Q1 2014 net lease drug store report

•

1 like•395 views

net lease drug store research report

Recommended

Recommended

More Related Content

Similar to Q1 2014 net lease drug store report

Similar to Q1 2014 net lease drug store report (20)

More from The Boulder Group

More from The Boulder Group (20)

Recently uploaded

Recently uploaded (20)

Q1 2014 net lease drug store report

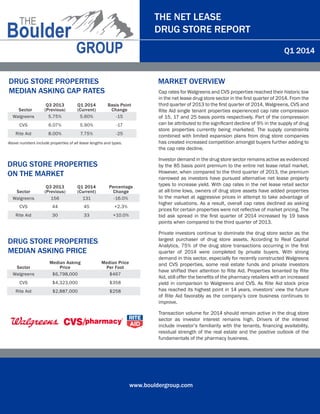

- 1. www.bouldergroup.com THE NET LEASE DRUG STORE REPORT Q1 2014 DRUG STORE PROPERTIES MEDIAN ASKING CAP RATES Q3 2013 Q1 2014 Basis Point Sector (Previous) (Current) Change Walgreens 5.75% 5.60% -15 CVS 6.07% 5.90% -17 Rite Aid 8.00% 7.75% -25 DRUG STORE PROPERTIES ON THE MARKET Q3 2013 Q1 2014 Percentage Sector (Previous) (Current) Change Walgreens 156 131 -16.0% CVS 44 45 +2.3% Rite Aid 30 33 +10.0% DRUG STORE PROPERTIES MEDIAN ASKING PRICE Median Asking Median Price Sector Price Per Foot Walgreens $6,798,000 $467 CVS $4,323,000 $358 Rite Aid $2,887,000 $258 MARKET OVERVIEW Cap rates for Walgreens and CVS properties reached their historic low in the net lease drug store sector in the first quarter of 2014. From the third quarter of 2013 to the first quarter of 2014, Walgreens, CVS and Rite Aid single tenant properties experienced cap rate compression of 15, 17 and 25 basis points respectively. Part of the compression can be attributed to the significant decline of 9% in the supply of drug store properties currently being marketed. The supply constraints combined with limited expansion plans from drug store companies has created increased competition amongst buyers further adding to the cap rate decline. Investor demand in the drug store sector remains active as evidenced by the 85 basis point premium to the entire net lease retail market. However, when compared to the third quarter of 2013, the premium narrowed as investors have pursued alternative net lease property types to increase yield. With cap rates in the net lease retail sector at all-time lows, owners of drug store assets have added properties to the market at aggressive prices in attempt to take advantage of higher valuations. As a result, overall cap rates declined as asking prices for certain properties were not reflective of market pricing. The bid ask spread in the first quarter of 2014 increased by 19 basis points when compared to the third quarter of 2013. Private investors continue to dominate the drug store sector as the largest purchaser of drug store assets. According to Real Capital Analytics, 75% of the drug store transactions occurring in the first quarter of 2014 were completed by private buyers. With strong demand in this sector, especially for recently constructed Walgreens and CVS properties, some real estate funds and private investors have shifted their attention to Rite Aid. Properties tenanted by Rite Aid, still offer the benefits of the pharmacy retailers with an increased yield in comparison to Walgreens and CVS. As Rite Aid stock price has reached its highest point in 14 years, investors’ view the future of Rite Aid favorably as the company’s core business continues to improve. Transaction volume for 2014 should remain active in the drug store sector as investor interest remains high. Drivers of the interest include investor’s familiarity with the tenants, financing availability, residual strength of the real estate and the positive outlook of the fundamentals of the pharmacy business. Above numbers include properties of all lease lengths and types.

- 2. www.bouldergroup.com THE NET LEASE DRUG STORE REPORT Q1 2014 MEDIAN ASKING CAP RATE BY LEASE TERM REMAINING Term Remaining Walgreens CVS Rite Aid 20+ 5.50% 5.50% N/A 15-19 5.65% 5.90% 7.00% 10-14 5.90% 6.08% 7.30% 6-9 6.63% 7.42% 8.50% 5 & Under 7.34% 7.75% 8.75% MEDIAN ASKING CAP RATE BY PROPERTY TYPE Property Type Walgreens CVS Rite Aid Ground Lease 5.10% 5.00% 6.25% Fee Simple 5.60% 5.90% 7.75% Leasehold 6.75% 6.88% 9.08% MEDIAN NATIONAL ASKING VS. CLOSED CAP RATE SPREAD Tenant Asking Closed Spread (bps) Walgreens 6.93% 7.23% 30 CVS 6.63% 6.85% 22 Rite Aid 8.00% 8.78% 78 DRUG STORE VS. RETAIL NET LEASE MARKET CAP RATE Q3 2013 Q1 2014 Tenant (Previous) (Current) Drug Store 6.00% 5.90% Retail Net Lease Market 7.02% 6.75% Drug Store Premium (bps) 102 85

- 3. www.bouldergroup.com THE NET LEASE DRUG STORE REPORT Q1 2014 Walgreens CVS Rite Aid Credit Rating BBB (Stable) BBB+ (Stable) B (Stable) Market Cap $61 billion $85 billion $6 billion Revenue $74 billion $126 billion $25 billion 2014 Stores Planned 150 150 N/A Number of Stores 8,681 7,660 4,595 Typical Lease Term 20 or 25 year primary term with fifty years of options 25 year primary term with six 5-year options 20 year primary term with six 5-year options Typical Rent Increases None None in primary 10% increases in option periods 10% increases every 10 years COMPANY AND LEASE OVERVIEW FOR MORE INFORMATION AUTHOR John Feeney | Research Director john@bouldergroup.com CONTRIBUTORS Randy Blankstein | President rblank@bouldergroup.com Jimmy Goodman | Partner jimmy@bouldergroup.com Zach Wright | Research Analyst zach@bouldergroup.com (Company estimates) © 2014. The Boulder Group. Information herein has been obtained from databases owned and maintained by The Boulder Group as well as third party sources. We have not verified the information and we make no guarantee, warranty or representation about it. This information is provided for general illustrative purposes and not for any specific recommendation or purpose nor under any circumstances shall any of the above information be deemed legal advice or counsel. Reliance on this information is at the risk of the reader and The Boulder Group expressly disclaims any liability arising from the use of such information. This information is designed exclusively for use by The Boulder Group clients and cannot be reproduced, retransmitted or distributed without the express written consent of The Boulder Group.