.15% -2.36% -1.09%

taxation

Taxation -1.01% -1.01%

PROFIT AFTER 16.76% 23.41% 16.29% 8.87% 0.52%

TAXATION