1. Private & Confidential Case Study: Volatility Control Equities 19 August 2013

Case Study: Adopting a risk controlled approach to managing equity allocation

Situation:

• A c£3.5bn closed and mature pension scheme with weak sponsor covenant, facing

a deficit of c£300m on a self sufficiency basis.

• The Scheme relies primarily on returns from investment strategy to fund its deficit in

the absence of significant sponsor contributions.

• The Scheme is therefore highly path dependent and vulnerable to stress events

which could throw it off course from its flight path.

Task:

• To reduce downside risk from equities while maintaining returns required for the

Scheme’s path to full funding.

• Redington recommended for the Scheme to adopt a risk controlled approach to

managing its equity allocation. Under this approach, the Scheme’s equity exposure

is dynamically managed to achieve a target volatility level.

- For example as equity volatility rises, exposure to equities is reduced

towards cash to keep the volatility at the target level

- Historical analysis showed that, across equity markets and time

periods, adopting this approach enables the Scheme to limit draw-downs and

deliver equity-like returns with substantially lower volatility

• A further advantage of managing equity against a target volatility is that it cheapens

the cost of buying explicit downside protection via a “put option” .

- For example, the cost to protect a global equity portfolio against a fall in

value of more than 10% over a one-year period may cost between 3-

4%, however, the same protection for a global, volatility controlled index

costs less than 1%).

Action:

• Following Trustee Training and Board Approval, the Trustees moved the equity

benchmark to a volatility controlled index with a target volatility of 10% and bought a

put option at a strike of 90% on the index.

• Redington also advised on other key parameters of the structure including

implementation vehicle, underlying index and management of currency hedging.

• The structure was executed by the Scheme’s LDI manager with oversight by

Redington as a total return swap with an investment bank.

1

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

0% 5% 10% 15% 20% 25% 30%

ExpectedReturnoverswaps(bps)

VaR95 (% of notional exposure)

Starting Point

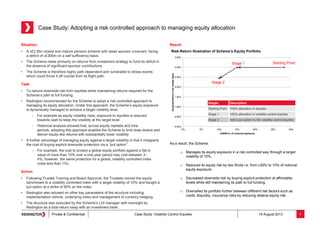

Stages Description

Starting Point 100% allocation in equities

Stage 1 100% allocation in volatility control equities

Stage 2 Add a put option to the volatility control equities

Stage 1

Stage 2

Risk-Return Illustration of Scheme’s Equity Portfolio

As a result, the Scheme:

o Manages its equity exposure in a risk controlled way through a target

volatility of 10%.

o Reduced its equity risk by two thirds i.e. from c30% to 10% of notional

equity exposure.

o Decreased downside risk by buying explicit protection at affordable

levels while still maintaining its path to full funding.

o Diversified its portfolio further between different risk factors such as

credit, illiquidity, insurance risks by reducing relative equity risk.

Result: