Egypt

- 2. Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing

operations across national borders. For 60 years it has been a source of information on business developments,

economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the

latest analysis is updated daily; through printed subscription products ranging from newsletters to annual

reference works; through research reports; and by organising seminars and presentations. The firm is a

member of The Economist Group.

London New York

Economist Intelligence Unit Economist Intelligence Unit

26 Red Lion Square The Economist Group

London 750 Third Avenue

WC1R 4HQ 5th Floor

United Kingdom New York, NY 10017, US

Tel: (44.20) 7576 8000 Tel: (1.212) 554 0600

Fax: (44.20) 7576 8500 Fax: (1.212) 586 0248

E-mail: london@eiu.com E-mail: newyork@eiu.com

Hong Kong Geneva

Economist Intelligence Unit Economist Intelligence Unit

60/F, Central Plaza Boulevard des Tranchées 16

18 Harbour Road 1206 Geneva

Wanchai Switzerland

Hong Kong

Tel: (852) 2585 3888 Tel: (41) 22 566 2470

Fax: (852) 2802 7638 Fax: (41) 22 346 93 47

E-mail: hongkong@eiu.com E-mail: geneva@eiu.com

This report can be accessed electronically as soon as it is published by visiting store.eiu.com or by contacting a

local sales representative.

The whole report may be viewed in PDF format, or can be navigated section-by-section by using the HTML links.

In addition, the full archive of previous reports can be accessed in HTML or PDF format, and our search engine

can be used to find content of interest quickly. Our automatic alerting service will send a notification via e-mail

when new reports become available.

Copyright

© 2010 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor

any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,

electronic, mechanical, by photocopy, recording or otherwise, without the prior permission

of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the

Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-526X

Symbols for tables

"0 or 0.0" means nil or negligible; "n/a" means not available; "–" means not applicable

Printed and distributed by IntypeLibra, Units 3/4, Elm Grove Industrial Estate, Wimbledon, SW19 4HE

- 3. Egypt 1

Egypt

Executive summary

3 Highlights

Outlook for 2011-15

4 Political outlook

6 Economic policy outlook

7 Economic forecast

Monthly review: December 2010

11 The political scene

12 Economic policy

15 Economic performance

Data and charts

18 Annual data and forecast

19 Quarterly data

20 Monthly data

22 Annual trends charts

23 Monthly trends charts

24 Comparative economic indicators

Country snapshot

25 Basic data

26 Political structure

Editors: Justin Alexander (editor); David Butter (consulting editor)

Editorial closing date: November 17th 2010

All queries: Tel: (44.20) 7576 8000 E-mail: london@eiu.com

Next report: To request the latest schedule, e-mail schedule@eiu.com

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 4. 2

Main railway

MEDITERRANEAN SEA Main road

Baltim

Sidi Barrani Dumyat International boundary

Rashid

Matruh Alexandria Al Mahalla Port Said Main airport

Al Kubra Al Manzala Al Arish

Arish

Damanhur Al Mansura ISRAEL Capital

Tanta Zagazig

Shibin al-Kom Ismailia Major town

Country Report December 2010

n Benha Other town

sio

r es Suez

D ep Giza CAIRO

0 km 100 200 300

ra

a

Sinai

tt

0 miles 50 100 150

Qa

Fayoum

Siwa Beni Suef

Gu

lf

of

S

Gr

ue

Bani Mazar

z

ea

Bawiti

Gulf of A qaba

Ras Gharib

t S

Al Minya

a

Mallawi Sharm el-Sheikh

nd

Dairut

Abnub

SAUDI ARABIA

Sea

Hurghada

Asyut Ni

le

R .

Bur Safaga

LIBYA EGYPT Akhmim

Sohag

www.eiu.com

Girga Qena Quseir

Qus

Luxor RED SEA

Al Kharga

Isna

Marsa Alam

Idfu

Aswan

S a h a r a D e s e r t Lake

Nasser

Halaib

Abu Simbul Triangle

© The Economist Intelligence Unit Limited 2006

2010 SUDAN

© The Economist Intelligence Unit Limited 2010

Egypt

- 5. Egypt 3

Executive summary

Highlights

December 2010

Outlook for 2011-15 • The ruling National Democratic Party (NDP) will maintain tight control over

domestic politics and will dominate the parliamentary election on

November 28th, preventing the Muslim Brotherhood from gaining ground.

• Attention will be focused on the 2011 presidential election and on who will

stand for the NDP—Hosni Mubarak, his son Gamal or another regime insider.

Mohamed ElBaradei is a possible opposition candidate, if allowed to run.

• In the wake of the economic slowdown, the government will move ahead

carefully with economic reform, aimed at raising living standards and creating

jobs, to try to mitigate rising social unrest.

• The expansionary fiscal policy in the 2009/10 (July-June) fiscal year widened

the budget deficit to around 8% of GDP, although it will narrow to 6.8% of

GDP in 2011/12 as tax and other revenue grows, and to 5.5% by 2014/15.

• Real GDP growth reached a respectable 5.2% in 2009/10, but will only

strengthen slightly over the forecast period until 2015, averaging 5.4%, well

below the peak of 2007/08.

• A slight narrowing of the trade deficit, combined with stronger tourism

receipts will help return the current account to a narrow surplus from 2011.

Monthly review • The approach of the parliamentary elections has led to splits within the

NDP—despite its decision to run multiple candidates in safe seats—and

division remains within the Muslim Brotherhood over whether to participate.

• There have been demonstrations, and some violent clashes, on university

campuses following a court ruling that the police units that have been

deployed since 1981 on campuses, and can be oppressive, should be removed.

• The government has drawn up a new contract ceding land to a developer

TMG, to replace the old one ruled invalid by a court. However fresh legal

challenges are pending to this new contract and other land sales.

• A new minimum wage of E£400 (US$70) per month has been proposed by

the National Council for Wages, although unions argue this is still too low.

• The Ministry of Housing has planned the relaunch of a PPP tender for a

major wastewater facility west of Cairo, and other PPP tenders are pending.

• The government has set aside 50m sq metres of land for industrial projects, in

the Suez Canal zone, Cairo suburbs, Alexandria and North Fayoum.

• Egypt's foreign-exchange reserves have returned to their peak level of

US$36bn.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 6. 4 Egypt

Outlook for 2011-15

Political outlook

Political stability Egypt has been under authoritarian military rule, with a democratic veneer,

since a coup in 1952. This has provided a degree of stability, even through

defeats in wars with Israel, and kept out of power the Muslim Brotherhood—a

banned but popular and partly tolerated Islamist group. However, the president,

Hosni Mubarak, who has ruled since 1981, is now 82 and underwent major

surgery in early 2010. There is considerable doubt about whether he would be

fit to see through another six-year term. The biggest question in Egyptian

politics at present is whether he will contest the presidential election in

September 2011, or stand aside in favour of his son, Gamal, or another regime

candidate (probably a military man such as Omar Suleiman, the intelligence

chief, or Ahmed Shafiq, a former Egyptian Air Force commander who is now

aviation minister). The ruling National Democratic Party (NDP) will use the

coming months to assess the acceptability of the various possible candidates to

the public and the military. Even if Mr Mubarak chooses to run for a sixth term

(which he would inevitably win, given the NDP's control over the election

apparatus), he would be unlikely to complete it. Nonetheless, in recent months

many of the NDP's old guard have voiced support for a sixth term, although a

final decision has probably not been made yet.

There is a growing sense of disaffection among the population about

inadequate salaries and poor living standards, leading to increasingly bold

demonstrations and industrial action by labour activists, which could develop a

more overtly political tone. The benefits of economic growth in recent years

have not been evenly spread, and despite the emergence of a growing middle

class, the bulk of Egypt's 84m population remain extremely poor—and as the

population is growing by around 1.6m a year, large numbers of new jobs must

be created just to keep unemployment at its current high levels. The

government is pursuing a long-term economic reform programme aimed at

raising living standards, education levels and access to jobs to stem social and

political tension. However, the inequality gap is so wide that these efforts will

be insufficient to eradicate discontent in the near term. There is also ongoing

frustration about corruption and police brutality. A cabinet reshuffle is likely

following the imminent parliamentary election, and there may even be a new

prime minister to replace Ahmed Nazif, in office since 2004. Other threats to

stability come from sporadic clashes between some Muslims and Coptic

Christians (about 10% of the population) and the long-term marginalisation of

the Bedouin population in the Sinai region, which may result in some

providing support to al-Qaida. However, the regime is unlikely to be seriously

destabilised and will continue to contain opposition and criticism from the

independent judiciary, the press and especially the Muslim Brotherhood.

The legal opposition parties are weak and divided and lack credibility. The

Brotherhood is more popular, but is divided between a conservative branch,

which wants the movement to revert to a more moralistic societal role (and

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 7. Egypt 5

which appears to be in the ascendant), and a younger, reformist arm that

remains keen to participate in the formal political process, despite the

government's ongoing crackdown on its activities and the prohibition on

political parties based on religion. Brotherhood candidates, running as

independents, won 88 seats in the People's Assembly (the lower chamber)

election in 2005, compared with just 14 seats for the legal opposition parties.

Election watch The NDP, which holds the vast majority of parliamentary seats, will seek to

reduce the Brotherhood's representation in the People's Assembly (in which the

number of seats will be increased from 454 to 518, with all the new seats

reserved for women) in the election on November 28th. The fact that eight of

the 88 seats available in the June 1st election for the Shura Council (the upper

house) went to opposition parties and independents, but none to Brotherhood-

backed independent candidates, may be seen as an indication of the regime's

intentions. Mohamed ElBaradei, the former director-general of the International

Atomic Energy Agency who returned to Egypt this year and has rallied the

opposition, has called a boycott of the elections, but there has been little

enthusiasm for this, and the main legal opposition parties—Wafd, Tagammu and

the Nasserists—will contest it, as well as about 150 independent candidates

linked to the Brotherhood.

The NDP's continued domination of parliament will in turn enable it to

determine the terms for the presidential election. Any presidential candidate

must currently either come from the leadership of a recognised party or obtain

250 signatures from members of parliament or local councillors, which would

be virtually impossible for any independent candidate, given the NDP's

domination of all the governing bodies. Mr ElBaradei is a possible candidate,

although he could not stand under current rules and is focusing his efforts on

easing the candidacy restrictions and on other reforms. If Mr Mubarak is

serious about engineering his son's succession, then he might eventually agree

to grant some of Mr ElBaradei's demands in the hope of giving the succession

some aura of democratic legitimacy.

International relations Ties between Egypt and the US will remain strong, as the US seeks Egyptian

support for its Middle East policies and Egypt relies on US military assistance.

However, tensions between the two will still flare up occasionally over

concerns about human rights violations, anti-democratic behaviour and the

situation of Egypt's Christian minority. Israel will continue to be a close ally, and

Mr Mubarak will work with Israel to continue the isolation of the Gaza Strip,

both because Egypt does not want to be forced to assume responsibility for the

crowded Palestinian territory, and because Gaza is controlled by Hamas, an

Islamist group related to the Muslim Brotherhood. Egypt remains concerned

about the regional role of Hamas's primary backer, Iran, and its apparent

nuclear ambitions. Gradual moves towards Egyptian-Syrian rapprochement

may have a bearing on relations with Hamas and Iran, both Syrian allies. Egypt

will play a role in US-mediated Israeli-Palestinian peace talks, if they continue,

but little is expected to come of them. There may be more chance for progress

towards peace later in the forecast period, although past experience invites

scepticism.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 8. 6 Egypt

Egypt's most significant diplomatic challenge will be maintaining its interests in

the Nile river waters. Most of the upstream countries have signed an agreement

to establish a new regime for co-operation along the river—in place of a colonial

era Anglo-Egyptian agreement—which come into effect in mid-2011 and would

facilitate their use of hydroelectric power and irrigation. Egypt and Sudan

strongly oppose any measures that would reduce the volume of flow into their

borders. The situation will be further complicated in January 2011 when

Southern Sudan—through which the White Nile flows—is expected to vote for

independence in a referendum promised in the 2005 agreement that ended the

Sudanese civil war. However, it is not expected that any of the upstream

initiatives currently under way will seriously reduce the Nile flow in the near

term. But if future projects were to, then Egypt might threaten, and even

seriously consider, a military response.

Economic policy outlook

Policy trends The government's overriding concern in the forecast period will be to maintain

economic activity and job creation as Egypt emerges from the aftermath of the

global recession. The government will continue with some economic reforms

and liberalisation, although concerns over political unrest are likely to slow

progress in some key areas, such as reform of public administration and

implementation of a new property tax. The government will continue its

programme of incrementally reducing subsidies on energy products in a bid to

align domestic and international prices and minimise the fiscal drain, although

some of this will be delayed until after the 2011 election. It aims to have

eliminated all energy subsidies by 2013.

The government's consolidation programme in the banking sector means that

Egypt's banks are relatively stable, and domestic liquidity will remain at

comfortable levels. The government will continue to tighten regulation and to

work on improving access to finance for the private sector. The privatisation of

Banque du Caire was put on hold in 2008, and it is unclear whether this has

been shelved entirely following the announcement in May 2010 of a halt in the

overall privatisation programme in favour of an approach based on private-

sector management of state-owned assets. The government is aware of the risk

of social dislocation if liberalisation moves too quickly, and reform will remain

gradual. The public-private partnership (PPP) law passed in June 2010 should

facilitate the implementation of PPPs and thereby speed up the ongoing

government programme to improve Egypt's infrastructure in areas such as

hospitals, roads, railways, ports and wastewater treatment.

Fiscal policy The government has been operating for many years with a large fiscal deficit,

averaging around 8% a year over the past decade. It aims to reduce this

substantially over the forecast period, to 3.5% of GDP by 2015; the Economist

Intelligence Unit expects that it will make some progress after the current

2010/11 fiscal year (July-June), but will still fall well short of this target, with a

deficit still around 5.5% of GDP in 2014/15. The presidential election in 2011,

together with fiscal stimulus in the aftermath of the global recession, will boost

spending growth in the current year, although gradual cuts will be made in

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 9. Egypt 7

some subsidies (for example in the price of subsidised butane canisters).

Meanwhile, having dipped in 2009/10, revenue growth should pick up to an

average of 15% in 2010/11-2014/15 as global trade, and thus earnings from the

Suez Canal and customs duties, recovers. This will be augmented by measures

to increase tax compliance and by the abolition of some tax exemptions. A

property tax introduced in 2010 will further boost receipts, although it will only

be gradually implemented.

Stronger than expected economic growth and tax revenue since the start of the

calendar year resulted in a deficit in 2009/10 of around 8% of GDP. Provided

that the economy recovers as forecast, the deficit should remain fairly stable in

2010/11, and then begin declining as revenue growth outstrips expenditure

growth, and as subsidies are reduced. Given the government's caution over

contracting foreign debt, we expect the deficit to be financed largely by local

borrowing, although some new Eurobonds will also be issued. The public debt

stock, domestic and external, totalled around 81% of GDP at end-2009, and

interest payments account for an increasing proportion of spending, but it is

expected to decline in relative terms to 69% of GDP at end-2015.

Monetary policy The Central Bank of Egypt (CBE) has begun to move towards making inflation-

targeting its main policy goal. It will be some time, however, before the CBE's

monetary instruments are fully in place. The CBE began loosening monetary

policy at the beginning of 2009 on the back of a gradual deceleration in the rate

of inflation, which bottomed out at 9% in August 2009, from a peak of 23.7% in

August 2008. The CBE last cut its rates in September 2009, when the overnight

deposit and lending rates were reduced by 25 basis points each, to 8.25% and

9.75% respectively. The discount rate was left unchanged at 8.5%.

However, given a subsequent pick up in inflation, the CBE has ended its

loosening cycle. In light of the potential inflationary impact of the government

resuming its programme of reducing energy subsidies, we expect the CBE to

starting raising interest rates early in the forecast period, particularly as

monetary policy begins to tighten elsewhere in the world in 2012 and Egypt

seeks to maintain a positive interest-rate differential with other countries to

discourage capital outflows.

Economic forecast

International assumptions 2010 2011 2012 2013 2014 2015

Economic growth (%)

US GDP 2.5 1.5 1.9 2.3 2.4 2.4

EU27 GDP growth 1.7 1.1 1.5 1.7 2.0 1.9

World GDP 3.5 2.5 2.9 3.0 3.1 3.1

World trade 12.2 5.9 6.3 6.6 6.7 6.1

Inflation indicators (%)

US CPI 1.5 1.1 1.9 2.5 2.8 2.8

EU27 CPI 1.8 1.7 1.7 1.9 2.0 2.1

Manufactures (measured in US$) 2.3 -1.6 -0.5 1.2 1.7 2.0

Oil (Brent; US$/b) 80.0 82.0 81.3 78.3 75.5 71.0

Non-oil commodities (measured

in US$) 21.9 9.0 -4.1 -4.0 2.1 0.3

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 10. 8 Egypt

2010 2011 2012 2013 2014 2015

Financial variables

US$ 3-month commercial paper

rate (av; %) 0.2 0.3 0.7 2.2 4.1 5.1

Exchange rate E£:US$ (av) 5.6 5.8 5.7 5.7 5.6 5.6

Economic growth Despite a slight hiccup in the second quarter of 2010, growth has been

accelerating since the start of 2009, following the sharp drop at the end of 2008.

The preliminary official estimate put real GDP growth in 2009/10 at 5.2%, up

slightly on the previous year. Although well down on rates recorded during the

recent boom, it was still a positive outcome against the background of a global

economic recession in which world GDP contracted by 0.8% in 2009 (at

purchasing power parity rates). However, it was probably not strong enough to

lift employment growth to the levels needed to create sufficient jobs for the

large number of new entrants coming onto the labour market. Egypt's exports

were hit by the recession, and although they are growing once again are not

forecast to exceed the 2007/08 level until 2011/12. External demand will

continue to be weak as the recovery in the EU and the US, Egypt's largest export

markets, remains fragile. On the plus side, domestic demand remains strong,

buoyed by the government's fiscal stimulus programme and by robust activity

in sectors such as construction and telecommunications. However, some effects

of the global slowdown will continue to be felt, especially through the labour

market, and this means that private consumption will pick up only gradually.

We forecast that the global economy will expand only weakly, and growth will

soften in 2011, as the positive effect of inventory restocking and stimulus

measures in the major economies wanes and the governments of many

developed economies instead cut expenditure significantly to control their

spiralling deficits, which in turn will dampen corporate and household

sentiment. Egypt will be affected through an only slow recovery in exports

and shipments through the Suez Canal, although tourism seems to be more

resilient than expected.

The government's spending on infrastructure will continue to offset some of the

negative effects of the slowdown on the manufacturing sector and employ-

ment, and will help to sustain investment and household demand. Private

investment remains strong in construction, and from 2011 the PPP programme

should help to boost demand in the sector. Additional investment will flow

from new oil and gas projects, particularly the deepwater Mediterranean fields

being developed by UK-based BP. The main risk to our forecast stems from

external factors: if Egypt's export markets pick up even more weakly than

forecast, or even slip back into recession, growth in Egypt may not be sufficient

to lift living standards significantly. However, assuming that investment, both

domestic and foreign, holds up, we forecast that real GDP will continue to grow

at an average of around 5.4% in 2010/11-2014/15.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 11. Egypt 9

Economic growth

% 2010 a 2011 b 2012 b 2013 b 2014 b 2015 b

GDP c 5.2 5.3 5.5 5.6 5.3 5.4

Private consumptiond 5.0 4.4 4.8 5.7 6.4 7.6

Government consumption 8.9 8.1 5.7 3.1 3.6 3.5

Gross fixed investment 6.1 9.2 13.3 14.1 13.8 13.5

Exports of goods & services 5.7 8.9 10.6 13.8 12.5 11.6

Imports of goods & services 6.1 10.3 13.3 17.3 17.9 18.0

Domestic demand 5.3 5.9 6.6 7.1 7.7 8.6

Agriculture 3.4 3.8 3.6 3.5 3.2 3.4

Industry 5.5 5.9 6.8 6.9 6.4 5.8

Services 5.4 5.1 4.4 4.4 4.4 5.6

a Economist Intelligence Unit estimates. b Economist Intelligence Unit forecasts.

Inflation Having peaked at an average of 18.3% in 2008, the year-on-year rate of inflation

has fallen steadily and will have averaged an estimated 11.1% in 2010. Oil prices

will remain high, averaging US$77/barrel in 2011-15, and non-oil commodity

prices will remain relatively flat on average over the forecast period (although

there will be sporadic spikes, as with wheat prices at the moment owing to a

drought in Russia). This relatively mild external environment will mean that

inflation should ease gradually and average 8.3% during 2011-15, although there

are risks to this scenario such as an upward revaluation of the Chinese

renminbi, which would increase import costs, and a sizeable increase in the

minimum wage in response to demands from the growing labour movement.

Exchange rates The exchange rate is driven in large part by capital flows and developments

with the US dollar. Egypt's robust economy and high interest rates compared

with much of the rest of the world have attracted substantial carry-trade

inflows in recent years. The trend has now reversed and the Egyptian pound

slipped to a five-year low against the dollar in late October 2010, possibly with

some help from the Central Bank. However, the CBE is unlikely to countenance

much more depreciation, owing to the impact on imported inflation, and the

resumption of quantitative easing in the US should anyway give the pound

support in late 2010 and early 2011. It is also likely to get a boost after the

presidential election in late 2011, as the political uncertainty may be weighing

negatively on the pound. The long-term average in 2011-15 is forecast to be

E£5.68:US$1, compared with an estimated E£5.63:US$1 in 2010. As a result of

weakness in the euro zone, the pound will strengthen steadily against the euro,

to an average of E£6.77:€1 in 2011-15 (from an estimated 2010 average of

E£7.47:€1 and around E£8:€1 in late October 2010), which could hurt exports to

Europe and the tourism sector. Capital inflows will be more moderate than in

recent years, but rising hydrocarbons and Suez Canal receipts will lift foreign-

exchange reserves, and the CBE will intervene to prevent sharp swings in the

exchange rate.

External sector Export earnings will continue to rise over the forecast period as external

demand strengthens gradually, and so the trade deficit will narrow steadily. The

non-merchandise surplus will also widen further, as the Egyptian tourism

sector and traffic through the Suez Canal pick up after the slump in 2009,

helping to boost the services balance. The transfers account will maintain a

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 12. 10 Egypt

solid surplus and the income balance will turn positive by around 2013.

Overall, the current account will return to a narrow surplus in 2011, after three

years in deficit. During the rest of the forecast period, the trade deficit will

remain relatively steady in absolute terms, although it will fall as a proportion

of GDP, but the non-merchandise surplus will steadily widen, pushing up the

current-account surplus to an average of 1.6% of GDP in 2011-15.

Forecast summary

(% unless otherwise indicated)

2010 a 2011 b 2012 b 2013 b 2014 b 2015 b

Real GDP growth 5.2 5.3 5.5 5.6 5.3 5.4

Industrial production growth 5.6 6.0 6.8 7.1 6.4 5.8

Gross agricultural production growth 3.4 3.8 3.6 3.5 3.2 3.4

Consumer price inflation (av) 11.1 10.0 9.3 8.1 7.0 7.1

Lending ratec 11.8 12.0 12.3 12.5 11.8 11.8

Government balance (% of GDP) -8.0 -7.6 -6.8 -6.7 -5.9 -5.5

Exports of goods fob (US$ bn) 26.0 27.8 30.4 34.3 39.0 41.9

Imports of goods fob (US$ bn) 47.7 47.9 48.3 52.0 56.6 61.2

Current-account balance (US$ bn) -0.7 1.1 5.2 6.8 8.6 9.4

Current-account balance (% of GDP)d -0.3 0.4 1.7 1.9 2.2 2.1

External debt (end-period; US$ bn) 31.2 31.2 29.2 28.5 27.9 27.5

Exchange rate E£:US$ (av) 5.63 5.75 5.72 5.67 5.64 5.62

Exchange rate E£:US$ (end-period) 5.69 5.74 5.70 5.66 5.63 5.61

Exchange rate E£:¥100 (av) 6.44 6.98 6.94 7.00 6.87 6.73

Exchange rate E£:€ (av) 7.47 7.19 6.86 6.69 6.55 6.58

a Economist Intelligence Unit estimates. b Economist Intelligence Unit forecasts. c Annual average.

d Ratio based on calendar year GDP; national accounts use fiscal year.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 13. Egypt 11

Monthly review: December 2010

The political scene

Election campaigning reveals Campaigning for the election for the People's Assembly (the lower house) on

rifts within parties November 28th has exposed the rifts and weaknesses within the ruling

National Democratic Party (NDP). The NDP's long hold on power has fostered a

climate of corruption and cronyism in which loyalties are to individuals rather

than to the party as a whole. The result of this in the 2005 elections was a wave

of resignations by NDP members who were not picked as candidates. Many of

them ran as independents instead and the NDP was then forced to invite those

that won seats to re-join the party to preserve its large majority. To avoid a

repeat of this embarrassing scenario, the NDP is fielding multiple candidates in

a significant number of constituencies, mainly those that it considers safe seats.

The party hopes this will mitigate violence in areas such as Upper Egypt and

Sinai that are seeing tribal tensions between prominent families within the

NDP competing for seats, although the multiple candidacies will mean that the

elections in these constituencies are even more individualised and less about

national party politics. The move has also failed to stem resignations, as not all

those who wanted to run could be accommodated even with the multiple

candidacies, and some NDP members have resigned after not being selected.

There are also signs of disappointment from the Coptic Church leadership,

because the NDP list does not include many Coptic candidates.

The Muslim Brotherhood is also suffering from dissent within its ranks. A bloc

called the Opposition Front has emerged from within the organisation, led by

Mokhtar Nouh, a former member of parliament and head of the Bar

Association who was expelled from the Brotherhood several years ago.

Mr Nouh told the local Al Masry Al Youm newspaper that his bloc could

transform into a parallel, though not separate, movement. Its stated aim is to

offer a platform for those who support the ideology of the Muslim

Brotherhood's founder, Hassan al-Banna, but not necessarily all the actions and

decisions of the current leadership. Most significantly, the Front has issued a

statement opposing the decision of the Brotherhood leadership to participate in

the election. The twenty signatories to this statement included Ibrahim

al-Zaafarani, a member of the Brotherhood's Shura Council, Kamal

al-Halabawy, a former Brotherhood representative in Europe, and Abdel-Hai

al-Faramawy, a professor at Al Azhar University in Cairo. The Front has also

highlighted a lack of consensus over the use of the Muslim Brotherhood's main

election slogan, "Islam is the Solution", which is officially banned according to

electoral laws that limit religious-based campaigning, but is still used by

Brotherhood candidates. Such internal disputes have weakened the

Brotherhood, perhaps influencing its decision to field fewer candidates than in

2005. Brotherhood members have also faced a greater than expected number of

arrests, to which it has reacted by threatening the use of "all means" to protect

its members "without any red lines". Members continue to protest against these

arrests, including a demonstration on November 13th in Alexandria, a city in

which the Brotherhood was particularly successful in 2005.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 14. 12 Egypt

With several opposition groups boycotting the elections and al-Ghad party

members facing harassment and arrest, the Wafd Party may become the major

opposition bloc in the new parliament. It is fielding almost twice as many

candidates as the Brotherhood, despite also suffering from internal dissent and

resignations by prominent members such as Kamal Zakher and Ahmed Fouad

Negm, and a mass resignation of 30 members in Minya, Upper Egypt. Overall,

with an NDP victory a forgone conclusion, it is the intra-party dissent within

the major political blocs that is more significant in the short-term for Egyptian

politics than the precise distribution of seats in the new parliament.

University campuses witness There have been demonstrations on university campuses, inspired by a

unrest campaign by the March 9th Movement, established by a group of professors at

Cairo University to promote academic freedom and the autonomy of

universities. The movement is particularly publicising a Supreme

Administrative Court verdict in October, which upheld a previous ruling that

annulled Ministerial Decree 1812 of 1981 that established "university guards",

including deploying police at Cairo University. Over the years, these police units

have clamped down, often aggressively, on student political activities, and

professors also complain of interference in academic life. University campuses

remain a site for frequent demonstrations and often witness disturbances

before elections.

The recent student demonstrations have been calling for the police units to be

removed from university campuses throughout Egypt. The most violent clash

so far was at another Cairo university, Ain Shams. When members of the

March 9th Movement arrived at Ain Shams, on November 4th, to inform

students about the ruling, they were attacked by armed thugs, and the

university guards present did not intervene to stop the clash. The incident has

led to questions over who carried out these attacks on the professors and

students supporting them. Hany Helal, the higher education minister, has

disputed the March 9th account and accused the group of stirring up trouble at

Ain Shams, but photographs and video footage of the incident appear to show

men armed with crude weapons threatening the students and professors.

Mr Helal has said that the court ruling applies only to Cairo University, but he

suggested that a scheme could be developed to provide private security for

each university in place of the police presence. Protests are continuing at the

gates of Cairo University insisting that the court ruling is implemented.

Economic policy

Real estate lawsuits worry The consequences of a recent verdict by Cairo's Supreme Administrative Court

developers cancelling the sale of state land to the Talaat Moustafa Group (TMG) for its

Madinaty development (October 2010, Economic policy) have continued to

unfold. The court decision forced the government to replace the original 2005

contract with a new one, signed on November 9th. The new contract provides

the same terms to TMG, one of Egypt's largest real estate developers, including

charging it a payment-in-kind (that is, as finished apartments) of 7% of the

development's land price value, which would be at least E£15bn (US$2.6bn) at

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 15. Egypt 13

current prices. The new contract ends the legal limbo created by the court

ruling, reassuring investors in TMG.

This may only be a temporary reprieve for the company and others in the

sector. The plaintiff in the original case against TMG, Hamdy Fakharany, has

vowed to challenge the new contract and those of other companies that have

purchased state land over the last decade. Mr Fakharany's next court date is

November 23rd, when another administrative court—which rules on the legality

of government decisions—will be asked to declare the new contract illegal. On

the same day, the court is to hear a case filed against Palm Hills Developments,

another major developer whose shareholders include a holding company

linked to the families of the current housing minister, Ahmed al-Maghrabi, and

a former transport minister, Mohammed Mansour. Other suits have been filed

against Egypt Kuwait Holding and Egyptian Resorts Company.

The government is now preparing to introduce a new land-sale law to resolve

contradictions in current legislation. One existing law stipulates that state land

must be sold through auctions, while another gives the government the right to

sell it directly to developers—with the administrative court favouring the first

interpretation. The content of the new law remains unknown, but it is likely

that it would close the loophole that allows past land sales to be cancelled and

allow the government to sell land directly to companies in certain cases, even if

the government has pledged greater transparency and competitive bidding for

future sales. The new law is unlikely to be passed until next year, given the

forthcoming People's Assembly election. The government may have to

intervene again before then to prevent courts cancelling existing deals.

A new minimum wage is On November 11th, the National Council for Wages, a body tasked with setting

proposed and contested the national minimum wage, recommended a new rate of E£400 (US$70) per

month, equivalent to almost exactly one-third of Egypt's estimated GDP per

head this year. This increases the minimum wage in the private sector

substantially and resolves a court's order that the Council, which had not met

in over two decades, update this base to reflect the increased cost of living over

this period. Previously the minimum wage had been E£112, or even as low as

E£36 in some cases.

Trade unions, regrouped under the government-controlled Egyptian Federation

of Trade Unions (EFTU), have asked for a higher figure of at least E£500. The

EFTU has also proposed three separate minimum wage levels, based on the

level of education of the employee: E£500 for the least educated, E£750 for high-

school graduates and E£1,000 for university graduates. Independent labour

non-governmental organisations and unrecognised trade unions (legal trade

unions must be government-approved and exist under the EFTU's umbrella) are

asking for a higher sum of E£1,200, a figure based on a single wage-earner

supporting a family of five at the UN poverty rate (June 2010, Economic

performance).

The new minimum wage is not likely to be put in effect until next year,

however. The president, Hosni Mubarak, must approve the new figure, and has

asked the Ministry of Finance to study various proposals. The new minimum

wage is likely to be part of the electoral campaign of the NDP's presidential

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 16. 14 Egypt

candidate (Mr Mubarak, his son, Gamal, or someone else) for the September

2011 election.

A PPP wastewater project Egypt is relaunching its tender for a wastewater treatment facility at Abu

is relaunched Rawash, west of Cairo, the first major infrastructure project planned under a

public-private partnership (PPP) scheme announced in 2009. The 20-year PPP

scheme for Abu Rawash has been upgraded to include sludge management and

co-generation capabilities in the tender, and includes the operation and

management of a 1.2m-cu metre/day treatment facility and an 800,000-

cu metre/d secondary treatment plant. The tender, which is run by the Ministry

of Housing, has also being adapted to fit with a new PPP law passed in June,

after the project was originally proposed. Bidders that have pre-qualified thus

far include five multinational consortia.

The tender relaunch is expected to happen at the end of November, alongside a

similar wastewater treatment scheme for 6th of October City (a suburb of

Cairo) and a tender for the construction of 34 km of highway at Rod al-Farag,

also near Cairo, estimated at around US$1bn. The new eight-lane highway will

link central Cairo along the north-eastern Nile corniche to 6th of October City,

and will be designed, operated and maintained by the winning consortium for

a 20-25-year period. These projects have been long-planned but were delayed

by a lack of clear executive regulations for the new PPP law.

More wastewater treatment plants are being planned under the PPP scheme to

resolve a growing water problem in rural areas. In October, the housing

ministry said that it would be bundling smaller wastewater treatment plant

schemes together to provide better sanitation to villages in the Delta and Upper

Egypt. Such schemes would probably rely on treatment plants run at the

governorate level. Only two-thirds of the country currently has adequate

wastewater services.

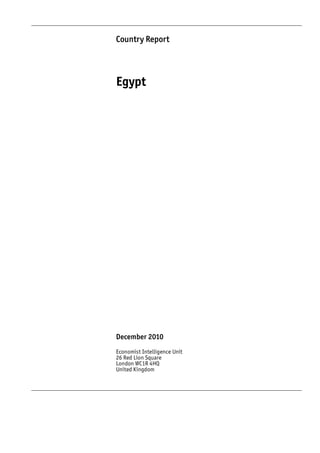

Government allocates land for Egypt's Industrial Development Authority (IDA) announced on November 9th

industrial investment that it would offer 50m sq metres of land for industrial projects starting in

January 2011, with the hope of attracting around E£73bn worth of investments.

The IDA's scheme is designed to relieve difficulties in securing land for

industrial projects under current regulations, thus addressing a recurrent

criticism in the World Bank's Doing Business reports. The land designated under

the scheme will be fast-tracked for sale to industrial developers, improving the

availability of construction permits and reducing transaction costs for investors.

According to Beltone Financial, a local investment bank, the land offering will

be valued at E£72.7bn and include the following areas:

• 15m sq metres in East Port Said, to attract E£22.5bn of investments;

• 1m sq metres in South Raswa in Port Said (E£1.8bn);

• 5m sq metres in Burg al-Arab, near Alexandria (E£8bn);

• 10m sq metres in North Fayoum industrial zone (E£12bn);

• 2m sq metres in Abu Khalifa industrial zone near Ismailia (E£3.4bn);

• 3m sq metres in Badr City near Cairo (E£4.6bn);

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 17. Egypt 15

• 10m sq metres in 10th of Ramadan City near Cairo (E£14bn); and

• 4m sq metres in Sadat City north of Cairo (E£6.4bn).

Egypt has had success in recent years in attracting Chinese and Turkish

investors, among others, in its industrial zone, notably by offering foreign

investors the advantage of its trade agreements with the EU.

Land allocated for industrial investment

Baltim MEDITERRANEAN SEA

Rashid Dumyat

Port Said

Alexandria

South Raswa East Port Said

Burg al-Arab 1m sq metres

5m sq metres 15m sq metres

(E£1.8 bn) (E£22.5 bn)

(E£8.0 bn) Tanta

Abu Khalifa industrial zone

2m sq metres Ismailia

EGYPT (E£3.4 bn)

Benha 10th of Ramadan City Sinai

Sadat City

10m sq metres

4m sq metres

(E£14.0 bn)

(E£6.4 bn)

Badr City

CAIRO Suez

3m sq metres

(E£4.6 bn)

le

R. Ni

North Fayoum

10m sq metres

Gu l

Fayoum

(E£12.0 bn)

fo

fS

ue

Beni Suef

z

0 km 50 100

0 miles 25 50

Economic performance

More IPOs are announced Amer Group Holding, a real estate firm, has announced plans to sell 30.7% of

the company through an initial public offering (IPO) on the Egyptian Exchange

in November. The final price of the shares will be announced on

November 22nd, with 80% of them to be sold through private placement and

the remaining 20% publicly, for an estimated total of as much as E£1.8bn

(US$315m). The sale is being managed by Beltone Financial. Amer Group owns

the Porto brand, which has resorts on Egypt's Mediterranean and Red Sea

coasts. It has plans to expand regionally, including a US$1bn resort in Syria.

Amer Group represents the first new IPO in Egypt since that of Juhayna, a dairy

and juice company, in June 2010, and only the second since mid-2008. Along

with planned future IPOs, it marks a revival of the Egyptian market as the

country recovers from the global economic recession. Other planned IPOs

include the sale of a US$200m-250m stake in Albatros Resorts, another real

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 18. 16 Egypt

estate firm, intended to finance a doubling of the number of rooms it operates.

The sale, also managed by Beltone, is expected to take place in 2011. Mo'men, a

fast food company operating in Egypt, Sudan, Libya and Bahrain, also

announced on October 7th that it will seek to raise funding through an IPO of

40% of its shares towards the end of 2012. The IPO is intended to finance

regional expansion and the goal is to raise at least E£400m (US$70m). In late

2009, Citadel Capital, a private equity firm, had said it would offer 12.5% of its

shares in an IPO to raise new capital, but not yet gone ahead with the move.

Reserves hit high as govern- Egypt's foreign-currency reserves reached US$35.5bn in October 2010, marking a

ment considers 100-year bond return to the previous peak in October 2008 at the start of the global financial

crisis. To stimulate the economy during the downturn, the government spent

over US$5.4bn in late 2008 and the first half of 2009, accounting for much of

the reserves' fall to a low of US$31bn April 2009.

The finance minister, Youssef Boutros-Ghali, said in November that the

government was considering issuing 100-year bonds, totalling as much as

US$500m. The project is still at an early stage and, although Mexico recently

issued its own century bonds, Egypt is more likely to focus on shorter

maturities, having raised US$1.5bn earlier this year through ten-year notes with

a 5.75% yield and 30-year notes at 6.95% (May 2010, Economic policy). That was

the first Egyptian bond offering in nine years, with the government keen to take

advantage of lower borrowing costs. In related news, the Central Bank of Egypt

cancelled a E£1bn bond auction at 12.35%, but gave no reason for this.

Orascom Telecom sale blocked Naguib Sawiris, chairman of Orascom Telecom (OT), said that his company's

by Algeria row with the Algerian government over alleged currency violations and unpaid

tax claims by its subsidiary Djezzy was blocking plans to sell much of OT to

Vimpelcom of Russia. On November 9th, Mr Sawiris said that he had sent a

final letter to the Algerian prime minister, Ahmed Ouyahia, requesting an end

to pressure on Djezzy or he would resort to international arbitration. He also

stated that it was unlikely that the Algerian government, which has repeatedly

stated its desire to nationalise Djezzy, would offer a fair price. Press reports

allege that Algeria offered US$2.5bn for Djezzy, much lower than the US$7.8bn

offered by MTN of South Africa.

If the complex OT-Vimpelcom deal were to collapse, it would leave Mr Sawiris

saddled with a high debt burden. Bloomberg News reported on November 10th

that another of Mr Sawiris's companies, an Italian mobile-phone operator,

Wind Telecom, is planning to raise up to €6.9bn (US$9bn) to refinance existing

debt. Wind is part of Mr Sawiris' Weather Investments, as is part of OT. Instead

of including Djezzy, which provided over 50% of OT's income in recent years, in

the sale, Mr Sawiris may be forced to sell his company piecemeal to various

investors. He has, however, stated that he will keep his interest in certain

OT ventures, notably his original Egyptian company, MobiNil, and a new

venture in North Korea. Despite his problems, Mr Sawiris appeared combative,

expressing interest in acquiring a Polish firm, Polkomtel, and a Serbian

company, Srbija.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010

- 19. Egypt 17

Data and charts

Annual data and forecast

Pl ea se se e g ra p hi c b el ow

2006 a 2007 a 2008 a 2009 a 2010 b 2011 c 2012 c

GDPd

Nominal GDP (US$ bn) 107.9 132.2 164.8 187.3 216.7 243.7 283.6

Nominal GDP (E£ bn) 618 745 896 1,039 1,221 1,402 1,622

Real GDP growth (%) 6.8 7.1 7.2 4.7 5.2 5.3 5.5

Expenditure on GDP (% real change)d

Private consumption 6.4 8.8 5.7 4.5 5.0 4.4 4.8

Government consumption 3.1 0.2 2.1 8.4 8.9 8.1 5.7

Gross fixed investment 13.8 23.7 14.8 -10.2 6.1 9.2 13.3

Exports of goods & services 21.2 20.2 28.8 -12.8 5.7 8.9 10.6

Imports of goods & services 21.7 30.5 26.3 -17.7 6.1 10.3 13.3

Origin of GDP (% real change)d

Agriculture 3.3 3.7 3.3 3.2 3.4 3.8 3.6

Industry 9.7 5.9 6.1 5.1 5.5 5.9 6.8

Services 5.4 20.2 8.2 4.2 5.4 5.1 4.4

Population and income

Population (m) 78.6 80.1 81.5 83.0 84.6 86.2 87.8

GDP per head (US$ at PPP) 4,679 5,064 5,445 5,650 5,866 6,169 6,527

Recorded unemployment (av; %) 10.6 8.9 8.7 9.4 9.7 8.9 8.1

Fiscal indicators (% of GDP)d

Central government revenue 24.5 24.2 24.7 27.2 21.5 22.0 22.4

Central government expenditure 33.6 29.8 31.5 33.8 29.5 29.7 29.3

Central government balance -8.2 -7.3 -6.8 -6.6 -8.0 -7.6 -6.8

Central government debt 114.8 101.0 85.0 80.9 b 81.3 78.8 75.6

Prices and financial indicators

Exchange rate E£:US$ (av) 5.73 5.63 5.43 5.55 5.63 5.75 5.72

Exchange rate E£:€ (av) 7.19 7.71 7.99 7.72 7.47 7.19 6.86

Consumer prices (av; %) 7.6 9.5 18.3 11.9 11.1 10.0 9.3

Stock of money M1 (% change) 20.0 25.1 14.9 12.9 14.5 14.9 15.7

Stock of money M2 (% change) 15.0 19.1 10.5 9.5 13.1 14.1 19.1

Lending interest rate (av; %) 12.6 12.5 12.3 12.0 11.8 12.0 12.3

Current account (US$ m)

Trade balance -12,558 -20,494 -26,774 -22,475 -21,718 -20,143 -17,909

Goods: exports fob 20,546 24,455 29,849 23,089 26,025 27,791 30,423

Goods: imports fob -33,104 -44,949 -56,623 -45,564 -47,742 -47,934 -48,332

Services balance 8,689 11,195 14,312 13,242 13,225 13,190 13,789

Income balance 831 1,478 1,373 -1,922 -155 -231 -48

Current transfers balance 5,770 8,322 9,758 7,960 7,899 8,274 9,334

Current-account balance 2,731 501 -1,331 -3,195 -748 1,091 5,166

External debt (US$ m)

Debt stock 29,351 32,830 32,616 29,656 b 31,233 31,212 29,151

Debt service paid e 2,487 2,740 3,131 5,187 b 2,471 3,485 4,346

Interest 773 881 934 806 b 688 661 686

International reserves (US$ m)

Total international reserves 25,581 31,374 33,849 33,933 36,543 38,770 39,544

a Actual. b Economist Intelligence Unit estimates. c Economist Intelligence Unit forecasts. d Fiscal year data ending June 30th. e Includes

prepayments of medium- and long-term debt in 2006-08.

Source: IMF, International Financial Statistics.

Country Report December 2010 www.eiu.com © The Economist Intelligence Unit Limited 2010