Market Outlook Remains Positive Despite Some Risks

1.

Whil

disap

solid

while

These

Comp

Perha

last t

week

analy

inves

Bond

and d

fell.

thoug

term

whos

inves

Finan

unem

first m

to arg

DJIA

S&P 5

Russe

NYSE

Comp

Index

Q

e market par

ppointments in

year overall

e the S&P 50

e two majo

posite Index r

aps one of th

two days of t

k of 2014 off,

ysts to predic

stors experien

d investors al

declining inf

Bonds were

gh they ended

interest rates

se holdings w

sted in sub-inv

ncial experts

mployment, ris

many predict

gue with the a

B

1

500

ell 2000

E

posite

x

1

Micha

Co

Quarterly

rticipants and

n 2014, many

l. The Dow J

00 experience

r indexes ou

rose a little m

e more tellin

the trading y

finishing mo

ct that 2015

nced in 2014.

so fared well

flation—espec

e also helped

d their stimul

s. This added

were in gover

vestment grad

are pointing

sing stock pri

ions for 2014

average strate

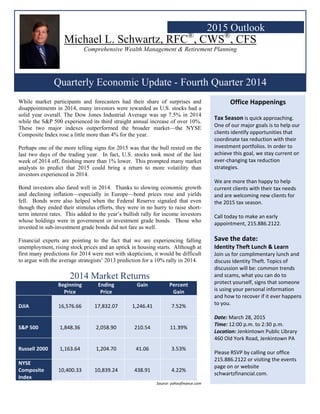

2014

Beginning

Price

16,576.66

1,848.36

1,163.64

10,400.33

ael L. S

omprehensiv

y Econo

d forecasters

y investors w

Jones Industr

d its third str

utperformed

more than 4%

g signs for 2

year. In fact,

ore than 1% lo

could bring

l in 2014. Th

cially in Eur

d when the F

lus efforts, th

d to the year’

rnment or inv

de bonds did

g to the fact

ices and an up

4 were met wi

egists’ 2013 p

Market

Ending

Price

17,832.07

2,058.90

1,204.70

10,839.24

Schwar

ve Wealth Ma

omic Up

had their sh

were rewarded

rial Average w

raight annual

the broader

for the year.

015 was that

U.S. stocks

ower. This p

g a return to

hanks to slow

rope—bond p

Federal Reser

hey were in n

s bullish rally

vestment grad

not fare as we

t that we are

ptick in housi

ith skepticism

prediction for

Returns

Gain

1,246.4

210.54

41.06

438.91

rtz, RF

anagement &

pdate -

hare of surp

d as U.S. stoc

was up 7.5%

increase of o

r market—th

the bull reste

took most o

prompted man

o more volati

wing economi

prices rose an

rve signaled t

no hurry to ra

y for income

de bonds. Th

ell.

e experiencin

ing starts. Al

m, it would be

a 10% rally i

Perc

Ga

1 7.52

4 11.3

3.53

1 4.22

Source: yahoo

2

FC®

, CW

& Retiremen

Fourth

prises and

cks had a

% in 2014

over 10%.

he NYSE

ed on the

of the last

ny market

ility than

ic growth

nd yields

that even

aise short-

investors

hose who

ng falling

lthough at

e difficult

in 2014.

cent

ain

2%

39%

3%

2%

ofinance.com

2015 Ou

WS®

, C

nt Planning

Quarte

Off

Tax Seaso

One of our

clients iden

coordinate

investment

achieve thi

ever‐chang

strategies.

We are mo

current clie

and are we

the 2015 ta

Call today t

appointme

Save the

Identity T

Join us for

discuss Ide

discussion

and scams,

protect you

is using you

and how to

to you.

Date: Marc

Time: 12:0

Location: J

460 Old Yo

Please RSV

215.886.21

page on or

schwartzfin

utlook

CFS

er 2014

fice Happe

on is quick ap

r major goals

ntify opportu

e tax reductio

t portfolios. I

is goal, we sta

ging tax reduc

ore than happ

ents with the

elcoming new

ax season.

to make an e

ent, 215.886.2

e date:

heft Lunch &

complimenta

ntity Theft. T

will be: comm

, what you ca

urself, signs t

ur personal in

o recover if it

ch 28, 2015

0 p.m. to 2:30

enkintown Pu

ork Road, Jenk

VP by calling o

122 or visiting

r website

nancial.com.

enings

proaching.

is to help our

nities that

n with their

n order to

ay current on

ction

py to help

ir tax needs

w clients for

arly

2122.

& Learn

ary lunch and

Topics of

mon trends

an do to

hat someone

nformation

ever happen

0 p.m.

ublic Library

kintown PA

our office

g the events

r

e

s

2.

Altho

conse

Bob D

strate

will b

consu

mark

howe

a dec

Weal

While

anoth

that th

analy

under

Acco

conse

corpo

Intere

The F

raise

that w

from

timel

finan

actua

This

if yo

If y

Loo

ough there are

ensus for 201

The U.S. e

Unemploy

The Europ

Japan’s re

The Fed w

Stocks wil

Treasuries

Doll, senior p

egist of Nuvee

be a good eco

umer spendin

et, and solid e

ever, is the ris

line in oil pri

lthManageme

e it’s easy for

her strong yea

he current bu

ysts conclude

r certain finan

ording to Bloo

ensus earning

orations is exp

est rates will p

Federal Reser

interest rates

were designed

the 2008 fina

ine for doing

cial experts a

ally go up in 2

year, our g

ou would:

Suggest a

Share this

Those clien

you are curr

one‐

oking Ahea

e still some st

5 appears to b

economy will

yment figures

pean economy

ecession will e

will raise the

ll remain attra

s

portfolio mana

en Asset Man

onomic year, w

g picking up,

earnings grow

sk of deflation

ces. (Source:

nt.com, 1/201

r investors to

ar in 2015, we

ull market star

that stocks ar

ncial metrics v

omberg, after

gs-per-share g

pected at 8%

Interest R

play a role fo

rve has alread

and phase ou

d to stimulate

ancial crisis.

so still remai

are split on wh

2015.

(So

Schw

goal is to of

friend to rec

s newsletter w

nts who do

incl

rently not a

‐hour, cons

ad to 2015

trong contrari

be bullish:

l move forwar

s will go lowe

y will get bett

ease

federal funds

active compar

ager and chie

nagement, bel

with low infla

an improving

wth. The bigg

n outside the U

:

15)

want U.S. sto

e still need to

rted in 2009. I

re no longer c

valuations, ar

gaining 10%

growth for U.S

in 2015.

Rates

r investors ag

dy signaled th

ut the easy mo

the faltering

Having said t

ins uncertain

hether interes

ource: Wall street

wartz Fina

ffer our serv

eive our mail

with a friend

any of the a

udes our si

a client of S

sultation w

ians, the

rd

er

ter

s rates

red to U.S.

f equity

lieves 2015

ation,

g job

gest risk,

U.S., led by

ocks to have

remember

In fact, some

cheap—and

re high.

in 2014,

S.

gain in 2015.

at it plans to

oney policies

economy

that, their

and

t rates will

Journal 12/2014)

ancial 20

vices to sev

lings

or colleague

above will b

ncere grati

Schwartz Fi

ith one of o

1

2

3

4

5

15 Client

veral other c

S

c

be entered

tude and a

nancial, we

our profess

Jurrie

Globa

Reser

inves

Reme

provi

again

shoul

In the

wrote

been

“will

return

Energ

perfo

mid-y

quest

share

oil pr

consu

on un

value

bond

“It’s n

Many analys

Federal Rese

bring more v

Oil prices co

International

The U.S. pol

t Advocat

clients like

Bring a guest

Share the new

consultations

into our Cl

special eve

e would lik

sionals. Plea

en Timmer, D

al Asset Alloc

rve uncertaint

stors.”

ember—in ma

ide portfolios

nst stock mark

ld not try to c

eir 2015 Inves

e, “We believ

in recent year

be transitioni

n expectation

gy stocks hav

ormers, as oil

year peak of o

tioning if ther

es. Some anal

rices still have

umers at the p

nemployment

es, energy-com

market.

not clear that

sts feel U.S. m

erve and inter

vitality

ould create ma

l concerns ne

litical landsca

te Progra

yourself. W

t to one of ou

ws of our com

s

ient Advoca

ent this fall

ke to offer y

ase call, 21

Director of Gl

cation Divisio

ty could mean

any cases, bo

with stability

ket swings. C

chase speculat

stment Outloo

ve returns will

rs.” They say

ing into a new

s ought to be

Oil Pric

ve been among

prices decline

over $100 a b

re are bargain

lysts see valu

e to stabilize.

pump, but the

t, capital spen

mpany balanc

t anyone can a

Quarterly

F

markets will r

rest rate uncer

arket disrupti

ed to be mon

ape has chang

m

We would be

r workshops

mplimentary

ate Program

.

you a comp

15.886.2122

obal Macro in

on, says that

n more volati

onds are suppo

y and hopeful

Conservative i

tive returns in

ok, Delaware

l be lower tha

y that bond in

w reality, one

tempered.”

ces

g the year’s w

ed almost 50%

barrel. Many

ns in beaten-d

ue, while othe

Lower oil pr

ey can wreak r

nding, loan co

ce sheets and

answer how l

y Economic

Fourth Quart

rise.

rtainty could

ion.

itored.

ged.

e honored

m which

plimentary,

2.

n Fidelity's

“Federal

ility for

osed to

lly help

investors

n bonds.

e Investments

an they have

nvesting

e in which

worst

% from their

investors are

own energy

rs fear that

rices help

real havoc

ollateral

the junk-

ow [oil

Update

ter 2014

4.

Quarterly Economic Update

Fourth Quarter 2014

Retirement Planning Strategies

· IRA/Roth IRA

· Pensions/Profit Sharing

· SIMPLE Plans

· SEP-IRA Plans

· 401(k)/403(B)

Insurance Services

· Life

· Annuities

· Long Term Health Care

· Disability

College Savings Analysis

· Educational IRA

· 529 Plans

· Custodial Accounts

Investment Services

· Stocks

· Corporate Bonds

· Municipal Bonds

· Mutual Funds

· Real Estate Investment Trusts

· Variable Insurance / Annuities

· Private Equity

Estate Analysis

· Estate Tax Analysis

· Creation

· Estate Conversion Strategies

· Tax and Distribution Analysis

· Legacy Planning

Quarterly Economic Update

Fourth Quarter 2014

In this quarterly review:

A Year in Review

2014 Market Returns

Office Happenings

- Tax Season

- Save the Date

Looking Ahead to 2015

- Interest Rates

- Oil Prices

- International Concerns

- U.S. Politics

An Outlook of 2015

Client Advocacy Program

Conclusion: What Should an Investor Do?

Schwartz Financial Services

Comprehensive Wealth Management & Retirement Planning

Schwartz Financial Services

Comprehensive Wealth Management & Retirement Planning

115 Old York Road | Jenkintown, PA 19046

215.886.2122 | 215.886.6144 (fax)

Schwartzfinancial.com

Complimentary Financial Review

If you are currently not a client of

Schwartz Financial, we would like

to offer you a complimentary,

one-hour, consultation with one of

our professionals. Please call,

215.886.2122.

Help us Grow in 2015

This year, our goal is to offer our

services to several other clients

like yourself. Refer a friend and

become part of our Client

Advocacy Program.