8 Major Trends in the first half of 2016 - Chicagoland market update

•

1 gefällt mir•374 views

Click a slice of the wheel to learn more on Chicagoland's office market in the first half of 2016

Empfohlen

Weitere ähnliche Inhalte

Mehr von Hailey Harrington

Mehr von Hailey Harrington (8)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

8 Major Trends in the first half of 2016 - Chicagoland market update

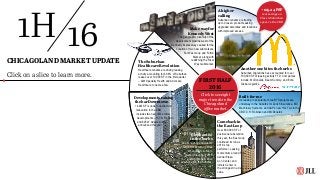

- 1. A higher calling Suburban tenants are trading up to Class A product seeking upgraded amenities and locations with improved access. Comeback in the East Loop Over 600,000 SF of positive net absorption this year, the East Loop continued its run as 2016’s top performer. Leasing momentum around Pru- dential Plaza, Aon Center, and Illinois Center is the strongest in a de- cade. Elephant(s) in the burbs An abundance of available large blocks with a series scheduled to come to market throughout 2016 could potentially drive vacancy up in the Suburbs. Developments raising the bar Downtown +4.4M SF is under construction/ renovation in the CBD, includes two new office tower developments – 151 N Franklin and 625 W Adams both announced this year. The Suburban Healthcare Revolution Healthcare tenants are driving leasing activity accounting for 40.8% of Suburban leases over 10,000 SF in the first quarter – AIM Specialty Health and Advocate Healthcare to name a few. Make way for Kennedy West The geographic diversity of the development pipeline west of the Kennedy Expressway caused for the creation of two new submarkets, Far West Loop and Fulton Market, along with redefining the River West submarket. Another one bites the burbs Suburban migrations have accounted for over 700,000 SF of leasing activity YTD. Companies include: McDonalds, Beam Suntory, and Echo Global Logistics. Built-for-me Increasing in popularity, three BTS projects are underway in the Suburbs for Zurich Insurance, MC Machinery Systems, and AAP’s new HQ. Two in the CBD: C.H. Robinson and McDonald’s. + $15.24 PSF rent savings on Class A Suburban space vs. the CBD FIRST HALF 2016 Click to see eight major trends in the Chicagoland office market. 1H 16CHICAGOLAND MARKET UPDATE Click on a slice to learn more.

- 2. ii. iii. iv. v. vi. vii. viii. a higher calling 777 Big Timber Road, Elgin 2703 Van Buren Street, Bellwood 3800-3850 N Wilke Road, Rolling Meadows 1900 Spring Road, Oak Brook 1205 E Algonquin Road, Schaumburg 6400 Shafer Court, Rosemont 1701 Golf Road, Rolling Meadows 1415 W 22nd Street, Oak Brook 1400 American Lane, Schaumburg 3025 Highland Parkway, Downers Grove 1501 Woodfield Road, Schaumburg 1315 W 22nd Street, Oak Brook Verizon 160,000 SF SMACNA 2,000 SF Paylocity 309,000 SF Veritas 8,120 SF MECU 28,000 SF Command Akon 11,195 SF i. a higher calling Many premier suburban office campuses have gotten some fresh touches, including new fitness centers, on-site cafés, restored outdoor spaces and other amenities, all designed to satisfy tenant demand. Those trading up have lately proved a draw to closer freeway access and proximity to downtown. HOME

- 3. i. iii. iv. v. vi. vii. viii. another one bites the burbs River West 0.53% River North 20% N. Michigan Ave 1% East Loop 8% Central Loop 5% West Loop 65% Evanston Uptown Northbrook Morton Grove Highland Park Deerfield Bannockburn Northfield Ravenswood Arlington Heights Elk Grove Village Libertyville Schaumburg Lake Forest Bensenville Itasca O’Hare Hoffman Estates GlenviewMount Prospect Lombard Oakbrook Downers Grove Naperville Hinsdale Lisle Warrenville Homewood Mokena Mettawa Riverwoods Rolling Meadows 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 3132 33 34 35 36 37 38 39 40 41 42 43 44 45 financial services retail trade law firm education health care leisure oil & gas transportation & utilities information technology business services manufacturing other annual migration leases in square feet 281,000 1,131,000 27,200 70,000 861,000 853,800 1,329,900 1,211,111 2008 2009 2010 2011 2012 2013 2014 2015 34% CLASS A WHERE DID THEY GO? RECEIVED INCENTIVES State or city 49% CLASS B 51% River West 0.53% 26,473 SF River North 20% 1,009,700 SF N. Michigan Ave 1% 53,000 SF East Loop 8% 420,400 SF Central Loop 5% 258,150 SF West Loop 65% 3,263,611 SF Evanston Uptown Northbrook Morton Grove Highland Park Deerfield Bannockburn Northfield Ravenswood Arlington Heights Elk Grove Village Libertyville Schaumburg Lake Forest Bensenville Itasca O’Hare Hoffman Estates GlenviewMount Prospect Lombard Oakbrook Downers Grove Naperville Hinsdale Lisle Warrenville Homewood Mokena Mettawa Riverwoods Rolling Meadows 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 3132 33 34 35 36 37 38 39 40 41 42 43 44 45 SUBURBAN MIGRATION April 2016 # Company Address RSF 2008 1 Thomson Reuters 1 N Dearborn 41,000 2 BP 10 & 30 S Wacker 240,000 2009 3 Combined Insurance 111 E Wacker 100,000 4 Silliker 111 E Wacker 33,000 5 PCM Logistics 300 S Riverside 28,000 6 United Airlines 233 S Wacker 830,000 7 Willis Group Holdings 233 S Wacker 140,000 2010 8 Bel Brands 10 & 30 S Wacker 27,200 2011 9 UHC 155 N Wacker 70,000 2012 10 Catamaran 300 N LaSalle 25,000 11 DeVry University 300 S Riverside 75,000 12 Maximus 303 E Wacker 70,000 13 W.W. Grainger 500 W Madison 58,000 14 Motorola Mobility Merchandise Mart 604,000 15 Zones 233 S Wacker 29,000 2013 16 Gogo Wireless 111 N Canal 232,000 17 Walgreens Co. 120 S Riverside 26,000 18 Presence Health 200 S Wacker 44,000 19 Guggenheim Partners 227 W Monroe 38,000 20 Great American Insurance 300 S Wacker 100,000 21 Discover 350 N Orleans 26,000 22 Hillshire Brands 400 S Jefferson 233,000 23 Nokia Xpress 425 W Randolph 32,500 24 Marketing Store Worldwide 55 W Monroe 31,300 25 Legal & General Investment Management America Inc. 71 S Wacker 26,000 26 Capital One 77 W Wacker 65,000 # Company Address RSF 2014 27 Assurance Agency 111 N Canal 27,000 28 AT&T 225 W Randolph 53,000 29 Newark Corp. 300 S Riverside 80,000 30 FGMK 333 W Wacker 26,200 31 Kraft 401 N Michigan 30,000 32 Fusion92 440 W Ontario 25,700 33 SAC Wireless 540 W Madison 40,000 34 Scor S.E. 233 S Wacker 30,000 2015 35 Horizon Pharma 150 S Wacker 65,111 36 Kraft Heinz 200 E Randolph 170,000 37 Stats 203 N LaSalle 70,000 38 Zurich 300 S Riverside 100,000 39 Mead Johnson 444 W Lake 75,000 40 Motorola Solutions 500 W Monroe 150,000 41 Baxalta 540 W Madison 83,000 42 ConAgra Merchandise Mart 210,000 2016 43 Allstate Merchandise Mart 45,000 44 BP 30 S Wacker 40,000 45 Beam Suntory Merchandise Mart 100,000 All leases less than 25,000 RSF 387,323 TOTAL 5,031,334 River West 0.53% 26,473 SF River North 20% 1,009,700 SF N. Michigan Ave 1% 53,000 SF East Loop 8% 420,400 SF Central Loop 5% 258,150 SF West Loop 65% 3,263,611 SF Evanston Uptown Northbrook Morton Grove Highland Park Deerfield Bannockburn Northfield Ravenswood Arlington Heights Elk Grove Village Libertyville Schaumburg Lake Forest Bensenville Itasca O’Hare Hoffman Estates GlenviewMount Prospect Lombard Oakbrook Downers Grove Naperville Hinsdale Lisle Warrenville Homewood Mokena Mettawa Riverwoods Rolling Meadows 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 3132 33 34 35 36 37 38 39 40 41 42 43 44 45 SUBURBAN MIGRATION April 2016 # Company Address RSF 2008 1 Thomson Reuters 1 N Dearborn 41,000 2 BP 10 & 30 S Wacker 240,000 2009 3 Combined Insurance 111 E Wacker 100,000 4 Silliker 111 E Wacker 33,000 5 PCM Logistics 300 S Riverside 28,000 6 United Airlines 233 S Wacker 830,000 7 Willis Group Holdings 233 S Wacker 140,000 2010 8 Bel Brands 10 & 30 S Wacker 27,200 2011 9 UHC 155 N Wacker 70,000 2012 10 Catamaran 300 N LaSalle 25,000 11 DeVry University 300 S Riverside 75,000 12 Maximus 303 E Wacker 70,000 13 W.W. Grainger 500 W Madison 58,000 14 Motorola Mobility Merchandise Mart 604,000 15 Zones 233 S Wacker 29,000 2013 16 Gogo Wireless 111 N Canal 232,000 17 Walgreens Co. 120 S Riverside 26,000 18 Presence Health 200 S Wacker 44,000 19 Guggenheim Partners 227 W Monroe 38,000 20 Great American Insurance 300 S Wacker 100,000 21 Discover 350 N Orleans 26,000 22 Hillshire Brands 400 S Jefferson 233,000 23 Nokia Xpress 425 W Randolph 32,500 24 Marketing Store Worldwide 55 W Monroe 31,300 25 Legal & General Investment Management America Inc. 71 S Wacker 26,000 26 Capital One 77 W Wacker 65,000 # Company Address RSF 2014 27 Assurance Agency 111 N Canal 27,000 28 AT&T 225 W Randolph 53,000 29 Newark Corp. 300 S Riverside 80,000 30 FGMK 333 W Wacker 26,200 31 Kraft 401 N Michigan 30,000 32 Fusion92 440 W Ontario 25,700 33 SAC Wireless 540 W Madison 40,000 34 Scor S.E. 233 S Wacker 30,000 2015 35 Horizon Pharma 150 S Wacker 65,111 36 Kraft Heinz 200 E Randolph 170,000 37 Stats 203 N LaSalle 70,000 38 Zurich 300 S Riverside 100,000 39 Mead Johnson 444 W Lake 75,000 40 Motorola Solutions 500 W Monroe 150,000 41 Baxalta 540 W Madison 83,000 42 ConAgra Merchandise Mart 210,000 2016 43 Allstate Merchandise Mart 45,000 44 BP 30 S Wacker 40,000 45 Beam Suntory Merchandise Mart 100,000 All leases less than 25,000 RSF 387,323 TOTAL 5,031,334 rent premium on office space in the CBD compared to the suburbs 56.3% Click the image to view our Suburban Migration research website ii. another one bites the burbs Seeking millennial talent and central locations, several suburban companies have relocated downtown catering to the new generation of urbanites reshaping the workplace. Suburban migration began with United Airlines in 2008, and has continued in waves through 2016. A slew of corporate relocations drove demand early this year, most notably - McDonald’s moving their corporate headquarters to Fulton Market, an area some observers consider emerging. With no slowdown in sight, we expect to see other companies looking carefully at their location strategies. HOME

- 4. i. ii. iv. v. vi. vii. viii. built-for-me iii. built-for-me Nearing completion, Zurich Insurance regional headquarters coincides with the construction of a number of build-to-suit projects that are infusing new life along the I-90 corridor in the Northwest submarket. CHALLENGE • Zurich was occupying 880,000 square feet of the space in two separate office towers with small, 20,000-square-foot floors. Zurich was seeking a transformation in both its branding and workplace • JLL’s greatest challenge on the project was the coordination of all activities such that delivery of the new headquarters matched the expiration of Zurich’s current lease CUSTOMIZED SOLUTION • The property will be a cutting edge Class A+ office campus with a high LEED Core & Shell Certification. • The building will offer a façade clad in articulated glass and stainless steel, office park amenities, a well appointed landscaped setting and ample covered garage parking • Sustainability initiatives include green roofs, native/ adaptive plants with water capture, low-flow fixtures, low VOC paints, FSC certified wood, weather-tight building envelope, and on-site CHP generator • JLL is providing advisory services on tax & accounting implications, location selection, developer selection, development capital procurement, sustainability program development and lease negotiation RESULTS • Successfully arranged site selection, developer selection, $350 million of capital procurement and construction management • Zurich began construction of the new campus in 3Q 2014. Lease commencement and rent commencement are estimated to be September 2016 and December 2016, respectively CLIENT PROFILE Industry: Insurance Geography: Schaumburg, IL Square Footage: 750,000 SF Schedule: Estimated 3Q 2016 Year completed: 2016 Budget: $340M Services Provided: Project Management Core & Shell, Tenant Interiors and Sustainability Zurich American Insurance Company North American Headquarters build-to-suit Zurich American Insurance Company planned to build and relocate to a new, North American headquarters. JLL was tapped for advisory services on tax and accounting implications, location selection, developer selection, development capital procurement, sustainability program development and lease negotiation. HOME

- 5. i. ii. iii. v. vi. vii. viii. comeback in the east loop iv. comeback in the east loop With tenants from the suburbs and the loop streaming into the East Loop, leasing momentum around Prudential Plaza, Aon Center, and the Illinois Center is the strongest in a decade. Hitting record lows in vacancy, the submarket has inspired a resurgence in tenant and investor demand to the area that’s coming back. Certainly, there is no more exciting example than the transformation of Prudential Plaza. Property repositioning case study – Prudential Plaza 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% $10.00 $14.00 $18.00 $22.00 $26.00 $30.00 2013 2014 2015 2Q 2016 4Q2016 Average Asking Rent 130 E Randolph Vacancy 180 N Stetson Vacancy 64% $15 Net $27 Net 10% 10% Skydell, Karasick, & Silberberg (601 W Company JV Berkeley Properties) recapitalizes the two buildings with $100.0M equity infusion, taking over the asset. Perceived as ‘zombie’ project in the market - One Pru. has had persistent high vacancy. Ownership confirms two-building complex renovations to include: • New lobby & upgraded plaza area • Tenant amenity floor with rooftop deck • Conference facility • Private shuttle service Cision US leases 49,464 SF @ One Pru. – first big tenant to lease with new ownership Ownership starts $85.0M in renovations – marketing focuses on the tenant amenity 11th floor @ One Pru, which includes: • 12,000 SF fitness center, • 7,000 SF tenant clubhouse, • 13,000 SF rooftop deck. Time Inc. leases 18,822 SF @ One Pru. - rent is $21.00/Net SF. Pandora Media leases 32,500 SF – doubling its Midwest presence – rent is $20.00/Net SF Clark Hill leases 72,000 SF – doubling its Chicago footprint – rent it $26.00/Net SF Ownership refinances the office complex with a 10-year, $415.0M loan from German American Capital replacing $410.0M in CMBS debt on the properties. Tenant amenity & lobby remodel complete – building has captured +700,000 SF of leasing in the past 24-months. ZS Associates renewed 19,879 SF at Two Pru – 2017 commencement - rent it $27.00/Net SF Move-in’s from Clark Hill, University of Chicago, among others will drive vacancy at the office complex to its lowest level since 2005. HOME

- 6. i. ii. iii. iv. vi. vii. viii. elephant(s) in the burbs v. elephant(s) in the burbs The Chicago suburbs abound with large corporate campuses, which are a relic from another era. Despite steady tenant demand, these dinosaur campuses are likely to stay vacant – unless they’re repositioned. Senior housing and daycare facilities will be in higher demand than office space, and converting some of the obsolete office product to alternative uses make financial and environmental sense. The total rentable inventory of suburban Chicago office properties is approximately 96.8 million square feet. At the current overall vacancy rate of 18.9%, the Chicago suburbs have 18.3 million square feet of empty office space. However, while all submarkets have varying supply and demand patterns, vacancy in the Chicago suburbs is significantly concentrated in a specific subset of properties that are functionally obsolete; skewing the overall market statistics. SHOWING THEIR AGE With this criteria applied, our analysis indicates an estimated 11.3 million-square-feet of the total suburban office inventory is vacant and functionally obsolete. Across the Chicago suburbs, there are hundreds of buildings that were built during the 1980s and are beyond their useful life, as indicated in this chart. Taking out the stock of functionally obsolete properties, the adjusted vacancy rate for tenant attractable properties is around 7% placing the Chicago suburbs on par with places like San Francisco, Portland and Nashville. While some may question the exact metrics of this analysis, most will acknowledge the difficulty in attracting employees in their twenties to buildings that are in their late thirties. With this in mind, it appears the suburban vacancy challenge will only improve if a large volume of obsolete inventory is removed entirely from the market. This means that it’s time for new ideas. THINKING OUTSIDE THE BOX: New Vision for Aging Suburban Office Buildings Adaptive reuse and repositioning of former office campuses could significantly reduce the suburban vacancy rate. In Downtown Chicago, office building conversions are standard practice. These conversions have contributed to a decline in vacancy while achieving the highest and best use of buildings, considering the current market demand. Even though suburban conversions remain quite rare. JLL has identified alternative uses for a few properties that may have greater potential than traditional office use. (next page) 18.3M SF That’s the equivalent of the entire office market inventory of Charlotte, NC. Of vacant office space in the Chicago suburbs NEW IDEAS FOR OLD BUILDINGS: 600 1950-1959 1960-1969 1970-1979 1980-1989 1990-1999 2000-2009 2010-Present 50M 45M 40M 35M 30M 500 25M 400 20M 300 15M 200 10M 100 5M 0 0 BuildingCount TotalSquareFeet Count Total SF Suburban Chicago Office Buildings Built by Decade In order to better understand the “true” vacancy in the suburbs, JLL identified the properties that are no longer in consideration for most tenants. For the purposes of this analysis, we defined properties with the following characteristics as functionally obsolete: 1. Constructed prior to 1990, or without any significant improvements since 1990, and 2. Vacant and available for three years or longer 90, 98 AND 100 HALF DAY RD, LINCOLNSHIRE 343,000 square feet, 95% vacant 1960 LUCENT LANE, NAPERVILLE 516,000 square feet, 50% vacant 1203 WARRENVILLE ROAD, LISLE 124,000 square feet, 100% vacant 2000 LAKEWOOD, HOFFMAN ESTATES 1,600,000 square feet, 100% vacant With an incredible, 43-acre parcel of land, this site has potential well beyond office use. Even with a full-scale development, there is sufficient space for a developer to set aside much of the heavily-wooded land for a nature preserve with wetlands, trails, and walking paths. While the office vacancy rate in North Lake county is over 22%, the demand for affordable residential options is increasing. This implies that market rate units with the right mix of amenities will maximize the potential of this site before a corporate occupier can be found. Furthermore, the Village of Lincolnshire has expressed a willingness to cooperate with a creative owner on the redevelopment of the property. DuPage County is forecast to have a population of over 153,000 seniors by 2020, and this aging cohort will require a range of additional assisted living facilities that do not exist today. Rather than constructing new facilities on undeveloped land, why not convert an existing office campus into this use? Suburban office campuses like the former Alcatel-Lucent building already contain many key senior housing amenities nearby, including: cafeterias, fitness centers, parking lots, and accessibility. At a fraction of ground-up development costs, the building could be converted to senior housing and independent living spaces. This would simultaneously benefit the community and the office market. Suburban office buildings will need to accommodate occupiers in new ways as millennials begin to have children and demand that their workplace adapts. Today, gyms and cafeterias are key tenant amenities, yet five years from now, the desired amenities may be in-office daycare or employer provided pre- schools. Owners with more than 30% vacancy in a given property might be wise to consider the conversion of a floor or several floors into a childcare amenity. While serving as a key amenity for suburban tenants, daycare within office buildings could reduce absenteeism, employee attrition, and even greenhouse gas emissions. Located near the transition point between suburban zoning and farm land, this campus is perfectly positioned to be used for the emerging global trend of indoor agriculture and farming. In one proposal, the massive 1,300,000 square-foot office building could be converted into a multi-level urban farm using varying hydroponic systems to grow fruits, vegetables, and garden plants. Local residents could lease space out for their own gardens, and large corporations could use the facility as a test lab for indoor growing and crop testing in a year-round environment. In the 287,000 square foot building, 50% of the space could be maintained as office space for lab employees. The remaining portion could be converted into an agricultural research and development laboratory. With proximity to some of the world’s largest food service companies and farming experts, the vacant space could be put to immediate use. The existing auditorium on the campus could be kept in place for use by speakers and conferences on agricultural research and the future of food. A partnership with the University of Illinois College of Agriculture could turn this empty office campus into an internationally recognized center for solving the world’s hunger challenge. These conversion options are just a sample of the significant potential that exists across the Chicago suburbs. With creative thinking and careful execution, the suburbs can be positioned to attract new talent and new occupiers to the region. Do you have additional ideas for solving the suburban vacancy challenge? Please send them to: Christian.Beaudoin@am.jll.com or Hailey.Harrington@am.jll.com ©2016 Jones Lang LaSalle IP, Inc. All rights reserved. 59002 Former use: Single-tenant headquarters Proposed use: Mixed-use with residential, retail, and educational components Former use: Single-tenant headquarters Proposed use: Assisted living facility and senior care housing Former use: Traditional office, flex space Proposed use: Maintain 50% office, and convert 50% to daycare facility Former use: Single-tenant headquarters Proposed use: Build an urban farming hub HOME

- 7. i. ii. iii. iv. v. vii. viii. developments raising the bar downtown Click the image to view our Chicago 2025 research website vi. developments raising the bar downtown The West Loop, studded with high-rise office towers and construction cranes along the riverfront, will soon have two more towers in this development cycle: John Buck’s 151 N Franklin Street anchored by CNA and White Oak JV CA Venture’s spec tower, 625 W Adams scheduled to both deliver by mid-2018. Adding to the appeal of downtown is nearby The Old Post Office, an ambitious 2.5-million-square-foot development project filled with office space, shops and restaurants, and rooftop public space. To keep new supply and demand in balance, the Chicago market will have to maintain near record absorption levels over the next two years to match the current construction pipeline. CHICAGO 2025 11 Development Timeline Chicago is a city of big plans and big projects. Over the next ten years, the city will grow upward with new developments. But mostly, Chicago will grow outward into new submarkets, as companies continue to seek larger floor plates, access to talent and flexibility in design. no small plans fulton market river west goose island clybourn corridor 2016 2025 HOME

- 8. i. ii. iii. iv. v. vi. viii. the suburban healthcare revolution vii. the suburban healthcare revolution The Chicago suburbs have long been home to some of the world’s largest healthcare and pharmaceutical firms. The region provides incredible access to an experienced talent base, a connected hospital network, and the nation’s top universities. In 2016, healthcare-related tenants have driven leasing activity in many submarkets, representing 41% of the leases over 10,000 square feet. As the industry consolidates, we expect continued activity, especially in the North and Northwest submarkets. HOME

- 9. i. ii. iii. iv. v. vi. vii. make way for kennedy west viii. make way for kennedy west Kennedy West used to be known for its seedy industrial and wholesale food markets; now, the area is home to tech giant, Google and a recent construction burst of boutique hotels like the Ace and Hoxton Hotel. Comprised of three submarkets – Far West Loop, River West, & Fulton Market - Kennedy West is remaking itself into one of Chicago’s premier destination. Office Retail HotelResidential Redevelopment KEY Randolph West • Former Harpo Studios site, 550,000 SF. redevelopment planned by Sterling Bay. • Built-to-suit opportunity, with full build out of 3-4 years. Proposed plan includes 488,000 SF. creative office, 63,000 SF. retail space, and 200-stall enclosed parking. 450 N Morgan • Five-story, 50,000 SF. commercial building development planned by MAB Dev. • Mixed-use building includes 24,000 SF. office space, 6,500 SF. ground floor retail, and 50 car indoor parking. Expected delivery in 4Q 2016. Fulton West • .5-acre site with +/-1 m.s.f. of new development capacity planned by Sterling Bay. • First phase of construction expected to deliver in April 2017. The first phase focuses on 296,000 SF. of modern office and retail space in a nine-story newly constructed building. Second phase in the adjacent parcel will add +/-600,000 SF. of office and retail space. Ace Hotel • 159 rooms, • 167,000 SF. building capacity • 2018 completion 215 N Peoria • Shapack purchased development parcel mid-block on between Lake and Fulton totaling 13,000 SF. of land with +/-120,000 buildable SF. in 2013. • Planned 11-story plus penthouse office building with ground retail & indoor parking. Hoxton Hotel • 175 rooms, 11-story hotel • 2018 completion NobuHotel • 93 rooms, seven-story plus penthouse • Construction begins late 2016 HOME

- 10. i. ii. iii. iv. v. vi. vii. viii. Thank you. for more information on this presentation please contact: Hailey Harrington Senior Research Analyst 312-228-3189 hailey.harrington@am.jll.com Shaina Nielson Senior Graphic Designer 312-228-2141 shaina.nielson@am.jll.com HOME