Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Ähnlich wie Goldman mnta

Ähnlich wie Goldman mnta (20)

Mehr von James Hilbert

Mehr von James Hilbert (20)

Goldman mnta

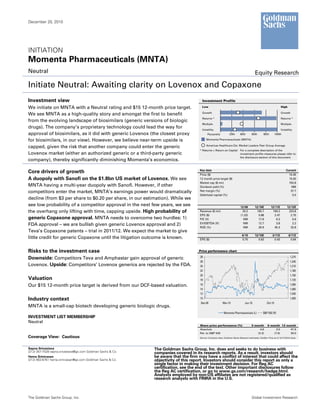

- 1. December 20, 2010 INITIATION Momenta Pharmaceuticals (MNTA) Neutral Equity Research Initiate Neutral: Awaiting clarity on Lovenox and Copaxone Investment view Investment Profile We initiate on MNTA with a Neutral rating and $15 12-month price target. Low High Growth Growth We see MNTA as a high-quality story and amongst the first to benefit Returns * Returns * from the evolving landscape of biosimilars (generic versions of biologic Multiple Multiple drugs). The company’s proprietary technology could lead the way for Volatility Volatility approval of biosimilars, as it did with generic Lovenox (the closest proxy Percentile 20th 40th 60th 80th 100th for biosimilars, in our view). However, we believe near-term upside is Momenta Pharmaceuticals (MNTA) Americas Healthcare Est. Market Leaders Peer Group Average capped, given the risk that another company could enter the generic * Returns = Return on Capital For a complete description of the Lovenox market (either an authorized generic or a third-party generic investment profile measures please refer to the disclosure section of this document. company), thereby significantly diminishing Momenta’s economics. Key data Current Core drivers of growth Price ($) 15.45 A duopoly with Sanofi on the $1.8bn US market of Lovenox. We see 12 month price target ($) 15.00 Market cap ($ mn) 702.8 MNTA having a multi-year duopoly with Sanofi. However, if other Dividend yield (%) NM competitors enter the market, MNTA’s earnings power would dramatically Net margin (%) 37.7 Debt/total capital (%) 0.0 decline (from $3 per share to $0.20 per share, in our estimation). While we see low probability of a competitor approval in the next few years, we see 12/09 12/10E 12/11E 12/12E the overhang only lifting with time, capping upside. High probability of Revenue ($ mn) 20.2 105.7 194.2 223.8 EPS ($) (1.33) 0.88 2.47 2.75 generic Copaxone approval. MNTA needs to overcome two hurdles: 1) P/E (X) NM 17.6 6.3 5.6 EV/EBITDA (X) NM 12.7 3.8 2.2 FDA approval – we are bullish given generic Lovenox approval and 2) ROE (%) NM 26.9 45.3 32.8 Teva’s Copaxone patents – trial in 2011/12. We expect the market to give 9/10 12/10E 3/11E 6/11E little credit for generic Copaxone until the litigation outcome is known. EPS ($) 0.75 0.63 0.43 0.64 Risks to the investment case Price performance chart 28 1,270 Downside: Competitors Teva and Amphastar gain approval of generic 26 1,240 Lovenox. Upside: Competitors’ Lovenox generics are rejected by the FDA. 24 1,210 22 1,180 20 1,150 Valuation 18 1,120 Our $15 12-month price target is derived from our DCF-based valuation. 16 1,090 14 1,060 12 1,030 Industry context 10 1,000 Dec-09 Mar-10 Jun-10 Oct-10 MNTA is a small-cap biotech developing generic biologic drugs. Momenta Pharmaceuticals (L) S&P 500 (R) INVESTMENT LIST MEMBERSHIP Neutral Share price performance (%) 3 month 6 month 12 month Absolute 4.6 3.0 47.6 Rel. to S&P 500 (5.3) (7.6) 30.0 Coverage View: Cautious Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 12/17/2010 close. Sapna Srivastava The Goldman Sachs Group, Inc. does and seeks to do business with (212) 357-7528 sapna.srivastava@gs.com Goldman Sachs & Co. companies covered in its research reports. As a result, investors should Hema Srinivasan be aware that the firm may have a conflict of interest that could affect the (212) 902-6761 hema.srinivasan@gs.com Goldman Sachs & Co. objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the end of the text. Other important disclosures follow the Reg AC certification, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. The Goldman Sachs Group, Inc. Global Investment Research

- 2. December 20, 2010 Momenta Pharmaceuticals (MNTA) Momenta Pharmaceuticals: Summary Financials Profit model ($ mn) 12/09 12/10E 12/11E 12/12E Balance sheet ($ mn) 12/09 12/10E 12/11E 12/12E Total revenue 20.2 105.7 194.2 223.8 Cash & equivalents 21.9 127.2 258.7 409.1 Cost of goods sold -- -- -- -- Accounts receivable 0.0 39.5 48.1 52.9 SG&A (17.4) (20.0) (20.3) (20.5) Inventory 0.0 0.0 0.0 0.0 R&D (56.2) (45.7) (47.6) (49.9) Other current assets 80.2 40.2 43.0 43.9 Other operating profit/(expense) 0.0 0.0 0.0 0.0 Total current assets 102.1 206.9 349.8 506.0 ESO expense -- -- -- -- Net PP&E 11.8 9.3 9.4 9.7 EBITDA (48.9) 44.3 129.1 156.3 Net intangibles 2.8 2.5 2.2 1.9 Depreciation & amortization (4.5) (4.3) (2.8) (3.0) Total investments 0.0 0.0 0.0 0.0 EBIT (53.4) 40.0 126.3 153.3 Other long-term assets 1.8 1.8 1.8 1.8 Net interest income/(expense) 0.3 (0.1) 0.4 0.7 Total assets 118.5 220.4 363.1 519.4 Income/(loss) from associates 0.0 0.0 0.0 0.0 Others (0.1) 0.0 0.0 0.0 Accounts payable 4.2 3.0 5.5 6.3 Pretax profits (53.3) 39.9 126.7 154.0 Short-term debt 0.0 0.0 0.0 0.0 Provision for taxes 0.0 0.0 (2.8) (15.4) Other current liabilities 12.1 11.3 11.3 11.3 Minority interest 0.0 0.0 0.0 0.0 Total current liabilities 16.3 14.3 16.8 17.6 Net income pre-preferred dividends (53.3) 39.9 123.9 138.6 Long-term debt 0.0 0.0 0.0 0.0 Preferred dividends 0.0 0.0 0.0 0.0 Other long-term liabilities 7.9 3.8 1.7 0.1 Net income (pre-exceptionals) (53.3) 39.9 123.9 138.6 Total long-term liabilities 7.9 3.8 1.7 0.1 Post tax exceptionals (10.8) (10.7) (7.9) (8.9) Total liabilities 24.3 18.1 18.5 17.8 Net income (post-exceptionals) (64.0) 29.2 115.9 129.7 Preferred shares 0.0 0.0 0.0 0.0 EPS (basic, pre-except) ($) (1.33) 0.89 2.54 2.83 Total common equity 94.2 202.3 344.6 501.6 EPS (diluted, pre-except) ($) (1.33) 0.88 2.47 2.75 Minority interest 0.0 0.0 0.0 0.0 EPS (basic, post-except) ($) (1.60) 0.65 2.38 2.65 EPS (diluted, post-except) ($) (1.60) 0.64 2.31 2.58 Total liabilities & equity 118.5 220.4 363.1 519.4 Common dividends paid -- -- -- -- DPS ($) 0.00 0.00 0.00 0.00 Dividend payout ratio (%) 0.0 0.0 0.0 0.0 Additional financials 12/09 12/10E 12/11E 12/12E Net debt/equity (%) (23.3) (62.9) (75.1) (81.6) Interest cover (X) (93.7) 131.5 829.2 1,006.3 Growth & margins (%) 12/09 12/10E 12/11E 12/12E Inventory days NM NM NM NM Sales growth 39.0 422.1 83.7 15.2 Receivable days 4.1 68.2 82.3 82.4 EBITDA growth 6.1 190.6 191.2 21.1 BVPS ($) 2.35 4.45 6.86 9.97 EBIT growth 4.8 174.9 215.9 21.4 Net income (pre-except) growth 0.3 174.9 210.6 11.9 ROA (%) (42.5) 23.5 42.5 31.4 EPS growth 10.5 167.2 184.0 11.6 CROCI (%) (60.4) 47.4 123.1 125.5 Gross margin NM NM NM NM EBITDA margin (241.7) 41.9 66.5 69.9 Dupont ROE (%) (56.6) 19.7 35.9 27.6 EBIT margin (263.8) 37.8 65.0 68.5 Margin (%) (263.0) 37.7 63.8 61.9 Turnover (X) 0.2 0.5 0.5 0.4 Cash flow statement ($ mn) 12/09 12/10E 12/11E 12/12E Leverage (X) 1.3 1.1 1.1 1.0 Net income (53.3) 39.9 123.9 138.6 D&A add-back (incl. ESO) 4.5 4.3 2.8 3.0 Free cash flow per share ($) (1.42) 0.02 2.32 2.70 Minority interest add-back 0.0 0.0 0.0 0.0 Free cash flow yield (%) (13.7) 0.1 15.0 17.5 Net (inc)/dec working capital (6.9) (42.4) (11.0) (6.5) Other operating cash flow 0.4 1.0 0.3 0.3 Cash flow from operations (55.3) 2.8 116.0 135.4 Capital expenditures (1.7) (1.8) (2.9) (3.4) Acquisitions 0.0 0.0 0.0 0.0 Divestitures 0.0 0.0 0.0 0.0 Others (20.6) 38.0 0.0 0.0 Cash flow from investing (22.3) 36.2 (2.9) (3.4) Dividends paid (common & pref) 0.0 0.0 0.0 0.0 Inc/(dec) in debt 0.0 0.0 0.0 0.0 Other financing cash flows 44.4 66.2 18.4 18.4 Cash flow from financing 44.4 66.2 18.4 18.4 Total cash flow (33.1) 105.2 131.5 150.5 Note: Last actual year may include reported and estimated data. Source: Company data, Goldman Sachs Research estimates. Analyst Contributors Sapna Srivastava sapna.srivastava@gs.com Hema Srinivasan hema.srinivasan@gs.com Goldman Sachs Global Investment Research 2

- 3. December 20, 2010 Momenta Pharmaceuticals (MNTA) Key investment themes Momenta was founded in 2001 based on technology characterizing complex mixtures developed at Massachusetts Institute of Technology. This proprietary technology allowed the company to be amongst the first to benefit from the evolving landscape of biosimilars. The technology is capable of characterizing complex biologic aspects of certain drugs to establish “sameness,” a key regulatory hurdle for approval of biosimilar drugs. Novartis’ generic drug unit Sandoz first partnered with Momenta in 2003 and has rights to M- enoxaparin (generic Lovenox), M356 (generic Copaxone), and several unnamed product candidates. We saw the first proof-of-principle for this technology with the approval of Momenta/Novartis’ generic Lovenox in July 2010. We see Lovenox, a complex mixture of sugars derived from pig intestines, as a good proxy for the potential approval process of biosimilar drugs. The key question was how to establish “sameness” for generic Lovenox, as most current technologies are inadequate due to their inability to thoroughly characterize sugars. We believe Momenta’s technology was capable of answering this question and was the key reason why Momenta was the first company to gain approval for generic Lovenox, even though it filed its ANDA over two years after competitors, Teva and Amphastar. The key question for Momenta now is whether other companies can gain approval of generic Lovenox. The answer will define: (1) what value to ascribe to the generic Lovenox opportunity, as different outcomes lead to significantly different economics for Momenta, and (2) what value to assign to Momenta’s proprietary technology, contingent on whether the tool can confer years of duopoly economics in other key biologic markets (like Teva’s Copaxone) or could be easily duplicated by other generic companies. Although we see Momenta’s technology creating a multi-year duopoly with Sanofi on Lovenox and eventually with Teva on Copaxone, we are Neutral on the stock. Given that there is no clarity on how the competitive process will evolve, we expect limited credit from the Street until a substantial amount of time passes without Teva (considered the most formidable competitor on generic Lovenox) gaining approval on its application for generic Lovenox. Separately, Momenta sued Teva on 12/2/2010 for infringing its patents covering innovative methods of producing Lovenox, the outcome of which could be defining, but is also likely several years away. Valuation: Though Momenta turned profitable last quarter, there is significant risk that Teva or another third party could launch a generic version of Lovenox, thereby diminishing Momenta’s economics from a 45% profit share to a high single digit royalty on sales, according to the contract with Novartis. In this scenario (assuming market dynamics are constant), we estimate the ultimate Lovenox earnings power would decline from $3 per share to $0.20 per share. In our view, this risk can be reflected in our DCF-based valuation in two ways: (1) by forecasting a single-generic market for the foreseeable future and applying a large discount rate (25-30%) to reflect the inherent risk or (2) by forecasting a third-party generic launch within the next year and applying a 10-15% discount rate. Based on our thesis that other companies will be unable to gain approvals of generic Lovenox in the near-term (as they lack Momenta’s proprietary technology), we model a duopoly (single-generic) market and assign a 30% discount rate to arrive at our $15 12-month, DCF-based price target. Our 2010-2012E EPS estimates are $0.88, $2.47, and $2.75, with growth driven by increasing enoxaparin utilization and market share expansion for Momenta’s M- enoxaparin vs. branded Lovenox. Goldman Sachs Global Investment Research 3

- 4. December 20, 2010 Momenta Pharmaceuticals (MNTA) Lovenox: We see a duopoly but competitive threat limits upside We believe Momenta/Novartis’s generic Lovenox will be the only generic version approved for the next several years, potentially capturing up to 55% of the $1.8bn and growing US market (achievable share is constrained by manufacturing capacity, with current supply allowing for 35-40% share of the Lovenox market). We see Momenta’s proprietary technology as unique in its ability to demonstrate that its generic version of Lovenox is the same as branded Lovenox, a key regulatory hurdle that we do not see competitors Teva and Amphastar overcoming. A duopoly (in this case a single-generic market) allows Momenta to achieve $3 per share in peak earnings power, in our estimate. We believe investors are concerned that competitors could enter the market shortly (Teva has said by YE2010), which would almost completely diminish the economics for Momenta (under contract with Novartis). While we do not see that as a likely scenario, we see no way for this overhang to lift until substantial time elapses, likely an additional six to twelve months, without competitor approvals. In the interim, we expect the stock to remain largely range-bound. Background See Appendix for Lovenox (enoxaparin) is a low molecular weight heparin that is derived from pig more on generic drug intestines. It is an anticoagulant used to prevent blood clots in a wide range of patients approval process (including those on bed rest, those having hip/knee replacements or stomach surgery, and patients post-angina or heart attack). Lovenox is rare in that it is a biologic drug that, like the growth hormones, was approved under a new drug application (NDA), as the biologic licensing application (BLA) regulatory path was not yet formed. Hence, there was a pathway for generics to apply for approval. A similar path is not yet available for drugs that are approved on the basis of a BLA. Since the first ANDA filing for Lovenox in 2003 (and Momenta’s filing in 2005), the approval process for generic Lovenox has been closely watched as reflective of what the FDA will do with biosimilars. Approval of generic Lovenox reflected on the key question for biosimilar drugs: how to establish “sameness” with drugs that themselves are not fully characterized. It took the FDA seven years to get comfortable with the key issues and approve the first generic Lovenox, Momenta and Novartis’s M-enoxaparin, in July 2010. We note that the FDA approved the drug shortly after healthcare reform legislation (in March 2010) gave the FDA the onus for developing a biosimilar pathway. Exhibit 1: Timeline of events leading to Momenta’s generic Lovenox approval March 2003: Teva & August 2005: Momenta March 2010: Amphastar submit files ANDA for generic Healthcare reform bill paragraph IV ANDA Lovenox (later added passed with biosimilar filings for enoxaparin paragraph IV certification) provisions included ????: FDA resolution of Teva and August 2003: May 2008: Final court verdict Amphastar's July 2010: FDA Aventis sues Teva invalidates Sanofi's '618 application approves and Amphastar for patent on grounds of Momenta/Novartis' patent infringement inequitable conduct generic Lovenox 2003 2004 2005 2006 2007 2008 2009 2010 2011 Source: Company data, Goldman Sachs Research Goldman Sachs Global Investment Research 4

- 5. December 20, 2010 Momenta Pharmaceuticals (MNTA) We see a multi-year duopoly based on proprietary technology Duopoly is important, as economics change significantly with more competitors Under Momenta’s contract with Novartis, there are three competitive scenarios that carry different economics for Momenta. Continuation of the current market dynamics, in which MNTA has the only approved generic, holds the best economics for the company (45% profit share). In the event that Sanofi launches an authorized generic, Momenta would receive a royalty on sales up to a certain threshold, and a profit share thereafter, according to the contract. While exact economics have not been disclosed, we estimate Momenta would receive a 10% royalty up to $1bn in sales and a 30% profit share thereafter. In the final scenario, if third-parties launch generic versions of Lovenox, Momenta would only receive a high single-digit royalty on sales (we estimate 8%) of a potentially smaller market, as generic pricing generally deteriorates with multiple competitors. Exhibit 2: Our estimate of Momenta’s economics in various competitive scenarios Competitive scenario Royalty rate Profit share 1) MNTA is sole approved generic N/A 45% 2) Sanofi launches an authorized generic 10% up to $1bn 30% over $1bn 3) Third party generics launch (Teva, Amphastar, Hospira) 8% N/A Source: Company data, Goldman Sachs Research estimates. See Appendix for We see MNTA’s proprietary technology as the basis of approval more on MNTA’s Momenta’s technology, exclusively in-licensed from Massachusetts Institute of technology Technology, enables it to sequence complex mixtures. This technology has been shown to sequence complex sugars (published in leading journals Science and Nature), and we believe it can be extended to other complex mixtures as well. To our knowledge, no other technology can so thoroughly characterize sugars, making Momenta unique in its ability to fully characterize Lovenox (a mixture of polysaccharides, also known as sugar chains) to demonstrate sameness. We believe that competitors do not have this technology and will therefore be unable to gain approval for the next several years. Moreover, Momenta recently sued Teva for infringement of two patents covering the company’s proprietary methods of producing enoxaparin. If Teva is found to infringe these patents, we believe it is less likely that Teva will be able to demonstrate the interchangeability of its generic version with branded Lovenox. Citizen petitions (CP) (1) FDA’s citizen petition response – Momenta’s technology was key to approval allow citizens to raise In its response to the Aventis citizen petition (CP) upon approval of M-enoxaparin, the issues relating to FDA laid out five criteria used to evaluate active ingredient sameness to enoxaparin: “(1) products that the FDA the physical and chemical characteristics of enoxaparin, (2) the nature of the source regulates. material and the method used to break up the polysaccharide chains into smaller fragments, (3) the nature and arrangement of components that constitute enoxaparin, (4) The FDA cannot approve a drug certain laboratory measurements of anticoagulant activity, and (5) certain aspects of the without resolving any drug’s effect in humans.” outstanding CPs We believe Momenta’s proprietary technology was instrumental in helping it address blocking approval. these criteria. For example, Momenta is able to sequence complex sugars, allowing it to specifically address criterion (3), which requires a generic Lovenox to demonstrate “equivalence in disaccharide building blocks, fragment mapping, and sequence of oligosaccharide species.” The technology Momenta in-licensed from MIT has been shown as the first to sequence complex sugar chains longer than 10 saccharide units (Lovenox is a combination of sugars that range between 2 and 32 sugar units), and the FDA response to the Lovenox CP references the original publications of this technology multiple times. Goldman Sachs Global Investment Research 5

- 6. December 20, 2010 Momenta Pharmaceuticals (MNTA) Moreover, Momenta’s ability to identify and link specific sugar structures with their corresponding biological function (the technology was validated by being used to identify the key contaminant of source material during the heparin contamination crisis) could also uniquely addresses the different criteria, an edge which we believe competitors lack. (2) FDA also relied on Momenta’s technology during the heparin crisis The FDA used Momenta’s technology in 2007-2008 when the heparin crisis broke out. Contamination of heparin, the source product for Lovenox, was responsible for 247 deaths. The source material is generally manufactured in China. At that time, there was significant debate over whether it was contamination of source material or processing in the US that was responsible for these deaths. The FDA partially relied on Momenta’s technology to discover the source of contamination and co-authored a paper with Momenta demonstrating the power of the company’s assays in detecting the key contaminant causing the severe reactions and deaths that were observed in late 2007/early 2008. In the publications, Momenta’s technology was used to demonstrate the mechanism by which the key contaminant (oversulfated chondroitin sulfate) generated adverse reactions in humans and to elucidate which assays could be used to test the global supply of heparin. (3) FDA approved Momenta’s application significantly faster than competitors Although Teva and Amphastar filed their ANDAs almost two years before Momenta did, their generic versions have not yet been approved. It has been about 4.5 months since Momenta’s product was approved. We believe this is a clear reflection of the higher quality application that Momenta/Novartis had versus competitors. While Amphastar has been mired in Chinese heparin supplier issues, Teva management has always said that they believe themselves to be similarly situated to Momenta. Nevertheless, there was no mention of the status of the Teva or Amphastar ANDAs in the FDA documents released upon approval of M-enoxaparin in July, 2010. As of its 3Q conference call, Teva management continued to remain optimistic that they would receive approval for their generic Lovenox by year-end. Still, we have heard no indication of this from the FDA. We also note that both Momenta and Teva expected approval for years before the FDA took any action on either ANDA or Sanofi’s citizen petition. However, we see limited upside until time removes the competitive overhang We believe that for Momenta to receive full credit, investors need to be convinced that: (1) Sanofi will not launch an authorized generic, and (2) competitors Teva and Amphastar will not receive FDA approval. While Sanofi can launch an authorized generic at anytime, it may not make sense to do so in the absence of other generic approvals. An authorized generic is generally priced in line with other generics – at around a 15-20% discount to the branded drug in the case of Lovenox. Therefore, if Sanofi can retain reasonable market share of branded Lovenox at the full price, it would not have a strong incentive to launch an authorized generic and reduce its average price per Lovenox prescription. From what we understand, it is rare for the FDA to give a non-approvable letter to generic applications, making time the only way to gauge the approvability of Teva’s and Amphastar’s applications. We believe a lack of competitor approvals in the next 6-12 months is necessary for the Street to gain confidence that Momenta’s generic Lovenox could have a duopoly for the foreseeable future. Until then, we see the overhang as limiting upside. Goldman Sachs Global Investment Research 6

- 7. December 20, 2010 Momenta Pharmaceuticals (MNTA) Copaxone: Positive on FDA approval, but could be a while away We believe the probability is high that Momenta (again partnered with Novartis) receive FDA approval of M356, its generic version of Teva’s Copaxone. The key reasons for our positive outlook are: (1) the FDA’s rejection of Teva’s citizen petition (CP), which sought to prevent any approvals of generic Copaxone (received 180 days after filing versus 7 years in the case of the Lovenox CP), (2) Momenta’s proprietary complex mixture sequencing technology, which we see as the basis for approval of generic Lovenox, and (3) the FDA’s increasing willingness to approve interchangeable versions of complex biologics; generic Lovenox can be see as the first. However, the ongoing litigation of Teva’s 2014 patents is a key gating factor. The trial is expected to start in 2011-2012. Background Momenta is seeking FDA approval for a generic equivalent of Teva’s branded multiple sclerosis (MS) drug Copaxone ($2.2 bn in estimated 2010 US sales). Momenta filed its Copaxone ANDA with a paragraph IV certification on July 11, 2008 and notified Teva in a letter received on July 14, 2008, dating the 30-month stay expiration (the earliest possible approval date) December 13, 2010. Teva filed suit against Sandoz and Momenta on August 28, 2008. In order to launch, Momenta and Sandoz must receive FDA approval for M356 (the generic version of Copaxone) and must not infringe any Orange Book-listed patents, which extend to 2014. Momenta has to show that either the patents are not infringed or are unenforceable due to inequitable conduct. The trial is expected to begin in the 2011- 2012 timeframe. We believe a tentative FDA approval is very unlikely before the litigation outcome is known, as the agency has little incentive to act on applications that are not actionable. Exhibit 3: Timeline of key events related to generic Copaxone January 2011: MYL August 2008: Teva files October 2010: MNTA May 2014: Copaxone claims construction patent infringement suit and Mylan cases are Orange Book patents hearing; Teva's low-dose against Sandoz/MNTA consolidated expire Copaxone PDUFA July 2008: Momenta September 2009: December 2010: MNTA's 2011/12?: November 2014: Copaxone and Sandoz submit Mylan submits 30-month stay on MNTA/MYL case patent expiration if PED paragraph IV ANDA paragraph IV ANDA approval expires (at-risk potentially exclusivity is granted filing for Copaxone filing for Copaxone launches possible) proceeds to trial 2008 2009 2010 2011 2012 2013 2014 2015 Source: Company data, FDA’s Orange Book, Goldman Sachs Research We see FDA approval as likely, given Lovenox precedent (1) FDA rejected Teva’s citizen petition on Copaxone The FDA took 7 years to render a final decision on the Aventis’ Lovenox CP (releasing its decision concurrent with final approval of M-enoxaparin). In contrast, the FDA resolved Teva’s CP within 180 days of filing. We believe that this shows the FDA may now have more clarity on what it takes to approve complex mixture drugs like Lovenox and Copaxone. We highlight the noteworthy points from the FDA’s response that we see as positive for Momenta, which are very similar to the points the FDA made in its rationale for the approval of generic Lovenox. Goldman Sachs Global Investment Research 7

- 8. December 20, 2010 Momenta Pharmaceuticals (MNTA) The FDA rejected the idea that the absence of pharmacodynamic markers (PD markers, measures of what a drug does in the body) for Copaxone precludes establishing “sameness.” Moreover, the FDA specifically notes, “given the complexity of Copaxone, we may require that any ANDA sponsor demonstrate active ingredient sameness through a multi-criteria test or series of tests, each criterion of which captures different aspects of the active ingredient’s ‘sameness’.” The FDA specifically asserts that sameness does not necessitate a finding of “complete chemical identity.” (2) Generic Lovenox approval gives us confidence in Momenta’s technology Generic drug approvals are driven by establishing “sameness” of active ingredients and bioequivalence. We note that using these criteria, Momenta was much better positioned for approval of generic Lovenox than it is for Copaxone. The publications on Momenta’s technology focus on characterizing sugars, and Lovenox is a sugar while Copaxone is a polypeptide (though most peptide characterization work was done after the company was founded and began actively protecting its trade secrets). Lovenox also has a clear PD marker to establish bioequivalence. Copaxone is a synthetic polypeptide with no PD markers. However, the generic Lovenox approval elucidated the process that the FDA defined to establish “sameness” of active ingredients. It was a five-step process, which heavily relied on technology, placing limited weight on PD markers. Our analysis shows that Momenta’s technology can be extended to sequence complex mixtures like Copaxone, and the FDA’s response to Teva’s CP shows that the absence of a PD marker is not an insurmountable hurdle. (3) Generic Lovenox decision shows that the FDA is willing to be bold In our view, the approval of generic Lovenox signaled that the FDA may be willing to move forward with biosimilars more aggressively than previously thought. The FDA approved generic Lovenox without clinical trials, knowing that it would be fully substitutable with branded Lovenox in complex and even life-threatening indications. Combined with the rejection of Teva’s CP on Copaxone within 180 days, we believe this indicates the FDA’s willingness to move forward with biosimilars, and generic Copaxone is the next application in line. We also note that the recent passage of biosimilar provisions within broader healthcare reform gives the FDA the onus for developing biogeneric pathways. We note that the FDA approved generic Lovenox shortly following passage of health reform legislation. In our view, a decision of this magnitude likely had the backing of multiple authorities, particularly as the contamination of heparin (the source product for Lovenox) was responsible for 247 deaths in 2007/08, placing generic Lovenox in the center of a high- profile safety issue for the agency. We believe this demonstrates that regulatory authorities are willing to take an aggressive stance on follow-on biologics, which we view as a negative for branded Copaxone. Trial outcome is tough to gauge – many risks to success remain (1) Trial timelines are extended – Decision could come as late as 2012 Momenta’s patent litigation case on Copaxone has been consolidated with Mylan’s. While Momenta’s case has gone through several required steps including claims construction and summary judgment (September 2010), Mylan has yet to complete the process. Its summary judgment hearing is scheduled for January 2011. As a result, the trial that was originally expected to start in January 2011 will be delayed. Momenta management believes that the trial could start as early as 1Q2011 and finish by 3Q2011, with a final District Court judgment within 4 months (around YE2011 or 1Q2012). Teva management indicated on its 3Q earnings call that consolidation with Mylan could push the start of the trial to 2012. Goldman Sachs Global Investment Research 8

- 9. December 20, 2010 Momenta Pharmaceuticals (MNTA) Depending on the duration of the trial and the time Judge Jones requires to render a decision, this could push an outcome out to 2012 or 2013. In the interim, we see little room for Momenta to receive credit for the generic Copaxone opportunity. However, we note that if Momenta’s projections are correct, a District Court judgment could come by 2012, followed by the appeals case. We note that if Momenta/Sandoz were successful in the District Court case, they could decide to launch at-risk (contingent on FDA approval of M356), as the 30-month stay expired in December 2010. (2) Hard to assess the strength of the Momenta/Mylan case In the summary judgment, the District Court denied Momenta’s motion that the Copaxone patents are invalid for indefiniteness (a patent claim must be definite to be valid, i.e., a person of ordinary skill in the art must be able to determine whether a specific device or method is covered by the claim or not). This was largely expected, as summary judgments are most often rendered in clear-cut cases and not in such complex cases. We expect Momenta to continue to make its case on invalidity on the basis of indefiniteness. However, we are unable to gain further clarity on the strength of Momenta’s case. We note that there is a clear risk that the Momenta/Mylan defense could now rely more heavily on inequitable conduct. This will pose a high hurdle for generics, as it requires proving that Teva (1) failed to disclose material information and (2) intended to deceive the USPTO. However, we also note that the Lovenox patent trial was won on inequitable conduct, so a victory for the generic companies would not be unprecedented. Teva’s life cycle management strategy could be successful We believe this risk is worth highlighting, as Teva is working on several extensions of its Copaxone franchise, including several new formulations and devices. The most advanced program is the new 20mg/0.5mL low-volume injection (the marketed product has a concentration of 20mg/1mL), with a PDUFA date of 1/1/2011. If Teva gains approval for this product and FDA determines it is not therapeutically equivalent to the existing product, the FDA can grant Teva 3-year data exclusivity. If Teva acquires this exclusivity AND is successful in converting the MS market to this new formulation, then even if Momenta gains approval of its generic Copaxone, it may not be commercially meaningful. In this scenario, Momenta may need to file a separate ANDA on the new formulation and wait out the 3-year exclusivity before potentially launching a generic version of the new formulation. Other key risks: (1) Momenta is unable to find a reliable biomarker for pharmacodynamics, the complexity of which is addressed in Teva’s Copaxone CP; (2) Momenta is unsuccessful in trial, likely postponing any FDA decision until at least 2014; (3) Other generic competitors can enter the Copaxone market (Mylan has already filed its ANDA, and other companies like Hospira could do the same); (4) Copaxone market share (and sales potential) could erode over time due to the advent of oral therapies like Gilenya in the multiple sclerosis market. Appendix Generic drug approval process ANDA filing: The approval process requires that a generic company file an abbreviated new drug application (ANDA) demonstrating the generic product’s substitutability with the reference (or branded) product. Paragraph IV certification: Concurrent with the ANDA filing, the generic company must certify against the patents listed in the Orange Book. A Paragraph III certification seeks Goldman Sachs Global Investment Research 9

- 10. December 20, 2010 Momenta Pharmaceuticals (MNTA) FDA approval of the generic version after the last patent expires, while a Paragraph IV certification states that the generic version does not infringe on the patents or that the patents are unenforceable. Notification of ANDA filing: After filing an ANDA, the generic company must notify the branded manufacturer within 20 days. Upon receipt of the letter, two events are triggered: (1) the branded company has 45 days to initiate a patent infringement suit against the generic company, and (2) the FDA cannot approve the ANDA for 30 months unless the generic company wins the suit. The first generic company to file an ANDA also receives 180 days of marketing exclusivity upon approval (with a few exceptions). Patent infringement suit: The patent infringement suit starts in the District Court. If the District Court ruling is positive, generic companies will sometimes request that the FDA grant them final approval of their drug to launch “at-risk.” This term reflects the fact that if the generic company loses on appeal, it will likely have to pull its drug from the market and pay the branded company significant damages. Appeals Court decision: After the District Court ruling, the case will proceed to the Appellate Court, which renders a final decision on the case. At this time, if the ruling is in favor of the generic company, it is free to launch (as long as it is first to file or the first filer’s exclusivity has expired). If the ruling is in favor of the branded company, the generic company will have to wait until all patents expire to launch its version of the drug. Exhibit 4: Generic drug approval process flowchart In favor of generic co. Generic company can launch upon FDA approval Generic company Branded company Appeals court makes District court makes Paragraph IV notifies branded co. has 45 days to file a final decision on decision on patent certification within 20 days of patent infringment patent infringement infringement case filing suit against generic case Generic company can launch only Triggers 180‐day Triggers 30‐ Generic company can request Generic company In favor of branded co. after patents exclusivity for month stay on FDA approval to launch at‐risk files ANDA with the expire first filer ANDA approval FDA Generic company FDA makes final Paragraph III waits until all Orange approval decision certification Book listed patents upon patent expiry expire Source: Company data, FDA.gov, Goldman Sachs Research Key features of Momenta’s technology (1) Fast and accurate sequencing – Momenta’s technology enables rapid sequencing of complex sugars with 6 to 8 sugar units and can sequence sugar chains longer than 10 saccharide units, which had never been done before. The technology also allows for sequencing of linear and branched sugars that had previously never been characterized. (2) Sensitive analytical techniques – Momenta has developed techniques to analyze small quantities of biological samples to identify and link sugar structures with corresponding biological functions. (3) Comprehensive analysis of molecules – Momenta’s technology can identify detailed sequences and complete chemical structures of complex sugars, not just the underlying backbone of the sugar chain. Many components of this technology are protected by Momenta’s intellectual property estate. In particular, Momenta has numerous patents covering its chain mapping technology as well as identity patents on enoxaparin and other compounds. While these Goldman Sachs Global Investment Research 10

- 11. December 20, 2010 Momenta Pharmaceuticals (MNTA) patents likely pertain mostly to the sequencing of complex sugars (particularly Lovenox), Momenta likely also has patents on its polypeptide sequencing technology (applicable to Copaxone), but there is very little information in the public realm, as these discoveries occurred after Momenta was founded and began actively protecting its trade secrets. Goldman Sachs Global Investment Research 11

- 12. December 20, 2010 Momenta Pharmaceuticals (MNTA) Reg AC We, Sapna Srivastava and Hema Srinivasan, hereby certify that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Investment Profile The Goldman Sachs Investment Profile provides investment context for a security by comparing key attributes of that security to its peer group and market. The four key attributes depicted are: growth, returns, multiple and volatility. Growth, returns and multiple are indexed based on composites of several methodologies to determine the stocks percentile ranking within the region's coverage universe. The precise calculation of each metric may vary depending on the fiscal year, industry and region but the standard approach is as follows: Growth is a composite of next year's estimate over current year's estimate, e.g. EPS, EBITDA, Revenue. Return is a year one prospective aggregate of various return on capital measures, e.g. CROCI, ROACE, and ROE. Multiple is a composite of one-year forward valuation ratios, e.g. P/E, dividend yield, EV/FCF, EV/EBITDA, EV/DACF, Price/Book. Volatility is measured as trailing twelve-month volatility adjusted for dividends. Quantum Quantum is Goldman Sachs' proprietary database providing access to detailed financial statement histories, forecasts and ratios. It can be used for in-depth analysis of a single company, or to make comparisons between companies in different sectors and markets. Disclosures Coverage group(s) of stocks by primary analyst(s) Sapna Srivastava: America-Biotechnology US. America-Biotechnology US: Alexion Pharmaceuticals, Inc., Amgen Inc., Biogen Idec, Inc., Celgene Corp., Gilead Sciences Inc., Momenta Pharmaceuticals. Company-specific regulatory disclosures The following disclosures relate to relationships between The Goldman Sachs Group, Inc. (with its affiliates, "Goldman Sachs") and companies covered by the Global Investment Research Division of Goldman Sachs and referred to in this research. Goldman Sachs expects to receive or intends to seek compensation for investment banking services in the next 3 months: Momenta Pharmaceuticals ($15.45) Goldman Sachs makes a market in the securities or derivatives thereof: Momenta Pharmaceuticals ($15.45) Goldman Sachs is a specialist in the relevant securities and will at any given time have an inventory position, "long" or "short," and may be on the opposite side of orders executed on the relevant exchange: Momenta Pharmaceuticals ($15.45) Distribution of ratings/investment banking relationships Goldman Sachs Investment Research global coverage universe Rating Distribution Investment Banking Relationships Buy Hold Sell Buy Hold Sell Global 30% 54% 16% 50% 43% 37% As of October 1, 2010, Goldman Sachs Global Investment Research had investment ratings on 2,845 equity securities. Goldman Sachs assigns stocks as Buys and Sells on various regional Investment Lists; stocks not so assigned are deemed Neutral. Such assignments equate to Buy, Hold and Sell for the purposes of the above disclosure required by NASD/NYSE rules. See 'Ratings, Coverage groups and views and related definitions' below. Regulatory disclosures Disclosures required by United States laws and regulations See company-specific regulatory disclosures above for any of the following disclosures required as to companies referred to in this report: manager or co-manager in a pending transaction; 1% or other ownership; compensation for certain services; types of client relationships; managed/co- managed public offerings in prior periods; directorships; for equity securities, market making and/or specialist role. Goldman Sachs usually makes a market in fixed income securities of issuers discussed in this report and usually deals as a principal in these securities. The following are additional required disclosures: Ownership and material conflicts of interest: Goldman Sachs policy prohibits its analysts, professionals reporting to analysts and members of their households from owning securities of any company in the analyst's area of coverage. Goldman Sachs Global Investment Research 12

- 13. December 20, 2010 Momenta Pharmaceuticals (MNTA) Analyst compensation: Analysts are paid in part based on the profitability of Goldman Sachs, which includes investment banking revenues. Analyst as officer or director: Goldman Sachs policy prohibits its analysts, persons reporting to analysts or members of their households from serving as an officer, director, advisory board member or employee of any company in the analyst's area of coverage. Non-U.S. Analysts: Non-U.S. analysts may not be associated persons of Goldman Sachs & Co. and therefore may not be subject to NASD Rule 2711/NYSE Rules 472 restrictions on communications with subject company, public appearances and trading securities held by the analysts. Distribution of ratings: See the distribution of ratings disclosure above. Price chart: See the price chart, with changes of ratings and price targets in prior periods, above, or, if electronic format or if with respect to multiple companies which are the subject of this report, on the Goldman Sachs website at http://www.gs.com/research/hedge.html. Additional disclosures required under the laws and regulations of jurisdictions other than the United States The following disclosures are those required by the jurisdiction indicated, except to the extent already made above pursuant to United States laws and regulations. Australia: This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. Canada: Goldman Sachs & Co. has approved of, and agreed to take responsibility for, this research in Canada if and to the extent it relates to equity securities of Canadian issuers. Analysts may conduct site visits but are prohibited from accepting payment or reimbursement by the company of travel expenses for such visits. Hong Kong: Further information on the securities of covered companies referred to in this research may be obtained on request from Goldman Sachs (Asia) L.L.C. India: Further information on the subject company or companies referred to in this research may be obtained from Goldman Sachs (India) Securities Private Limited; Japan: See below. Korea: Further information on the subject company or companies referred to in this research may be obtained from Goldman Sachs (Asia) L.L.C., Seoul Branch. Russia: Research reports distributed in the Russian Federation are not advertising as defined in the Russian legislation, but are information and analysis not having product promotion as their main purpose and do not provide appraisal within the meaning of the Russian legislation on appraisal activity. Singapore: Further information on the covered companies referred to in this research may be obtained from Goldman Sachs (Singapore) Pte. (Company Number: 198602165W). Taiwan: This material is for reference only and must not be reprinted without permission. Investors should carefully consider their own investment risk. Investment results are the responsibility of the individual investor. United Kingdom: Persons who would be categorized as retail clients in the United Kingdom, as such term is defined in the rules of the Financial Services Authority, should read this research in conjunction with prior Goldman Sachs research on the covered companies referred to herein and should refer to the risk warnings that have been sent to them by Goldman Sachs International. A copy of these risks warnings, and a glossary of certain financial terms used in this report, are available from Goldman Sachs International on request. European Union: Disclosure information in relation to Article 4 (1) (d) and Article 6 (2) of the European Commission Directive 2003/126/EC is available at http://www.gs.com/client_services/global_investment_research/europeanpolicy.html which states the European Policy for Managing Conflicts of Interest in Connection with Investment Research. Japan: Goldman Sachs Japan Co., Ltd. is a Financial Instrument Dealer under the Financial Instrument and Exchange Law, registered with the Kanto Financial Bureau (Registration No. 69), and is a member of Japan Securities Dealers Association (JSDA) and Financial Futures Association of Japan (FFAJ). Sales and purchase of equities are subject to commission pre-determined with clients plus consumption tax. See company-specific disclosures as to any applicable disclosures required by Japanese stock exchanges, the Japanese Securities Dealers Association or the Japanese Securities Finance Company. Ratings, coverage groups and views and related definitions Buy (B), Neutral (N), Sell (S) -Analysts recommend stocks as Buys or Sells for inclusion on various regional Investment Lists. Being assigned a Buy or Sell on an Investment List is determined by a stock's return potential relative to its coverage group as described below. Any stock not assigned as a Buy or a Sell on an Investment List is deemed Neutral. Each regional Investment Review Committee manages various regional Investment Lists to a global guideline of 25%-35% of stocks as Buy and 10%-15% of stocks as Sell; however, the distribution of Buys and Sells in any particular coverage group may vary as determined by the regional Investment Review Committee. Regional Conviction Buy and Sell lists represent investment recommendations focused on either the size of the potential return or the likelihood of the realization of the return. Return potential represents the price differential between the current share price and the price target expected during the time horizon associated with the price target. Price targets are required for all covered stocks. The return potential, price target and associated time horizon are stated in each report adding or reiterating an Investment List membership. Coverage groups and views: A list of all stocks in each coverage group is available by primary analyst, stock and coverage group at http://www.gs.com/research/hedge.html. The analyst assigns one of the following coverage views which represents the analyst's investment outlook on the coverage group relative to the group's historical fundamentals and/or valuation. Attractive (A). The investment outlook over the following 12 months is favorable relative to the coverage group's historical fundamentals and/or valuation. Neutral (N). The investment outlook over the following 12 months is neutral relative to the coverage group's historical fundamentals and/or valuation. Cautious (C). The investment outlook over the following 12 months is unfavorable relative to the coverage group's historical fundamentals and/or valuation. Not Rated (NR). The investment rating and target price have been removed pursuant to Goldman Sachs policy when Goldman Sachs is acting in an advisory capacity in a merger or strategic transaction involving this company and in certain other circumstances. Rating Suspended (RS). Goldman Sachs Research has suspended the investment rating and price target for this stock, because there is not a sufficient fundamental basis for determining, or there are legal, regulatory or policy constraints around publishing, an investment rating or target. The previous investment rating and price target, if any, are no longer in effect for this stock and should not be relied upon. Coverage Suspended (CS). Goldman Sachs has suspended coverage of this company. Not Covered (NC). Goldman Sachs does not cover this company. Not Available or Not Applicable (NA). The information is not available for display or is not applicable. Not Meaningful (NM). The information is not meaningful and is therefore excluded. Global product; distributing entities The Global Investment Research Division of Goldman Sachs produces and distributes research products for clients of Goldman Sachs, and pursuant to certain contractual arrangements, on a global basis. Analysts based in Goldman Sachs offices around the world produce equity research on industries and companies, and research on macroeconomics, currencies, commodities and portfolio strategy. This research is disseminated in Australia by Goldman Sachs & Partners Australia Pty Ltd (ABN 21 006 797 897) on behalf of Goldman Sachs; in Canada by Goldman Sachs & Co. regarding Canadian equities and by Goldman Sachs & Co. (all other research); in Hong Kong by Goldman Sachs (Asia) L.L.C.; in India by Goldman Sachs (India) Securities Private Ltd.; in Japan by Goldman Sachs Japan Co., Ltd.; in the Republic of Korea by Goldman Sachs (Asia) L.L.C., Seoul Branch; in New Zealand by Goldman Sachs & Partners New Zealand Limited on behalf of Goldman Sachs; in Russia by OOO Goldman Sachs; in Singapore by Goldman Sachs (Singapore) Pte. (Company Number: 198602165W); and in the United States of America by Goldman Sachs & Co. Goldman Sachs International has approved this research in connection with its distribution in the United Kingdom and European Union. Goldman Sachs Global Investment Research 13

- 14. December 20, 2010 Momenta Pharmaceuticals (MNTA) European Union: Goldman Sachs International, authorized and regulated by the Financial Services Authority, has approved this research in connection with its distribution in the European Union and United Kingdom; Goldman Sachs & Co. oHG, regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht, may also distribute research in Germany. General disclosures This research is for our clients only. Other than disclosures relating to Goldman Sachs, this research is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. We seek to update our research as appropriate, but various regulations may prevent us from doing so. Other than certain industry reports published on a periodic basis, the large majority of reports are published at irregular intervals as appropriate in the analyst's judgment. Goldman Sachs conducts a global full-service, integrated investment banking, investment management, and brokerage business. We have investment banking and other business relationships with a substantial percentage of the companies covered by our Global Investment Research Division. Goldman Sachs & Co., the United States broker dealer, is a member of SIPC (http://www.sipc.org). Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and our proprietary trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our asset management area, our proprietary trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views expressed in this research. We and our affiliates, officers, directors, and employees, excluding equity and credit analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives, if any, referred to in this research. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. The price and value of investments referred to in this research and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments. Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Investors should review current options disclosure documents which are available from Goldman Sachs sales representatives or at http://www.theocc.com/about/publications/character-risks.jsp. Transactions cost may be significant in option strategies calling for multiple purchase and sales of options such as spreads. Supporting documentation will be supplied upon request. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client websites. Not all research content is redistributed to our clients or available to third-party aggregators, nor is Goldman Sachs responsible for the redistribution of our research by third party aggregators. For all research available on a particular stock, please contact your sales representative or go to http://360.gs.com. Disclosure information is also available at http://www.gs.com/research/hedge.html or from Research Compliance, 200 West Street, New York, NY 10282. Copyright 2010 The Goldman Sachs Group, Inc. No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of The Goldman Sachs Group, Inc. Goldman Sachs Global Investment Research 14