Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

Crude By Rail Congress

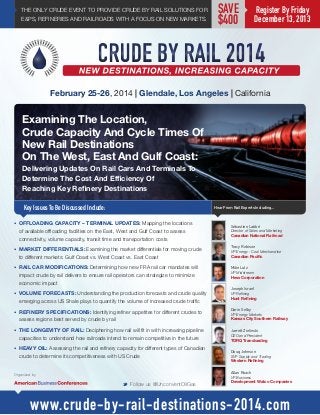

- 1. THE ONLY CRUDE EVENT TO PROVIDE CRUDE BY RAIL SOLUTIONS FOR E&PS, REFINERIES AND RAILROADS WITH A FOCUS ON NEW MARKETS. SAVE $400 Register By Friday December 13, 2013 February 25-26, 2014 | Glendale, Los Angeles | California Examining The Location, Crude Capacity And Cycle Times Of New Rail Destinations On The West, East And Gulf Coast: Delivering Updates On Rail Cars And Terminals To Determine The Cost And Efficiency Of Reaching Key Refinery Destinations Key Issues To Be Discussed Include: Hear From Rail Experts Including... • OFFLOADING CAPACITY – TERMINAL UPDATES: Mapping the locations of available offloading facilities on the East, West and Gulf Coast to assess connectivity, volume capacity, transit time and transportation costs • MARKET DIFFERENTIALS: Examining the market differentials for moving crude to different markets: Gulf Coast vs. West Coast vs. East Coast • RAIL CAR MODIFICATIONS: Determining how new FRA rail car mandates will impact crude by rail delivers to ensure rail operators can strategize to minimize economic impact • VOLUME FORECASTS: Understanding the production forecasts and crude quality emerging across US Shale plays to quantify the volume of increased crude traffic • REFINERY SPECIFICATIONS: Identifying refiner appetites for different crudes to assess regions best served by crude by rail Sébastien Labbé Director of Sales and Marketing Canadian National Railroad Tracy Robison VP Energy - Coal Merchandise Canadian Pacific Mike Lutz VP Midstream Hess Corporation Joseph Israel VP Refining Hunt Refining Darin Selby VP Energy Markets Kansas City Southern Railway • THE LONGEVITY OF RAIL: Deciphering how rail will fit in with increasing pipeline capacities to understand how railroads intend to remain competitive in the future • HEAVY OIL: Assessing the rail and refinery capacity for different types of Canadian crude to determine its competitiveness with US Crude Jarrett Zielinski CEO and President TORQ Transloading Doug Johnson SVP Supply and Trading Western Refining Allan Roach Organized by VP Business M Follow us @UnconventOilGas Development Watco Companies www.crude-by-rail-destinations-2014.com

- 2. SAVE $400 Register By Friday December 13, 2013 Crude By Rail: New Destinations, Increasing Capacity 2014 has come at a time where the rail industry faces several big question marks - some even as big as questioning the longevity of rail as an economically competitive mode of crude takeaway. With the collapse in price differentials, new pipeline projects not far from completion and additional costs potentially incurred from new rail car modification mandates, the evaluation of available capacity, economics and logistics of getting to different rail terminal destinations could not come at a better time. Railroad companies will be leading the congress at the upcoming Crude By Rail 2014: New Destinations, Increasing Capacity to deliver updates on the location of on-loading and offloading terminals, railroad expansion plans as well as cycle times to different destinations on the East, West & Gulf Coast to allow refiners and producers to determine the cost and efficiency of reaching key refinery destinations. Latest FRA rail car regulations and modifications will also be discussed to enable strategies for cost-effective compliance and minimize the impact on the efficiency and cost of crude by rail. As crude oil volumes continue to rise, the demand for increased capacity to take crude to new markets quickly and economically, is on the rise with it. Producers and refiners want to know the latest offloading terminal locations, railroad connectivity to new and emerging markets in the West, Gulf and East Coast, cycle times, volume capacities and the cost of transportation to enable a thorough evaluation of the market differentials of moving crude to different rail markets vs. pipeline. Against the current climate, it is crucial that railroads stay competitive and as a result, the congress will be focused around how rail operators are planning to meet the demands of refiners and producers through the expansion of railroads, rail cars and terminal capacity. DAY ONE: DESTINATION LOGISTICS - ON-LOADING & OFFLOADING TERMINAL CAPACITY AND REFINERY SPECIFICATIONS The timely agenda has been designed specifically to deliver solutions for all three major stakeholders: SOLUTIONS FOR E&P’s: Identifying Refinery Demand And Most Viable Markets For Different Crude Types To Assess The Cost And Logistics Of Getting Crude To New Delivery Points And Ultimately Determine Whether Economic Netbacks Can Still Be Achieved By Moving Crude By Rail Vs. Pipeline SOLUTIONS FOR RAIL OPERATORS: Understanding Refiner Markets And Preferences To Identify Regions Best Served By Crude By Rail As Well As Identifying Strategies To Decrease Cycle Time And Compete With Pipeline In The Future SOLUTIONS FOR REFINERIES: Mapping The Locations, Volume Capacity And Crude Types Offered At Different Offloading Terminals To Ensure Crude Quality And Volume Specifications Are Met Within Budget Day one will start by providing a keynote perspective from each of the major stakeholders: we will first hear a rail operator’s perspective on how they seek to meet the demands of refiners and producers through the expansion of railroads, rail cars terminal capacity. This will then be followed by a producer perspective on the crude grades and volumes emerging from different US shale plays as well as a refiner’s perspective on future plans to redesign crude slates to take advantage of different crude types being produced. Speakers will then assess different delivery points and refineries across the West, East and Gulf Coast to enable an evaluation of the volume capacity, rail connectivity and economics of each. The day will end with an assessment of current rail and refinery capacity for different types of Canadian crude as well as exploring the flexibility of heavy crude terminals to accept light crude. DAY TWO: ECONOMICS OF RAIL Day two will scrutinize the market differentials and the different options for minimizing rail costs to assess the long-term economic viability of rail to different markets. The following things will be discussed with regards to increasing rail efficiencies and minimizing costs: unit vs. manifest trains, increasing cycle time and creating efficiencies, rail car regulations and modifications. The day will end with a discussion of existing and future pipeline developments to enable an assessment of the longevity of crude by rail once these West Coast & East Coast pipelines have been built. Sponsorship And Exhibition Opportunities Available At The Congress Venue Information Need to generate new sales leads, launch a new product, engage key decision makers, build new future business relationships in key markets, or simply educate the industry about a new product? Then you need to exhibit at the Crude By Rail 2014: New Destinations, Increasing Capacity. Our busy exhibit area is an integral part of the Congress and is of genuine practical value to delegates, who are looking for new solutions and technologies. Exhibiting at the congress will help you position yourself as a market leader and centre of excellence to the key decision makers in the industry. Crude By Rail 2014: New For further information, please contact: info@american-business-conferences.com Glendale, CA 91202 Destinations, Increasing Capacity will be held at: Hilton Glendale Pasadena 100 West Glenoaks Blvd or + (1) 800 721 3915 www.crude-by-rail-destinations-2014.com (1) 800 721 3915 info@american-business-conferences.com

- 3. Day 1 Tuesday February 26, 2014 8.30 Chair’s Opening Remarks Chaired By: Joseph Israel, SVP Refining, Hunt Refining Company KEYNOTE: RAILROAD PERSPECTIVE 8.40 How Rail Operators Seek To Meet The Demands Of Refiners And Producers Through The Expansion Of Railroads, Rail Cars & Terminal Capacity • Determining the frequency of crude movements per week to assess the availability of crude by rail to refiners on a daily basis • Examining the number of cars being sent per movement to examine the capacity of the railroad to deliver required volumes by refineries • Understanding the measures being taken to ensure crude reaches refineries without delay • Assessing how a leading rail operator plans to increase capacity to ensure increased crude volumes can get to market • Evaluating how to avoid congestion in areas like Chicago and LA to guarantee on-time delivery and ensure product reaches market • Identifying the maximum capacity of the railroad system to determine its flexibility in handling increased crude volumes Tracy Robinson, VP Energy - Coal & Merchandise, Canadian Pacific 9.10 Question & Answer Session KEYNOTE 2: PRODUCER PERSPECTIVE 9.20 Forecasting Crude Grades And Volumes Emerging From Different US Shale Plays To Locate Favorable Supply Points And Optimize Capital Allocation • Supply Of Crude: Identifying the proportion of total production an operator is planning to move by rail to quantify crude volumes • Examining the key crude markets a producer would like to reach to assess the current capacity of rail to get it there and plan for any necessary expansion • Understanding any constraints from lateral lines or rail lines to connect production fields to main rail lines to identify any connectivity issues to get crude to market • Identifying promising emerging shale plays to indicate new potential sources of crude supply for refineries Todd Morgan, VP Crude Oil & NGL Marketing, Devon Energy 9.50 Question & Answer Session 10.00 Morning Refreshments In Exhibition Showcase Area KEYNOTE 3: REFINERY PERSPECTIVE 10.30 Examining Refinery Plans To Redesign Crude Slate To Take Advantage Of Different Crudes Being Produced Across Varying US Shale Plays • Determining the extent to which the refinery industry can change to adapt and facilitate the processing of new products such as condensate • Determining how much more light crude US refineries as a whole will be able to absorb if they were to absorb more light oil and back out heavy imported oil • Considering the key factors influencing crude selection, crude quality and choice of other intermediates • Understanding what adjustments refiners are making to their infrastructure to enable acceptance of a broader range of crudes Joseph Israel, SVP Refining, Hunt Refining Company 11.00 Question & Answer Session SECTION 1 DELIVERY POINTS AND REFINERIES: WEST, EAST AND GULF COAST THE NEXT 6 PRESENTATIONS WILL EXAMINE THE VOLUME CAPACITY AND RAIL CONNECTIVITY TO OFFLOADING FACILITIES AND REFINERIES TO EVALUATE THE ECONOMIC VIABILITY OF EACH DELIVERY POINT SOLUTIONS FOR E&Ps : Identifying Refinery Demand And Most Viable Markets For Different Crude Types To Assess The Cost And Logistics Of Getting Crude To Those Delivery Points SOLUTIONS FOR RAIL OPERATORS : Understanding Refiner Markets And Preferences To Identify Regions Best Served By Crude By Rail And Co-ordinate An Investment Strategy SOLUTIONS FOR REFINERIES: Mapping The Locations, Volume Capacity And Crude Types Offered At Different Offloading Terminals To Ensure Crude Quality And Volume Specifications Are Met WEST COAST: LOAD OUT LOCATIONS 11.10 Locating Available Offloading Facilities In The West Coast To Assess Connectivity, Volume Capacity, Transit Time And Transportation Costs • Mapping load out terminals across California to identify new potential crude destinations • Revealing new terminal development projects that are planned to identify the additional offloading capacity this will provide Destination Logistics Onloading And Offloading Terminal Capacity And Refinery Specifications • Addressing the proximity of rail terminals to West Coast refineries to evaluate its economic viability in light of the full cost of transportation • Determining whether West Coast terminals have sufficient storage and loading capacity to support the number of cars required on a daily basis • Evaluating the transit times for offloading facilities that have been built to support unit trains relative to that of manifest trains • Examining charter rates to quantify any additional marine barge costs involved in shipping oil to its final location Ryan Fischer, AVP Emerging Markets, Genesee & Wyoming Inc 11.40 Question & Answer Session 11.50 Lunch In Exhibition Showcase Area CALIFORNIAN REFINERIES 12.50 Defining The Crude Types That Fit The Current Product Slates Of Californian Refineries To Quantify Demand For Specific Crude Qualities • Identifying the maximum levels of wax and paraffin that are allowed in the oil to isolate suitable naphthenic crude supplies • Stating the API, boiling point and sulphur content cut offs to identify crude supply matches and assess existing rail loading facilities to those areas • Examining how refineries are adapting to accept more viscose crude oils • Exploring the potential for West Coast refiners to receive domestic supply by barge from Canadian sources • Assessing the requirement for crude oils with a higher plopoint than current supply to the West Coast to determine how available products will be able to flow Mark Phair, VP And General Manager, Wilmington RefineryValero Doug Johnson, SVP Supply & Trading, Western Refining 1.20 Question & Answer Session WEST COAST OPPORTUNITIES 1.30 Examining The West Coast And Mid Continent As Potential Markets For Crude By Rail: What Is The Nature And Extent Of Investment Required To Maximize Connectivity To Domestic Supply? • Detailing the crude slates and complexity of West Coast refiners to better understand market demand for domestic supply and the potential for crude by rail within the regional supply chain • Revealing existing crude by rail offload capacity and terminal development on the West Coast and Mid Continent • Understanding existing footprint constraints for refiners and the impact on the business case for rail direct service in contrast to intermodal supply • Exploring the potential for West Coast refiners to receive domestic supply via barge from Canadian sources • How does the lack of pipeline connectivity to West Coast markets, and the lack of marine optionality for Mid Continent refiners, affect the business case for deeper rail and intermodal integration? of capacity expansion • Understanding if pipeline capacity will ever reach high enough levels to fully satisfy the market to derive the long-term sustainability of rail • Examining the long-term impact of East Coast refineries becoming solvent or remaining compressed on other players in the industry Allan Roach, SVP Business Development, Watco Companies 3.50 Question & Answer Session GULF COAST: REFINERIES 4.00 Addressing Volumes And Crude Types Being Accepted In The Gulf • Coast To Identify Potential Customers And Expected Capacity • Detailing high TAN crude deliveries to Gulf Coast Refineries to quantify volume capacity to the marketIdentifying the range of crudes accepted into the Gulf Coast to identify the crude quality in the highest demand • Examining refinery complexity to better evaluate market demand for different crudesForecasting transportation costs from Canada to the Gulf Coast terminals over the next 5-10 years to understand if refineries might switch to heavy oil sources • Calculating the different netbacks received for marketing crude to the Gulf Coast vs. the East & West Coast Joseph Israel, SVP Refining, Hunt Refining Company 4.30 Question & Answer Session SECTION 2 CANADIAN LIGHT AND HEAVY OILTHE NEXT 2 PRESENTATIONS WILL ASSESS THE CURRENT RAIL AND THE NEXT 2 SESSIONS LOOK AT REFINERY CAPACITY FOR DIFFERENT TYPES OF CANADIAN CRUDE ACROSS THE US TO DETERMINE ITS COMPETITIVENESS WITH US CRUDE SOLUTIONS FOR E&PS: Evaluating The Possibility Of Having Light Crude Accepted At Heavy Oil Terminals To Assess The Flexibility Of Accepting A Wider Range Of Crude Types SOLUTIONS FOR REFINERIES: Mapping The Distance Of Different Offloading Locations To Different Refineries To Quantify The Supply Available At Different Delivery Points SOLUTIONS FOR RAIL OPERATORS: Identifying The Crude Quality And Capacity Requirements Of Heavy Oil Refineries To Ensure Sufficient Rail Infrastructure To Meet Them HEAVY CRUDE: REFINERIES AND TERMINALS 4.40 Evaluating The Possibility Of Having Light Crude Accepted At Heavy Crude Terminals To Assess Flexibility For Accepting A Wider Range Of Crude types • Examining the turn times of transporting and offloading heavy crude by rail to determine the time and cost requirements • Assessing the capabilities of carrying out in-terminal blending 2.00 Question & Answer Session EAST COAST: OFFLOADING FACILITIES 2.10 Providing Updates On New Offloading Terminals To Facilitate The Railing Of Crude To PADD 1 Refineries to enable the acceptance of multiple crude streams that can be blended to refinery specs • Examining the quality parameters that refiners are seeking to assess how they value different types of Canadian crudeComparing the quality of heavy crude from Western Canada vs. competing regions to evaluate competitiveness of the product and clarify crude quality misconceptions • Determining the number of light processing refineries vs. heavy processing refineries to evaluate capacity requirements • Outlining new projects under construction in the East Coast Jarrett Zielinski, CEO, TORQ Transloading Mark Smith, VP Development, Supply & Logistics, Tesoro to assess the status of new rail destinations • Calculating the netbacks from different East Coast delivery points to determine the economic feasibility of railing to these markets • Examining scheduling to West Coast markets to deduce frequency of deliveries • Quantifying the volume capacity of different East terminals to determine which are the most viable for large volumes of crudeIdentifying if any advances or efficiencies have been made to speed up offloading and transit time Erik Johnson, VP & General Manager, Canopy Prospecting 2.40 Question & Answer Session 2.50 Afternoon Refreshments In Exhibition Showcase Area EAST COAST REFINERIES 3.20 The Future Of East Coast Refineries: Examining Strategies For Economically Connecting East Coast Refiners To Domestic Supply • Examining the market demand for different crudes on the East Coast to evaluate the current supply-demand dynamic • Analyzing how rail offloading capacity and East Coast terminals have developed in the past year to determine extent 5.10 Question & Answer Session CANADA: RAIL CAPACITY INCREASE 5.20 Delivering Expansion Plans For Track And Loading Terminal Construction To Deliver Crude From Canada To The US: Location, Capacity And When It Will Be Available • Examining the location of new tracks and track expansion projects to determine alternate routes to market for Western Canadian crude • Examining crude qualities that can be moved by rail compared to pipeline to determine the usability of rail expansions for both light and heavy oil producers • Quantifying the increase in takeaway capacity new projects will provide to determine how much extra product will be able to reach US markets • Hearing when the projects will be finished and available for use to assess the speed at which future crude volumes will reach markets • Outlining the decline in the transportation of coal to examine how this could increase the availability of railway capacity for Canadian Ryan Fischer, AVP Emerging Markets, Genesee & Wyoming Inc 5.40 Question & Answer Session 5.50 Chair’s Closing Remarks 6.00 - 7.00 Networking Drinks Reception In Exhibition case Area www.crude-by-rail-destinations-2014.com (1) 800 721 3915 info@american-business-conferences.com

- 4. Day 2 Economics Of Rail Wednesday February 26, 2014 9.00 Chair’s Opening Remarks SECTION 3 THE ECONOMICS OF CRUDE BY RAIL THE NEXT 4 PRESENTATIONS WILL SCRUTINIZE MARKET DIFFERENTIALS AND OPTIONS FOR MINIMIZING RAIL COSTS TO DETERMINE THE ECONOMIC SUSTAINABILITY OF RAIL SOLUTIONS FOR E&PS: Determining Whether Economic Netbacks Can Still be Achieved Moving Crude By Rail Over Pipe In Light Of Recent Collapse Of Price Differentials SOLUTIONS FOR RAIL OPERATORS: Identifying Innovative Techniques And Technologies To Drive Down Costs, Optimize Terminal Efficiency, Rail Car Safety And Improve Cycle Times SOLUTIONS FOR REFINERIES: Calculating The Cost For Transporting Specific Crude Types And Volumes By Rail To Determine If Pipeline Or Rail Better Meet Their Needs MARKET DIFFERENTIALS 9.10 Examining The Market Differentials For Moving Crude To Different US Markets: Gulf Coast Vs. West Coast Vs. East Coast • Breaking down operating, feedstock, energy, labor and environmental costs against market price being offered in each of these markets • Examining how markets might change over the next year to determine the impact this might have on cost of rail and overall netbacks • Evaluating how differentials might suggest movements of crude and volumes shifting over time • Using the industrial price deck IHS to determine supply and demand: where crude price is going by grade and type and source of origin • Exploring the capabilities of transport to under-utilized US markets to highlight the potential to increase market diversity Mike Lutz, VP Midstream, Hess Corporation 9.40 Question & Answer Session RAIL PERSPECTIVE: LONGEVITY OF RAIL 9.50 Deciphering How Rail Will Fit In With Increasing Pipeline Capacities To Understand How Railroads Intend To Remain Competitive In The Future • Clarifying what incentives rail operators can provide to reduce rail costs and maximize netbacks • Examining forecasted crude production volumes vs. pipeline capacity once built to quantify excess production that cannot be moved by pipe • Identifying new rail expansion projects that will allow railcars to reach markets that pipeline cannot access • Assessing where the demand for freight will be to assess whether rail capacity can be expanded to transport other oilfield related products • Providing a strong economic business case for using rail to justify 5 year railcar and 3-4 year terminal commitments Sebastien Labbe, Director Of Sales And Marketing, Canadian National Railroad 10.20 Question & Answer Session 10.30 Morning Refreshments In Exhibition Showcase Area UNIT VS. MANIFEST TRAIN 11.00 Economics Of Using Unit Trains Vs. Manifest Trains Relative To Pricing At Destination To Determine Which System Is Most Effective In Increasing Netback DECREASING CYCLE TIME AND CREATING EFFICIENCIES 11.40 Exploring The Innovative Techniques A Leading Railroad Is Using To Decrease Cycle Time, Optimize Terminal Efficiencies And Avoid Delays • Examining how railroads keep track of forecasted deliveries and schedules to ensure product reaches the market on time • Exploring the effectiveness of tracking devices to avoid paying demerge costs • Discussing manpower considerations and measures taken to ensure the constant movement at offloading facilities • Alleviating congestion to avoid costs incurred by cars getting stuck in a bottleneck • Comparing the efficiencies of moving crude via pipelines vs. rail Marvin Matthews, Customer Communications Manager, Canadian Pacific 12.10 Question & Answer Session 12.20 Lunch In Exhibition Showcase Area SECTION 4 RAIL CAR REGULATIONS AND MODIFICATIONS THE NEXT 2 PRESENTATIONS WILL OUTLINE THE LATEST FRA REGULATIONS AND THE STRATEGIES FOR RAIL OPERATORS TO COMPLY WITH THEM SOLUTIONS FOR E&PS: Understanding If New Rail Car Regulations Will Impact The Efficiency And Cost Of Crude By Rail For Producers SOLUTIONS FOR RAIL OPERATORS: Examining The Most Cost-Efficient Strategies For Enhancing Rail Car Safety And Understanding If Leasing New Cars Will Render Some Rail Destinations Economically Viable SOLUTIONS FOR REFINERIES: Assessing The Impact New Regulations Will Have On The Speed And Efficiency Of Crude By Rail Deliveries REGULATIONS: RAIL CARS 1.20 Determining How New FRA Regulations Will Impact The Speed, Efficiency, Economics And Future Growth Of Crude By Rail Deliveries • Examining if speed restrictions will be brought in to slow down rail cars in transit to assess the impact on scheduling and delivery times • Understanding what fines have been put in place and under what conditions, to ensure rail operators adhere to new regulations • Detailing the required modifications to the 1.11 cars and the required modifications for the T77 cars to understand retrofitting costs involved • Clarifying what changes will be implemented and when to determine if new cars will have to be leased, the costs implied and re-assess the economic viability of certain projects as a result Joseph C Szabo, Administrator, FRA 1.50 Question & Answer Session NEW RAIL CAR DESIGNS 2.00 Modeling New Rail Car Designs: Strategies For Ensuring The Most Effective Rail Car Protection For The Least Coast • Ensuring the optimum balance between additional protection Darin Selby, VP Energy Markets, Kansas City Southern Railway and car weight: at what point do transport costs as a result of increased car weight become uneconomical? • Examining advances in car design including head shields and protection hardening and their effectiveness in preventing derailment • Understanding if old rail cars are going to be obsolete or if there is an economic strategy to retro-fit old cars with new types of lining • Will there be a phasing out of DOT 1.11 cars? - Will there be enough new cars in the industry to keep up with the pace required if so? 2.30 Question & Answer Session 11.30 Question & Answer Session SECTION 5 EAST AND WEST COAST PIPELINE UPDATES THE NEXT 2 PRESENTATIONS WILL DISCUSS EXISTING AND FUTURE PIPELINE DEVELOPMENTS TO EVALUATE THE SUSTAINABILITY OF CRUDE BY RAIL IN DIFFERENT GEOGRAPHICAL LOCATIONS SOLUTIONS FOR E&PS: Assessing The Commitments Required By Pipelines To Determine If A Producer Would Benefit From The Increased Flexibility Provided By Rail SOLUTIONS FOR RAIL OPERATORS: Identifying The Markets That Pipeline Will Not Be Able To Reach To Ensure Rail Connectivity To Those Locations SOLUTIONS FOR REFINERIES: Examining Whether Pipeline Projects Will Result In Higher Profit Margins And If The Crude They Move Will be Able To Meet Refinery Specifications PIPELINE UPDATES: WEST COAST 3.10 Determining The Impact Of The Trans-Mountain Pipeline On Rail Traffic To The West Coast • Examining the status of the pipeline expansion into different regions to assess the economics of rail expansion into these areas • Identifying refineries that will not be easily reached by the pipeline to coordinate rail infrastructure to best serve the markets needs • Forecasting transport costs and tariffs against market prices to assess the netback compared to that of rail • Discussing the argument for rail as a long-term compliment to pipe rather than a short term competitor 3.40 Question & Answer Session PIPELINE UPDATES: EAST COAST 3.50 Strategizing Ways To Stay Competitive Once The East Coast Pipeline • Has Been Built • Examining which lanes are likely to be affected by the East Coast pipeline to allow effective repositioning of cars as is possible • Understanding the time frame in which this pipeline capacity will come on and the volume capacity to determine the economic viability of crude by rail in those areas • Investigating the possible capacities of the plans for the East Coast pipeline and whether it will cause rail car displacement • Assessing the lack of flexibility and long-term commitments required by pipeline agreements can incentivize the growth of rail infrastructure 4.10 Question & Answer Session 4.20 Chair’s Closing Remarks And End Of Conference “I was extremely excited to see that a follow up crude by rail conference was being hosted. The first event provided timely information on a broad range of issues facing CBR. In addition, this conference was so well attended, it allowed me to connect with colleagues across the industry. As the upcoming conference seeks to extend its focus on key issues brought out in the first meeting, I look forward to this event” 2.40 Afternoon Refreshments In Exhibition Showcase Area • Outlining the quantity of crude that needs to be transported to make both unit and manifest operations economical • Detailing the cost of building and operating a unit vs. manifest train terminal and how this impacts tariffs • Determining the effect increased unit train operations will have on alleviating bottlenecks and how this will impact net value • Analyzing the increased transportation volumes of unit vs. manifest rail expansion to determine the increased takeaway capacity out of Alberta Delek US www.crude-by-rail-destinations-2014.com (1) 800 721 3915 info@american-business-conferences.com

- 5. Yes P I would like to register the delegate(s) below for the 2 day conference Crude By Rail 2014: New Destinations, Increasing Capacity Details PLEASE USE CAPITALS - PHOTOCOPY FOR MULTIPLE DELEGATES Delegate 1 Delegate 2 * Mr * Mr * Dr * Miss * Ms * Mrs * Other: * Dr * Miss * Ms * Mrs * Other: Name Name Position Position Organization Organization Email Email Telephone Telephone Address For Invoice Purposes WE HAVE GROUP DISCOUNTS Zip/Postal Code So you can involve your whole team Country Call for rates: (1) 800 721 3915 Delegate Rates GUESTS ARE RESPONSIBLE FOR THEIR OWN TRAVEL AND ACCOMODATION ARRANGEMENTS Super Early Booking Discount Early Booking Discount Standard Rate Book And Pay By Friday December 13, 2013 Book And Pay By Friday January 10, 2014 From January 11, 2014 * $1399 USD SAVE $400 * $1599 USD SAVE $200 2 Day Conference Pass * $1799 USD All prices quoted above are inclusive of GST Payment PLEASE TICK APPROPRIATE BOXES AND COMPLETE DETAILS Payment must be received in full prior to the event. * 1. CREDIT CARD Option Please charge my * VISA * AMERICAN EXPRESS Amount $ USD Expiry date Card number Security Code / CVV (required) Name on card * MASTERCARD Signature of card holder * 2. INVOICE Option An invoice containing payment instructions will be sent electronically upon receipt of the completed registration form. How To Finalize Your Registration Terms & Conditions The conference is being organized by American Business Conferences, a division of London Business Conferences Ltd, a limited liability company formed under English company law and registered in the UK no. 5090859. Cancellations received 30 days prior to the start of the event will be eligible for a refund less $150 administration fee, after this point no refund will be given. Cancellations must be made in writing, if you are unable to attend you may nominate a colleague to attend in your place at no additional cost. Receipt of this registration form, inclusive or exclusive of payment constitutes formal agreement to attend and acceptance of the terms and conditions stated. All outstanding fees must be paid within our standard payment period of 7 days. Any outstanding invoices will remain valid should cancellation of attendance be received outside of the aforementioned cancellation period. *If you are claiming the early booking discount this may not be used in conjunction with other discounts advertised elsewhere. All discount codes and offers must be claimed at the time of registration. American Business Conferences reserves the right to alter or cancel the speakers or program. American Business Conferences reserve the right to refuse admission. We would like to keep you informed of other American Business Conferences products and services. This will be carried out in accordance with the Data Protection Act. Please write to the Head of Marketing, American Business Conferences at the address below if you specifically do not want to receive this information. American Business Conferences. City Center One. 800 Town & Country Blvd. Suite 300. Houston. Texas. 77024 American Business Conferences will not accept liability for any individual transport delays and in such circumstances the normal cancellation restrictions apply. American Business Conferences is a Division of London Business Conferences Limited, Registered in England No. 5090859 EIN. no: 98-0514924 Now that your details are completed please send your registration form to our Customer Service Team using one of the following options: Option 1. Email: info@american-business-conferences.com Option 2. Fax: (1) 800 714 1359 Enquiries And More Information Should you have any enquiries or if you would like to request more information please contact our friendly Customer Service Team on (1) 800 721 3915 or visit the conference website at www.crude-by-rail-destinations-2014.com www.crude-by-rail-destinations-2014.com (1) 800 721 3915 info@american-business-conferences.com