Journal Communications, Inc. is a media company that operates newspapers, television stations, radio stations, and websites across 12 states. The company generates most of its revenue from advertising sales. The analyst initiates coverage of Journal Communications with a Neutral rating and $8 price target due to concerns about weak advertising spending in 2008 and the company's exposure to struggling real estate markets. However, the company is transforming its business model and expanding its faster-growing internet and broadcast segments. The analyst expects the company's performance to improve in late 2008 and 2009 as the economy recovers and advertising spending increases.

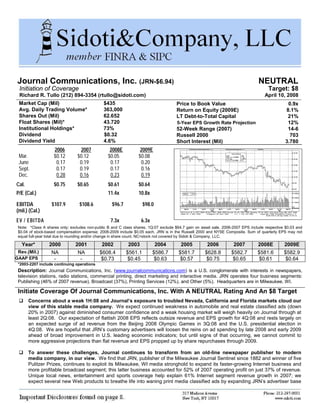

1. Journal Communications, Inc. (JRN-$6.94) NEUTRAL

Initiation of Coverage Target: $8

Richard R. Tullo (212) 894-3354 (rtullo@sidoti.com) April 10, 2008

Market Cap (Mil) $435 Price to Book Value 0.9x

Avg. Daily Trading Volume* 363,000 Return on Equity (2009E) 8.1%

Shares Out (Mil) 62.652 LT Debt-to-Total Capital 21%

Float Shares (Mil)* 43.720 12%

5-Year EPS Growth Rate Projection

Institutional Holdings* 73% 52-Week Range (2007) 14-6

Dividend $0.32 Russell 2000 703

Dividend Yield 4.6% Short Interest (Mil) 3.780

2006 2007 2008E 2009E

Mar. $0.12 $0.12 $0.05 $0.08

June 0.17 0.19 0.17 0.20

Sept. 0.17 0.19 0.17 0.16

Dec. 0.28 0.16 0.23 0.19

Cal. $0.75 $0.65 $0.61 $0.64

P/E (Cal.) 11.4x 10.8x

EBITDA $107.9 $108.6 $96.7 $98.0

(mil.) (Cal.)

EV / EBITDA 7.3x 6.3x

Note: *Class A shares only; excludes non-public B and C class shares. 1Q:07 exclude $64.7 gain on asset sale. 2006-2007 EPS include respective $0.03 and

$0.04 of stock-based compensation expense; 2008-2009 include $0.05 each. JRN is in the Russell 2000 and NYSE Composite. Sum of quarterly EPS may not

equal full-year total due to rounding and/or change in share count. NC=stock not covered by Sidoti & Company, LLC.

Year* 2000 2001 2002 2003 2004 2005 2006 2007 2008E 2009E

Rev.(Mil.) NA NA $608.4 $561.1 $586.7 $581.7 $628.8 $582.7 $581.6 $582.9

GAAP EPS - - $0.73 $0.45 $0.63 $0.57 $0.75 $0.65 $0.61 $0.64

*2003-2207 include continuing operations

Description: Journal Communications, Inc. (www.journalcommunications.com) is a U.S. conglomerate with interests in newspapers,

television stations, radio stations, commercial printing, direct marketing and interactive media. JRN operates four business segments:

Publishing (46% of 2007 revenue), Broadcast (37%), Printing Services (12%), and Other (5%). Headquarters are in Milwaukee, WI.

Initiate Coverage Of Journal Communications, Inc. With A NEUTRAL Rating And An $8 Target

Concerns about a weak 1H:08 and Journal’s exposure to troubled Nevada, California and Florida markets cloud our

view of this stable media company. We expect continued weakness in automobile and real estate classified ads (down

20% in 2007) against diminished consumer confidence and a weak housing market will weigh heavily on Journal through at

least 2Q:08. Our expectation of flattish 2008 EPS reflects outsize revenue and EPS growth for 4Q:08 and rests largely on

an expected surge of ad revenue from the Beijing 2008 Olympic Games in 3Q:08 and the U.S. presidential election in

4Q:08. We are hopeful that JRN’s customary advertisers will loosen the reins on ad spending by late 2008 and early 2009

ahead of broad improvement in U.S. leading economic indicators; but until signs of that occurring, we cannot commit to

more aggressive projections than flat revenue and EPS propped up by share repurchases through 2009.

To answer these challenges, Journal continues to transform from an old-line newspaper publisher to modern

media company, in our view. We find that JRN, publisher of the Milwaukee Journal Sentinel since 1882 and winner of five

Pulitzer Prizes, continues to exploit its Milwaukee, WI media stronghold to expand its faster-growing Internet business and

more profitable broadcast segment; this latter business accounted for 52% of 2007 operating profit on just 37% of revenue.

Unique local news, entertainment and sports coverage help explain 61% Internet segment revenue growth in 2007; we

expect several new Web products to breathe life into waning print media classified ads by expanding JRN’s advertiser base

2. JOURNAL COMMUNICATIONS INC.

and introducing new ad products to existing local advertisers. We argue that Journal will need to build upon its successful

Milwaukee model in newer markets, such as Las Vegas, NV and Fort Myers, FL, which are feeling the sting of major

housing slumps and subsequent steep declines in ad spending by auto and consumer retailers and real estate agencies.

We expect JRN’s broadcast business on the whole to benefit from an advertising rebound in 2H:08-2009. JRN’s

broadcast revenue declined 12% in a challenging 2007, but we expect improvement starting in 2H:08 owing to the Olympics

and presidential election. (During the last U.S. national election in 2006, Journal’s combined political and Olympic

advertising sales were $16.5 million despite a weakening economy; just $3.3 million was spent on local political advertising

in 2007.) We otherwise view aggressive interest rate cuts by the Federal Reserve as a catalyst to stimulate auto, financial

services and consumer durables ad growth by 2009 as national advertisers attempt to increase market share and local

advertisers piggyback national campaigns to boost sales. We also expect 3Q:07 improvements to JRN’s local daytime and

news programming will bolster the company’s ratings and market ranking, leading to higher ad rates.

A solid balance sheet and cash flow generation position JRN among the strongest in the peer group… JRN was in

line with the peer group (Exhibit I – page 5) for 2007 with $0.51 per share of free cash flow, implying about a 7% yield. We

expect FCF per share of $0.89 for 2008 and $1.01 in 2009 and expect management to use cash to buy back stock (2.7

million shares remain on the current authorization), pay down the comparatively low long-term debt to capital ratio (21%,

versus 30% for the peer group) and acquire small-market TV stations in regions where Journal already competes; we note

that JRN bought back 10 million shares and nearly halved long-term debt (to $140 million, from $274 million) since 4Q:05.

…but fail to incite investor interest in media companies with exposure to out-of-favor markets, in our view. We find

that JRN typically trades at a 15% discount to peer group EV/EBITDA multiples. We deem the current 40% discount a bit

excessive considering the relative stability of Journal’s core Milwaukee market and the area’s long-standing employers (i.e.

Harley-Davidson, Badger Meter and Johnson Controls) that buy advertising. That said, we cannot discount investor

concerns with Journal’s 10% revenue exposure to Nevada, California and Florida or management’s strategy of buying out-

of-favor TV and radio properties in growing U.S. communities (i.e., Las Vegas, Palm Springs, CA).

We initiate coverage of Journal Communications, Inc. with a NEUTRAL rating and an $8 price target. Although we

find tremendous potential for Journal to increase ratings and resultant advertising revenue of acquired TV stations in Las

Vegas and Palm Springs, we set a price target that appropriately balances the company’s flattish EPS prospects through

2009 against a lackluster ad environment and weakened domestic economy. We value JRN at an implied 20% discount to

the 10x peer average EBITDA multiple and at a P/E multiple of 12x our 2009 EPS estimate of $0.64, in line with our

normalized five-year EPS growth rate estimate of 12%. We would revisit our NEUTRAL rating with a decline in the share

price to about $6, assuming no change in the company’s fundamentals.

Company Overview Class B is a legacy of Journal Communications’ employee

ownership program; these 11.2 million shares carry 10

Journal Communication, Inc. is a media conglomerate that votes apiece and convert into one publicly traded Class A

operates 49 newspapers, 13 broadcast television stations, share. Class C shares (3.3 million) have two votes, pay a

35 radio stations and 121 websites that, combined, special $0.57 dividend (versus $0.32 annually for class A or

comprise more than 80% of annual revenue; JRN also B) and convert into 1.12 Class A shares plus 0.24 Class B

provides outsource printing and direct marketing services. shares. Insiders own 12.6% of the Class B shares; retired

and non-executive employees own the rest. JRN’s founding

Wisconsin is Journal’s primary market, but JRN operates in Grant family owns the Class C shares.

12 different states, including California, Florida and Nevada.

Journal’s media assets are in strong local communities with Whereas many of the Class B holders once purchased their

stable to above-average population growth and are linked shares using special financing from local banks, tighter

to either a state capitol or a major university. lending standards now discourage the use of privately-held

equity shares as collateral for bank loans. Thus, Journal’s

JRN has an experienced management team. CEO Steven current or retired employees sold 40 million Class B shares

Smith has been a director since 1987, and CFO Paul since the company’s IPO. Overall, we suggest that JRN’s

Bonaiuto has held various roles with the company since unique shareholder structure aligns management’s and the

1994. President Douglas Kiel, with JRN since 1986, current employees’ interests with public shareholders.

manages the TV and radio operations. Elizabeth Brenner,

Industry Overview

COO of publishing, was hired in 2004 after managing

publishing operations for McClatchy (NYSE: MNI, NC).

PricewaterhouseCoopers (PwC) projects the $1.3 trillion

Three-Tiered Share Structure global entertainment and media industry will grow 6.6% per

year through 2010. Media includes both physical and digital

Journal Communications went public in 3Q:03 via the sale formats and consists of TV and cable broadcasts, as well

of 30 million Class A shares priced at $15 per. Class A as newspapers, books, magazines, recorded music, radio,

shares (47.1 million) are the only publicly traded, and each billboards, movies, theatrical plays, gaming and interactive

has one vote. media. Revenue mostly derives from advertising sales and

paid subscriptions. The growth areas are licensed content

Sidoti & Company LLC

2

3. JOURNAL COMMUNICATIONS INC.

distribution, emerging markets and interactive media (i.e., in JRN’s production expense to $143 million in 2007 mostly

information, content and advertising delivered to mobile reflected lower newsprint and distribution expenses. JRN

devices, the Internet, and video games). reduced consumption 14%, and prices declined 12%.

Media in the U.S. is roughly a $500 billion industry and In 2007, the company consolidated the printing of the

grew 2.9% in 2007, as calculated by market researcher Journal Sentinel onto two of three presses to free the third

Universal McCann. U.S. media trailed global media growth for outsource printing of other newspapers. JRN’s high-

for a third straight year, due to a decline in housing and capacity presses can print 85,000-plus color newspapers

automobile related advertising. Moreover, U.S. government per hour. JRN’s two largest contracts are with USA Today

restrictions on media cross ownership and Internet (82,000 issues daily), published by Gannett (NYSE: GCI,

gambling also limited industry growth, in our view. NC), and the Chicago Reader (135,000 issues per week).

JRN’s print facilities operate at 80% of capacity; we think

Virtually every physical media product, such as newspapers there is enough capacity for JRN to expand its GCI

and music, has been converted into a digital format, and the relationship or add new clients.

newspaper industry has been especially hard hit. Classified

help wanted ad revenue (once 20% of industry sales) is In our view, the combined reach of JRN’s newspapers

down 90% since 1998 due to the introduction of Internet and Internet sites is the key to newspaper advertising

career websites. Automobile and real estate classifieds also growth. In the last 12-18 months, U.S.-based local

are falling (down 20% in 2007) amid a weak consumer and newspapers offset waning classified ad revenue with

housing economy. Circulation (sales of subscriptions and Internet ad revenue from news websites. Industry–wide

single copies) declines compound the industry ad sales digital ad revenue was up about 25% in 2007. We think

falloff because national advertisers, such as telecom and there is still room to grow as local Internet news products

healthcare companies, reduced newspaper advertising due can capture market share. According to media consultant

to a decrease in subscriptions Borrell Associates, local websites run by newspapers and

TV stations capture just 7% of the local internet advertising

JRN has responded to falling newspaper circulation and ad market (estimates of the entire Internet ad market run as

sales by selling its non-core community newspapers, print high as $20 billion).

facilities and telecom businesses to focus on core media

assets, expand its Internet product offering and enter new Typically, online advertisers pay a premium to advertise on

markets thought to provide faster growth than the core high-traffic sites. We think as JRN takes steps to improve

Milwaukee, WI, base. JRN sold the Northstar Print its Internet offering traffic, ad sales will grow. In March

Business in 2005 for $229 million, and purchased network- 2008, JRN entered into the Yahoo (NASDAQ: YHOO, NC)

affiliated TV stations in Tucson, AZ (ABC), Omaha, NE consortium of 300 newspapers. Yahoo will provide the

(CBS) and Naples/Ft. Myers, FL (FOX) for $238 million. In newspaper industry with Internet tools that will enable JRN

2007, JRN sold Norlight Telecommunications, a phone, to: 1) increase website traffic; 2) sell traditional newspaper

Internet and data management services provider in the advertising on the Internet to national advertisers; and 3)

Midwest, for $185 million, as well as local newspapers in provide web-based tools such as a paid local search. We

Ohio, Louisiana and New England. JRN booked a $62 think by entering the Yahoo consortium JRN will have a

million gain on the Norlight sale in 1Q:07. competitive Internet offering. We project 30% average

annual Internet ad revenue growth through 2009 for JRN as

Publishing (46% Revenue) more advertisers discover the benefit of newspaper-run

websites. We expect JRN will offset waning newspaper

JRN operates 49 weekly and local newspapers, but we find revenue with Internet ad sales as its newspaper websites

the Milwaukee Journal Sentinel (JS) is by far the company’s develop better advertising vehicles and tools for

most important asset. The JS, founded in 1882 and winner advertisers.

of six Pulitzers, has a weekly circulation of 220,000 and a

Sunday circulation of 391,000. JS Sunday circulation We point to industry data to suggest that JRN’s local papers

declined 2.6% in 2007, versus 3.5% for the industry. We and websites reach a large relative audience and will prove

think JRN’s stronger relative performance reflects the to be a more attractive venue to advertisers than media

Journal Sentinel’s focus on the greater Milwaukee behemoths and news aggregators, such as Google

community and in-depth coverage of local politics and (NASDAQ: GOOG, NC). Audience-FAX, a partnership

sports, namely the Green Bay Packers, Milwaukee between Audit Bureau of Circulations (ABC) and Arbitron

Brewers, Milwaukee Bucks and college teams. We think (NYSE: ARB, BUY), shows that JS and jsonline.com reach

newspaper sales comprise just 20% of publishing sales, but 75% of Milwaukee’s college graduates (a highly sought

largely determine the ad rate Journal charges in our view; demographic for advertisers) per week. By contrast, popular

so declines affect retail and national advertising sales. local TV or radio news programs might capture 10%, while

major market papers, such as the New York Daily News

We pin as much as 50% of Journal’s circulation decline on (1.2 million readers daily), will reach only 25%. In our view,

preemptive expense control, as management curtailed local papers such as JS, with limited competition and

unprofitable circulation in order to rein in energy and exclusive content, can compete against far bigger outlets

newsprint costs. Newsprint, paper, energy and skilled labor and capture greater local online market share from national

are the bulk of production expenses. Newsprint costs are advertisers seeking a trusted source for more-captive

volatile, at 12%-14% of production expense. A 4% decline

Sidoti & Company, LLC

3

4. JOURNAL COMMUNICATIONS INC.

Printing Services (12%) and Other Revenue (5%)

audiences in less-competitive markets, as opposed to a

small slice of a major market such as New York City.

Printing Services includes IPC Print Services in St. Joseph

Broadcast (37% of Revenue) Michigan which prints short to medium run magazines and

product manuals. In 2007, revenue grew 3.6% as IPC

JRN’s TV and radio stations accounted for about one-third increased business with existing customers and added new

of 2007 revenue, but 52% of income from operations. JRN higher margin clients. We forecast 2.6% annual printing

broadcasts 13 TV stations and 35 radio stations, each with sales growth in the next two years, based on our

a corresponding website, in markets anchored by the state assumption that the economy improves in 2H:08 and 2009.

capitol or large universities. We favor this strategy because

these communities tend to be economically stable and are “Other” includes the Journal’s PrimeNet marketing services

active. As such, JRN’s communities create the demand for arm, which provides database and direct mail services, and

the company’s media content, in our view. so-called “eliminations,” or sales of products and services

between JRN divisions. Other sales declined 23% in 2007

JRN’s broadcast revenue comes from advertisements aired to $28.9 million on an increase in eliminations (deducted

during news and local TV and radio programming. JRN from revenue) and a decline in marketing services demand

cross sells ad space on its websites and collects due to economic weakness. We expect flattish “Other

retransmission (carriage) fees from cable systems that revenue” of $24.9-$25.6 million annually in 2008 and 2009

distribute its TV channels. Ad rates are determined by as increased eliminations offset modest services growth.

audience size, the advertising customer and audience

Risks

income, as well as Nielsen (TV) and Arbitron (radio) ratings.

Local advertisers pay higher rates than national advertisers;

they typically buy fewer slots and have limited alternatives, Union activity. JRN’s print and broadcast operations are in

but need to advertise locally to generate sales. JRN boasts part staffed by union employees, so any prolonged strike

strong local ad sales: 72% of TV ad slots and 80% of radio would hurt Journal’s earnings.

ad slots are filled by local advertisers. This signifies to us

the benefits of a strong connection to smaller communities Economic. Most media industry revenue is based on

and less reliance, versus many peers, on network advertising. Advertising revenue is cyclically sensitive, with

programming or volatile budgets of national advertisers. advertisers typically cutting back on discretionary ad

purchases during periods of economic slowness.

Only five of JRN’s 47 TV and radio stations, however, are in

its core Wisconsin market. The others span 11 states, six of Plant Disruption. JRN consolidated print operations to its

which we consider (including Wisconsin and Florida) as key Milwaukee facility; any disruption in production could affect

battlegrounds (i.e., greater advertising revenue) in the 2008 both JRN’s publishing and commercial print operations.

Presidential election.

The Internet crippled newspaper classified ad sales; to a

JRN’s top line included $16.5 million of TV/radio political lesser extent, the expansion of TV/radio channels altered

advertising (local and state) in 2006 and only $3.3 million in the broadcast ad landscape. A decline in broadcast

2007. We expect Journal to benefit in 2008, with total U.S. advertising revenue could hurt sales and earnings;

election advertising spending expected to exceed (by most however, JRN is diversifying its ad revenue stream by way

industry forecasts) the previous (2006) record of $2.1 billion of new Web products and tuck-in acquisitions.

because the U.S. Supreme Court lifted restrictions on

Recent Results

special interest ads. We also expect JRN’s three NBC

affiliates to benefit from the 2008 Olympics; for comparison,

In 2007, revenue fell 7.3% to $583 million as ad sales

the 2006 winter games contributed revenue of $3.3 million.

tracked the cyclical slowdown in the economy, political ad

revenue slipped $13 million from a 2006 election year, and

New local programming, improved news broadcasts (i.e., in

Journal’s Sunday newspaper circulation declined 2.6%.

Las Vegas) and expected 2H:09 renegotiation of carriage

Publishing revenue declined 5.9% to $268 million.

rates with Cablevision (NYSE: CVC, NC) and Time Warner

Recurring non-political broadcast revenue declined 7% to

(NYSE: TWX, NC) are other revenue catalysts, in our view.

$209.7 million (from $225.3 million) absent the 2006

Less than 1% of JRN’s broadcast revenue is from carriage,

political ad revenue. However, Printing Services grew 3.6%

but we expect new contracts to generate $3-$7 million of

to $69 million (from $66 million).

incremental revenue (based on $0.25-$1.00 fees cable

channels typically get per subscriber). New programs, such

Operating costs ebbed 4% in 2007 to $501 million with staff

as the Milwaukee talk show “Morning Blend”, may provide

cutbacks in publishing and less newsprint consumption

upside to our EPS estimates, since the show is less

amid circulation declines and the reduction in width (web

expensive to air than comparable syndicated talk shows

size) of the Journal Sentinel. The operating margin

and will likely attract high-margin local advertisers, in our

narrowed 310 basis points to 13.5% in 2007, from 16.6% in

view. JRN plans to roll out versions of the show to other

2006, as the above-mentioned cost reductions did not offset

local markets in 2008. In Las Vegas, JRN hired the leading

the revenue decline. The tax rate fell to 38%, from 40% in

news anchors away from rivals and revamped its entire

2006. Excluding gains on asset sales, however, 2007 EPS

format to appeal to the local audience in the hopes of rising

declined 13% to $0.65, from $0.75 in 2006.

from No. 3 in the ratings.

Sidoti & Company, LLC

4

5. JOURNAL COMMUNICATIONS INC.

Earnings Outlook compares with 30% for the peer group, though we find that

investors seemingly give little reward to this metric in

We expect continued challenges for the media industry, and valuing JRN stock. Since 4Q:05, JRN bought back 10

Journal in particular, at least through the first half of 2008, million shares and reduced debt to $140 million from $274

owing to weakness in automobile and classified advertising million. We forecast continued debt reduction (to 19% of

declines (down 20% in 2007) and weakness in the housing total capital) by the end of 2009. Journal’s returns on assets

market. As well, we suspect political and Olympic spending and equity for 2007 declined to 5% (from 5.7%) and 8.8%

will do little to prop up 1H:08 EPS. (from 11.4%), respectively, hurt by the decline in net

income with the sale of North Star and weakness in the

By 2H:08, we think Journal will benefit from an improved ad newspaper industry. We target diminished ROA and ROE

environment as the Olympics and presidential election lead in 2009 of 4.7% and 8.1%, respectively.

to top-line growth of 2% in 3Q:08 and 16% in 4Q:08, by our

model. Since we project that a 7.5% increase in high- The sale of Journal’s profitable telecom business (Norlight)

margin broadcast ad sales offsets a 2.5% decline in lower- helped to explain the 2007 FCF decline to $0.51 per share,

margin publishing sales, we estimate operating margin from $1.40 in 2006. Nonetheless, we argue that JRN’s

expansion of 80 basis points to 14.3% in 2H:08, from 13.5% 13.5% FCF yield is quite attractive. We forecast FCF per

in 2H:07. Based on these assumptions, we project a 14% share of $0.89 for 2008 and $1.00 for 2009. As noted, we

2H:08 EPS advance to $0.40 (from $0.35 in 2H:07). think JRN will use FCF to pay down debt and buy back

stock. There are 2.7 million shares outstanding in the

We predict 2008 net income from continuing operations will current program.

slip to $39 million, from $43 million in 2007, but that JRN

Valuation

will put cash toward stock buybacks (reducing the diluted

share count 8.6% from 2007), debt repayment and small

bolt-on acquisitions. Thus, we predict a 16% interest We find tremendous potential for Journal to increase ratings

expense decline in 2008 to $7.7 million (from $9.2 million in and resultant advertising revenue of acquired TV stations in

2007) and EPS to decline to $0.61, from $0.65 in 2007. We Las Vegas and Palm Springs, CA, but set a price target that

expect JRN’s tax rate to decline to 34.9%, from 38.2% in appropriately balances flattish EPS prospects through 2009

2007, absent capital gains on asset divestitures. against a lackluster advertising environment and weakened

domestic economy.

We think the recent Fed rate cuts will stimulate automotive

and housing advertising improvement in 2009 and offset the We are concerned by JRN’s growing 10% top-line exposure

loss of political advertising, but forecast flattish revenue of to Nevada, California and Florida and the related affect on

$583 million against a projected 1%-2% slide in newspaper 2008 and 2009 results. Management’s strategy of buying

circulation. We expect JRN to command higher broadcast out-of-favor TV and radio properties in growing U.S.

TV and radio rates due to the steps taken to strengthen the communities (i.e. Las Vegas, Palm Springs, CA) has great

broadcast schedule and ratings with new programs and potential, in our view, but the economic downturns and

news personalities. We suggest increased Internet ad sales associated ad revenue declines in those markets may offset

will offset a circulation decline at the Journal Sentinel and any programming-related revenue gains, in our view.

that publishing will grow 2.0% in 2009. We expect the

operating margin to hold steady at 11.8% based on our We value JRN at price-to-earnings multiple of 12x our $0.64

projection that income from continuing operations is about 2009 EPS estimate to set an $8 price target. This valuation

flat at $39.2 million against a $20 million drop in political ad implies steep discounts to media conglomerate peers (see

revenue. We forecast a 5% EPS advance to $0.64 in 2009 Exhibit I) on the basis of EPS (a 30% discount) and

based on the repurchase of 2.6 million shares. EV/EBITDA (40% discount, versus the 15% average).

Balance Sheet and Cash Flow Although we find the latter discount overdone, we initiate

coverage of JRN shares with a NEUTRAL rating, since we

JRN has a strong balance sheet and ample free cash flow think the weak ad markets in Las Vegas and Florida will

(FCF) that allows the company to create shareholder value keep a lid on annual EPS growth (absent buybacks)

by paying down debt and buying back stock. JRN’s long- through 2009. We would revisit our rating if JRN shares

term debt to capital ratio of 21% at the end of 2007 decline below $6 with no change in fundamentals.

Exhibit I. Journal Communications Comparable Table

P/BV FCF/P EV/EBITDA Curent

EPS Forward LT-Debt/ 5Yr.

2007 2009 2007 Ratio

Company Rating Ticker PX MCAP 2009E P/E Capital PEG

1.0 13.4%

Journal Communications JRN $7.46 $430 $0.64 11.7 7.1 1.4 21% 0.97

NEUTRAL

4.6%

News Corp NC NWS.A $19.32 $58,200 $1.44 13.4 1.8 11.7 1.5 25% 0.81

NM

The New York Times Company NC NYT $19.16 $2,590 $1.10 17.4 2.8 7.2 0.7 41% NM

4.0%

Hearst-Argyle Television Inc. NC HTV $21.62 $2,007 $0.80 27.0 1.1 16.7 1.1 30% 3.9

19.6%

Media General Inc. BUY MEG $15.68 $358 $1.32 11.9 0.4 8.7 1.6 51% 0.74

4.3%

The Washington Post Co. NC WPO $671.00 $6,375 $34.25 19.6 2.3 11.3 1.0 10% 2.80

Industry Average: 17.9 1.6 9.2% 10.4 1.2 30% 2.05

Source: Sidoti & Company, LLC Estimates, First Call and company reports

Sidoti & Company, LLC

5

6. JOURNAL COMMUNICATIONS, INC.

T ab le 1 . J o u rn al C o m m u n ica tio n s

In c o m e S ta tem e n t

2006 M ar. Jun. Sep. Dec 2007 Mar. Jun. Sep. Dec 2008E Mar. Jun. Sep. Dec 2009E

REVENUE 6 2 8 ,7 6 3 1 5 2 ,8 3 1 1 4 7 ,4 6 4 1 4 4 ,3 7 9 147,617 582,654 140,002 141,472 143,575 156,559 581,608 142,317 147,839 143,271 149,502 582,929

A n n u a l C h an g e 8 .0 9 % -2 .2 7 % -4 .2 6 % -5 .6 3 % -20.9% -7.3% -8.4% -4.1% -0.6% 6.1% -0.2% 1.7% 4.5% -0.2% -4.5% 0.2%

O p er a tin g co sts:

P u b lish in g 1 4 9 ,8 9 8 4 2 ,8 2 8 3 5 ,4 7 6 3 4 ,1 7 2 36,798 143,321 41,757 34,589 33,318 35,878 145,542 42,789 35,444 34,141 36,765 149,140

B ro ad c ast 9 5 ,7 4 5 2 2 ,3 9 5 2 3 ,7 3 5 2 5 ,4 6 2 25,332 96,924 23,291 25,159 26,990 26,852 102,292 23,757 25662 27,530 27,389 104,337

P rin tin g 5 6 ,1 2 9 1 4 ,1 6 5 1 3 ,4 0 7 1 3 ,7 5 8 13,982 55,313 14,590 13,809 13,772 14,401 56,572 15,465 14,638 14,598 15,266 59,967

O th e r 3 2 ,8 9 3 6 ,9 2 4 6153 6 ,1 5 5 5,428 24,659 6,993 6,215 6,217 5,482 24,907 7,203 6,401 6,403 5,647 25,654

S e llin g an d a d m in istra tiv e 1 8 9 ,4 9 8 4 9 ,3 4 6 4 5 ,9 4 8 4 3 ,3 6 8 48,126 183,649 46,201 43,856 44,508 50,099 184,664 42,695 44,352 42,981 44,850 174,879

D ep r ec ia tio n a n d a m o r tiza tio n 2 9 ,0 7 8 7 ,7 1 4 7 ,0 3 8 7 ,2 6 0 7,260 29,272 7,260 7,260 7,260 7,260 29,040 7,260 7,260 7,260 7,260 29,040

T o ta l o p e ra tin g c o sts 5 2 4 ,1 6 3 1 3 5 ,6 5 8 1 2 4 ,7 1 9 1 2 2 ,9 1 5 129,666 500,866 132,832 123,628 124,804 132,713 513,977 131,910 126,497 125,653 129,917 513,976

O p era tin g in c o m e 1 0 4 ,6 0 0 1 7 ,1 7 3 2 2 ,7 4 5 2 1 ,4 6 4 17,951 78,788 7,170 17,844 18,771 23,847 67,631 10,408 21,342 17,618 19,585 68,953

O p era tin g M a rg in 1 6 .6 % 1 1 .2 % 1 5 .4 % 1 4 .9 % 12.2% 13.5% 5.1% 12.6% 13.1% 15.2% 11.6% 7.3% 14.4% 12.3% 13.1% 11.8%

O th e r in co m e (e x p e n se ):

In terest in c o m e 37 2 1 23 10 36 12 12 12 12 48 12 12 12 12 48

In terest ex p en se (1 5 ,6 0 7 ) (2 ,9 9 5 ) (1 ,9 8 3 ) (1 ,9 3 7 ) (2,261) (9,180) (1,937) (1,937) (1,937) (1,937) (7,748) (1,937) (1,937) (1,937) (1,937) (7,748)

T o ta l o th e r in co m e (ex p e n se) (1 5 ,5 7 0 ) (2 ,9 9 3 ) (1 ,9 8 2 ) (1 ,9 1 4 ) (2,251) (9,144) (1,925) (1,925) (1,925) (1,925) (7,700) (1,925) (1,925) (1,925) (1,925) (7,700)

E a rn in g s fro m co n tin u in g o p e ra tio n s b /f ta x 8 9 ,0 3 0 1 4 ,1 7 8 2 0 ,7 6 2 1 9 ,5 5 0 15,700 69,644 5,245 15,919 16,846 21,922 59,931 8,483 19,417 15,693 17,660 61,253

In c o m e ta x e s 3 5 ,2 4 7 5 ,6 0 6 8 ,0 6 0 6 ,9 4 4 5,459 26,626 1,731 5,253 6,065 7,892 20,940 3,054 6,990 5,649 6,358 22,051

T ax % 3 9 .6 % 3 9 .5 % 3 8 .8 % 3 5 .5 % 35.0% 38.2% 33.0% 33.0% 36.0% 36.0% 34.9% 36.0% 36.0% 36.0% 36.0% 36.0%

In c o m e fro m co n tin u in g o p e ra tio n s 5 3 ,7 8 3 8 ,5 7 2 1 2 ,7 0 2 1 2 ,6 0 6 10,241 43,018 3,514 10,665 10,781 14,030 38,991 5,429 12,427 10,043 11,302 39,202

D isco n tin u ed o p eratio n s:

In c o m e(L o ss) fro m d isc . o p s (n et o f in co m e ta x e s) 1293 (772)

G ain (L o ss)o n sale o f o p s (n et o f in c o m e T ax ) 1 0 ,5 9 0 6 4 ,7 5 9 1448 67,060

N et in co m e (lo ss) 6 4 ,3 7 3 7 3 ,3 3 1 1 4 ,1 5 0 1 3 ,8 9 9 9,469 110,078 3,514 10,665 10,781 14,030 38,991 5,429 12,427 10,043 11,302 39,202

E a rn in g s a v a ilab le to cla ss a,b sh a re h o ld ers 6 2 ,5 1 8 72867 13686 13436 9,002 108,991 3,047 10,198 10,314 13,563 37,123 4,962 11,960 9,576 10,835 37,334

E a rn in g s (lo ss) p er c o m m o n sh a re:

E a rn in g s(lo ss) p er sh a re $ 0 .8 0 $ 0 .1 3 $ 0 .1 9 $ 0 .2 0 $0.17 $0.66 $0.05 $0.18 $0.19 $0.24 $0.66 $0.09 $0.22 $0.18 $0.20 $0.70

D isco n tin u ed O p era tio n s (n e t) $ 0 .1 3 $ 0 .9 3 $ 0 .0 3 $ 0 .0 2 ($0.01) $1.08

N et in c o m e (lo ss) p e r sh are $ 0 .9 3 $ 1 .0 5 $ 0 .2 2 $ 0 .2 2 $0.15 $1.74 $0.05 $0.18 $0.19 $0.24 $0.66 $0.09 $0.22 $0.18 $0.20 $0.70

D ilu ted e a rn in g s(lo ss) p e r sh a re $ 0 .7 5 $ 0 .1 2 $ 0 .1 9 $ 0 .1 9 $0.16 $0.65 $0.05 $0.17 $0.17 $0.23 $0.61 $0.08 $0.20 $0.16 $0.19 $0.64

S h a re s O u tsta n d in g

B asic 6 7 ,4 7 5 6 9 ,3 9 7 6 2 ,2 0 9 6 1 ,0 7 3 58,138 62,276 56,938 55,738 55,738 55,738 56,038 54,956 54,175 54,175 53,394 53,394

D ilu te d 7 1 ,9 8 4 6 9 ,3 9 7 6 5 ,1 7 1 6 3 ,9 8 1 62,652 66,809 61,402 60,152 60,152 60,152 60,465 59,371 58,590 58,590 57,809 58,590

D iv id en d s 0 .2 6 0 .0 7 5 0 .0 7 5 0 .0 7 5 0.075 0.30 0.08 0.08 0.08 0.08 0.32 0.08 0.08 0.08 0.08 0.32

E B IT D A 1 3 3 ,7 1 5 2 4 ,8 8 7 2 9 ,7 8 3 2 8 ,7 4 7 25,221 108,096 14,442 25,116 26,043 31,119 96,719 17,680 28,614 24,890 26,857 98,041

E B IT D A T T M 1 3 3 ,7 1 5 1 3 4 ,6 8 9 1 2 5 ,7 4 7 1 0 9 ,1 1 5 108,638 108,638 98,193 93,526 90,822 96,719 96,719 99,956 103,455 102,302 98,041 98,041

E B IT D A p e r sh are 1 .8 6 1 .9 4 1 .9 3 1 .7 1 1.73 1.63 1.60 1.55 1.51 1.61 1.60 1.68 1.77 1.75 1.70 1.67

E V /E B IT D A 8 .5 2 7 .5 7 .7 6 .9 6.4 7.1 7.3 7.5 7.7 7.3 7.3 6.8 6.5 6.6 6.9 6.3

G ro ss M arg in 4 6 .8 % 4 3 .5 % 4 6 .6 % 4 4 .9 % 44.8% 45.0% 38.1% 43.6% 44.1% 47.2% 43.4% 37.3% 44.4% 42.3% 43.1% 41.8%

E B IT M arg in 1 3 .4 % 4 9 .7 % 1 3 .7 % 1 3 .1 % 8.6% 21.9% 2.4% 9.9% 10.4% 12.8% 9.0% 4.6% 11.8% 9.6% 10.5% 9.2%

E B IT D A M a rg in 2 1 .3 % 8 8 .1 % 8 5 .3 % 7 5 .6 % 73.6% 18.6% 70.1% 66.1% 63.3% 61.8% 16.6% 70.2% 70.0% 71.4% 65.6% 16.8%

N et M arg in 1 0 .2 % 4 8 .0 % 9 .6 % 9 .6 % 6.4% 18.9% 2.5% 7.5% 7.5% 9.0% 6.7% 3.8% 8.4% 7.0% 7.6% 6.7%

A nnual change

T o ta l re v e n u e 8 .1 % -2 .3 % -4 .3 % -5 .6 % -20.9% -7.3% -8.4% -4.1% -0.6% 6.1% -0.2% 1.7% 4.5% -0.2% -4.5% 0.2%

O p era tin g c o sts 3 .5 % -1 .2 % -3 .5 % -4 .4 % -13.0% -4.4% -2.1% -0.9% 1.5% 2.3% 2.6% -0.7% 2.3% 0.7% -2.1% 0.1%

EPS 1 9 .0 % -7 .7 % 1 1 .8 % 1 1 .8 % -49.7% -13.3% -58.6% -10.8% -9.8% 44.5% -6.2% 68.4% 20.4% -4.7% -16.9% 9.8%

S o u rce : S id o ti & C o m p a n y , L L C E stim ate s a n d co m p an y rep o rts

Sidoti & Company, LLC

6

7. JOURNAL COMMUNICATIONS, INC.

T a b le 2 . J o u r n sl C o m m u n ic a tio n s

Q u a r te r ly S ta te m e n t o f C a sh F lo w s

(0 0 0 s) 2006 M a r. A Ju n. A S ep. A D ec A 2007A 2008E 2009E

N et Incom e 6 4 ,3 7 3 7 3 ,3 3 1 1 4 ,1 5 0 1 3 ,8 9 9 8 ,6 9 8 1 1 0 ,0 7 8 3 8 ,9 9 1 3 9 ,2 0 2

G a in fro m d is c o n tin u e d o p e ra tio n s 8 ,6 3 6 6 4 ,7 5 9 1 ,7 8 0 1 ,2 9 3 1 ,1 0 0 6 7 ,0 6 0

E a rn in g s fro m c o n tin u in g o p e ra tio n s 5 5 ,7 3 7 8 ,5 7 2 1 2 ,3 7 0 1 2 ,6 0 6 7 ,5 9 8 4 3 ,0 1 8 3 8 ,9 9 1 3 9 ,2 0 2

A d ju stm e n ts

D e p re c ia tio n 2 7 ,8 8 7 7 ,2 2 5 6 ,5 7 7 6 ,7 6 2 6 ,7 6 2 2 7 ,4 0 7 2 7 ,0 4 8 2 7 ,0 4 8

A m o rtiz a tio n 2 ,0 6 0 489 461 498 498 1 ,9 6 1 1 ,9 9 2 1 ,9 9 2

W rite -o ff o f fin a n c in g c o s ts

P ro v is io n fo r d o u b tfu l a c c o u n ts 1 ,4 8 1 71 382 564 400 1 ,6 4 6 1 ,9 0 0 1 ,4 0 0

D e fe rre d in c o m e ta x e s 6 ,8 8 7 (3 ,8 4 7 ) 1 ,0 9 1 (8 5 5 ) 7 ,9 2 1 (1 ,2 7 5 ) (3 ,0 0 0 ) 6 ,0 2 5

N o n -c a sh c o m p e n sa tio n 1 ,3 7 3 249 880 256 300 1 ,8 2 9 2 ,0 0 0 2 ,0 0 0

C u rta ilm e n t g a in s fo r d e fin e d b e n e fit a n d p e n s io n p la n s (2 ,4 0 2 )

N e t lo s s (g a in ) fro m d is p o s a l o f b u s in e s s a n d a s s e ts (3 ,4 4 3 ) (3 9 ) (8 6 1 ) (4 ) (7 4 4 )

N e t o p e ra tin g a c tiv itie s o f d is c o n tin u e d o p e ra tio n s 2 7 ,3 2 9 2 ,7 7 3 1 8 ,7 3 8 (2 1 ,5 1 1 ) -

N e t c h a n g e s in o p e r a tin g a s s e ts a n d lia b ilitie s

R e c ie v a b le s (7 ,6 0 8 ) 7 ,1 7 5 (5 ,4 9 9 ) (2 ,2 6 2 ) ( 1 ,0 4 7 ) (4 1 2 ) 3 ,2 0 0 (2 ,8 9 4 )

In v e n to rie s 862 798 (1 2 0 ) (2 2 4 ) 200 (5 0 6 ) (9 4 5 ) 316

A c c o u n ts p a y a b le (6 ,1 5 6 ) (6 ,6 9 3 ) 695 1 ,4 9 7 (1 ,0 8 2 ) 650 (1 ,8 7 6 )

O th e r a s s e ts a n d lia b ilitie s 1 5 ,9 9 2 ( 1 2 ,1 8 7 ) 5 ,9 0 6 (2 ,8 3 5 ) (5 ,2 0 1 ) (3 ,4 3 4 )

N e t c a s h p r o v id e d b y o p e r a tin g a c tiv itie s 1 1 9 ,9 9 9 4 ,5 8 5 (2 ,3 9 7 ) 3 7 ,5 1 0 4 ,5 8 5 6 6 ,6 4 1 6 8 ,4 0 1 7 3 ,2 1 2

C F fr o m In v e s tm e n ts

C a p ita l e x p e n d itu re s ( 2 2 ,2 2 3 ) (7 ,8 5 5 ) (9 ,0 3 8 ) (6 ,6 5 6 ) ( 5 ,5 0 0 ) (3 5 ,9 0 6 ) ( 1 4 ,8 0 0 ) ( 1 4 ,8 0 0 )

P ro c e e d fro m s a le s o f a s s e ts 2 ,8 7 1 63 2 ,0 0 3 658 3 ,3 9 1

A c q u is itio n o f b u s in e s s e s 7 ,2 5 2 ( 1 1 ,4 2 5 ) 0 (1 7 1 ) (1 2 ,2 2 1 )

P ro c e e d s fro m s a le o f b u s in e s s ( 1 4 ,9 4 7 ) 1 7 6 ,3 9 5 8 ,8 5 9 1 9 ,9 6 4 2 0 5 ,0 0 7

N e t In v e s tin g o f d is c o n tin u e d o p s (6 4 1 ) (3 8 ) 679 -

( 2 7 ,0 4 7 ) 1 5 6 ,5 3 7 1 ,7 8 6 1 4 ,4 7 4 (5 ,5 0 0 ) 1 6 0 ,2 7 1 (1 4 ,8 0 0 ) (1 4 ,8 0 0 )

C a s h P r o v id e d b y (u s e d in ) I n v e s tin g A c tiv itie s

C F fr o m F in a n c in g A c tiv itie s

F in a n c in g c o s ts o n n o te s p a y a b le

P ro c e e d s fro m lo n g -te rm n o te p a y a b le 2 2 4 ,0 5 2 9 9 ,3 4 5 7 6 ,5 4 0 8 9 ,5 7 0 8 9 ,5 7 0 3 4 3 ,3 1 0

P a y m e n ts o f lo n g te rm n o te p a y a b le ( 2 6 3 ,5 9 7 ) ( 2 2 9 ,0 6 5 ) ( 6 3 ,4 6 5 ) (5 8 ,8 0 5 ) ( 8 1 ,7 3 1 ) ( 3 9 9 ,4 2 5 )

N e t n o te p a y a b le ( 3 9 ,5 4 5 ) ( 1 2 9 ,7 2 0 ) 1 3 ,0 7 5 3 0 ,7 6 5 7 ,8 3 9 (5 6 ,1 1 5 ) ( 1 2 ,7 8 0 ) ( 1 5 ,0 0 0 )

P ro c e e d s fro m is s u a n c e o f c o m m o n s to c k 1 ,3 3 2 321 1 322

R e d e m p tio n o f c o m m o n sto c k ( 3 4 ,2 3 7 ) ( 2 8 ,1 1 1 ) (6 ,9 4 4 ) (4 3 ,9 0 9 ) ( 1 0 2 ,3 9 6 ) ( 2 0 ,0 0 0 ) ( 2 5 ,0 0 0 )

C a s h d iv id e n d s ( 1 9 ,4 4 3 ) (5 ,3 6 5 ) (5 ,2 4 4 ) (5 ,0 0 5 ) ( 5 ,0 0 5 ) (2 0 ,4 4 5 ) ( 1 9 ,8 1 3 ) ( 1 9 ,8 1 3 )

( 9 1 ,8 9 3 ) (1 6 3 ,1 9 6 ) 1 ,2 0 8 ( 1 8 ,1 4 8 ) 2 ,8 3 4 ( 1 7 8 ,6 3 4 ) (5 2 ,5 9 3 ) (5 9 ,8 1 3 )

C a s h P r o v id e d b y (u s e d in ) F in a n c in g A c tiv itie s

N e t c a s h fr o m d is c o n tin u e d o p e r a tio n s (3 3 ,6 2 2 ) ( 2 ,3 2 3 ) (4 9 ,9 4 5 )

In c re a s e (D e c re a s e ) in c a s h a n d e q u iv a le n ts 1 ,0 5 9 (2 ,0 7 4 ) 597 214 1 ,9 1 9 (1 ,6 6 7 ) 1 ,0 0 8 (1 ,4 0 1 )

C a sh , b e g in n in g 5 ,7 7 0 7 ,9 2 3 5 ,8 4 9 6 ,4 4 6 6 ,6 6 0 7 ,9 2 3 6 ,2 5 6 7 ,2 6 4

C a s h , e n d in g 7 ,9 2 3 5 ,8 4 9 6 ,4 4 6 6 ,6 6 0 6 ,2 5 6 6 ,2 5 6 7 ,2 6 4 5 ,8 6 3

C a s h , c a sh a n d s/t in v e s tm e n ts, e n d in g 7 ,9 2 3 5 ,8 4 9 6 ,4 4 6 6 ,6 6 0 6 ,2 5 6 6 ,2 5 6 7 ,2 6 4 5 ,8 6 3

F re e C a sh F lo w 1 0 0 ,6 4 7 (3 ,2 0 7 ) (9 ,4 3 2 ) 3 1 ,5 1 2 (9 1 5 ) 3 4 ,1 2 6 5 3 ,6 0 1 5 8 ,4 1 2

F C F P e r S h a re 1 .4 0 (0 .0 5 ) (0 .1 4 ) 0 .4 9 (0 .0 1 ) 0 .5 1 0 .8 9 1 .0 1

S o u r c e : S i d o t i & C o m p a n y , L L C E s t i m a t e s a n d c o m p a n y r e p o rrtt s

Sidoti & Company, LLC

7