1. Daily Derivatives Outlook

28 March 2013

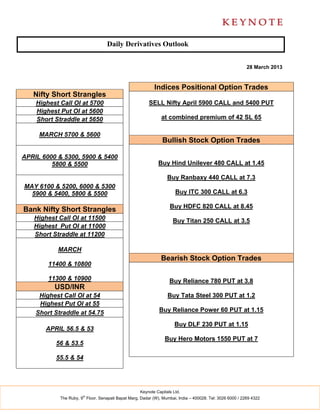

Indices Positional Option Trades

Nifty Short Strangles

Highest Call OI at 5700 SELL Nifty April 5900 CALL and 5400 PUT

Highest Put OI at 5600

Short Straddle at 5650 at combined premium of 42 SL 65

MARCH 5700 & 5600

Bullish Stock Option Trades

APRIL 6000 & 5300, 5900 & 5400

5800 & 5500 Buy Hind Unilever 480 CALL at 1.45

Buy Ranbaxy 440 CALL at 7.3

MAY 6100 & 5200, 6000 & 5300

5900 & 5400, 5800 & 5500 Buy ITC 300 CALL at 6.3

Buy HDFC 820 CALL at 8.45

Bank Nifty Short Strangles

Highest Call OI at 11500 Buy Titan 250 CALL at 3.5

Highest Put OI at 11000

Short Straddle at 11200

MARCH

Bearish Stock Option Trades

11400 & 10800

11300 & 10900 Buy Reliance 780 PUT at 3.8

USD/INR

Highest Call OI at 54 Buy Tata Steel 300 PUT at 1.2

Highest Put OI at 55

Short Straddle at 54.75 Buy Reliance Power 60 PUT at 1.15

Buy DLF 230 PUT at 1.15

APRIL 56.5 & 53

Buy Hero Motors 1550 PUT at 7

56 & 53.5

55.5 & 54

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322

2. READY RECKONER ON OPTION AND TECHNICAL STRATEGIES :

INTRODUCTION TO OPTIONS:

Options are Wasting Assets with Option Pricing like Insurance Pricing.

Strike Price is similar to Age of the Assets.

OTM(Out of the Money) are Low Probability strikes (young assets), ATM (At the Money)

are equal probability strikes (average age assets) and ITM (In the Money) are High

Probability strikes ( old assets).

Premium reduces from ITM to ATM to OTM as probability of event happening reduces.

Mirror Image Concept : OTM for Calls is same as ITM for Puts and ITM for Calls is same as

OTM for Puts.

View for Strike Selection : OTM - Strong conviction. ATM - Moderate conviction . ITM –

Low Conviction

Advantages of Options – Profit from Trading range Markets, High Leverage, Built-in Stop

Loss, Higher Probability of Profit using Spread Trades, Increase in trading opportunities due to

multiple legs, Lower Margin requirements due to high gearing in options, Increase in Reward to

Risk ratio.

OPTION INTERNALS:

Call-Put Parity : Futures Price = Strike Price + Call Premium – Put Premium

Put Call Ratio ( Open Interest) is bullish at levels between 0.8 to 1.2 and bearish between

1.75 to 2.

Equilibrium strike is with equal Call and Put Open interest with Highest Call Open interest

strike as resistance and Highest Put Open interest as support.

Greeks – Delta is the Probability. Gamma is the Change in Delta. Theta is the change in time

remaining.

Vega is the Change in Volatility (VIX) and Rho is the Change in Interest Rate.

If VIX ( Volatility Index) is above average selling options is preferred and if VIX is below

average buying options is preferred. The long-term average of the India VIX is around 24.

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322

3. Historical Volatility (Realized Volatility) is based on the standard deviation of the underlying

asset while Implied Volatility is derived from the option premium traders are willing to pay to

hedge their positions.

The Put Implied Volatility generally trades at a premium to Call Implied Volatility with panic

or fear conditions in the market leading to expansion of the premium.

RISK MANAGEMENT:

Risk Management using options - Quantify the maximum risk and maximum reward and the

breakeven points of a position before committing capital. A risk manager always focuses on

how much can be lost in a position. Control the losses and the profits will take care of

themselves. Determine an exit strategy in advance for every trade initiated. An exit strategy

enables closure of loss-making positions unemotionally so that there is no freeze or panic

when confronted with the loss.

Stop Loss : Use 50% stop loss for premium paid or received for both one-leg and multiple-leg

strategies.

ONE-LEG STRATEGIES:

Long Call and Long Put are Limited Risk and Unlimited Reward strategies.

Short Call and Short Put are Unlimited Risk and Limited Reward strategies.

TWO LEG STRATEGIES:

Long Synthetic ( Buy ATM Call and Sell ATM Put) and Long Combo( Buy OTM Call and Sell

OTM Put) are used to create synthetic long positions which have lower margins than

comparable futures positions.

Short Synthetic ( Buy ATM Put and Sell ATM Call) and Short Combo( Buy OTM Put and

Sell OTM Call) are used to create synthetic short positions which have lower margins than

comparable futures positions.

Long Straddle, Long Strangle and Long Guts are Long volatility strategies ahead of

events/results etc.

Short Straddle, Short Strangle and Short Guts are Short volatility strategies when range-

bound action is anticipated.

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322

4. TWO-LEG FUTURE AND OPTION COMBINATION STRATEGIES:

Protective Put and Protective Call protect futures positions by buying options.

Covered Call/Ratio Call Write and Covered Put/Ratio Put Write cover futures positions by

selling options. They involve unlimited risk and limited reward.

Collar is a combination of the Covered Call and the Protective Put or the Covered Put and

the Protective Call.

TWO-LEG AND THREE- LEG SPREAD STRATEGIES:

Bull Call Spread, Ratio Bull Call Spread and Bull Call Ladder are bullish debit spreads

which involve buying a lower call option and selling upper call options.

Bear Put Spread, Ratio Bear Spread and Bear Ladder are bearish debit spreads which

involve buying a upper Put option and selling a lower Put option.

Bull Put Spread is a bullish credit spread which involves selling a upper put option and

buying a lower put option.

Bear Call Spread is a bearish credit spread which involves selling a lower call option and

buying a upper call option.

Call Ratio Backspread is a credit spread which involves selling one or two lower strike calls

(ITM or ATM) and buying two or three upper strike calls.(OTM).

Put Ratio Backspread is a credit spread which involves selling one or two upper strike puts

(ITM or ATM) and buying two or three lower strike puts.(OTM).

FOUR-LEG BUTTERFLY AND CONDOR STRATEGIES:

Long Iron Butterfly is a credit strategy using a combination of the Short Straddle and

Long Strangle, while in a Long Iron Condor the middle strikes are separated.

Short Iron Butterfly is a debit strategy using a combination of the Long Straddle and Short

Strangle, while in a Short Iron Condor the middle strikes are separated.

Long Call Butterfly involves buying a lower strike call (ITM), selling two middle strike calls

(ATM) and buying a upper strike call(OTM). In Long Call Condor the middle strikes are

separated.

Long Put Butterfly involves buying a lower strike put (OTM), selling two middle strike

puts(ATM) and buying a higher strike put (ITM). In Long Put Condor the middle strikes are

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322

5. separated.

LONG TERM OPTIONS and CALENDAR/DIAGONAL STRATEGIES

Long Term Options can be used to create investment grade positions using spreads,

synthetics and covered /protective positions.

Calendar/Diagonal Calls is a debit spread involving buying a long-dated call option and selling

a short-dated call option against it ( Diagonal Calls involve different strikes).

Calendar/Diagonal Puts is a debit spread involves buying a long-dated put option and selling

a short-dated put option against it ( Diagonal Puts involve different strikes).

DELTA HEDGING METHODS

The distance between the current market price and the short option breakeven point is

divided into equal parts so that futures exposure is increased at consecutive delta

adjustment points to ensure that the short option position is totally hedged by the time the

breakeven point is reached.

The size of the short option position is directly proportional to the distance of the short

breakeven point to the current market price. Position size should be maximum at deep-out-of-

the money strikes and reduce gradually as the distance to the market price reduces.

Short gamma positions carry the maximum risk and using options instead of futures to hedge

is advisable since futures does not cover the gap risk, while using ITM options covers the gap

risk

USING OPTIONS WITH SUPPORT/RESISTANCE AND MOVING AVERAGES:

Buy call options at Support ( Bottom-fishing) and above resistance ( Breakout) .

Buy Put options at Resistance ( Top-picking) and Below Support ( Breakdown).

Moving Average Crossovers – Buy call options if price crosses the moving average from

below and buy put options if price crosses moving average from above.

The one month options can be linked to the 20dma with the three month options linked to

the 50dma and the 1 year options linked to the 200dma.

USING OPTIONS WITH OSCILLATORS:

RSI – Buy call options when RSI is below 30 and Buy put options when RSI is above 70.

The RSI 50 crossover can be used to buy calls on the upside crossover and to buy puts on

the downside crossover.

MACD and Parabolic SAR early warning buy signals indicate buying of calls ( bottom-

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322

6. fishing) and sell signals indicate buying of puts ( top-picking).

ADX indicates the strength of the trend and whether the market is in a trending or trading

mode. When ADX is above 25 and +DI is above –DI then buy calls and if –DI is above +DI

then buy puts. When ADX is below 25, then selling strangles and straddles will be profitable.

Widening Bollinger Bands indicate increasing volatility and option buying is advised as

a trending move is expected.

Flat or Narrowing Bollinger Bands indicate reducing volatility and range-bound option

selling strategies are advised.

MARKET INTERNALS:

Market Breadth Indicators – Volume and Delivery Volume Expansion, Open Interest

Expansion and Contraction, Advance/Decline Ratio, 52 Week Highs/Lows.

Open Interest Expansion and Contraction Rules –

1. Price Up and Open Interest Up – Long Buildup

2. Price Up and Open Interest Down – Profit Taking

3. Price Down and Open Interest Up – Short Buildup

4. Price Down and Open Interest Down – Short Covering.

SECTOR AND STOCK SELECTION:

Defensive stocks have low to moderate beta in sectors like FMCG, Healthcare, IT, Cement,

Telecom.

Cyclical stocks have high beta like Financials and Rate Sensitives like Auto, Infrastructure,

Realty.

Stock Selection – Invest in the constituents from broadbased indices like Nifty, Junior Nifty

and Midcap as well as constituents of Sectoral Indices like Auto, Banking, Capital Goods, IT,

FMCG, HC etc.

Alpha Strategies - Long Stock and Short Index( Outperformance) or Short Stock and Long

Index ( Underperformance).

Pair Strategies - Long Stock and Short Stock within the same sector.

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322

7. Disclaimer

This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or

redistributed to any other person. Persons into whose possession this document may come are required to observe these restrictions.

This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report

is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or

solicitation would be illegal. It is for the general information of clients of Keynote Capitals Ltd. It does not constitute a personal

recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients.

We have reviewed the report, and in so far as it includes current or historical information, it is believed to be reliable though its

accuracy or completeness cannot be guaranteed. Neither Keynote Capitals Ltd., nor any person connected with it, accepts any liability

arising from the use of this document. The recipients of this material should rely on their own investigations and take their own

professional advice. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide

for future performance. Certain transactions -including those involving futures, options and other derivatives as well as non-investment

grade securities - involve substantial risk and are not suitable for all investors. Reports based on technical analysis centers on studying

charts of a stock’s price movement and trading volume, as opposed to focusing on a company’s fundamentals and as such, may not

match with a report on a company’s fundamentals.

Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a

reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us

from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be

subject to change without notice. Our proprietary trading and investment businesses may make investment decisions that are

inconsistent with the recommendations expressed herein.

We and our affiliates, officers, directors, and employees world wide may: (a) from time to time, have long or short positions in, and buy

or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities

and earn brokerage or other compensation or act as a market maker in the financial instruments of the company (ies) discussed herein

or act as advisor or lender / borrower to such company (ies) or have other potential conflict of interest with respect to any

recommendation and related information and opinions.

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the

subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly

related to specific recommendations or views expressed in this report.

No part of this material may be duplicated in any form and/or redistributed without Keynote Capitals Ltd’s., prior written consent.

Keynote Capitals Ltd.

th

The Ruby, 9 Floor, Senapati Bapat Marg, Dadar (W), Mumbai, India – 400028. Tel: 3026 6000 / 2269 4322