Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Glc Market Matters April 2012[1]

1. APRIL 2012

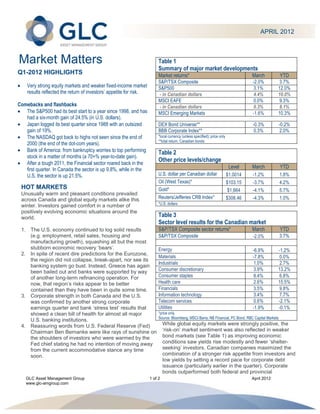

Market Matters Table 1

Summary of major market developments

Q1-2012 HIGHLIGHTS Market returns* March YTD

S&P/TSX Composite -2.0% 3.7%

Very strong equity markets and weaker fixed-income market S&P500 3.1% 12.0%

results reflected the return of investors’ appetite for risk. - in Canadian dollars 4.4% 10.0%

MSCI EAFE 0.0% 9.3%

Comebacks and flashbacks - in Canadian dollars 0.3% 8.1%

The S&P500 had its best start to a year since 1998, and has MSCI Emerging Markets -1.6% 10.3%

had a six-month gain of 24.5% (in U.S. dollars).

Japan logged its best quarter since 1988 with an outsized DEX Bond Universe** -0.3% -0.2%

gain of 19%. BBB Corporate Index** 0.3% 2.0%

The NASDAQ got back to highs not seen since the end of *local currency (unless specified); price only

**total return, Canadian bonds

2000 (the end of the dot-com years).

Bank of America: from bankruptcy worries to top performing Table 2

stock in a matter of months (a 70+% year-to-date gain).

Other price levels/change

After a tough 2011, the Financial sector roared back in the

first quarter. In Canada the sector is up 9.8%, while in the Level March YTD

U.S. the sector is up 21.5%. U.S. dollar per Canadian dollar $1.0014 -1.2% 1.8%

Oil (West Texas)* $103.15 -3.7% 4.2%

HOT MARKETS Gold* $1,664 -4.1% 5.7%

Unusually warm and pleasant conditions prevailed

across Canada and global equity markets alike this Reuters/Jefferies CRB Index* $308.46 -4.3% 1.0%

*U.S. dollars

winter. Investors gained comfort in a number of

positively evolving economic situations around the

world. Table 3

Sector level results for the Canadian market

1. The U.S. economy continued to log solid results S&P/TSX Composite sector returns* March YTD

(e.g. employment, retail sales, housing and S&P/TSX Composite -2.0% 3.7%

manufacturing growth), squashing all but the most

stubborn economic recovery ‘bears’. Energy -6.9% -1.2%

2. In spite of recent dire predictions for the Eurozone,

Materials -7.8% 0.0%

the region did not collapse, break-apart, nor see its

Industrials 1.0% 2.7%

banking system go bust. Instead, Greece has again

been bailed out and banks were supported by way Consumer discretionary 3.9% 13.2%

of another long-term refinancing operation. For Consumer staples 8.4% 6.8%

now, that region’s risks appear to be better Health care 2.6% 15.5%

contained than they have been in quite some time. Financials 3.5% 9.8%

3. Corporate strength in both Canada and the U.S. Information technology 3.4% 7.7%

was confirmed by another strong corporate Telecom services 0.6% -2.1%

earnings quarter and bank ‘stress test’ results that Utilities -1.9% -0.1%

showed a clean bill of health for almost all major *price only

Source: Bloomberg, MSCI Barra, NB Financial, PC Bond, RBC Capital Markets

U.S. banking institutions.

4. Reassuring words from U.S. Federal Reserve (Fed) While global equity markets were strongly positive, the

Chairman Ben Bernanke were like rays of sunshine on ‘risk-on’ market sentiment was also reflected in weaker

the shoulders of investors who were warmed by the bond markets (see Table 1) as improving economic

Fed chief stating he had no intention of moving away conditions saw yields rise modestly and fewer ‘shelter-

from the current accommodative stance any time seeking’ investors. Canadian companies maximized the

soon. combination of a stronger risk appetite from investors and

low yields by setting a record pace for corporate debt

issuance (particularly earlier in the quarter). Corporate

bonds outperformed both federal and provincial

GLC Asset Management Group 1 of 2 April 2012

www.glc-amgroup.com

2. government bonds as investors were happy to reach for Corporate earnings results of banks and insurance

the additional yield. companies exceeded analysts’ expectations

(referred to by analysts as ‘a beat’, as in ‘to beat

THE ODDITIES OF COMMODITIES expectations’).

While the Canadian market maintained a positive quarterly U.S. Financial stocks were undervalued by a large

return, it lagged its global peers. After having outperformed margin and were coming off a very low base.

the U.S. market throughout the financial crisis and in the Strongly tied to economic conditions, financial

early goings of the recovery, the commodity-driven companies are seen to be direct beneficiaries of a

Canadian market is stepping back while the broader-based rosier outlook for the U.S. economy and subdued

U.S. equity market is having its day. With over 46% of the concerns out of Europe.

S&P/TSX concentrated in the Materials and Energy The U.S. ‘bank stress test’ results were positive

sectors, the Canadian S&P/TSX cannot escape its ties to and there were subsequent dividend hikes from

the global commodity market. March’s pull back of oil, bellwether companies such as JPMorgan.

natural gas and gold prices (see Table 2) helped wipe out

all of the Canadian market’s gains for the month, and took OTHER NOTABLES

a big bite out of the quarterly return results (see Table 3). The Consumer Discretionary sector in Canada and the

We’ve highlighted three commodities that played a U.S. also rallied as retail and auto sales showcased a

significant role in the Canadian market this quarter. healthier and more confident consumer, backed by

stabilizing U.S. housing prices and strengthening U.S.

Gold employment figures. Meanwhile the U.S. Information

The continuing flow of positive economic data out of the Technology sector soared as Apple Inc. continues to

U.S. puts pressure on gold prices. It reduces investors’ dominate the tablet market and recently announced the

desire for a safe haven asset, and places the metal in initiation of a quarterly dividend. Apple alone has

competition with a stronger dollar for those still looking for contributed approximately 15% of the total index return in

the safety of high liquidity. the first quarter of 2012.

Natural gas

Natural gas is trading near its 10-yr low as the warmer- SIMPLE AND SMART – LIKE SUNSCREEN

than-average winter led to low demand and a significant A sunny and warm day in the depths of winter is a rarity to

oversupply situation. be relished in Canada. This past winter gave us the

opportunity to enjoy both rising temperatures and rising

Oil equity markets. But if you have a nagging uneasiness that

Concerns about the impact of China’s slowing economic begs the question, ‘If that just happened, what’s next?’-

growth and a stronger U.S. dollar have created a drag on you are not alone. We don’t claim to be able to predict the

oil prices. In addition, preliminary talks out of the U.S., the future anymore than we can predict the weather, but we

U.K., Japan and France about releasing strategic oil will stick to what we do know - taking a diversified

reserves in an effort to moderate the high price of oil has approach to your investments allows you to enjoy what’s

put downward pressure on the price. Having said that, currently hot (like equities) with the moderating effect of

these are not the only factors at play in regard to the what may not be hot at the moment (like fixed income). For

current price of oil. Geopolitical concerns out of the Middle most investors, holding some of both is a comfortable way

East continue to threaten supply chains and provide to reach your long-term investment goals. It’s like

support to the $100+ per barrel price levels we see today. sunscreen – sure it takes discipline, forethought and some

planning, but in the end it’s a simple, smart solution that

has been proven to prevent both short-term pain, and

GIMME THE ‘BEAT’ BOYS long-term damage.

The Financial sector rallied on both sides of the border

with very strong returns. A number of factors contributed:

Copyright GLC, You may not reproduce, distribute, or otherwise use any of this article without the prior written consent of GLC Asset Management Group

The views expressed in this commentary are those of GLC Asset Management Group Ltd. (GLC) as at the date of publication and are subject to

change without notice. This commentary is presented only as a general source of information and is not intended as a solicitation to buy or sell

specific investments, nor is it intended to provide tax or legal advice. Prospective investors should review the offering documents relating to any

investment carefully before making an investment decision and should ask their advisor for advice based on their specific circumstances.

GLC Asset Management Group 2 of 2 April 2012

www.glc-amgroup.com