2. 2

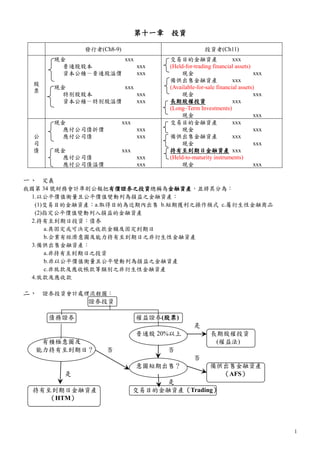

三、 證券投資之分類:

交易目的金融資產 期末採市價法

權益證券 備供出售金融資產 (MV)評價

長期股權投資 權益法(期末「不」作評價)

證券投資

交易目的金融資產 期末採市價法

債務證券 備供出售金融資產 (MV)評價

持有至到期日金融資產 攤銷後成本(期末「不」作評價)

四、 相關會計處理:(課本 p.330 表 11-1)

權益證券(股票) 交易目的金融資產 備供出售金融資產 長期股權投資

1.交易成本(手續費) 當期費用 成本之加項 成本之加項

2.現金股利

Y1:股利收入

Y2 以後:股利收入

Y1:資本退回

Y2 以後:股利收入

資本退回

3.投資收益 無 無 有

4.期末(12/31) MV(損益表) MV(股東權益) 不作評價

債務證券(債券) 交易目的金融資產 備供出售金融資產 持有至到期日金融資產

1.交易成本(手續費) 當期費用 成本之加項 成本之加項

2.是否攤銷折、溢價 否 是 是

3.期末(12/31) MV(損益表) MV(股東權益) 不作評價

*上述表格中的「交易成本」為購買時之交易成本。

交易成本(1)購買時:(a)交易目的:當期費用

(b)其他(備供出售、持有至到期日、長期股權):成本之加項

(2)處分時:皆為售價之減項淨售價=售價-交易成本

五、 長期股權投資

乃投資公司擁有被投資公司之股權,而對被投資公司有某種的決策影響力。長期股權投資按其對被投

資公司決策之影響力,可分為三級:

種類 投資股份 會計處理 收到股利 期末調整

有控制力 投股>50%者

採權益法

及編製合併報表

視為資本退回。

按約當持股比例

認列投資收益

有影響力 投股 20%~50% 採權益法 視為資本退回。

按約當持股比例

認列投資收益

無重大

影響力

投股<20% 市價法

交易目的:為股利收入。

備供出售:第一年為清算股利,

之後為股利收入。

無

所謂權益法,係指投資公司長期股權投資之帳面價值,隨被投資公司股東權益之增減變化而變動。

<例 1>選擇題-自行練習

1. Trading investments are reported on the balance sheet at their _________ value.

A. market B. investment C. market or investment D. book 答:A

2. All trading securities are classified as:

A. current assets. B. long-term assets. C. equity securities. D. available-for-sale securities. 答:A

3. When a company sells a trading investment, the gain or loss on the sale is reported in the:

A. revenues section of the income statement.

B. short-term investments section of the balance sheet.

C. other revenue, gains, and losses section of the balance sheet.

D. other revenue, gains, and losses section of the income statement. 答:D

3. 3

4. Trading securities purchased in 2008 for $85,000 were valued at $80,000 on December 31,

2008.The securities were sold at the beginning of 2009 for $83,000. The 2009 income

statement should report a(n):

A. realized loss of $2,000.

B. realized gain of $3,000.

C. unrealized loss of $5,000 and a realized gain of $3,000.

D. unrealized gain recovered of $3,000. 答:B

08 年 12/31 BV=MV=$80,000 09 年損益=$83,000-$80,000=利益$3,000

5. Trading securities are reported on the balance sheet at:

A. original purchase price. B. current market value.

C. amortized cost. D. historical cost adjusted for investment income. 答:B

6. 有關備供出售金融資產之金融商品未實現損益,應如何處理?

(A)列於資產負債表中之流動負債 (B)列於損益表中之其他損益項下

(C)列為股東權益項下 (D)列為資產負債表中保留盈餘項下 答:C

7. 在權益法之下,下列何種情況可能導致投資公司帳上「採權益法之長期股權投資」金額的減少?

(A)被投資公司宣告股票股利

(B)被投資公司宣告現金股利,或股票股利時

(C)被投資公司宣告現金股利,或發生虧損時

(D)被投資公司宣告現金,或股票股利,或被投資公司發生虧損時 答:C

股票股利不做分錄

8. 下列對於持有至到期日債券投資的描述,何者正確?

(A)期末評價時所產生的未實現跌價損失應列在損益表

(B)期末評價時所產生的未實現跌價損失應列在資產負債表

(C)買進債券之溢價的攤銷會造成認列之利息收入低於收現數

(D)買進債券之折價的攤銷,應貸記:持有至到期日債券投資折價,借記:利息收入 答:C

溢價攤銷為利息收入之減項,故溢價的攤銷會造成認列之利息收入低於收現數

9. 甲公司指派之人員獲聘為乙公司之總經理,但甲公司僅持有乙公司有表決權之股份百分之十八,

甲公司對乙公司之長期股權投資會計處理應採用:

(A)市價法 (B)成本法 (C)成本市價孰低法 (D)權益法 答:D

10. 甲公司購入乙公司之股票 30,000 股,每股買價為$120,另付佣金千分之 1.5,甲公司係於除息日

前購進,則甲公司應借記「交易目的金融資產」:

(A)$3,605,400 (B)$3,600,000 (C)$3,270,000 (D)$3,275,400 答:B

股數×每股價格=30,000 股×$120=$3,600,000,佣金當費用處理。

11. 甲公司在民國94年1月1日,以$300,000購買乙公司25%之普通股,乙公司94年之淨利為$80,000,

並支付$40,000之現金股利,試問甲公司投資科目在民國94年12月31日之餘額為何?

(A)$290,000 (B)$300,000 (C)$310,000 (D)$320,000 答:C

購買乙公司普通股300,000+乙公司淨利80,000×0.25-乙公司支付現金股利40,000×0.25=310,000

12. 信正公司以$200,000之價格購入8年期,面額$240,000之公司債作為備供出售資產。五年後依面額

售出,信正公司採直線法攤銷該投資之溢折價。則出售該投資時信正公司會發生之損益為:

(A)利益$40,000 (B)損失$15,000 (C)利益$15,000 (D)$0 答:C

售價(面額)240,000-帳面價值225,000=15,000利益

<例 2>

東海公司有關權益證券投資之交易如下,試作相關分錄。

情況(一)權益證券被歸類為「交易目的金融資產」。

情況(二)權益證券被歸類為「備供出售金融資產」。

情況(三)假設 5,000 股為逢甲公司股權之 30%,採權益法處理。

96 年 1/1 以每股$20 購買逢甲公司之股票 5,000 股,並支付手續費$1,000(購買時的交易成本)。

6/1 逢甲公司發放每股$2 之現金股利。

12/31 逢甲公司 96 年之淨利為$100,000,股票之每股市價為$25。

97 年 6/1 逢甲公司發放每股$3 之現金股利。

12/31 逢甲公司 96 年之淨利為$200,000,股票之每股市價為$22。

98 年 3/1 以每股市價$24 出售逢甲公司之股票,交易成本為$1,500(出售時的交易成本)。

(五年後帳面價值)公司債折價購入公司債

(已攤銷折價)

公司債折價

00022500025000200

000255

8

00040

,,,

,

,

=+

=×

8. 8

<例 8>自行練習

(1)As a long-term investment, George Company purchased 5,000 of the 12,500 outstanding voting shares of Bush

Corporation at $10 per share on January 1, 2007. At the end of 2007, Bush reported net income of $30,000 and

declared and paid dividends of $10,000. The market price of the Bush stock at the end of 2007 was $8 per share.

The net balance in George's investment account at the end of 2007 would be: $____.

持股5,000/12,500 = 40% 採權益法 (5,000× $10) + ($30,000 × 40%) - ($10,000 × 40%) = $58,000

(2)On January 1, 2007, as a long-term investment in available-for-sale securities, Ha Company purchased 1,000 of

the 10,000 outstanding voting common shares of Will Corporation at $9 per share. Will reported 2007 net

income of $30,000 and declared and paid cash dividends of $20,000. The market price of the Will stock at the

end of 2007 was $10 per share. The carrying value of Ha's investment at the end of 2007 would be: $____.

持股1,000/10,000 = 10% 用市價法 07年底BV=MV=$10×1,000= $10,000

<例 11>自行練習

On January 31, 2005, Dole Corporation purchased the following shares of voting common stock as long-term

investments in available-for-sale securities. None of these holdings amounted to more than 5% of the respective

company's outstanding voting shares. The accounting period ends December 31.

Stock Cost Market 12/31, 2005 Market 12/31, 2006

Apple Corporation $15,000 $12,000 $14,000

Bell Corporation $13,000 $12,000 $13,000

Dole received cash dividends of $500 from Bell Corporation on January 12, 2007. Give the required journal

entries at the following dates:

(1)January 31, 2005 (2)December 31, 2005 (3)December 31, 2006 (4)January 12, 2007

(1)

備供出售金融資產 28,000

現金 28,000

(3)

備供出售金融資產 3,000

未實現金融資產損益 3,000

(2)

未實現金融資產損益 4,000

備供出售金融資產 4,000

(4)

現金 500

股利收入 500

<例 12>自行練習

On January 1, 2007, Frederich Corporation purchased 7,500 shares of SportTech, Inc. as a long-term

investment for a total of $235,000. The 7,500 shares represent 30% of the outstanding (25,000) shares of SportTech.

Prepare the journal entries for Frederich to record the following transactions and events:

December 31, 2007: SportTech reported net income of $66,000 for 2007.

February 1, 2008: Sold 1,875 of the SportTech shares for $34 per share.

November 1, 2008: Frederich received a $0.90 per share cash dividend from SportTech.

(a)

12/31/07 長期股權投資(Long–Term Investments) 19,800

投資收益(Earnings from Long-Term Investment) 19,800

(b)

2/01/08 現金(Cash) 63,750 =1,875×$34

長期股權投資(Long–Term Investments) 63,700 =(235,000+19,800) ×1,875/7,500

出售投資利得(Gain on Sale of Investment) 50

(c)

11/01/08 現金(Cash) 5,062.50

長期股權投資(Long–Term Investment) 5,062.50=(7,500-1,875)×0.9

<例 13>自行練習

A company paid $500,000 for 12% bonds with a par value of $500,000. The bonds pay 6% interest

semiannually on September 1 and March 1. The company intends to hold the bonds until they mature. Prepare the

journal entries for the following dates and transactions related to this bond acquisition.

(a) Bonds purchased on September 1, 2007. (b) Year-end adjusting entry, December 31, 2007.

(c) Receipt of semiannual interest March 1, 2008. (d) Redemption of the bonds at maturity on August 31, 2017.

(a)

9/01/07 持有至到期日金融資產 500,000

現金 500,000

(b)

12/31/07 應收利息 20,000

利息收入 20,000 =$500,000×0.06×4/6

(c)

3/01/08 現金 30,000 =$500,000×0.06

應收利息 20,000

利息收入 10,000

(d)

8/31/17 現金 500,000

持有至到期日金融資產 500,000