Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie journal and ledger

Ähnlich wie journal and ledger (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

journal and ledger

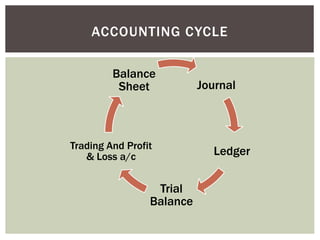

- 1. Journal Ledger Trial Balance Trading And Profit & Loss a/c Balance Sheet ACCOUNTING CYCLE

- 2. Book of original or prime entry as business transactions are recorded at the first instance. Transactions recorded in the order in which they occur, i.e. in chronological order. Basic book of accounting JOURNAL

- 3. The process of entering or recording the transaction in the journal is called Journalising. Record of each transaction in the journal is called journal entry.

- 4. Date Particulars L.F Debit Credit JOURNAL

- 5. Personal A/c Debit the receiver Credit the giver Real A/c Debit what comes in Credit what goes out Nominal A/c Debit all expenses and losses Credit all gains and incomes RULES OF DEBIT AND CREDIT

- 6. Journal provides a chronological i.e. date wise record of all business transactions at one place. Transactions recorded as and when they take place, chances of any transaction being unrecorded is reduced to the minimum. Facilitates preparation of ledger accounts. Serves as evidence in the court of law. Transactions recorded with narration, reason for each transaction can be ascertained. ADVANTAGES OF JOURNAL

- 7. When the number of transactions is very large, it may practically be difficult, if not impossible, to record all the transactions through one journal because of the following reasons: (1) The system of recording all the transactions in a journal requires the writing down the name of the account involved as many times as the transactions occur. (2) Such a system does not provide the information on prompt basis. (3) Such a system does not facilitate the installation of an internal check system, since the journal can be handled only by one person. If we have a serious look on the limitations, it can be observed that most of them have been done away with, because of the advent of computer vis a vis accounting related softwares like tally. LIMITATION OF JOURNAL

- 8. LEDGER

- 9. Book of secondary entry Transactions recorded in the journal are finally carried to the ledger. Contains all the accounts of a business whether real, personal or nominal. LEDGER

- 10. Debit Credit Date Particulars J.F Amount Date Particulars J.F Amount FORMAT

- 11. BASIS JOURNAL LEDGER 1.Nature Of Book It is a book of prime entry It is book of secondary entry 2.Basis Of Preparation It is prepared on the basis of source documents. It is prepared on the basis of journal. 3.Object It is prepared to record all transactions in chronological order. It is prepared to know the net effect of various transactions affecting a particular account. 4.Balancing Journal is not balanced. All ledger accounts are balanced 5.Narration Narration is written for each entry No narration is given. 6. Name of process The process is called journalizing. The process of recording in the ledger is called posting. DISTINCTION BETWEEN JOURNAL AND LEDGER

- 12. “Trial balance is a statement containing the balances of all ledger accounts, as at any given date, arranged in the form of debit and credit columns placed side by side and prepared with the object of checking the arithmetical accuracy of ledger postings.” TRIAL BALANCE

- 13. It is a statement or a schedule. It contains debit and credit balances of various accounts. If the trial balance does not agree, it points out that there are some errors. It can be prepared only after balancing all the accounts in the ledger. It is prepared to check the arithmetical accuracy of books of accounts. FEATURES OF TRIAL BALANCE

- 14. To provide check on arithmetical accuracy of books of accounts To provide a basis for the preparation of final accounts To provide a summary of ledger accounts OBJECTIVES

- 15. There are certain errors which are not disclosed by a trial balance. Does not provide detailed information about ledger accounts. It is not a substitute of financial statements. LIMITATIONS OF TRIAL BALANCE

- 17. 1. Posting of wrong amount: Wrong amount posted in the ledger in one of the two accounts involved. For example, received Rs. 450 from Mr. A and wrongly posted to his account as Rs. 540 2. Posting to wrong side: For example, if discount allowed to customer Rs. 100 is posted to the credit side of the discount allowed, trial balance will not match. ERRORS DISCLOSED BY TRIAL BALANCE

- 18. 3. Omission to post from journal: For example, if goods purchased from A are recorded in purchases a/c but omitted to be posted to A’s account in the ledger, the credit side of the trial balance shall fall short 4. Carrying wrong amount to the trial balance: When a wrong amount is carried from ledger to the trial balance, it would cause disagreement of the trial balance. For example, a balance of Rs. 580 in Mohan a/c wrongly recorded as Rs. 850 in the trial balance.

- 19. 5. Wrong totalling or balancing of ledger accounts: If some error is committed while totalling or balancing of ledger accounts, the wrong balance shall be carried to the trial balance and the trial balance will not agree. 6. Wrong totalling of trial balance: If there is an error in totalling the two sides of the trial balance, the trial balance does not agree.

- 20. 1. Errors of omission: If a transaction is omitted to be recorded in the books of original entry, i.e. journal, both debit and credit aspects will not be posted in the ledger and hence the trial balance will not be affected. For example, goods purchased from Sohan omitted to be recorded in the journal. ERRORS NOT DISCLOSED BY TRIAL BALANCE

- 21. 2. Incorrect amount recorded: If an incorrect amount is recorded in the books of journal, both debits and credits shall still be equal and the trial balance will agree. For example, sale of Rs. 10000 wrongly recorded as Rs. 100 in sales book. 3. Errors of compensatory nature: When two or more errors are made in such a manner that they neutralize the effect of each other, it will not cause any disagreement in the trial balance. For example, Rs. 500 not debited to some account is compensated if the same amount is not credited to some other account.