1. CHINA GLOBAL ANALYSIS INC

ARGENTINA: A RISKY BUSINESS

We see Argentina as a risky country due to

inflationary pressure and currency controls.

This deeply influences industrial production,

causing a shortage of some consumption

goods and the consumer prices to increase.

Argentinian economy is mostly based on

Services (62.98% of 2011 GDP, Statista.com),

but also the Industry and Manufacturing

sectors and Agriculture play a significant role.

Due to lack of agreements with the “vulture

funds”, China and Argentina have signed pacts

to provide the latter with USD11bn from

China’s Central bank. Moreover in February

the two countries closed a key contract to

enhance partnerships for aerospace

technology, agriculture, infrastructure, and

telecom projects in the third largest economy

of South America (Euler Hermes).

Over the years, China has increased its

footprint in Argentina. In particular China has

major interests in the green gold (soybeans)

and in the black gold (crude oil) (Forbes).

-5

-4

-3

-2

-1

0

1

2

3

4

2013 2014 2015e 2016f 2017f 2018f

REAL GDP GROWTH (%)

Developing Latin America and the Caribbean Argentina Brazil Mexico

IN BRIEF

• Risk from shocks in international trade.

• Dependency on the prices of agricultural

commodities.

• China’s influence: 6% exports, 14.5%

imports (doubled over the years).

• Standard and Poor’s raising rating to B- due

to positive expectations on Macri’s reforms.

• No access to International financial markets

since 2001.

• The lack of majority in the Congress is a

significant obstacle for Macri’s reforms.

• Brazil, the leading export partner, has to deal

with a difficult economic situation causing a

slowdown in demand.

• Currency swap with China to stabilize Peso.

Source: Doing business 2016, World Bank

2. CHINA GLOBAL ANALYSIS INC

As reported by Washington Post after former President

Kirchner met with Xi Jinping, China and Argentina are

hardly working on the deepening of their strategic

relationship.

Chisa has heavily invested in the Latin American

country, building dams, railways and two nuclear plants

(up to $15bn according to Financial Times), which

could fill the void of governmental investments.

Agreements signed also include travel visas,

information technology, financing.

These big steps are part of Chinese strategy which aims

at investing in problem states, especially in Latin

America. This would secure allies, clients and resources

to Beijing, in a long-term view.

Argentina, with a GDP of more than 540B USD, is the

third largest economy in Latin America.

This significant role is the result of the growing

importance and international footprint of its two main

strengths: large-scale agricultural and livestock

industry.

To register a steady growth over the past decades,

Argentina has invested significantly in health and

education, areas accounting repectively for 8% and 6%

of GDP (World Bank).

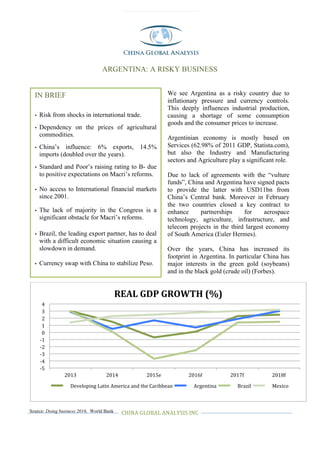

In recent months, the worsening economic situation in

Brazil (the main trade partner) and the inflationary

pressure have deteriorated country’s fiscal situation. During the first half of 2015, the primary

deficit rose to 1% of GDP and the fiscal deficit increased to 2.3% of GDP, the double respect to one

year ago. To conclude, due to the risky scenario the government had to deal with, the growth for

2015 is expected at about 0.5%.

BANKING ENVIRONMENT

Present financial structure is in force since 1977 Financial Entities Law; its aim was to consolidate

the system (approx. 80 entities) and make it safer through a guarantee on deposits, even if country

default makes us doubtful. The system is regulated by the central bank, Banco Central de la

República Argentina.

We noted that ICBC, China’s biggest bank has an Argentinian branch, as HSBC does. Banking

environment is mainly free, as there are no restrictions for foreign institutions and investors (Doing

Business in Argentina, PwC). However, local financing is costly since interest rates are still high.

Law enforcement is efficient, but uncertainty and lack of confidence about governmental decisions

mine the system at its core pillar. However we believe foreign international banks like CITI, HSBC

and the aforementioned ICBC could fill the gap with their experience and international network.

• Population: 41,800,000

• GDP per capita 2014:

US $12,509.5.

• Exchange rate:

1 USD=14.85 ARS.

• Inflation, GDP deflator

(annual%): on average

29.3% during the

period 2011-2015.

• Current account

balance: -1.0% of GDP

in 2014.

• Trade balance

(monthly, million

USD): actual -160,

previous -1100

MACROECONOMIC

OVERVIEW

3. CHINA GLOBAL ANALYSIS INC

ARGENTINA COUNTRY & EQUITY RISK PREMIUM

Rating-based assessment

Argentina’s bad reputation among international investors keeps high its perceived country

risk. It shows among the highest ERP in the whole continent, even higher than Ecuador

(16.30%) but still lower than Venezuela (21.69%).

Moody’s rating Country Risk

Premium

Equity Risk

Premium

Argentina Caa1 11.55% 17.80%

Venezuela Caa3 15.44% 21.69%

Ecuador B3 10.05% 16.30%

Brazil Baa3 3.39% 9.64%

Chile Aa3 0.93% 8.02%

Source: Damodaran, Moody’s. USA assumed as default risk-free country.

Moody’s rating reflects Argentina’s lack of capital, since its disappearing from global

capital markets in 2001. Economy is weak, depending on agricultural commodities whose

prices dropped, reaching 2001 levels. Insufficient government investments add more risk. In

addition to that, country data are not reliable (famous manipulation of inflation data).

Relative Standard Deviation-based assessment

Argentina’s capital market is unstable and volatile. Unpredictable governmental decisions

made markets a risky place, where nothing is certain. High inflation like 30% avg 2015

corrodes savings and gains, requisition of capitals is still possible. This inflations is seen

among highest in the world (Don’t lie to me Argentina, Reuters 2015).

Annual Standard

Deviation (5 Years)

Relative Standard

Deviation

Equity Risk Premium

Argentina 43.63% 4.59 28.67%

Brazil 28.48% 2.99 18.72%

Chile 20.92% 2.20 13.75%

Mexico 18.25% 1.92 11.99%

Source: MSCI Investable Market Indexes (IMI), our analysis. RSD is relative to USA volatility.

The weakness of country’s balance, the uncertainty over the future and the unpredictable

business environment make internal markets highly volatile, more than 4x USA volatility.

Too high uncertainty makes difficult to price relative CDS, because of the excessive lack of

certainty surrounding this country’s future. Final Moody’s rating is a Caa1, “junk” rating.

Setting up a banking business requires some degrees of certainty about government policies

and trust in financial markets. Both of them are very unpredictable and unreliable in

Argentina. However things could change with new president, but will require a lot of effort.

4. China Global Analysis inc®, 2016. For professional and institutional investors only

CHINA GLOBAL ANALYSIS INC

RISK OVERVIEW

Argentina relies on agricultural commodities, therefore the drop in their prices occured in

2014-2015 was a huge shock. Commercial partnerships with Brazil and China (30% export,

38% import) expose Argentina to their recent economic slowdown.

Difficulty to trust governments. No serious reforms have been taken since 2001, budgetary

policy are not rigorous and public spending in energy and transport is really low. Risk of

expropriation is high and there is no transparency in data (inflation manipulation).

Since its default in 2001 Argentina is absent from global capital markets. This factor

increased the isolation and made even harder a possible recovery. However new president

Macri took agreements in order to reinsert Argentina into international capital markets

(Wells Fargo).

The result is a very uncertain business environment, in which establishing new banking

businessess could be very hard. Law enforcement is generally good, but more rigorous

actions have to be taken by the government. Overall outlook can change to positive if

president Macri really takes a path of rigorous and serious reforms, so difficult but so

needed, finally fading away every doubt about next government’s steps.

CHINA GLOBAL ANALYSIS INC.

THE COUNTRY RISK ASSESSMENT TEAM

Enrico Astegiano Filippo Cattabiani

Analyst Analyst

16 March 2016