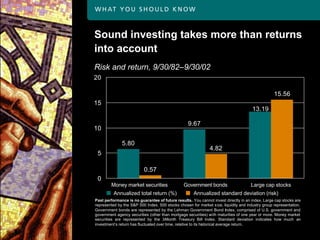

1. Sound investing takes more than returns

into account

Risk and return, 9/30/82–9/30/02

20

15.56

15

13.19

9.67

10

5.80

4.82

5

0.57

0

Money market securities Government bonds Large cap stocks

Annualized total return (%) Annualized standard deviation (risk)

Past performance is no guarantee of future results. You cannot invest directly in an index. Large cap stocks are

represented by the S&P 500 Index, 500 stocks chosen for market size, liquidity and industry group representation.

Government bonds are represented by the Lehman Government Bond Index, comprised of U.S. government and

government agency securities (other than mortgage securities) with maturities of one year or more. Money market

securities are represented by the 3 -Month Treasury Bill Index. Standard deviation indicates how much an

investment’s return has fluctuated over time, relative to its historical average return.

2. A targeted blend captures higher

risk-adjusted returns

High

Same risk,

more return

Efficient

frontier

Expected return

Same return,

less risk

Inefficient (less return,

portfolio more risk)

Low

Risk

Low High

3. Sophisticated strategies incorporate

classes and subclasses

The basics

Stocks: 60%

Bonds: 30%

Cash: 10%

The next level

Large cap U.S. stocks: 30% Investment-grade

corporate bonds: 10%

Small cap U.S. stocks: 10%

High yield bonds: 5%

International stocks: 20%

Cash: 10%

Government bonds: 15%

Asset allocations are for illustrative purposes only and do not constitute a recommendation.

4. Asset allocation has provided protection

in volatile markets

12/31/72–12/31/74

30%

20%

10%

1.22%

0%

-10%

-11.99%

-20%

-20.80%

-30%

Large cap stocks Bonds 60% stocks/40% bonds

5. Know your goals

Goal Ideal time to start investing Key considerations

Retirement When you get your first job • Years until retirement

• Company plans

• Desired lifestyle

in retirement

College When each child is born • Age of child(ren)

education • Public or private college

• Current savings

• Grandparent contributions

New house As soon as you decide you • Size of mortgage

may want to be an owner • Time horizon

Rainy-day When you have some • Potential level of need

fund savings accumulated • Other financial

commitments

Build a legacy As your career progresses • Tax implications

for your heirs • Time horizon

• Number of heirs

6. Make it work

Asset allocation #1: Aggressive

1982–2001

Number of down years 3

Average loss in down years -4.51%

Worst 1-year loss -7.80%

Average annual total return 14.50%

Stocks: 80% Bonds: 20%

7. Make it work

Asset allocation #2: Moderate

1982–2001

Number of down years 2

Average loss in down years -1.04%

Worst 1-year loss -2.06%

Average annual total return 12.79%

Stocks: 50% Bonds: 40% Cash: 10%

8. Make it work

Asset allocation #3: Conservative

1982–2001

Number of down years 0

Average loss in down years N/A

Worst 1-year loss N/A

Average annual total return 10.98%

Stocks: 30% Bonds: 40% Cash: 30%

9. How rebalancing works — an example

Initial allocation: 12/31/99 Ending allocation: 12/31/02

Large cap stocks 35% Large cap stocks 26%

Small cap stocks 25% Small cap stocks 24%

International stocks 15% International stocks 10%

Bonds 25% Bonds 40%