Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Ähnlich wie Asian paints 20110405_1302845884

Ähnlich wie Asian paints 20110405_1302845884 (20)

Asian paints 20110405_1302845884

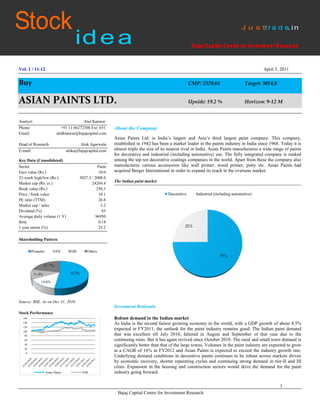

- 1. Stock Idea – Asian Paints Ltd. Vol. 1 / 11-12 April 5, 2011 Buy CMP: 2529.65 Target: 3014.0 ASIAN PAINTS LTD. Upside: 19.2 % Horizon: 9-12 M Analyst: Atul Kanwar Phone: +91 11 66272300 Ext: 651 About the Company Email: atulkanwar@bajajcapital.com Asian Paints Ltd. is India’s largest and Asia’s third largest paint company. This company, Head of Research: Alok Agarwala established in 1942 has been a market leader in the paints industry in India since 1968. Today it is E-mail: aloka@bajajcapital.com almost triple the size of its nearest rival in India. Asian Paints manufactures a wide range of paints for decorative and industrial (including automotive) use. The fully integrated company is ranked Key Data (Consolidated) among the top ten decorative coatings companies in the world. Apart from these the company also Sector Paint manufactures various accessories like wall primer, wood primer, putty etc. Asian Paints had Face value (Rs.) 10.0 acquired Berger International in order to expand its reach in the overseas market. 52-week high/low (Rs.) 3027.3 / 2008.0 The Indian paint market Market cap (Rs. cr.) 24264.4 Book value (Rs.) 250.3 Price / book value 10.1 Decorative Industrial (including automotive) PE ratio (TTM) 26.8 Market cap / sales 3.2 Dividend (%) 85 Average daily volume (1 Y) 96950 Beta 0.14 1 year return (%) 25.2 25% Shareholding Pattern Promoter FII DII Others 75% 21..7% 11.4% 52.3% 14.6% Source: BSE. As on Dec 31, 2010 Investment Rationale Stock Performance 160 Robust demand in the Indian market 140 As India is the second fastest growing economy in the world, with a GDP growth of about 8.5% 120 100 expected in FY2011, the outlook for the paint industry remains good. The Indian paint demand 80 that was excellent till July 2010, faltered in August and September of that year due to the 60 continuing rains. But it has again revived since October 2010. The rural and small town demand is 40 significantly better than that of the large towns. Volumes in the paint industry are expected to grow 20 0 at a CAGR of 16% in FY2012 and Asian Paints is expected to exceed the industry growth rate. Underlying demand conditions in decorative paints continues to be robust across markets driven by economic recovery, shorter repainting cycles and continuing strong demand in tier-II and III cities. Expansion in the housing and construction sectors would drive the demand for the paint Asian Paints NSE industry going forward. 1 Bajaj Capital Centre for Investment Research

- 2. Stock Idea – Asian Paints Ltd. The Indian paint industry has grown at an India paint industry: growth in volumes average of 15.3% from FY05 to FY10. 18% 18% 16% 16% 14% 13% 14% 13% FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E Source: Company Asian Paints is a giant of the Indian paint industry Asian Paints is the clear market leader in the Indian paints industry with about 32.4% market share. The top four players that include Berger, Kansai & ICI (Akzo Nobel) apart from Asian Paints, have cornered around 60% of the total market share. Other players in the organized sector account for only 5% of the industry market share. The unorganized sector is a large one but is very fragmented, constituting 35% of the total paints market. The organized section of the industry is growing faster than the unorganized sector. The competition in the paint industry is India’s paint industry: market share of major players becoming more intense with the entry of foreign players like Jotun, Nippon & Sherwin Asian Paints Berger Kansai ICI (Akzo Nobel) Others Unorganized sector Williams. 35.0% 32.4% 5.0% 10.8% 6.0% 10.8% Source: Company, BCCIR Huge capacity addition plans Strong volume visibility has resulted in Asian Paints continuing its streak of capacity addition. The commercial production at its new paint manufacturing facility at Rohtak, Haryana has started. The plant has an initial capacity of 1.5 lakh kl per annum. The project cost for setting up this capacity was Rs ~500 cr. The plant capacity can be scaled up to 4 lakh kl per annum in future expansions. The company is also planning to set up a manufacturing plant in northeastern parts of Andhra Pradesh with a capacity of 1 lakhs tonnes per annum. The company is considering this location because it is well connected with all parts of the country. Though the investment in the proposed plant was not disclosed but the management has said that they would like to set up one of the largest plants in India, if the Andhra Pradesh government provides them with land. The proposed Asian Paints bought land in Maharashtra for project will be classified under mega projects category. This decision was taken by the company a greenfield mega project with a capacity of 4 after the state government denied permission, due to environmental concerns, to set up the plant at lakh tonnes per annum. An amount of Rs 735 Patancheru on the outskirts of Hyderabad where the company has a manufacturing facility and cr would be spent on the project in 5 years. wanted to go in for brownfield expansion. 2 Bajaj Capital Centre for Investment Research

- 3. Stock Idea – Asian Paints Ltd. Asian Paints may look at further hike in prices Price hike if raw material prices continue to move up. To pass on the rise in raw material costs, Asian Paints has gone in for multiple price increase. The company has affected four price hikes in FY2011 i.e. 4.15% on May 1, 2.6% on July 1, 1.2% on August 1, and 2.9% in December 2010. The price hike has been the highest in the past 10 years, Asian Paints is the price leader and other players in the industry follow with a lag. Broadly, price hikes by all players have been similar. The paint industry in the past has been able to raise prices in line with the rise in inflation without having a significant impact on volumes. Asian Paints: price hikes over the years 4.2% 2.5% 2.6% 2.9% 1.4% 1.2% -1.8% -2.0% -2.3% -5.1% Source: Company In-house manufacturing of raw material Most paint companies are hit by the fact that they do not make raw materials themselves. For example, Phthalic Anhydride (PAN) is manufactured from orthoxylene, which goes into the Asian Paints benefits by selling Phthalic production of paints along with titanium dioxide. Asian Paints is the only paint company in India Anhydride (PAN) in the open market. that manufactures PAN. The other industry players have to import this stock. Since PAN prices generally outpace international orthoxylene prices by ~50%, paint companies end up paying a fortune when prices rise Shift to enamels & emulsion would lead to significant growth Growth is expected in future, in the paints industry through an increase in enamels and emulsion use. At present 19% of the revenue in the industry is realized through the distemper segment. But going ahead, the share of distemper is expected to come down, while that of enamels and emulsion is expected to go up. This would lead to better realizations and higher margins for the company. Revenue breakdown of Indian paint industry (FY10) Enamels Distemper Interior Emulsion Exterior Emulsion Wood Finish 2% 12% 17% 50% 19% Source: Company Extensive distribution network Almost half of the revenues earned by the Asian Paints has a very large distribution network in India. It boasts of 90 depots across the Indian paint industry are through enamels. country. It has over 27,000 retailers as compared to 6,500 of Kansai Nerolac. 3 Bajaj Capital Centre for Investment Research

- 4. Stock Idea – Asian Paints Ltd. Industrial coating accounts for ~25% of the Second JV with PPG industries ~Rs 17,000 cr paints segment and has a high Asian Paints approved plans to enhance its fourteen year relationship with PPG Industries Inc, presence of unorganized players. Major USA, to accelerate growth of the non-decorative coatings businesses in India. As part of this organized players in this segment include arrangement, Asian Paints and PPG will enhance their existing non-decorative coatings presence Kansai Nerolac, ICI and Jotun Paints apart in India by expanding their current 50-50 joint venture relationship - Asian PPG Industries Ltd from Asian Paints Industrial Coating Ltd. (APPG) and also establish a second 50-50 joint venture. The modalities are being worked on. The (APICL), a 100% subsidiary of Asian Paints. arrangement is subject to regulatory approval and is expected to be completed during CY2011. APPG currently services the Indian transportation coatings markets and this change will expand its scope to additionally service the marine and consumer packaging markets. The second joint venture will service the industrial containers and light industrial coatings markets. The two joint ventures together will serve all customers for non-decorative products in the Indian market. The JV's would leverage PPG's technology and global customer relationships while continuing to build on Asian Paints' customer base, manufacturing footprint, distribution channels and local relationships. Asian Paints and PPG have agreed that Asian Paints will take the lead in the second venture and PPG will take the lead in APPG in order to utilize their respective strengths to best capture the growth in infrastructure development and the economic boom in India. Geographically diversified The Asian Paints group operates in five regions across the world i.e. South Asia, South East Asia, South Pacific, Middle East & Caribbean through its five corporate brands viz. Asian Paints, Berger International, SCIB Paints, Apco Coatings and Taubmans. The company along with its subsidiaries has operations in 17 countries across the world with 23 paint manufacturing facilities, servicing consumers in 65 countries. It is the largest paint company in eleven countries. International operations: regional sales contribution (FY2010) Middle East Caribbean South Asia South East Asia South Pacific Middle East accounts for the majority of Asian Paints’ international sales 7.0% 7.9% 15.4% 53.6% 16.1% Source: Company International operations: countries Region Countries Middle East Egypt, Oman, Bahrain & UAE Caribbean Barbados, Jamaica, Trinidad & Tobago South Asia Bangladesh, Nepal & Sri Lanka In 9MFY11, International operations accounted for Rs 756.7 cr or ~13% of Asian South East Asia Singapore Paints’ sales. South Pacific Fiji, Solomon Islands, Samoa, Tonga & Vanuatu Source: Company 4 Bajaj Capital Centre for Investment Research

- 5. Stock Idea – Asian Paints Ltd. For 9MFY11, net sales of the company Financial Performance jumped by 19.5% to Rs 5740.6 cr, compared to Rs 4804.2 cr in 9MFY10. Decent Q3FY11 results On a standalone basis, the company posted a growth of 15.6% in its APAT for the quarter ended December 31, 2010 at Rs 206.6 cr as compared to Rs 178.7 cr for the corresponding quarter of the previous year. Its net sales surged by 37.3% at Rs 1754.2 cr, compared to Rs 1277.7 cr for the similar quarter of the previous year due to a robust decorative paints segment. On consolidated basis, the group has posted a APAT attributable to shareholders of Rs 220.3 cr for the quarter ended December 31, 2010 as compared to Rs 198.6 cr for the quarter ended December 31, 2009, rising by 11.0%. Its consolidated net sales has increased 29.6% to Rs 2099.6 cr for the quarter ended December 31, 2010 from Rs 1620.0 cr for the December quarter of 2009. Consensus EPS forecast Financial Year Consensus Forecast FY 2011 94.4 FY 2012 113.9 Net sales performance (consolidated) 2500.0 2099.6 40.0% 1876.8 1830.2 1810.8 2000.0 1723.9 1620.0 30.0% 1422.6 1460.2 1500.0 31.9% 25.2% 25.3% 20.0% 1000.0 22.5% 29.6% 17.5% 16.8% 5.0% 500.0 10.0% The net sales performance of Asian Paints 0.0 0.0% dipped YoY in Q2FY11 due to prolonged Q4FY10 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11 monsoon and delayed festival season, but the sales staged a smart recovery in Q3FY11. Net sales (Rs cr) % increase (YoY) Operating profit performance (consolidated) 500.0 410.2 25.0% 20.0% 334.9 365.5 356.4 364.3 400.0 23.8% 332.5 20.0% 291.4 20.0% 300.0 20.7% 17.7% 19.7% 17.3% 15.0% 188.9 200.0 10.0% 13.3% 100.0 5.0% 0.0 0.0% Q4FY10 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11 Operating profit (Rs cr) Operating margins APAT performance (consolidated) 300.0 268.4 20.0% 250.0 222.2 214.7 220.3 198.4 192.0 15.0% 200.0 176.1 15.6% 150.0 102.2 12.1% 11.9% 10.0% 12.1% 12.2% 10.2% 10.5% 100.0 7.2% 5.0% 50.0 0.0 0.0% Asian Paints is expected to sustain operating Q4FY10 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11 margins at 16-18% levels going forward, aided by strong pricing power and superior APAT (Rs cr) APAT margins product mix (higher proportion of emulsions). 5 Bajaj Capital Centre for Investment Research

- 6. Stock Idea – Asian Paints Ltd. Though the APAT has remained steady for the Paints products: volume growth past few quarters, the APAT margins have shown a dip due to high raw material costs and 500000 20.0% 17.7% 16.8% 411369 higher depreciation. 400000 354370 316871 15.0% 12.1% 241903 282602 16.1% 300000 220284 11.8% 10.0% 187221 12.1% 200000 184622 9.8% 5.0% 100000 1.4% 0 0.0% FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 Production (million tonnes) Growth (YoY) Paints products: sales realization growth 120000 12.0% 98972 97963 100000 84512 87240 90147 10.0% 75771 78946 80634 80000 8.0% 9.8% 4.8% 6.0% 60000 4.2% 3.2% 3.3% 2.1% 4.0% 40000 2.0% 20000 -0.1% 0.0% -1.0% 0 -2.0% FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 Robust performance was seen in the Decorative paint business though the Sales realization/kilo litre (Rs) Growth (YoY) Industrial paint business did not match that performance. Review of Business Segments (Q3FY11) Decorative Business In Q3FY11 the performance was mostly good in all parts of the country. The demand for interior and exterior emulsions was particularly good. The demand for Enamel was higher than anticipated. Industrial business Demand condition for Industrial paints was challenging. Automotive business grew in line with the market. International operations Demand conditions for International business was challenging in some areas. However, South Asia has shown a decent growth. Net Sales & operating income growth was flat in the period April – Dec 2010 compared to 9 months of the previous year. International operations: net sales (Rs cr) Region 9MFY11 9MFY10 Growth Caribbean 123.9 129.7 -4.4% South Asia outperformed. There was growth Middle East 401.7 409.6 -1.9% in South Pacific too. But the Caribbean and Asia 174.8 142.9 22.3% Middle East business was sluggish. South Pacific 56.3 52.4 7.3% 6 Bajaj Capital Centre for Investment Research

- 7. Stock Idea – Asian Paints Ltd. Asian Paints has better margins than its Peer Analysis peers. It also scores over the other paint companies in terms of a high RONW%. Major paint companies: strengths Company Strengths Asian Paints Market leader in the paints industry ICI (Akzo Nobel) Strong in premium end paints/emulsion Berger Paints Focused on enamels and lower end paints Kansai Nerolac Leader in Industrial paints, with half the sales coming from auto industry Nippon Largest paint manufacturer in the world with premium technology. No. 1 in China. Paint industry majors - comparison (standalone financials in Rs cr) Net PBIDTM APATM RONW Mkt Company Sales PAT (%) (%) D/E (%) P/E P/BV Cap Akzo Nobel 1041.7 159.3 12.6 8.6 0.0 16.2 19.4 2.4 2676.2 Berger Paints 1686.5 120.1 11.0 6.6 0.1 22.9 20.9 4.0 2912.0 Kansai Nerolac 1822.0 165.5 14.4 8.4 0.1 23.2 23.4 4.6 4232.0 Asian Paints 5372.7 774.5 20.5 13.4 0.1 58.4 31.0 11.7 24260.6 P/E, P/BV & Mkt Cap figures are for March 25, 2011. Net Sales, PAT, PBIDTM (%), APATM (%) & RONW% statistics are for FY10. On an average, raw materials account for 60% of net sales in the paints industry. Key Concerns Rising price of raw material The paint industry is raw material intensive. These raw materials are of a wide variety. Rising cost and erratic availability of raw material mark the Indian paint industry. Crude derivatives account for about 30-35% of Asian Paint’s raw material costs. Brent crude prices (US$) 115.6 104.0 96.3 91.8 82.9 85.7 76.7 77.8 Crude prices have been in an upswing and this is raising the cost burden of the industry Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 players. Note: March 2011 figures are for the closing on the 25th day of that month. 7 Bajaj Capital Centre for Investment Research

- 8. Stock Idea – Asian Paints Ltd. There is a demand supply gap in case of The input costs have shown a northward trend since Q1FY10 but the surge has been particularly Titanium Dioxide. There is no greenfield harsh in CY2010. Prices of raw materials like titanium dioxide, solvent and crude related inputs capacity on the anvil and it would almost take have increased sharply. a couple of years before a brownfield additional capacity starts operating. Titanium Input cost index dioxide accounts for 20-25% of the total input cost. 103.9 104.5 100.0 98.5 94.4 91.7 92.7 91.4 FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11 Source: Company Slowdown in the economy The well being of the paint industry is dependent on the growth of the economy. 75% of the decorative paints demand comes from repainting and repainting demand depends on how well the Indian economy is doing. Any slowdown in the real estate and the industrial growth impacts the volumes of the paints industry negatively. The crisis in Egypt and Bahrain would impact Asian Paints’ business marginally. Egypt has Advertisement and promotion spends expected to rise going forward two manufacturing facilities and accounts for The competition in the paint industry has intensified with new players entering the Indian market 50-53% of the company’s middle-east This has resulted in an increase in advertisement spend of some companies in this sector. For revenues. Bahrain has one manufacturing unit Asian paints, the advertising and promotion spend has been ~4.5% of its net sales. But on account and contributes 10-12% of the company’s of higher competition and advertisement rate inflation, it may rise in the future. middle-east sales. These two countries together contribute ~4.5% to the net sales of Asian Paints. Valuation Asian Paints is by far the largest paint company in India, with almost one-third of the total market share. It also ranks among the top ten decorative coating companies in the world. With the Indian economy expanding at a fast rate and the housing & infrastructure sectors expected to attract big investments, the paint industry volumes are expected to grow at a healthy 16% in FY12.This bodes well for Asian Paints, the market leader of the industry. The company also has huge expansion plans. After commencing operations at its new facility in Haryana recently, it plans to set up mega projects in Maharashtra and Andhra Pradesh. Asian Paints boasts of an extensive distribution network comprising of 27,000 retailers. The company is fully capable of negating the increase in price of raw materials, by increasing the price of its products. This was amply demonstrated when it raised prices four times in CY2010. Asian Paints is also planning to start its second joint venture with PPG Industries of USA in CY2011. These two JV’s would provide the entire spectrum of paints for the industrial sector. A is also geographically well diversified servicing customers in 65 countries across the globe. . Asian Paints has a market capitalization of Rs 24264.4 cr. and is trading at a share price of Rs. 2529.65. The consolidated TTM EPS is Rs. 94.4 translating into a TTM PE of 26.8. The price to book value stands at 10.1. The stock is an attractive buy considering the growth prospects of the industry as well as the company. We expect the company to register an EPS of Rs 115.9 for FY12 on the basis of strong volume growth and pricing power. This makes the stock currently trade at The demand in the paint industry is seasonal 21.8x FY12. to some extent. While the demand dips in the monsoon season, it is the maximum in the festive season We recommend a “BUY” on the stock with an investment horizon of 9-12 months and target price of Rs. 3014. 8 Bajaj Capital Centre for Investment Research

- 9. Stock Idea – Asian Paints Ltd. SWOT Analysis Strengths Weaknesses • Market leader: Asian Paints is the largest paint • Industrial business performing below par: The company in India with a market share of 32.4%. It is industrial business of the company has performed below also the 3rd largest in Asia and among the top 10 expectations, though the decorative business has done decorative paint companies in the world. very well. The automotive business has performed in • Capacity expansion plans: The company has already line with expectations. Subject to regulatory approvals, commenced its Rohtak operations recently that has a Asian Paints is planning to have a second joint venture capacity of 1.5 lakh kl per annum. In addition to this it with PPG industries. Both the joint ventures would has plans for greenfield expansion of 4 lakh tonnes in cover the entire gamut of the non-decorative paint Maharashtra and 1 lakh tonnes per annum in AP. business. Asian Paints would leverage PPG's technology • Pricing power: Asian paints has had four price hikes in and customer relationships around the globe. CY2010. It intends to raise product prices again if the • Hiccups in international business: The middle east raw material prices keep going northwards. business is being hampered by strife in Egypt & • Manufactures PAN: The company manufactures Bahrain.The Caribbean sales also dipped in Q3FY11. Phthalic Anhydride (PAN), a key raw material. But Asia & South Pacific business has been doing well. • Wide distribution network: Comprising of 90 depots • International presence restricted to small pockets: and 27,000 retailers. Asian Paints need to spread its business to big centres worldwide, to become a true multinational. Opportunities Threats • Fast growing Indian economy: The fast growing • Competition from the world majors: Major world Indian economy and a growth in the realty and players like Jotun, Nippon and Sherwin Williams are construction industries presents a big opportunity for now competiting with Asian Paints in the domestic Asian Paints. Indian markets. • Shorter repainting cycles: The growing affluence of • Competition from the unorganized sector: The the Indian people is resulting in shorter repainting cycles unorganized sector, though fragmented holds a ~35% benefiting the paint industry. share of the Indian paint industry and gives tough • Growth in the tier II and III towns: The paint demand competition to established players. in these towns is growing at a faster rate than the tier I • Rising cost of raw materials: The input costs for Asian cities. Paints and the other players in the industry are rising. • Steady growth in industry volumes: The paint industry The price of crude derivatives and titanium dioxide, two has shown an average volume growth of 15.3% in the key inputs has seen a sharp upswing. past six years and the growth is expected to be 16% in • Slowdown in the economic growth: The paint industry FY12. fortunes are positively co-related to the growth of the • Expected decrease in the use of distemper in future: economy. Increase in enamels & emulsion use would have a • Unstable political situation in middle east: This region positive impact on company's margins. accounts for over 50% of company's international sales. 9 Bajaj Capital Centre for Investment Research

- 10. Stock Idea – Asian Paints Ltd. Financials Income Statement (Quarterly) Consolidated Rs. Cr. Particulars Q3FY11 Q2FY11 Q3FY10 QoQ (%) YoY (%) Net Sales 2099.6 1810.8 1620.0 15.9 29.6 Total Income 2119.0 1835.7 1636.9 15.4 29.5 Total Expenditure 1754.7 1479.3 1302.0 18.6 34.8 PBIDT 364.3 356.4 334.9 2.2 8.8 PBIDT Margin % 17.3 19.7 20.7 Interest 5.9 4.6 7.9 28.3 -26.1 Depreciation 28.6 28.4 19.7 0.8 45.8 Tax 87.9 90.2 92.3 -2.5 -4.7 APAT 220.3 214.7 198.4 2.6 11.0 APATM (%) 10.5 11.9 12.2 Financials (Annual):Consolidated Rs. Cr. 5 yr CAGR 9MFY11 201003 200903 200803 200703 200603 200503 % Share Capital 95.9 95.9 95.9 95.9 95.9 95.9 95.9 Networth 1710.0 1203.2 982.4 777.8 646.3 567.2 Capital Employed 1939.2 1511.8 1257.6 1084.0 907.5 806.7 Debt 229.2 308.6 275.2 306.2 261.3 239.5 CWIP 407.2 92.1 114.2 13.8 33.7 10.6 Inventory 955.9 769.0 714.0 598.0 488.9 454.5 Sundry Debtors 542.5 571.9 460.3 420.6 347.5 295.9 Cash & Bank Balance 105.8 210.4 110.7 105.4 73.4 60.8 Revenues 5740.6 6965.3 5719.0 4590.9 3835.9 3166.9 2673.3 21.1 Total Income 5803.3 7208.5 5802.8 4687.5 3960.1 3209.8 2779.9 21.0 Total Expenditure 4717.1 5831.2 5079.1 3970.6 3445.2 2795.7 2419.9 19.2 PBIDT 1086.2 1377.3 723.7 717.0 514.9 414.2 360.0 30.8 Interest 14.6 36.8 32.5 26.4 24.0 11.4 10.8 27.7 Depreciation 84.0 83.6 74.4 59.2 61.1 60.6 61.4 6.4 APAT 657.2 785.5 395.7 411.3 284.9 211.8 171.3 35.6 Cash Flow from Operating Activities 1058.0 401.9 473.7 252.2 179.2 106.7 Cash Flow from Investing Activities -299.0 -270.1 -334.8 -109.5 -125.0 -73.9 Cash Flow from Financing Activities -331.9 -230.4 -133.6 -110.8 -41.6 -41.9 Free Cash Flows 759.0 131.9 139.0 142.8 54.2 32.9 Dividend % 270.0 175.0 170.0 130.0 125.0 95.0 EPS (Rs.) 68.5 87.6 40.7 41.7 27.6 20.1 17.6 Debt-Equity Ratio 0.2 0.3 0.3 0.4 0.4 0.3 RoNW % 57.3 36.2 45.6 36.7 31.4 29.6 Fixed Asset Turnover Ratio 4.9 4.6 4.3 4.0 3.6 3.1 PBIDT Margin % 18.9 19.8 12.7 15.6 13.4 13.1 13.5 APAT Margin % 11.4 11.3 6.9 9.0 7.4 6.7 6.4 10 Bajaj Capital Centre for Investment Research

- 11. Stock Idea – Asian Paints Ltd. Disclaimer: This document has been prepared by Bajaj Capital Centre for Investment Research (BCCIR), a unit of Bajaj Capital Limited (BCL). BCL and its subsidiaries and associated companies form an integrated unit imparting investment banking, investment advisory and brokerage services in stocks, mutual funds, debt, real estate, personal finance etc. Our research analysts and sales persons provide important input into our investment banking and advisory activities. This document does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data or other sources believed to be reliable. We do not represent that information contained herein is accurate or complete and it should not be relied upon as such. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved). The investment discussed or views expressed may not be suitable for all investors. Affiliates of BCL may have issued other reports that are inconsistent with and reach to a different conclusion from the information presented in this report. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject BCL and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. BCL & affiliates may have used the information set forth herein before publication and may have positions in, may from time to time purchase or sell or may be materially interested in any of the securities mentioned or related securities. BCL and affiliates may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall BCL, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. Any comments or statements made herein are those of the analyst and do not necessarily reflect those of BCL and affiliates. This Document is subject to changes without prior notice and is intended only for the person or entity to which it is addressed and may contain confidential and/or privileged material and is not for any type of circulation. Any review, retransmission, or any other use is prohibited. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. BCL will not treat recipients as customers by virtue of their receiving this report. Equity and securities investments are subject to market risks and there is no assurance or guarantee that the objectives of the investment will be achieved. As with any investment in securities, the share price of a particular company can go up or down depending on the forces and factors affecting the capital markets. Disclosure of interest: 1. BCL and its affiliates do not hold paid up capital of the company. 2. The Analyst and his/her dependent family members do not hold any long or short position in the shares of the company covered as on the date of publication of research on the subject company. © Copyright in this document vests exclusively with BCL. Bajaj Capital Centre for Investment Research Bajaj Capital Ltd 97, Bajaj House, Nehru Place New Delhi 110019 Tel 4169 3000, 4169 2900, Ext. 651 Email: bccir@bajajcapital.com 11 Bajaj Capital Centre for Investment Research