Empfohlen

Weitere ähnliche Inhalte

Mehr von Elisa Camahort Page

Mehr von Elisa Camahort Page (20)

Blog her mobilegen_infographic

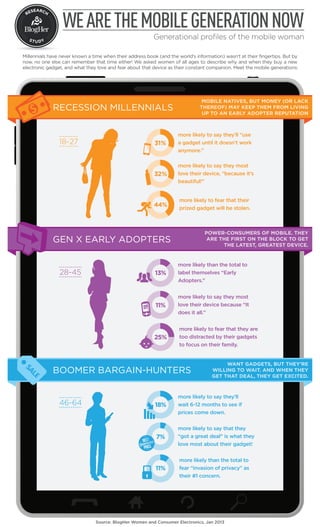

- 1. WE ARE THE MOBILE GENERATION NOW Generational profiles of the mobile woman Millennials have never known a time when their address book (and the world’s information) wasn’t at their fingertips. But by now, no one else can remember that time either! We asked women of all ages to describe why and when they buy a new electronic gadget, and what they love and fear about that device as their constant companion. Meet the mobile generations: MOBILE NATIVES, BUT MONEY (OR LACK RECESSION MILLENNIALS THEREOF) MAY KEEP THEM FROM LIVING UP TO AN EARLY ADOPTER REPUTATION more likely to say they’ll “use 31% a gadget until it doesn’t work anymore.” more likely to say they most 32% love their device, “because it’s beautiful!” more likely to fear that their 44% prized gadget will be stolen. POWER-CONSUMERS OF MOBILE. THEY GEN X EARLY ADOPTERS ARE THE FIRST ON THE BLOCK TO GET THE LATEST, GREATEST DEVICE. more likely than the total to 13% label themselves “Early Adopters.” more likely to say they most 11% love their device because “It does it all.” more likely to fear that they are 25% too distracted by their gadgets to focus on their family. WANT GADGETS, BUT THEY’RE BOOMER BARGAIN-HUNTERS WILLING TO WAIT. AND WHEN THEY GET THAT DEAL, THEY GET EXCITED. more likely to say they’ll 18% wait 6-12 months to see if prices come down. more likely to say that they 7% “got a great deal” is what they love most about their gadget! more likely than the total to 11% fear “invasion of privacy” as their #1 concern. Source: BlogHer Women and Consumer Electronics, Jan 2013