Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Should Your Marketing Manager be doing Your Cost Accounting? 160428

Similar to Should Your Marketing Manager be doing Your Cost Accounting? 160428 (20)

Recently uploaded

Recently uploaded (20)

Should Your Marketing Manager be doing Your Cost Accounting? 160428

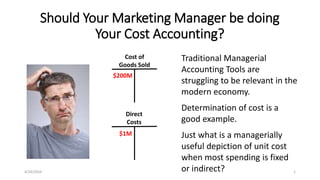

- 1. 4/28/2016 1 Should Your Marketing Manager be doing Your Cost Accounting? Traditional Managerial Accounting Tools are struggling to be relevant in the modern economy. Determination of cost is a good example. Just what is a managerially useful depiction of unit cost when most spending is fixed or indirect? Cost of Goods Sold Direct Costs $200M $1M

- 2. 4/28/2016 2 Should Your Marketing Manager be doing Your Cost Accounting? A firm’s Marketing Department(s) may have cost knowledge and information that is more relevant and useful than does the Accounting Department -- and these Marketing personnel probably don’t even know it!

- 3. Exactly correct but entirely irrelevant. An accountant? Financial Accounting = Rule-based reporting to investors Tax Accounting = Rule-based reporting to the authorities Managerial Accounting Business Modeling = Do what the business requires – be cognizant of context; be relevant and accepted by all elements within the business [Managerial Accounting is also called Cost Accounting] Oxymoron: an accounting joke 4/28/2016 3 Should Your Marketing Manager be doing Your Cost Accounting?

- 4. 4/28/2016 4 Financial (rule-based) Tax (rule-based) Managerial (free form) Managerial Accounting needs to be relevant…it must effectively model the business. Managerial Accounting should take primacy over Financial and Tax Accounting. Some/many Financial Accounting and Tax Accounting rules may be disregarded by the Managerial process (and accounted for after-the-fact). Financial vs Tax vs Managerial Accounting

- 5. Should Your Marketing Manager be doing Your Cost Accounting? Consider a new 10 nanometer semiconductor fab: • $10B of Capital (!) • Lights Out Manufacturing – almost no direct labor • Significant maintenance and other indirect labor • Small direct materials costs as % of total 4/28/2016 5

- 6. Should Your Marketing Manager be doing Your Cost Accounting? 4/28/2016 6 In this scenario, traditional accounting is almost entirely an exercise in allocating depreciation and overhead to volumes in an arbitrary manner Useful? Does this support good decision- making?

- 7. Should Your Marketing Manager be doing Your Cost Accounting? The divergence of Managerial need versus Rule-based Accounting methods is large and growing. This is everybody’s future: ever-smaller % of costs that vary directly with unit volume. So, what is the “Cost” of running a wafer through this fab plant? Sidebar: If direct costs still predominate in your company, are you behind technologically? Are you an easy competitive target? 4/28/2016 7

- 8. 4/28/2016 8 Should Your Marketing Manager be doing Your Cost Accounting? The overwhelming “cost” in this 10 nanometer semiconductor fab is for capacity. These costs are largely fixed. There’s almost no correlation between the true costs of capacity and factory volume, at least as traditionally measured. The true cost of committing or utilizing capacity is an Opportunity Cost – i.e., capacity becomes unavailable for other uses. What are these other uses? Who is most knowledgeable of these other uses? Opportunity Cost, where there’s a capacity shortfall, is cash margin generated (foregone) per scarce unit of capacity.

- 9. Should your Marketing Manager be doing your cost accounting? YES, or at least have involvement Managerial Accounting is too important to be left to the Accountants! 4/28/2016 9 Should Your Marketing Manager be doing Your Cost Accounting? Who is most knowledgeable of these other uses of Capacity? Your Marketing Manager!

- 10. 0 20 40 60 80 100 120 140 160 180 200 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Forecast Plant Loading vs Capacity Capacity Forecast Loading 4/28/2016 10 Should Your Marketing Manager be doing Your Cost Accounting? Excess Capacity Capacity Shortfall Consider: Build-Ahead Build-Ahead

- 11. 4/28/2016 11 Should Your Marketing Manager be doing Your Cost Accounting? 0 20 40 60 80 100 120 140 160 180 200 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Forecast Plant Loading vs Capacity Capacity Forecast Loading The Marketing Manager(s) (or Department), by virtue of owning the Forecast Loading line and Pricing, is defining the Capacity Cost. Opportunity Cost per unit, where there’s a capacity shortfall, is cash margin generated (i.e., foregone) per scarce unit of capacity.

- 12. 4/28/2016 12 Should Your Marketing Manager be doing Your Cost Accounting? Can Opportunity Cost be Measured/Forecasted? Can Opportunity Cost be integrated into a Firm’s Everyday Management Information and Routines? 0 20 40 60 80 100 120 140 160 180 200 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Forecast Plant Loading vs Capacity Capacity Forecast Loading

- 13. 4/28/2016 13 Should Your Marketing Manager be doing Your Cost Accounting? Organizational Design complicates things further… Plant A Plant B Plant C Cost Centers Profit CentersProfit Centers #6 #7 #8 #1 #2 #3 #4 #5 • Profit Centers and Cost Centers are distinct • Each P&L Center likely has its own Marketing Manager • Traditional managerial accounting tools are hapless • How do you “charge” a Profit Center for Capacity Costs?

- 14. 4/28/2016 14 Should Your Marketing Manager be doing Your Cost Accounting? So, how do you “charge” a Profit Center for Capacity Costs? How do you construct business information and processes that create the correct incentives/disincentives, while being understandable and manageable? One approach: don’t explicitly charge the Profit Centers at all. No Charge? It’s Free?

- 15. 4/28/2016 15 Should Your Marketing Manager be doing Your Cost Accounting? Charge Profit Centers only for the that small amount of direct cost. Ration constrained capacity via the Available-to-Promise (ATP) and Order Promising functions -- i.e., Ration based upon cash margin per scarce unit of capacity. 50 50 50 50 50 50 50 50 50 50 50 45 45 40 40 40 30 30 20 20 10 10 0 0 25 25 25 25 25 25 25 25 25 25 25 25 30 30 30 30 30 30 30 30 40 40 50 50 56 45 44 66 56 76 56 39 58 66 45 77 78 77 59 59 72 77 20 20 25 20 25 20 0 20 40 60 80 100 120 140 160 180 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec CAPACITY SUPPORT FOR PROFIT CENTER #1 Contractual Strategic Rationed Capacity is constrained starting in July. This profit center (i.e., #1) has poorer margins per unit of scarce capacity than do other profit centers competing for capacity and consequently receives diminished support Capacity Constraint deemed to start here

- 16. 4/28/2016 16 Should Your Marketing Manager be doing Your Cost Accounting? 50 50 50 50 50 50 50 50 50 50 50 45 45 40 40 40 30 30 20 20 10 10 0 0 25 25 25 25 25 25 25 25 25 25 25 25 30 30 30 30 30 30 30 30 40 40 50 50 56 45 44 66 56 76 56 39 58 66 45 77 78 77 59 59 72 77 20 20 25 20 25 20 0 20 40 60 80 100 120 140 160 180 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec CAPACITY SUPPORT FOR PROFIT CENTER #1 Contractual Strategic Rationed Capacity Constraint deemed to start here This particular approach may or may not work for a particular business – or maybe not for any business – but demonstrates a departure from traditional accounting- based managerial approaches. In other words, the generalization is the point Can existing ERP / ATP (Available-to-Promise) tools accommodate?